System On Chip (SoC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

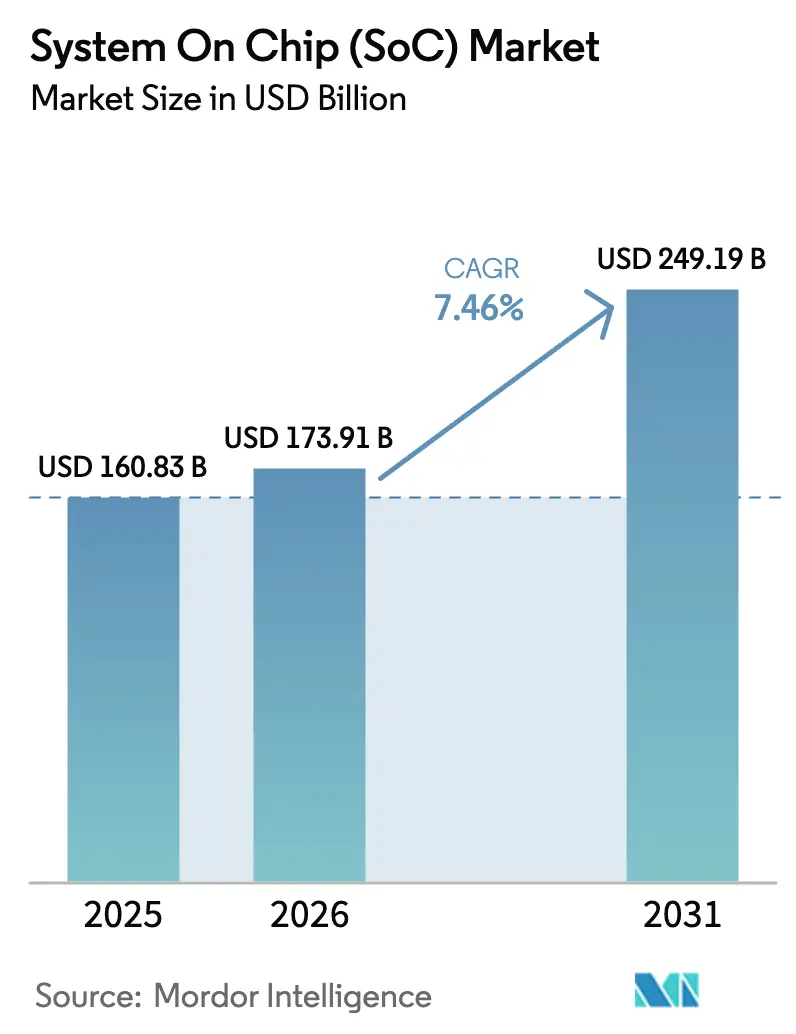

| Market Size (2026) | USD 173.91 Billion |

| Market Size (2031) | USD 249.19 Billion |

| Growth Rate (2026 - 2031) | 7.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

System On Chip (SoC) Market Analysis by Mordor Intelligence

The System on chip market size was valued at USD 160.83 billion in 2025 and estimated to grow from USD 173.91 billion in 2026 to reach USD 249.19 billion by 2031, at a CAGR of 7.46% during the forecast period (2026-2031). Momentum stems from heterogeneous integration that unites logic, memory, radio, and analog blocks on one substrate, enabling higher performance-per-watt for premium phones, centralized vehicle controllers, and hyperscale servers. Sovereign-AI policies in Europe and Asia are pushing device makers to embed on-device inference engines, which boosts demand for fusion-class silicon pairing CPU cores with neural processing units. Automakers are collapsing more than 100 electronic control units into under 10 domain controllers, a direction cemented by General Motors’ 2025 Ultifi announcement that targets a 35-fold AI compute rise by 2028. Foundry investments sparked by the CHIPS and Science Act and similar subsidy packages are adding regional capacity yet labor shortages delay output, keeping pricing power with incumbents.

Key Report Takeaways

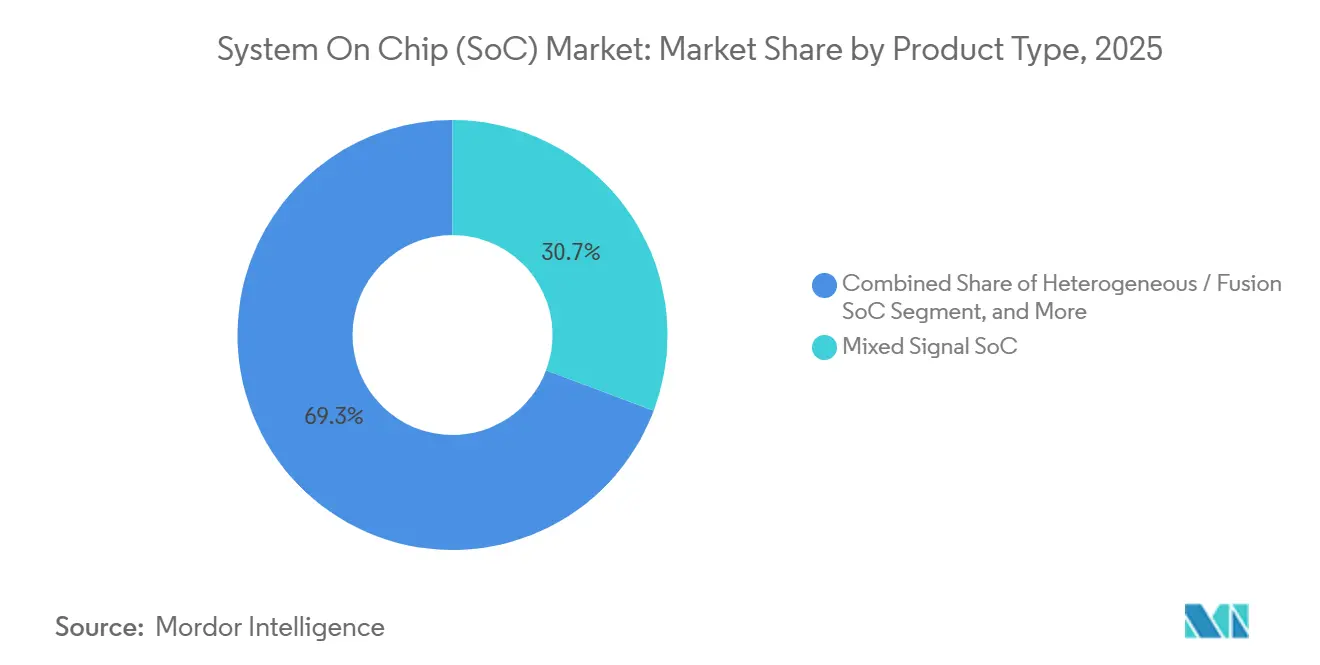

- By product type, mixed-signal devices led with 30.73% of the System on chip market share in 2025, heterogeneous/fusion variants are projected to expand at a 7.83% CAGR through 2031.

- By end-user, consumer electronics commanded 37.81% of 2025 revenue, and automotive usage is forecast to register the fastest 8.03% CAGR to 2031.

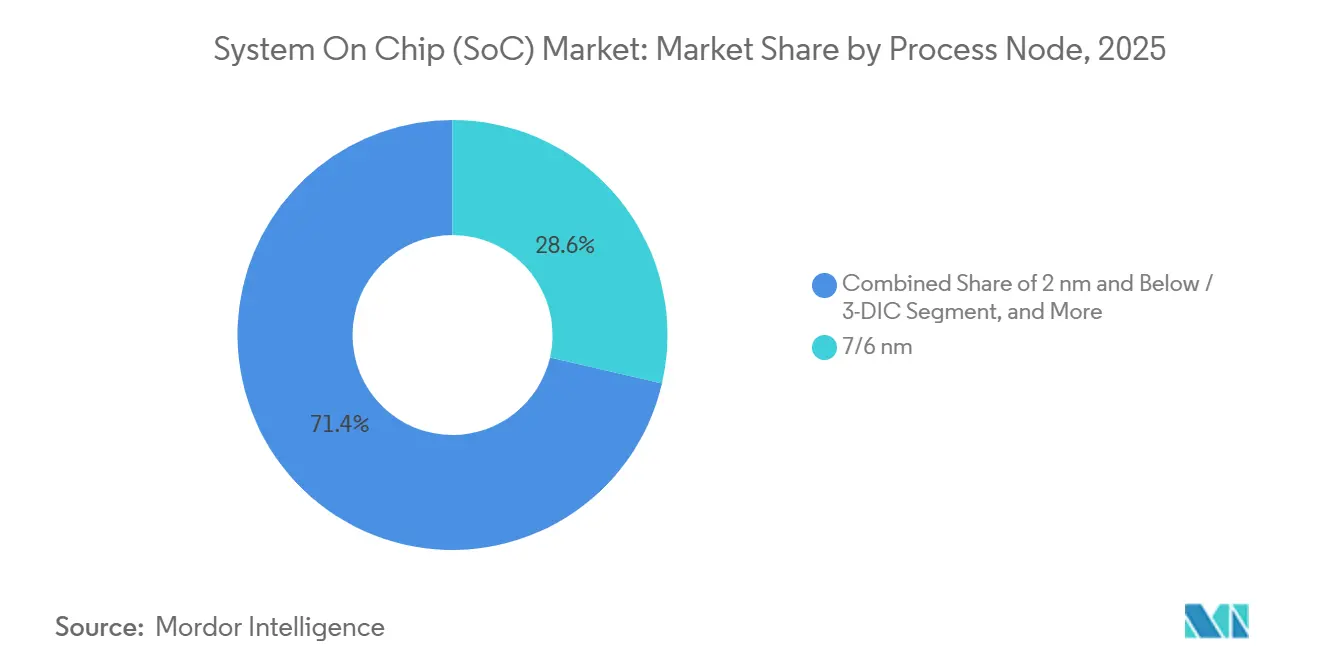

- By process node, 7/6 nm captured 28.62% of 2025 volume, 2 nm and 3-DIC solutions are projected to grow at a 7.62% CAGR over 2026-2031.

- By application, smartphones and tablets accounted for 42.83% of 2025 demand, and edge-AI and IoT devices are advancing at a 7.97% CAGR to 2031.

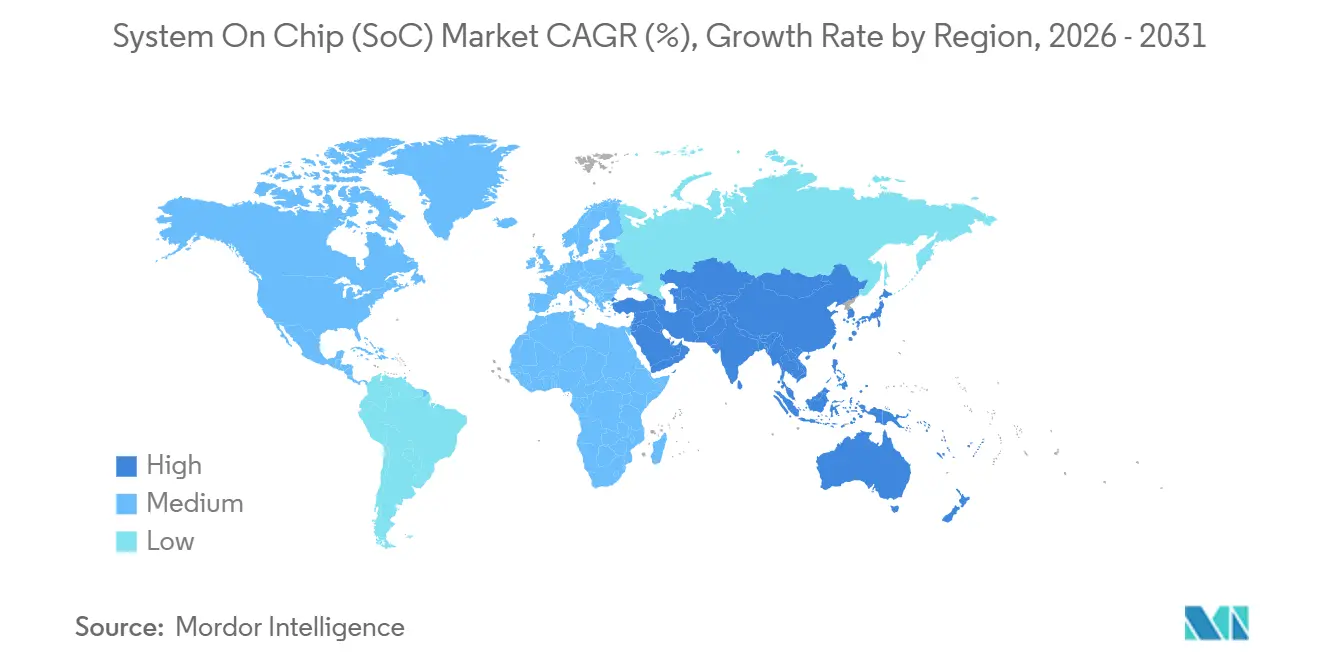

- By geography, Asia-Pacific held 46.92% of 2025 revenue and is set to rise at an 8.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global System On Chip (SoC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring Demand for 5G-Enabled Devices | +1.4% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Rapid IoT and AI-Edge Proliferation | +1.6% | Global, concentrated in APAC and North America | Long term (≥ 4 years) |

| Automotive Shift to Centralized E/E Architectures | +1.5% | Global, strongest in Europe and North America | Long term (≥ 4 years) |

| Subsidy-Fuelled Regional Fab Build-Out | +1.2% | North America, Europe, APAC (India, Japan) | Medium term (2-4 years) |

| Chiplet-Based Heterogeneous Integration Momentum | +0.9% | North America and APAC data center markets | Long term (≥ 4 years) |

| Edge-Native AI Model Inference Needs | +1.3% | Global, with early adoption in APAC and NA | Medium ter |

| Source: Mordor Intelligence | |||

Soaring Demand for 5G-Enabled Devices

Fifth-generation networks require SoCs that integrate RF transceivers, millimeter-wave antenna arrays, and efficient modems capable of sustained gigabit throughput without draining batteries. Global 5G handset shipments exceeded 700 million units in 2025, supporting single-digit growth through 2027 that underpins stable demand for flagship application processors. Qualcomm’s Snapdragon 8 Elite on a 3 nm node integrates a Hexagon NPU rated at 45 TOPS alongside an X80 modem, demonstrating radio-compute convergence in a single die.[1]Qualcomm Investor Relations, “Snapdragon Platform Updates,” qualcomm.com Mid-tier brands are adopting MediaTek Dimensity 9400 to extend 5G into price-sensitive markets. LPDDR5X and UFS 4.0 controllers inside these chips cut latency and power draw, retaining consumer price ceilings. Migration to standalone 5G cores further drives on-device inference, cementing heterogeneous system requirements.

Rapid IoT and AI-Edge Proliferation

Industrial automation, smart cities, and healthcare telemetry deploy billions of endpoints where local inference replaces cloud round-trips.[2]SEMI, “Semiconductor Market Analysis,” semi.org Edge-AI processor revenue is set to climb from USD 5 billion in 2024 to USD 21 billion by 2029, reflecting take-up of vision processors and TinyML microcontrollers. NVIDIA’s Jetson Orin packages an Ampere GPU and Arm CPU in one module that robotics start-ups prize for watt-level efficiency. Wearable glucose sensors and ECG patches rely on mixed-signal silicon that merges analog front ends with low-power controllers. Frameworks such as TensorFlow Lite Micro enable quantized networks on microcontrollers, widening addressable use cases.

Automotive Shift to Centralized E/E Architectures

Tier-1 suppliers are redesigning vehicle electronics around high-performance SoCs instead of dozens of microcontrollers.[3]McKinsey & Company, “Zonal Architecture Adoption Forecast,” mckinsey.com McKinsey expects 30% of new cars to adopt zonal setups by 2032, trimming harness weight and enabling secure over-the-air updates. GM’s Ultifi platform will leverage Snapdragon Ride Flex to deliver 35× more AI compute than legacy systems. NVIDIA Drive Thor, due in 2026 Chinese EVs, supplies 2,000 TOPS and fuses ADAS with infotainment on one package. ISO 26262 certification for chiplet assemblies remains unsettled, delaying mainstream uptake until after 2027.

Subsidy-Fuelled Regional Fab Build-Out

More than USD 150 billion in subsidies across the United States, Europe, Japan, Korea, and India is financing new fabs meant to ease dependence on Taiwan and Korea. TSMC’s USD 40 billion Arizona project will start 4 nm output in late 2026, and Intel’s Ohio complex brings 18A capacity in 2025. Europe’s EUR 43 billion Chips Act prioritizes pilot lines and competence centers for automotive SoCs. India approved Micron’s USD 2.75 billion assembly plant opening in 2026. Worker shortages and equipment delays mean tight supply persists until 2027, sustaining price premiums.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating <5 nm Design and Mask Costs | -0.8% | Global, most acute in North America and APAC | Medium term (2-4 years) |

| Export-Control-Driven Supply-Chain Fragility | -1.1% | Global, concentrated impact on China and APAC | Short term (≤ 2 years) |

| Thermal-Density Limits in High-End SoCs | -0.5% | North America and APAC data center markets | Long term (≥ 4 years) |

| Immature Chiplet Interoperability Standards | -0.4% | Global, affecting data center and automotive | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating <5 nm Design and Mask Costs

Sub-5 nm tape-outs now exceed USD 500 million in non-recurring engineering, with mask sets alone costing up to USD 30 million as EUV layering proliferates. Only hyperscalers and premium phone vendors can absorb such costs, sidelining mid-tier fabless firms. ASML can ship just 20 high-NA EUV tools annually through 2027, creating a tight equipment funnel. Yield lags raise wafer costs and slow automotive qualification, bifurcating the market between cutting-edge and mature-node zones.

Export-Control-Driven Supply-Chain Fragility

Successive U.S. rules ban EUV tools and high-end accelerators from Chinese buyers, capping SMIC at 7 nm and forcing Huawei to rely on N+2 processes. Yield gaps versus TSMC inflate costs and limit Chinese volume. Global suppliers juggle compliance with utilization needs, relocating capacity to North American and European accounts while Chinese demand stays robust. Packaging restrictions on TSV and flip-chip further constrain China to wire-bonded assemblies, lowering performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fusion Designs Propel Value Capture

Mixed-signal silicon captured 30.73% of 2025 revenue because power-management and sensor-fusion blocks are ubiquitous in smartphones, industrial gateways, and automotive body modules. Digital SoCs dominate application processing yet face slower growth as phone replacement cycles stretch. RF/connectivity chips regain momentum from Wi-Fi 7 and Bluetooth 5.4 rollouts. Heterogeneous or fusion devices are expanding at a 7.83% CAGR and are the fastest contributor to the System on chip market size, led by Amazon’s Graviton4 and NVIDIA’s Drive Thor that meld CPUs with domain accelerators.

Second-generation chiplet-based architectures permit combining logic on advanced nodes with analog or I/O dies on cost-efficient processes, cutting both area and leakage. AMD’s EPYC 9005 uses 3 nm compute chiplets around a 4 nm I/O die, raising core counts while controlling thermals. Automotive zonal controllers follow a similar path, attaching ASIL-D certified microcontroller chiplets to AI compute clusters. This fine-grained disaggregation will widen adoption once UCIe interoperability matures, promising broader penetration across the System on chip market.

By End-User Industry: Automotive Leads Growth Vector

Consumer electronics still contributed 37.81% of the 2025 System on chip market share, yet saturation in premium smartphones tempers incremental volume. Data center demand rises as hyperscalers ship custom Arm-based CPUs to curb total cost of ownership, and communications infrastructure absorbs mid-single-digit growth from 5G densification. Industrial and IoT deployments require ruggedized silicon with IEC 61508 compliance to ensure deterministic control in harsh environments.

Automotive revenue is climbing at 8.03% CAGR, the steepest among end-users, as electrification and ADAS mandates push OEMs to software-defined vehicles. A 2026 premium EV will host five to seven high-performance SoCs instead of dozens of microcontrollers, boosting average silicon content per car. Mobileye’s EyeQ Ultra delivers 176 TOPS for Level 3 autonomy, and NXP’s S32 platform underpins zonal body controllers slated for Volkswagen and BMW models. Continued regulatory emphasis on functional safety and upgradeable features safeguards long-run automotive demand within the System on chip market.

By Process Node: Advanced Nodes Sustain Premium Pricing

The 7/6 nm class retained 28.62% of 2025 revenue, balancing performance and die cost for flagship phones and mid-range ADAS. Mature 28 nm platforms remain indispensable for power management and vehicle body chips that demand decade-long lifecycles. Foundries are adding 28 nm automotive-grade capacity to support these needs.

Conversely, 2 nm and below nodes will expand at a 7.62% CAGR, fueled by TSMC’s N2 gate-all-around deployment in 2026 and Intel’s 18A in 2025. Gate-all-around nanosheets offer 10-15% speed gains or 25% power cuts versus 3 nm, allowing Apple’s future M-series to extend single-threaded leadership. Three-dimensional stacking that pairs logic with HBM3E sustains AI accelerators such as AMD’s MI325X, aligning with data center appetite for high-bandwidth memory.

By Application: Edge-AI Devices Outpace Legacy Segments

Handsets and tablets still generated 42.83% of 2025 value, yet shipment plateauing keeps growth muted. Data center silicon demand benefits from AI-centric workloads migrating from GPUs to custom CPUs like Microsoft’s Cobalt 100, trimming power by 40% for web services. Automotive cockpit consolidation places Snapdragon Digital Chassis across 30 automakers for 2026 launches.

Edge-AI and IoT devices will record the quickest 7.97% CAGR, reflecting smart cameras, industrial gateways, and wearables executing inference locally. Google’s Tensor G4 inside Pixel 9 showcases on-device generative models for photography and translation. Industrial robots depend on Renesas R-Car Gen 4 that integrates real-time Ethernet with Arm Cortex-R52 for sub-millisecond control loops. These trends ensure sustained diversification of the System on chip market beyond smartphones.

Geography Analysis

Asia-Pacific retained 46.92% of 2025 revenue and is projected to rise at an 8.08% CAGR to 2031 as Taiwan and Korea maintain leading-edge capacity and China expands domestic 7 nm output despite equipment curbs. Samsung is scaling 3 nm gate-all-around in Pyeongtaek, while SMIC’s N+2 process reaches 60% yield, supporting Huawei’s Kirin 9000S and select automotive chips. India positions itself as a back-end hub; Micron’s USD 2.75 billion Gujarat plant will start assembly-test service in 2026, and Tata Electronics’ 28 nm fab opens in 2027.

North America captured roughly 28% of 2025 turnover, anchored by Apple’s device volumes and hyperscale AI clusters from Amazon, Microsoft, and Google. Seventeen new fabs under the CHIPS Act—including TSMC Arizona and Intel Ohio—will lift regional output, but engineer shortfalls push high-volume production past 2026. Intel’s foundry unit has 18A commitments from Microsoft and the U.S. Department of Defense pending node qualification in late 2025.

Europe generated around 18% of 2025 revenue, with Germany, France, and the Netherlands hosting automotive Tier-1 suppliers and mixed-signal fabs. The EU Chips Act funds pilot lines rather than full-scale GAA fabs, making the region a competence center for 28 nm automotive chips instead of smartphone flagships. STMicroelectronics and GlobalFoundries are jointly expanding 28 nm capacity in France and Germany under long-term supply contracts with European automakers.

Competitive Landscape

The System on chip market features moderate concentration; the top 10 vendors held roughly 60% of 2025 revenue. Apple, Samsung System LSI, and Huawei HiSilicon leverage vertical integration to tailor silicon to proprietary ecosystems, while fabless leaders Qualcomm, MediaTek, and NVIDIA compete through aggressive node adoption and broad developer support. Apple’s 3 nm M4 and A18 chips deliver desktop-class CPU performance in sub-20 W envelopes and deepen macOS/iOS tight coupling. Qualcomm’s royalties on Snapdragon modems create funding for R&D yet face discount pressure as Chinese OEMs adopt MediaTek Dimensity chipsets.

RISC-V cores are gaining share as SiFive’s P870 challenges Arm’s Cortex-A78 with lower licensing overhead. Data-center SoCs increasingly rely on chiplet approaches; AMD’s 192-core EPYC 9005 uses 3 nm compute dies around a 4 nm I/O hub connected by Infinity Fabric. Standards consolidation lags, and fewer than 10% of 2025 tape-outs used UCIe for die-to-die links. TSMC’s CoWoS packaging capacity is a bottleneck for NVIDIA’s Blackwell GB200, and the foundry is investing USD 5 billion to triple advanced-packaging output by 2026.

Regulatory certifications favor incumbents; ISO 26262 for automotive and IEC 62443 for industrial cybersecurity extend design cycles for newcomers. Start-ups such as Tenstorrent and Ayar Labs target niches—open-source AI cores and optical I/O chiplets respectively—but must clear multiyear safety and reliability hurdles before mainstream adoption.

System On Chip (SoC) Industry Leaders

-

Broadcom Inc.

-

Intel Corporation

-

MediaTek Inc.

-

Microchip Technology Inc.

-

NXP Semiconductors NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: TSMC confirmed Arizona Fab 21 will begin 4 nm production in Q4 2026, aided by USD 6.6 billion CHIPS Act grants and USD 5 billion loans.

- January 2025: Qorvo unveiled the QPG6200L SoC for smart-home hubs with <1 µA sleep current and tri-radio Matter, Zigbee, and BLE support.

- January 2025: Intel announced 18A design-rule check completion for external customers, with volume production slated for Q4 2025.

- December 2024: Broadcom announced FY 2024 AI infrastructure revenue of USD 12.2 billion in its investor release and crossed the USD 1 trillion valuation mark.

Global System On Chip (SoC) Market Report Scope

System-on-a-chip refers to a type of integrated circuit (IC) design that combines many or all high-level function elements of an electronic device onto a single chip instead of using separate components mounted to a motherboard, as is done in traditional electronics design. The components that an SoC generally looks to incorporate within itself include a central processing unit, input and output ports, internal memory, and analog input and output blocks, among other things.

The System On Chip Market Report is Segmented by Product Type (Digital SoC, Analog SoC, Mixed-Signal SoC, RF/Connectivity SoC, Heterogeneous/Fusion SoC), End-User Industry (Consumer Electronics, Communications Infrastructure, Automotive, Computing and Data Center, Industrial and IoT, Healthcare and Medical Devices), Process Node (≥28 nm, 16/14 nm, 10/8 nm, 7/6 nm, 5/4/3 nm, 2 nm and Below/3-DIC), Application (Smartphones and Tablets, Edge-AI and IoT Devices, Servers and Data Centers, Automotive ADAS/Infotainment, Industrial Automation, Wearables and Smart Home), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Digital SoC |

| Analog SoC |

| Mixed-Signal SoC |

| RF / Connectivity SoC |

| Heterogeneous / Fusion SoC |

| Consumer Electronics |

| Communications Infrastructure |

| Automotive |

| Computing and Data Center |

| Industrial and IoT |

| Healthcare and Medical Devices |

| ≥28 nm |

| 16/14 nm |

| 10/8 nm |

| 7/6 nm |

| 5/4/3 nm |

| 2 nm and Below / 3-DIC |

| Smartphones and Tablets |

| Edge-AI and IoT Devices |

| Servers and Data Centers |

| Automotive ADAS/Infotainment |

| Industrial Automation |

| Wearables and Smart Home |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Digital SoC | |

| Analog SoC | ||

| Mixed-Signal SoC | ||

| RF / Connectivity SoC | ||

| Heterogeneous / Fusion SoC | ||

| By End-user Industry | Consumer Electronics | |

| Communications Infrastructure | ||

| Automotive | ||

| Computing and Data Center | ||

| Industrial and IoT | ||

| Healthcare and Medical Devices | ||

| By Process Node | ≥28 nm | |

| 16/14 nm | ||

| 10/8 nm | ||

| 7/6 nm | ||

| 5/4/3 nm | ||

| 2 nm and Below / 3-DIC | ||

| By Application | Smartphones and Tablets | |

| Edge-AI and IoT Devices | ||

| Servers and Data Centers | ||

| Automotive ADAS/Infotainment | ||

| Industrial Automation | ||

| Wearables and Smart Home | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What revenue did system-on-chip suppliers book in 2025?

Sales reached USD 160.83 billion.

How much could total revenue climb by 2031?

Forecasts point to USD 249.19 billion, implying a 7.46% CAGR between 2026 and 2031.

Which geographic region is projected to post the quickest growth?

Asia-Pacific shows an 8.08% CAGR outlook as new capacity in Taiwan, Korea, and China scales up.

Which end-use segment is expanding the fastest?

Automotive electronics lead with an 8.03% CAGR as centralized domain controllers replace dozens of legacy modules.

What process node captures the greatest near-term upside?

The 2 nm and below class is set to rise at a 7.62% CAGR once gate-all-around technologies hit volume in 2026.

Why are heterogeneous or fusion devices attracting investment?

Chiplet-based fusion designs grow at a 7.83% CAGR because they couple CPUs with domain accelerators for AI and networking while optimizing cost and thermals.

Page last updated on: