Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

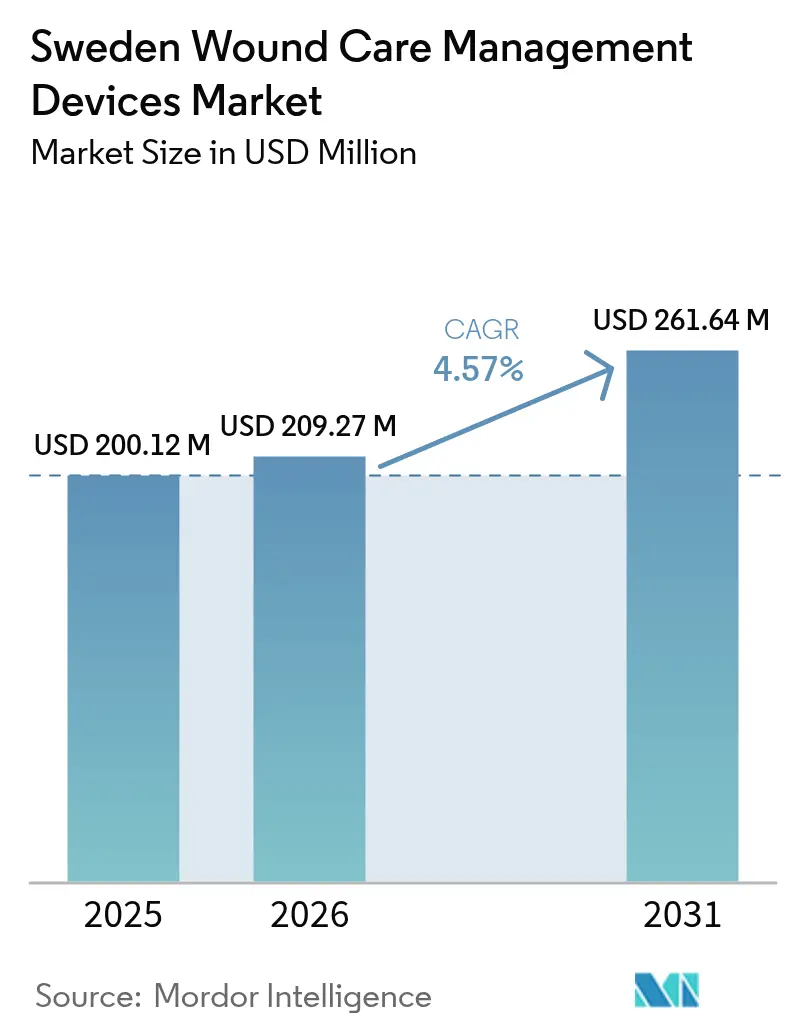

| Base Year Market Size (2025) | USD 200.12 Million |

| Market Size (2026) | USD 209.27 Million |

| Market Size (2031) | USD 261.64 Million |

| Growth Rate (2026 - 2031) | 4.57% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sweden Wound Care Management Devices Market Analysis by Mordor Intelligence

The Sweden wound care management devices market size is expected to grow from USD 200.12 million in 2025 to USD 209.27 million in 2026 and is forecast to reach USD 261.64 million by 2031 at 4.57% CAGR over 2026-2031. Robust public funding, region-level autonomy, and aggressive environmental targets are reshaping clinical practice and procurement, pushing hospitals and municipalities toward bio-based dressings, rental models for negative-pressure therapy, and AI-guided triage. Sweden’s 21 regions now pool purchasing power while still tailoring formularies to local needs, creating price transparency but also intense evidence demands. Home-care nurses are taking on more complex wounds, driving telemedicine adoption and propelling the Sweden wound care management devices market toward connected solutions that reduce travel and hospitalization. Chronic-wound prevalence tied to diabetes and obesity keeps advanced dressings at the center of spending, yet fast growth in elective surgery spurs rising demand for closure devices. A parallel push to cut single-use plastics nudges suppliers toward circular-economy packaging, further influencing the Sweden wound care management devices market trajectory.

Key Report Takeaways

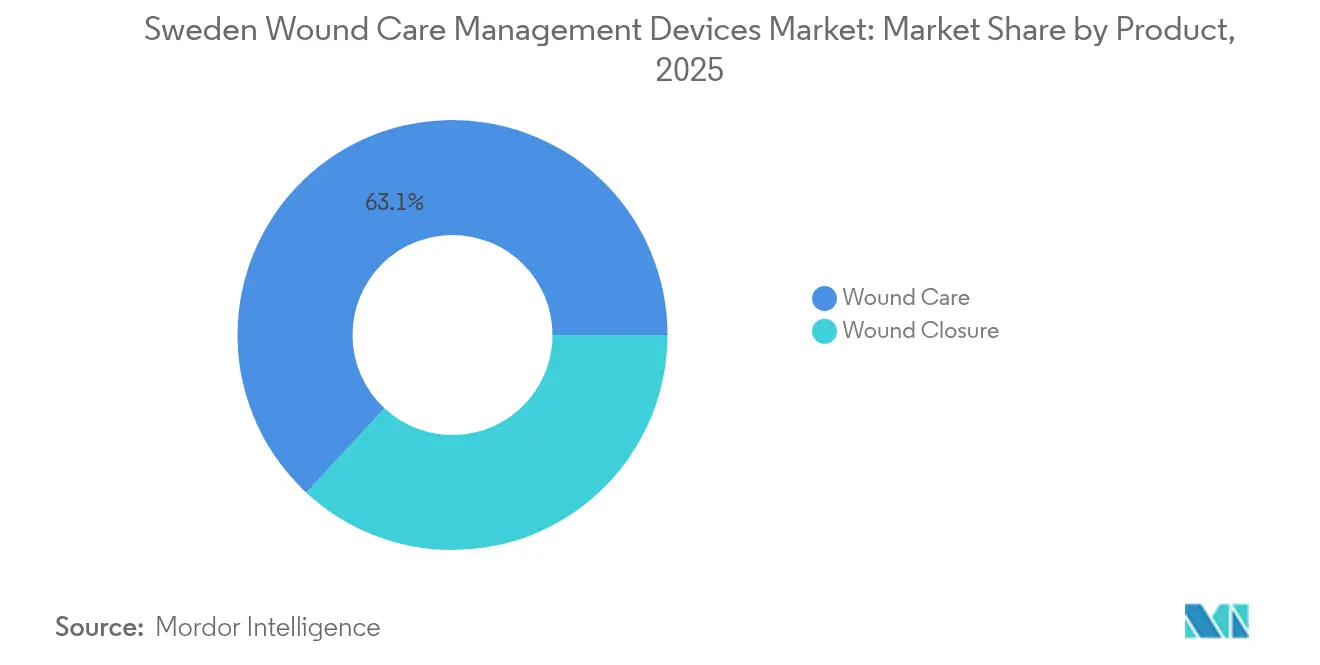

- By product, wound care products led with 63.10% of Sweden wound care management devices market share in 2025, while wound closure solutions are projected to post the fastest 5.21% CAGR through 2031.

- By wound type, chronic wounds accounted for 60.00% of total cases in 2025; acute wounds are set to expand at a 5.48% CAGR through 2031.

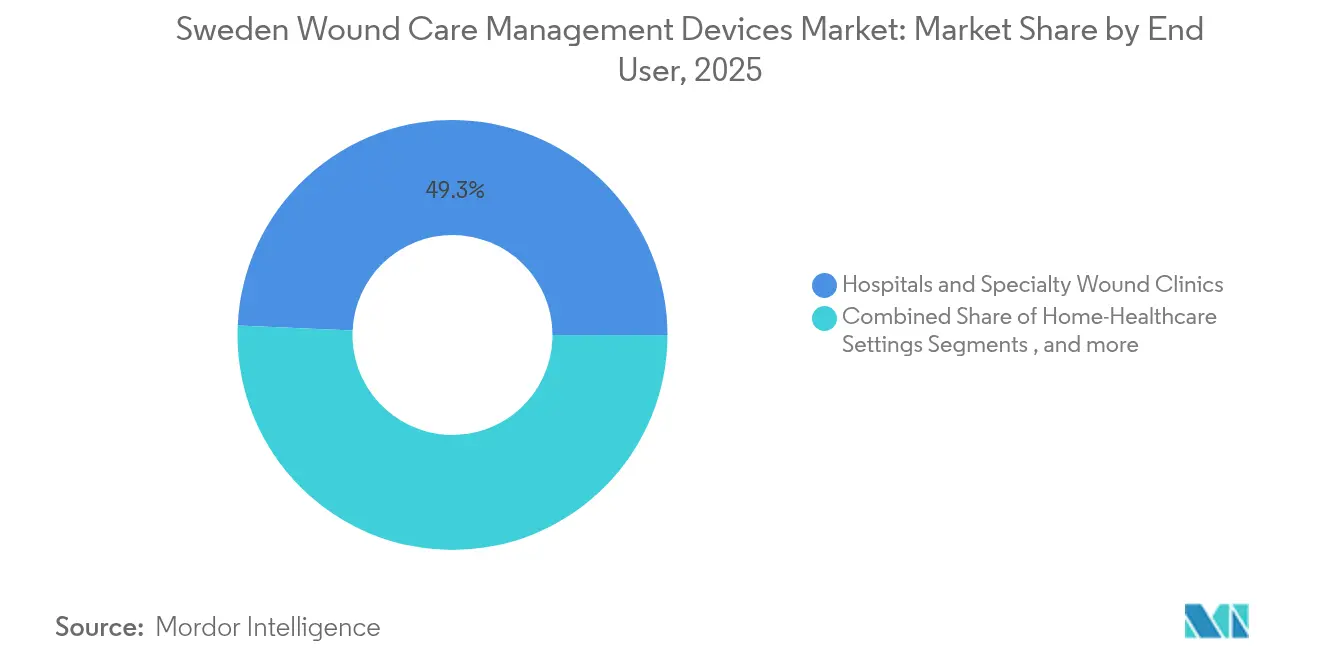

- By end user, hospitals and specialty wound clinics held 49.30% Sweden wound care management devices market share in 2025, whereas home healthcare is the swiftest climber at 5.33% CAGR.

- By mode of purchase, institutional procurement captured 64.50% of spending in 2025; retail and over-the-counter channels are advancing at a 5.29% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising chronic-wound incidence linked to diabetes & obesity | +1.2% | National, urban clusters | Long term (≥ 4 years) |

| Growing volume of elective & trauma surgery | +0.8% | University hospitals nationwide | Medium term (2-4 years) |

| Favourable reimbursement for advanced dressings | +0.6% | National, region-level variation | Short term (≤ 2 years) |

| Adoption of AI-enabled digital imaging in primary care | +0.4% | Stockholm & Gothenburg pilots | Medium term (2-4 years) |

| Carbon-reduction tenders favour bio-based dressings | +0.3% | Region Scania first mover | Long term (≥ 4 years) |

| Home-based NPWT rental models in municipal care | +0.4% | Municipal systems country-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Chronic-Wound Incidence Linked to Diabetes & Obesity

Sweden’s diabetes surveillance programs now detect metabolic markers decades before diagnosis, revealing four clinically distinct diabetes subtypes that influence ulcer healing rates [1]Tatjana P. Liedtke, "Characterizing trajectories of diabetes-related health parameters before diabetes diagnosis in diabetes subtypes: analysis of a 20-year long prospective cohort study in Sweden," Cardiovascular Diabetology, cardiab.biomedcentral.com. Registry data show that delayed treatment lengthens healing durations, prompting municipalities to subsidize early, home-based negative-pressure wound therapy (NPWT). Rental NPWT kits cut hospital bed-days and improve quality of life, accelerating uptake across the Sweden wound care management devices market. Manufacturers able to link dressings to continuous glucose monitors meet growing demand for personalized protocols.

Growing Volume of Elective & Trauma Surgical Procedures

University hospitals report high adoption of closed-incision NPWT, trimming surgical-site infections by 47% and cutting dressing-change labor in vascular and orthopedic units. Expansion of 3D surgical planning at Sahlgrenska University Hospital underscores Sweden’s commitment to precision surgery, thereby boosting need for smart closure materials that conform to complex anatomies. Gender-specific infection data from coronary artery bypass surgery drive protocol differentiation and fuel demand for algorithm-guided dressings [2]Charlotte Stor Swinkels, "Preclinical paired noninferiority study comparing in-house and commercially available 3D planning for corrective osteotomy of the distal radius," Scientific Reports, nature.com.

Favourable Reimbursement for Advanced Dressings in Sweden

TLV’s rigorous health-economic reviews create clear reimbursement pathways for novel dressings that shorten healing time or nurse visits, pushing global suppliers to anchor launches in Stockholm before wider EU roll-out. Regional purchasing consortia amplify price discipline yet reward proven value, so companies supplying silicone-based super-absorbents with validated labor savings gain rapid formulary access across the Sweden wound care management devices market.

Adoption of AI-Enabled Digital Wound-Imaging in Primary Care

District nurses cite training gaps in complex wound staging, leaving room for AI-guided imaging that offers real-time depth and exudate analysis. Pilot apps in Stockholm achieve near-expert segmentation accuracy, though clinicians demand transparent algorithms and seamless electronic-record integration. Teleconsults using AI-tagged images now bridge specialist shortages in sparsely populated northern counties, supporting broader decentralization of the Sweden wound care management devices market [3]Davide Griffa, "Artificial Intelligence in Wound Care: A Narrative Review of the Currently Available Mobile Apps for Automatic Ulcer Segmentation," MDPI, mdpi.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict MDR/IVDR conformity assessment delays | -0.7% | EU-wide, Swedish submissions | Short term (≤ 2 years) |

| Pricing pressure from regional buying alliances | -0.5% | High-volume regions nationwide | Medium term (2-4 years) |

| Skill gap in advanced wound nursing outside universities | -0.4% | Rural & municipal settings | Long term (≥ 4 years) |

| Environmental tax on single-use plastics | -0.3% | National, Nordic expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict MDR/IVDR Conformity Assessment Delays

Medical Device Regulation transitions stretch to 2028 for lower-risk classes, and Swedish notified bodies face capacity bottlenecks that can stall launch timelines by up to 18 months. Larger incumbents absorb audit costs, while start-ups postpone EU entry or seek strategic partnerships, tempering short-term product diversity in the Sweden wound care management devices market.

Pricing Pressure from Regional Purchasing Alliances

Sweden’s 21 regions increasingly negotiate as blocs, demanding lifetime cost proofs instead of unit prices, compressing margins but sparking value-based contracting models. Suppliers tie reimbursement to healing-time benchmarks and readmission rates, a shift echoing across the Sweden wound care management devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Advanced Technologies Drive Wound Care Dominance

The wound care products segment captured 63.10% Sweden wound care management devices market share in 2025, underscoring its status as the clinical workhorse for chronic ulcers. Advanced foams, super-absorbents, and antimicrobial hydrofibers lengthen change intervals, translating to lower community-nursing labor and aligning with region-level cost-containment goals. Negative-pressure systems supplement, rather than replace, high-performance dressings, and rental programs now cover half of municipal NPWT deployments. Traditional gauze persists in emergency rooms for rapid bleeding control, but silicone-coated options lessen adhesion trauma, boosting patient satisfaction.

Wound closure solutions are on track for a 5.21% CAGR through 2031 as minimally invasive surgery gains momentum in orthopedics and cardiology. Smart staplers with real-time compression feedback reduce leak complications, while bio-absorbable sealants appeal to surgeons aiming to limit foreign-body load. The Sweden wound care management devices market size for closure solutions is projected to climb steadily as 3D-planned reconstructions multiply in university hospitals. Tissue adhesives that polymerize within seconds are becoming standard in pediatric units, shortening theater time and attracting favorable TLV rulings.

By Wound Type: Chronic Complexity Meets Acute Innovation

Chronic wounds represented 60.00% of treated cases in 2025, dominated by diabetic foot ulcers and venous leg ulcers that often exceed 100 days to heal. Self-care education alone shows limited effect, so regions are piloting sensor-embedded compression wraps that alert patients when pressure falls outside therapeutic windows. The Sweden wound care management devices market size for chronic wounds is expected to edge upward as the diabetic population ages, yet unit spending is capped by aggressive tendering.

Acute wounds exhibit the stronger growth trajectory at 5.48% CAGR as trauma centers adopt closed-incision NPWT to lower infection risk in hip fracture repairs. Electric-stimulation dressings from university spin-offs triple re-epithelialization speed in burns, a breakthrough now under TLV review. Such innovations expand the clinical reach of the Sweden wound care management devices market, especially in metropolitan emergency departments.

By End User: Municipal Care Transformation Accelerates Home Healthcare Growth

Hospitals and specialty wound clinics retained 49.30% Sweden wound care management devices market share in 2025 thanks to concentrated expertise and advanced imaging infrastructure. University sites double as trial hubs where AI-linked bandages stream perfusion data to cloud dashboards, giving firms real-time evidence for reimbursement submissions. Clinics also refine multidisciplinary protocols combining vascular surgery, endocrinology, and podiatry to cut amputation rates.

Home healthcare is expanding fastest at 5.33% CAGR, propelled by welfare-technology grants that subsidize portable NPWT and Bluetooth-enabled ulcer cameras. District nurses now consult specialists via secure video links, trimming travel hours and carbon emissions. This diffusion of capability is enlarging the Sweden wound care management devices market as municipal budgets shift toward equipment rentals and remote monitoring subscriptions.

By Mode of Purchase: Institutional Procurement Dominance Faces Retail Channel Growth

Institutional procurement flowed through regional alliances that commanded 64.50% of total spending in 2025, enforcing strict life-cycle-cost evaluations that filter out minimally differentiated products. Suppliers must document carbon footprint and packaging recyclability, a hurdle encouraging design revisions throughout the Sweden wound care management devices market.

Retail and over-the-counter channels, though smaller, are advancing at 5.29% CAGR as pharmacies expand wound-care assortments and e-commerce platforms offer home-delivery of dressings approved for self-treatment. VAT relief on device repair services feeds a refurbish-and-reuse niche for NPWT pumps, illustrating how circular-economy rules reshape consumer access.

Geography Analysis

The Sweden wound care management devices market is anchored in Stockholm, Gothenburg, and Malmö, where university hospitals pilot AI-driven decision tools and carbon-neutral supply chains. High procedure volumes in these hubs generate the clinical data required for TLV reimbursement filings, positioning them as early-adopter zones for advanced imaging and smart dressings.

Northern counties with low-population density lean on tele-wound networks that route encrypted images to regional centers, enabling specialist advice within minutes despite vast distances. Portable NPWT kits paired with 4G modems allow home nurses to intervene before infections escalate, expanding the Sweden wound care management devices market beyond traditional hospital walls. Municipalities allocate digital-health budgets to these tools, citing evidence of reduced ambulance transfers and shorter inpatient stays.

Region Scania’s procurement agency is Sweden’s sustainability frontrunner, awarding multi-year tenders to suppliers of bio-based or reusable dressings that meet its carbon-reduction scorecard. Neighboring regions now copy these criteria, accelerating the shift toward plant-fiber absorbents and recyclable closure kits. As such policies spread, they reinforce environmental performance as a competitive lever within the Sweden wound care management devices market.

Regulatory Landscape

Wound care management devices in Sweden operate under the EU Medical Device Regulation (MDR, Regulation (EU) 2017/745) framework. CE marking is the core market-access requirement, and classification is set under MDR Annex VIII based on invasiveness and duration of contact (typically spanning Class I to Class IIb depending on the device and intended use). The Swedish Medical Products Agency, Läkemedelsverket (MPA), acts as the national competent authority for medical-device supervision, market surveillance, and vigilance, rather than providing national pre-market approvals for CE-marked products.

Sweden also supplements EU requirements through national provisions such as SFS 2021:631. For suppliers, day-to-day compliance centers on economic-operator obligations (manufacturer, authorized representative, importer, distributor), post-market surveillance, and incident reporting to the MPA. In 2026, ongoing Eudamed registration requirements are expected to increase supply-chain transparency and traceability for relevant actors, while pricing and reimbursement decisions for wound care products continue to be driven largely by region-level healthcare processes rather than by the MPA.

Competitive Landscape

The Sweden wound care management devices market remains moderately fragmented. Mölnlycke Health Care and Essity AB leverage domestic relationships and deep familiarity with TLV dossiers to secure top positions. Their portfolios span antimicrobial foam to compression systems, and both firms actively pilot bio-based prototypes with Region Scania. International contenders like Solventum and Smith+Nephew gain traction via partnerships that bundle analytics dashboards with dressings, satisfying Swedish demands for outcome proof rather than product features alone.

Success hinges on randomized clinical trials conducted within Swedish registries, allowing suppliers to tie cost savings to local practice patterns. Smaller innovators such as Imago AI focus on ulcer-segmentation algorithms that feed telemedicine workflows, carving out niches despite MDR compliance hurdles. Sustainability remains a strategic differentiator; companies that can certify cradle-to-grave emissions below tender thresholds enjoy scoring bonuses in rubric-based procurements.

Strategic moves increasingly include risk-sharing contracts where suppliers reimburse regions if healing targets are missed. Mölnlycke’s 2025 diabetic-foot pilot in Västra Götaland links dressing costs to ulcer-closure days, setting a precedent other vendors may follow. Meanwhile, Essity’s subscription offering bundles NPWT pump rentals, dressing refills, and cloud analytics for a per-patient monthly fee, illustrating the shift from device sales to service models in the Sweden wound care management devices market.

Sweden Wound Care Management Devices Industry Leaders

-

Smith & Nephew

-

Medtronic Plc

-

Convatec

-

Coloplast

-

Solventum

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Care delivery across Sweden is decentralized across 21 regions and 290 municipalities, which creates room for suppliers to demonstrate total-cost-of-care benefits and align with regional procurement models. Solutions that fit municipal home-care workflows, including portable NPWT programs structured around rentals and service, can complement telemedicine protocols already used to extend specialist coverage into low-density northern counties. They also align with regional documentation requirements tied to labor savings and reduced travel.

A second opportunity is in evidence-led advanced dressings, closure solutions, and adjunct technologies that support value-based procurement criteria while remaining consistent with MDR post-market obligations. In 2026, European-wide rollouts and EU approvals that support advanced wound care platforms, including Smith+Nephew ALLEVYN COMPLETE CARE and Convatec ConvaMatrix, offer near-term pathways into Swedish tenders and formularies when suppliers can package local clinical evidence, maintain robust post-market surveillance, and provide traceability-ready supply documentation (including Eudamed-aligned operator readiness) for region-level review.

Recent Industry Developments

- May 2026: Smith+Nephew highlighted progress in chronic wound care around EWMA 2026, emphasizing ALLEVYN COMPLETE CARE and its RENASYS EDGE topical NPWT platform. The update reinforced the companys effort to combine advanced dressings and NPWT within evidence-led care pathways that fit European hospital and community-wound workflows.

- September 2025: Convatec secured EU regulatory approval for ConvaMatrix, a porcine placenta-derived device positioned for complex and hard-to-heal wounds, with European commercialization steps starting in 2026. The approval expands the range of advanced biologic options available to Swedish regions that increasingly buy based on documented outcomes rather than unit price alone.

- July 2024: Kerecis expanded its silicone fish-skin combination line with the launch of Shield Spiral for wound management. The product broadened the companies portfolio in biologic-derived wound solutions, supporting differentiation in advanced dressing categories where Swedish procurement weighs clinical performance and pathway efficiency.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers spending in Sweden on clinically approved devices and advanced dressings used to protect, close, off-load, or actively manage acute and chronic wounds in clinical care and supervised home settings.

Scope exclusions: We exclude disposable gauze, over-the-counter first-aid kits, purely pharmaceutical creams, and consumer first-aid supplies such as standalone antiseptic solutions.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Topical Agents

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping the Sweden care pathway and payment context, since device demand is closely tied to clinical protocols and procurement rules. We reviewed public sources such as the Swedish National Board of Health and Welfare (Socialstyrelsen), the Swedish eHealth Agency (E-halsomyndigheten), Statistics Sweden (SCB), and the Swedish Medical Products Agency for definitions, care volumes, and regulatory signals.

To turn those signals into usable model inputs, we also used sources such as hospital and regional procurement portals, peer-reviewed clinical guidelines and journals for chronic wound prevalence ranges, and company annual reports and investor presentations for business mix hints. We used select paid subscriptions only for company financial intelligence and patent lookups when public disclosures were thin. These examples are not exhaustive, and we checked other public materials for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys with clinicians involved in wound management, procurement and supply leads, and local distributors who see ordering patterns. These discussions helped confirm what care settings typically buy, how pricing moves with tender cycles, and where utilization is shifting between advanced dressings and device-led therapies.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 16% | |

| Mid tier: 53% | Functional/Unit leaders: 41% | |

| Smaller Players: 17% | Managers: 43% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where treated wound volumes and care-setting activity in Sweden are translated into expected device and advanced dressing consumption, and then priced using typical tender and channel pricing ranges. After that first view was formed, we cross-checked it with selective bottom-up approximations using supplier revenue exposure, sampled average selling prices multiplied by expected unit demand, and distributor channel checks to adjust for gaps.

Key inputs that shaped the model (illustrative) included chronic wound prevalence and treated-patient share, the mix of inpatient versus outpatient and supervised home care, usage patterns for negative-pressure therapy versus dressing-led management, tender timing and price resets, and adoption of advanced dressings for hard-to-heal wounds. When direct bottom-up visibility was missing for smaller categories, we used ratio-based estimates anchored to better-observed therapy groups, then pressure-tested those assumptions using interview feedback.

For forecasting, we applied scenario analysis around a baseline demand path, since yearly growth is influenced by procurement cycles and protocol-driven adoption. Assumptions on wound burden, care shifting, and price progression were reviewed with primary respondents, and the scenario that best matched observed purchasing signals was used for the final forecast path.

Data Validation & Update Cycle

Outputs were validated through multiple checks, including triangulation between demand signals, supply-side sanity checks, and year-over-year variance screens for abnormal jumps. When results looked inconsistent with care setting volumes or known tender outcomes, we revisited assumptions, rechecked source inputs, and re-contacted experts to confirm whether a real market event explained the change.

Before sign-off, analysts review the model in steps to keep calculations, unit logic, and currency handling consistent across the history and forecast. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is done so clients receive the latest updated view.

Mordor Intelligence's Sweden Wound Care Management Devices Market Size Compared With Other Published Estimates

Published market values for Sweden wound care often do not match because each study draws the line differently on what counts as a device market and what sits outside it. Differences also show up when years, currency timing, and the way procurement pricing is treated are not aligned.

The table shows a spread mainly because some sources either narrow the view to wound therapy devices only or broaden it into a wider wound care universe, and then apply different growth or price assumptions. In Mordor Intelligence's model, the number is kept tied to clinically approved wound care management devices and advanced dressings used in licensed care or supervised home settings, while excluding retail first-aid and drug-only products, which shifts the total versus broader consumer-style definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 200.12 M (2025) | |

| Industry Publisher A | USD 186.00 M (2024) | Uses an earlier base year and a broader wound care framing that can mix management devices with adjacent wound care categories, and it does not clearly separate retail first-aid from clinically supervised demand. |

| Databook Publisher B | USD 74.20 M (2023) | Limits scope to wound therapy devices, which removes advanced dressings and other wound management device categories that drive a larger share of routine care spending in Sweden. |

Taken together, the comparison points to scope as the biggest driver, followed by base-year choice and how pricing is handled around tender cycles. By keeping inputs traceable to treated-wound activity and care-setting purchasing, the sizing steps remain repeatable and easier to reconcile with real procurement behavior.

Key Questions Answered in the Report

What is the current value of the Sweden wound care management devices market?

The market is valued at USD 209.27 million in 2026 and is projected to grow to USD 261.64 million by 2031.

Which product segment holds the largest share in Sweden?

Wound care products, primarily advanced dressings, account for 63.10% of the Sweden wound care management devices market share in 2025.

Why is home healthcare the fastest-growing end-user segment?

Municipal welfare-technology funding, portable NPWT rentals, and telemedicine protocols are enabling district nurses to manage complex wounds at home, driving a 5.33% CAGR through 2031.

How do Swedish procurement rules affect suppliers?

Regional alliances demand life-cycle-cost proofs and increasingly award sustainability points, putting pressure on vendors to provide clinical and environmental evidence alongside competitive pricing.

What impact does MDR/IVDR have on market entry?

Extended conformity assessment timelines can delay launches by up to 18 months, favoring established companies with robust compliance systems.

Which emerging technologies are gaining attention in Sweden?

AI-powered wound-imaging apps, bio-based dressings that meet carbon-reduction targets, and smart closure devices linked to data dashboards are rapidly attracting clinical trials and procurement interest.

Page last updated on: