Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

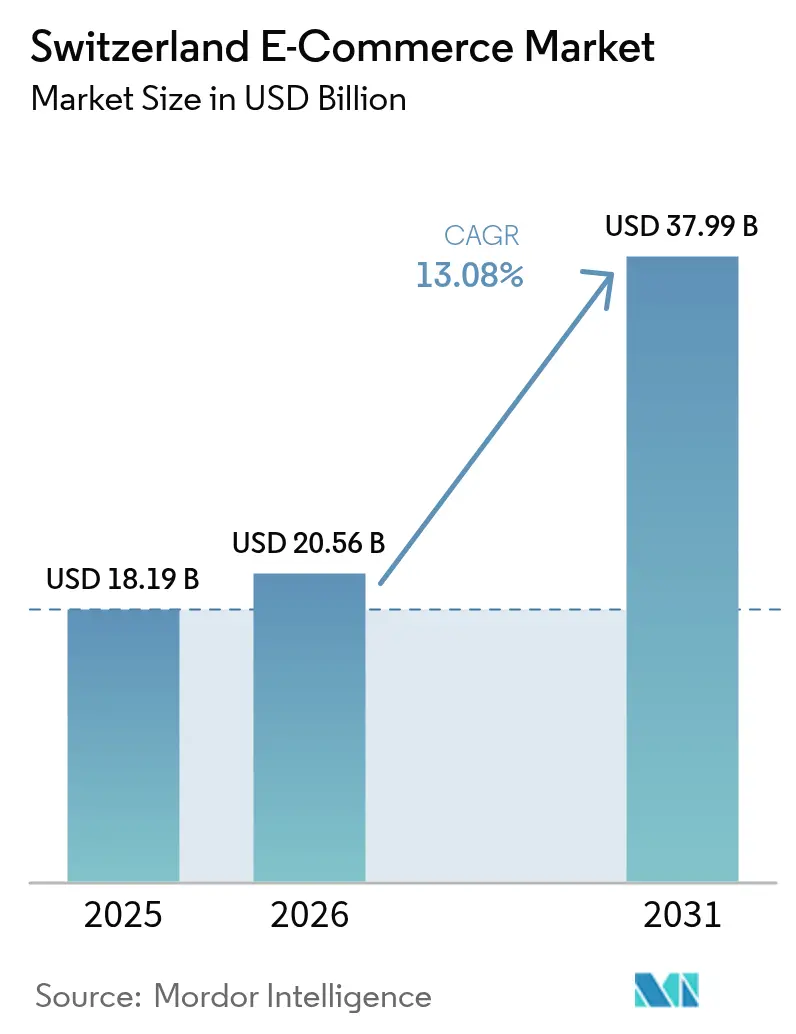

| Base Year Market Size (2025) | USD 18.19 Billion |

| Market Size (2026) | USD 20.56 Billion |

| Market Size (2031) | USD 37.99 Billion |

| Growth Rate (2026 - 2031) | 13.08% CAGR |

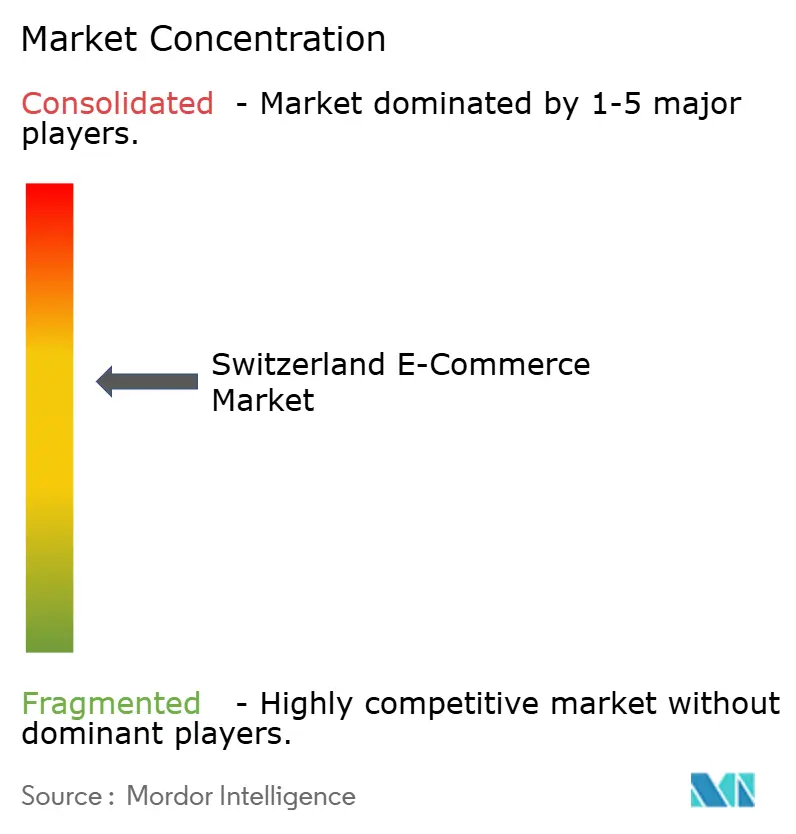

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland E-Commerce Market Analysis by Mordor Intelligence

The Switzerland e-commerce market size is expected to grow from USD 18.19 billion in 2025 to USD 20.56 billion in 2026 and is forecast to reach USD 37.99 billion by 2031 at 13.08% CAGR over 2026-2031. This growth trajectory is anchored in nationwide fibre coverage, 5G rollout, and some of the world’s highest disposable incomes, which together raise average basket values and reduce price sensitivity. The 2024 abolition of industrial duties for authorised importers has expanded cross-border supply, trimming landed costs and accelerating sales from neighbouring countries.[1]Asendia, “Warum sich der Onlineversand in die Schweiz gerade jetzt lohnt,” asendia.de Mobile-first behaviour is deepening, with smartphones handling 60.03% of 2024 online checkouts, while wearables and smart speakers introduce hands-free, ambient commerce pathways. Logistics investments by Swiss Post and private couriers now support reliable same-day delivery in major cities, enabling retailers to match consumers’ rising service expectations and maintain loyalty against overseas platforms. At the same time, heightened privacy laws constrain data-driven personalisation, forcing merchants to balance compliance with the need for tailored experiences in an increasingly competitive arena.

Key Report Takeaways

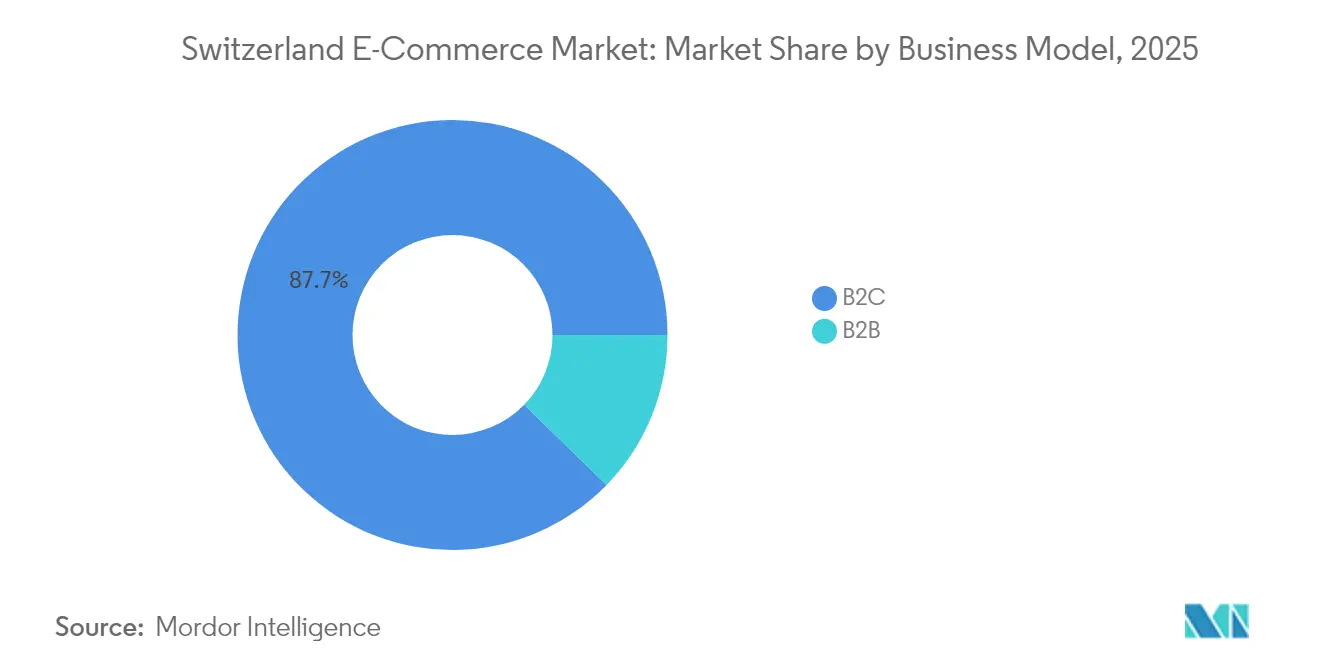

- By business model, B2C accounted for 87.72% of the Switzerland e-commerce market share in 2025, while B2B records the highest projected CAGR at 14.78% through 2031.

- By device type, smartphones captured 59.62% of the Switzerland e-commerce market size in 2025; other device types are forecast to advance at an 17.62% CAGR between 2026-2031.

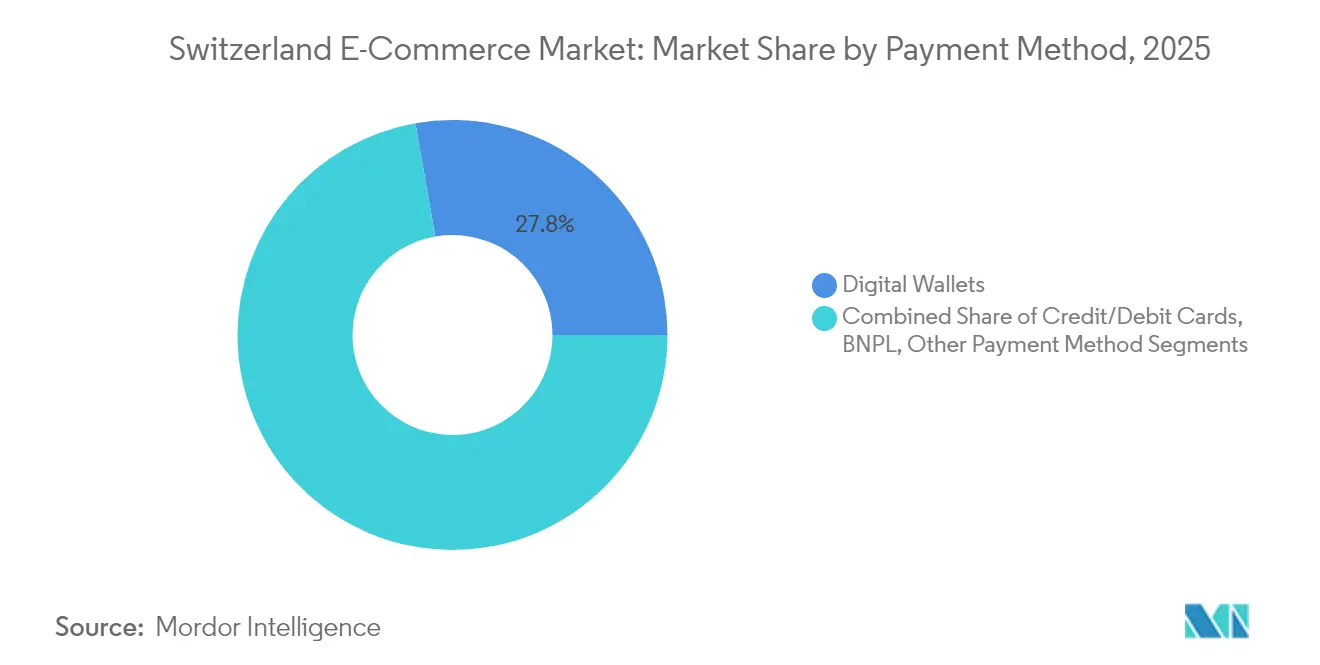

- By payment method, digital wallets held 27.76% share in 2025, whereas Buy Now Pay Later (BNPL) is expected to grow at 18.94% CAGR to 2031.

- By B2C product category, Fashion & Apparel led with a 23.74% revenue share in 2025; Food & Beverages is projected to expand at a 15.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland E-Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cross-Border E-Commerce Adoption Fuelled by Language & Currency Compatibility | +2.7% | National, with stronger impact in border cantons (Basel, Geneva, Ticino) | Medium term (2-4 years) |

| Accelerated Same-Day Logistics Infrastructure Deployment by Swiss Post & Private Couriers | +2.0% | Urban centers (Zurich, Geneva, Basel), with gradual expansion to secondary cities | Short term (≤ 2 years) |

| High Per-Capita Disposable Income Driving Premium Online Shopping | +3.4% | National, with concentration in German-speaking cantons | Long term (≥ 4 years) |

| Government-Backed Digital Identification (E-ID) Enhancing Checkout Conversion | +1.3% | National, with early adoption in tech-forward urban areas | Medium term (2-4 years) |

| Growing Penetration of Mobile P2P Payments (Twint) Boosting Mobile Commerce | +2.4% | National, with higher impact in German and French-speaking regions | Short term (≤ 2 years) |

| Tourism Rebound Increasing Online Pre-Trip Purchases of Swiss Goods | +1.1% | Tourist destinations (Zurich, Geneva, Lucerne, mountain resorts) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cross-Border E-Commerce Adoption Fuelled by Language & Currency Compatibility

The Switzerland e-commerce market benefits from seamless linguistic and currency overlap with Germany, France, Italy, and Austria. Removal of industrial import duties in 2024 triggered an 18% jump in cross-border orders within one year. Roughly 30% of Swiss households already shop abroad online, a share soaring near borders where price gaps on identical goods reach 20-30%.[2]A. Burstein, “Cross-border shopping: Evidence and welfare implications for Switzerland,” sciencedirect.com German merchants enjoy an edge through cultural proximity, while domestic players respond by enriching assortments and tightening fulfillment windows to defend share. Over the medium term, continued regulatory simplicity and transparent landed-cost calculators are expected to amplify foreign brand penetration, especially in consumer electronics and fashion.

Accelerated Same-Day Logistics Infrastructure Deployment by Swiss Post & Private Couriers

Swiss Post is channeling CHF 1.5 billion (USD 1.9 billion) into parcel capacity by 2030, doubling throughput and adding 1,500 jobs. A CHF 11 million (USD 13.90 million) Rümlang hub already sorts 5,000 parcels per hour.[3]Parcel and Postal Technology International, “Swiss Post opens parcel center,” parcelandpostaltechnologyinternational.com Private provider FIEGE complemented this with a 17,000 m² fulfilment centre near Zurich Airport featuring Autostore robotics. Concentrated urban coverage now supports same-day delivery for platforms such as Galaxus, whose 2023 rollout elevated conversion rates among premium electronics buyers. Faster delivery narrows the experiential gap between domestic and foreign sellers, raising the service bar for the Switzerland e-commerce market.

High Per-Capita Disposable Income Driving Premium Online Shopping

Average Swiss online spend reached EUR 1,548 (USD 1,674) in 2024. Galaxus leveraged this purchasing power to report CHF 2.744 billion sales in 2023, up 13.1% despite a declining non-food retail segment. Affluence lifts demand for quality, provenance, and sustainability—traits that enable Swiss retailers to differentiate against lower-cost marketplaces. Luxury, high-end electronics, and niche organic groceries therefore capture disproportionate wallet share, underpinning long-term growth expectations.

Government-Backed Digital Identification (E-ID) Enhancing Checkout Conversion

After revising its initial proposal, the federal government is pilot-testing a state-issued electronic identity to simplify age verification and high-value transactions. Full rollout is slated for 2026, with architecture interoperable under the EU Digital Identity Regulation. Retailers anticipate lower cart abandonment for regulated goods and smoother cross-border verification. While adoption will depend on consumer trust post-2021 referendum rejection, early sandbox feedback indicates a favorable user experience, positioning E-ID as a medium-term conversion catalyst.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Foreign VAT & Customs Thresholds Increasing Basket Abandonment for Imports | -1.6% | National, with higher impact on cross-border purchases | Medium term (2-4 years) |

| High Parcel Delivery Costs in Alpine & Rural Cantons Limiting Merchant Margins | -1.3% | Alpine regions (Valais, Graubünden) and rural cantons | Long term (≥ 4 years) |

| Conservative Consumer Data-Privacy Sentiment Reducing Personalization Uptake | -1.1% | National, with stronger effect in German-speaking regions | Medium term (2-4 years) |

| Fragmented Canton-Level Return Regulations Complicating Reverse Logistics | -0.9% | National, with varying impact based on cantonal regulations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Foreign VAT & Customs Thresholds Increasing Basket Abandonment for Imports

Foreign retailers exceeding CHF 100,000 (USD 126397.20) turnover must register for Swiss VAT, adding compliance costs and discouraging smaller entrants. Hidden duties remain a top reason for the 76% of shoppers who abandon cross-border carts. Postal versus commercial customs clearance introduces service variability, favouring established players with Swiss-specific logistics setups. Unless thresholds are harmonised, friction will persist, tempering growth from overseas sellers.

High Parcel Delivery Costs in Alpine & Rural Cantons Limiting Merchant Margins

Low delivery density and mountainous terrain inflate final-mile expenses. Swiss Post’s universal-service mandate sustains coverage, yet surcharges or higher minimum order values prevail for groceries and bulky goods. While fleet electrification reduces fuel costs and supports sustainability targets, fundamental geography continues to erode margins, driving service level disparities versus urban hubs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Segment Accelerates Digital Transformation

B2C dominated 2025 with 87.72% of the Switzerland e-commerce market; nonetheless, B2B is projected to outpace it at a 14.78% CAGR through 2031. Digitec Galaxus B2B AG increased its SKU count by 30% in 2023, targeting corporates that seek transparent pricing and API-based procurement. Mid-sized manufacturers migrate to digital channels to shorten quote cycles and integrate inventory feeds, reinforcing B2B’s structural momentum.

Large enterprises prioritise integration with ERP suites, driving demand for punch-out catalogues and consolidated invoicing. As these capabilities mature, the Switzerland e-commerce market size for institutional purchasing is poised to capture incremental wallet share from traditional distributors. In parallel, the mature B2C arena fends off low-cost entrants such as Temu, prompting incumbents to enhance loyalty programmes and same-day delivery guarantees. Strategic investment in AI-powered content and customer service allows domestic leaders to preserve high-margin niches even as price competition intensifies.

By Device Type: Wearables Disrupt Traditional Shopping Interfaces

Smartphones generated 59.62% of 2025 orders, underscoring mobile’s central role in the Switzerland e-commerce market. Voice-enabled shopping via smart speakers and purchase journeys initiated on smartwatches are expanding at an 17.62% CAGR, the fastest among devices. Emerging IoT concepts such as replenishment buttons on connected appliances introduce subscription-like revenue streams and reduce basket friction.

Retailers now allocate design budgets to responsive PWA interfaces that render efficiently on small screens and watchOS complications. Desktop retains relevance for high-consideration products, yet session share continues to shift toward pocketable devices. Context-aware offers that blend geolocation, biometric authentication, and real-time stock visibility will differentiate brands as wearable penetration rises. Consequently, the Switzerland e-commerce market size attributed to alternative interfaces is expected to triple before 2030.

By Payment Method: BNPL Disrupts Traditional Payment Hierarchy

Digital wallets accounted for 27.76% of 2025 online spend, led by TWINT’s national reach. BNPL solutions are forecast to grow 18.94% annually, unlocking larger average order values and facilitating discretionary purchases among younger cohorts. International providers enter via merchant plug-ins that require minimal integration, sparking price competition on fees.

Credit cards remain indispensable for cross-border sales owing to fraud insurance features, whereas invoice-based settlement still appeals to older demographics. Payment orchestration platforms therefore gain traction by routing transactions dynamically to the most cost-efficient rail. As regulatory guidelines on consumer credit tighten, transparent disclosure and soft credit checks will be critical to sustain BNPL adoption without reputational backlash in the Switzerland e-commerce industry.

By B2C Product Category: Food & Beverages Reshape Online Retail

Fashion & Apparel commanded the largest 2025 share at 23.74%, with Zalando holding an estimated 10% slice of apparel turnover. However, Food & Beverages is accelerating at a 15.98% CAGR, driven by last-mile temperature-controlled networks and pandemic-induced habit shifts. Discount grocer Aldi’s entry challenged incumbent duopoly Migros and Coop, prompting dynamic fee structures based on postcode.

Consumer electronics sustain robust volumes due to standardised specifications and low return rates, while Beauty & Personal Care recorded 30% sales growth at Galaxus during 2023. Furniture’s online share reached 17% in 2023, yet bulky returns remain a profitability hurdle. Toys and DIY categories exhibit counter-cyclical resilience, benefiting from stay-at-home leisure trends. The diversified mix reduces single-category risk and supports steady expansion of the Switzerland e-commerce market.

Geography Analysis

German-speaking cantons generate the majority of online GMV, reflecting both population size and entrenched digital habits. French-speaking regions outperformed in 2023, aided by Galaxus’ targeted marketing and expanded fulfilment footprint. The Italian-speaking south exhibits the highest cross-border exposure, with 69% of shoppers purchasing from Chinese marketplaces.

Border areas leverage physical pick-up points in Germany and France to bypass Swiss delivery fees, a behaviour intensified after the 2015 franc surge. The 2024 duty removal magnified this effect, pushing cross-border online sales up 18% year-on-year. Conversely, Alpine cantons confront extended delivery times that dampen conversion for fast-moving consumer goods. Swiss Post’s parcel-centre programme aims to narrow this gap by situating hubs closer to mountain valleys.

Urban agglomerations such as Zurich, Geneva, and Basel enjoy sub-same-day service, fostering impulse purchasing and reinforcing brand stickiness. As electrified fleets and micro-depots expand, carbon-neutral delivery messaging further resonates with environmentally conscious Swiss consumers. Collectively, regional nuances compel merchants to localise language, logistics, and pricing tactics to fully monetise the Switzerland e-commerce market.

Competitive Landscape

The Switzerland e-commerce market features a moderately concentrated hierarchy where Amazon, Galaxus, and Zalando together oversee 27.9% of revenue. Amazon leverages Prime logistics and broad assortment, yet faces higher customs duties that erode its price advantage. Galaxus counters through domestic warehousing, Swiss-compliant returns, and a marketplace model that added 1.4 million SKUs in 2023. Zalando sustains dominance in apparel via convenient returns and curated fashion campaigns.

Chinese entrants Temu and Shein deploy aggressive discounting, assisted by global direct-from-factory supply chains. Temu amassed 4.6% share within two years, overtaking several local mid-tier shops. In response, Swiss retailers upscale loyalty schemes, extend private-label lines, and champion sustainability credentials. AI-enabled search, automated product photography, and chatbots raise operational efficiency and personalise engagement despite privacy constraints.

Niche platforms flourish in verticals such as second-hand luxury, ethical beauty, and regional delicacies, reflecting consumer appetite for provenance and exclusivity. Several are exploring subscription commerce for replenishment categories, providing predictable cash flow and tighter customer lock-in. M&A activity may accelerate as incumbents acquire speciality players to solidify ecosystem breadth and defend the Switzerland e-commerce industry against international incursions.

Switzerland E-Commerce Industry Leaders

Digitec Galaxus AG

Amazon.com, Inc.

Nestlé Nespresso SA

Zalando SE

Brack.ch AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Swiss Post reported a 4.2% rise in parcel volumes while letters fell 4.6%. The operator is investing in video consultations and electrifying its PostBus fleet to sustain e-commerce profitability; the move strengthens rural service reliability and reinforces brand trust.

- March 2025: A University of St. Gallen study ranked Amazon, Galaxus, and Zalando as the three most-used platforms. The benchmarking encourages local players to differentiate on Swiss-specific service attributes to defend share.

- January 2025: Ringier Advertising’s “Digital Commerce” feature reported Zalando’s acquisition of About You and growing AI investment at Digitec Galaxus. Integration of data science underlines the strategic pivot toward relevance algorithms in the Switzerland e-commerce market.

- November 2024: The Universal Postal Union noted domestic parcel volumes surpassing 40 billion globally, with Switzerland ranking in the top performance tier. High service quality continues to underpin consumer confidence.

Switzerland E-Commerce Market Report Scope

The internet trade of goods and services is known as e-commerce (or electronic commerce). These commercial dealings are either B2B (business-to-business), B2C (business-to-consumer), or C2C (consumer-to-consumer). A more recent business model is known as "direct-to-consumer" (D2C), allowing brands to sell directly to consumers. The internet is what drives e-commerce. Consumers use their devices to access an online store to browse the selection and place orders for goods or services.

The Switzerland E-Commerce Market is Segmented by B2C E-Commerce (by application [beauty & personal care, consumer electronics, fashion & beverage, furniture & home, others (toys, DIY, media, etc.]]) and by B2B E-Commerce. The report offers market forecasts and size in value (USD) for all the above segments.

By Business Model

| B2C |

| B2B |

By Device Type

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method

| Credit / Debit Cards |

| Digital Wallets |

| BNPL |

| Other Payment Method |

By B2C Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories |

| By Business Model | B2C |

| B2B | |

| By Device Type | Smartphone / Mobile |

| Desktop and Laptop | |

| Other Device Types | |

| By Payment Method | Credit / Debit Cards |

| Digital Wallets | |

| BNPL | |

| Other Payment Method | |

| By B2C Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories |

Key Questions Answered in the Report

What is the current value of the Switzerland e-commerce market?

It stands at USD 20.56 billion in 2026 and is projected to rise to USD 37.99 billion by 2031.

Which product category is growing the fastest online?

Food & Beverages is expanding at a 15.98% CAGR due to improved cold-chain delivery and changing consumer habits.

How dominant are mobile devices in Swiss online shopping?

Smartphones account for 59.62% of transactions, and alternative devices such as wearables are rising at an 17.62% CAGR.

Why is BNPL important in Switzerland?

BNPL solutions are forecast to grow at 18.94% CAGR, making high-ticket items more accessible and diversifying payment choice.

Who are the leading e-commerce platforms?

Amazon, Galaxus, and Zalando together hold nearly 28% of sales, while Temu is the fastest-growing newcomer with 4.6% share.

How will the national E-ID influence online retail?

The planned 2026 rollout should streamline identity verification, lower cart abandonment, and support cross-border commerce once fully adopted.

Page last updated on: