Technology, Media and Telecom

5th MayAccelerating Additive Manufacturing Adoption in India

3 Min Read

Study of Data Center Water Consumption in South Korea Report is Segmented by Source of Water Procurement (Potable Water, Non-Potable Water, Other Alternate Sources), by Data Center Type (Enterprise, Colocation, Cloud Service Providers), and by Data Center Size (Mega, Massive, Large, Medium, Small). The Market Sizes and Forecasts are Provided in Terms of Volume (Billion Liters).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

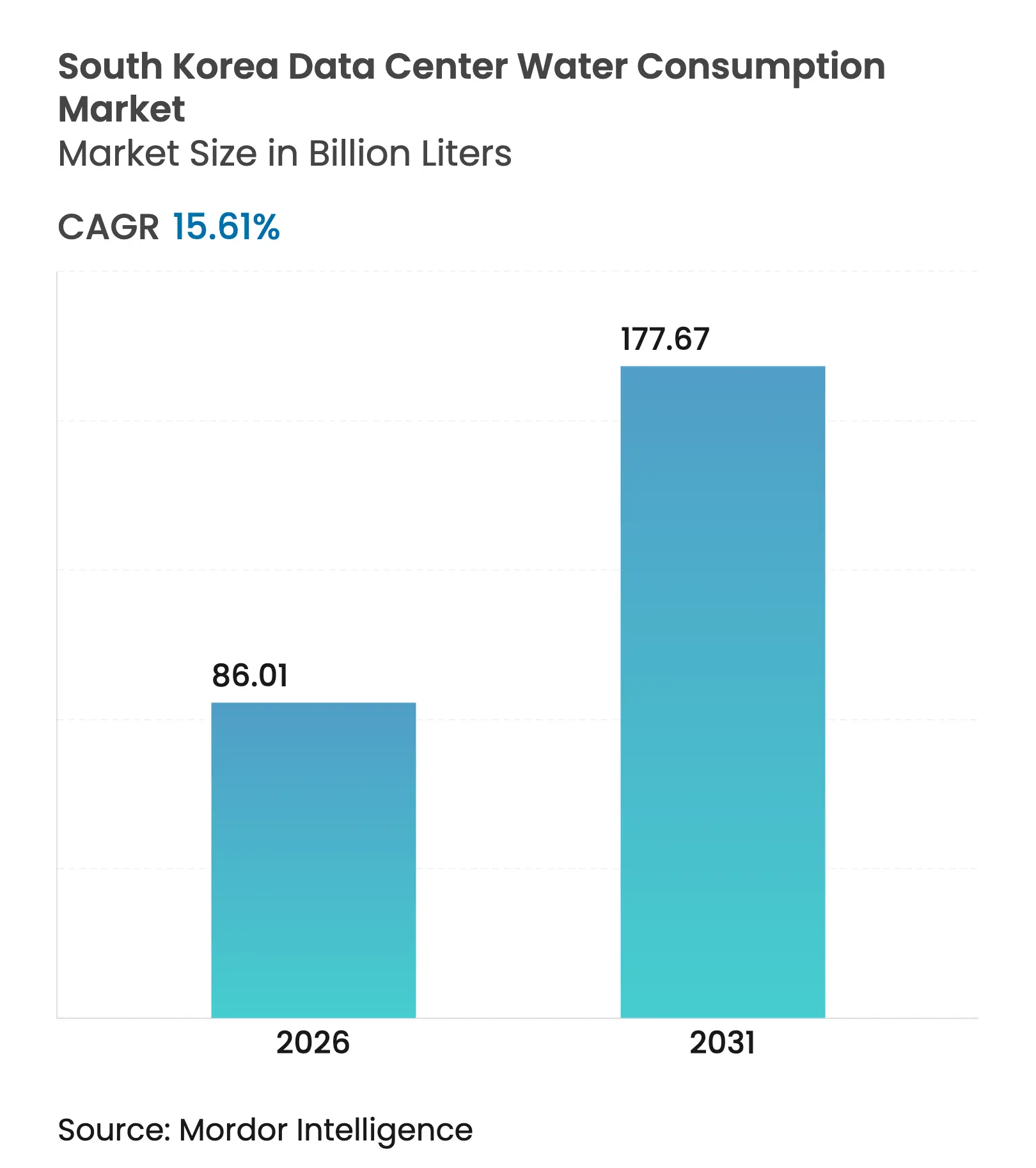

| Market Volume (2026) | 86.01 Billion liters |

| Market Volume (2031) | 177.67 Billion liters |

| CAGR | 15.61 % |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The South Korea data center water consumption market size is expected to grow from 74.40 billion liters in 2025 to 86.01 billion liters in 2026 and is forecast to reach 177.67 billion liters by 2031 at 15.61% CAGR over 2026-2031. Rapid adoption of artificial-intelligence workloads, hyperscaler expansion, and government incentives for digital infrastructure underpin this growth trajectory. Operators are re-engineering cooling architectures to manage higher rack densities while moderating freshwater stress, and municipal authorities are tightening disclosure rules that make Water Usage Effectiveness (WUE) a competitive benchmark. Alternative sourcing of grey- and seawater advances quickly, cloud platforms outpace colocation growth, and mega-scale projects above 50 MW become the new normal as AI clusters consolidate capacity in fewer but much larger halls. Technology partnerships—ranging from two-phase immersion to hydrogen-powered cooling—are reshaping capital-expenditure priorities and encouraging vertical integration between energy, water, and computing assets

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Adoption

of two-phase liquid immersion cooling

Adoption

of two-phase liquid immersion cooling

| +2.8% | Seoul metro, Busan coastal areas | Medium term (2-4 years) | (~) %

Impact on CAGR Forecast:

+2.8%

|

Geographic

Relevance

:

Seoul

metro, Busan coastal areas

|

Impact

Timeline

:

Medium

term (2-4 years)

|

Shift

from potable to grey-/seawater sourcing

Shift

from potable to grey-/seawater sourcing

| +3.2% | Coastal cities, industrial zones | Short term (≤ 2 years) | |||

Government-mandated

WUE disclosure for hyperscalers

Government-mandated

WUE disclosure for hyperscalers

| +1.9% | National, concentrated in Seoul | Short term (≤ 2 years) | |||

Seoul

municipal water-reuse subsidies for ICT parks

Seoul

municipal water-reuse subsidies for ICT parks

| +1.4% | Seoul metropolitan area | Medium term (2-4 years) | |||

AI-optimised

cooling algorithms reducing make-up water

AI-optimised

cooling algorithms reducing make-up water

| +2.1% | Major data center hubs nationwide | Medium term (2-4 years) | |||

Growth

of district-cooling back-up loops

Growth

of district-cooling back-up loops

| +1.6% | Urban centers, industrial complexes | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Adoption of Two-Phase Liquid Immersion Cooling

Two-phase immersion cooling replaces conventional chiller loops by submerging servers in dielectric fluid that vaporizes at low temperature, thereby eliminating large volumes of make-up water previously needed for heat rejection. Korean pilots report Power Usage Effectiveness as low as 1.02 and rack densities surpassing 100 kW per cabinet—figures unattainable with legacy water-cooled systems.[1]Min-Soo Kim, “Immersion Cooling Cuts PUE to 1.02”, Samsung Electronics, samsung.com Commercial deployments accelerate as hyperscalers recognise total energy savings of 30-50% and the regulatory relief that comes from drastically lower water withdrawals in Seoul and Busan.

Shift from Potable to Grey-/Seawater Sourcing

Alternative sourcing addresses rising tariffs and municipal quotas. Coastal campuses channel seawater through titanium-plate exchangers, achieving coefficients of performance near 4.8 and removing freshwater from the equation.[2]David Chernicoff, “Ulsan LNG Cold Energy Project Lowers Water Use”, Light Reading, lightreading.com Greywater reuse spreads in Seoul where tertiary-treated effluent is piped to ICT parks at 60–70% lower cost than potable supply, supported by subsidies that underwrite capital expenditure on ultrafiltration and UV polishing units.

Government-Mandated WUE Disclosure for Hyperscalers

New rules oblige facilities above 20 MW to publish annual WUE in line with ISO/IEC 30134-9:2022, transforming water consumption into a publicly benchmarked metric.[3]ISO Technical Committee 30134, “ISO/IEC 30134-9:2022 Water Usage Effectiveness”, ISO, iso.org Average Korean WUE of 1.8 L/kWh now sits well above international best practice of 0.4 L/kWh, prompting retrofits such as air-side economizers that trim water demand by over 40% during temperate months.

AI-Optimised Cooling Algorithms Reducing Make-Up Water

Machine-learning control loops ingest sensor data to predict thermal loads and modulate set-points every few seconds. Demonstrations at leading cloud sites indicate 56.1% lower energy use and up to 30% reduction in evaporative losses versus static control strategies. By dynamically lifting chilled-water temperatures in cooler seasons, facilities gain additional water savings without sacrificing uptime.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Tightening

groundwater-extraction quotas

Tightening

groundwater-extraction quotas

| -2.1% | National, acute in Seoul metro | Short term (≤ 2 years) | (~) %

Impact on CAGR Forecast:

-2.1%

|

Geographic

Relevance

:

National,

acute in Seoul metro

|

Impact

Timeline

:

Short

term (≤ 2 years)

|

Escalating

wastewater-discharge fees

Escalating

wastewater-discharge fees

| -1.8% | Industrial zones, coastal areas | Medium term (2-4 years) | |||

Public

opposition to mega-DC water draws in coastal cities

Public

opposition to mega-DC water draws in coastal cities

| -1.3% | Busan, Incheon coastal regions | Medium term (2-4 years) | |||

Limited

greywater pipe infrastructure outside Seoul metro

Limited

greywater pipe infrastructure outside Seoul metro

| -0.9% | Secondary cities, rural areas | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Tightening Groundwater-Extraction Quotas

The National Groundwater Monitoring Network shows falling aquifer levels, leading regulators to cap industrial abstraction. New data-center permits now require recharge offsets or alternative supply, forcing builders toward seawater or advanced closed-loop cooling. Operators circumvent restrictions by installing dewatering heat-pump systems that recycle foundation seepage as coolant, improving overall COP by up to 30%.

Escalating Wastewater-Discharge Fees

Fee hikes tied to effluent volume and quality elevate operating costs for blow-down streams that can top 1,000 m³/day in mega-facilities. On-site zero-liquid-discharge skids recover 95% of cooling water through reverse osmosis and crystallisers, but raise energy consumption 15–25%, challenging ROI calculations.

By Source of Water Procurement: Alternate Supplies Gain Ground

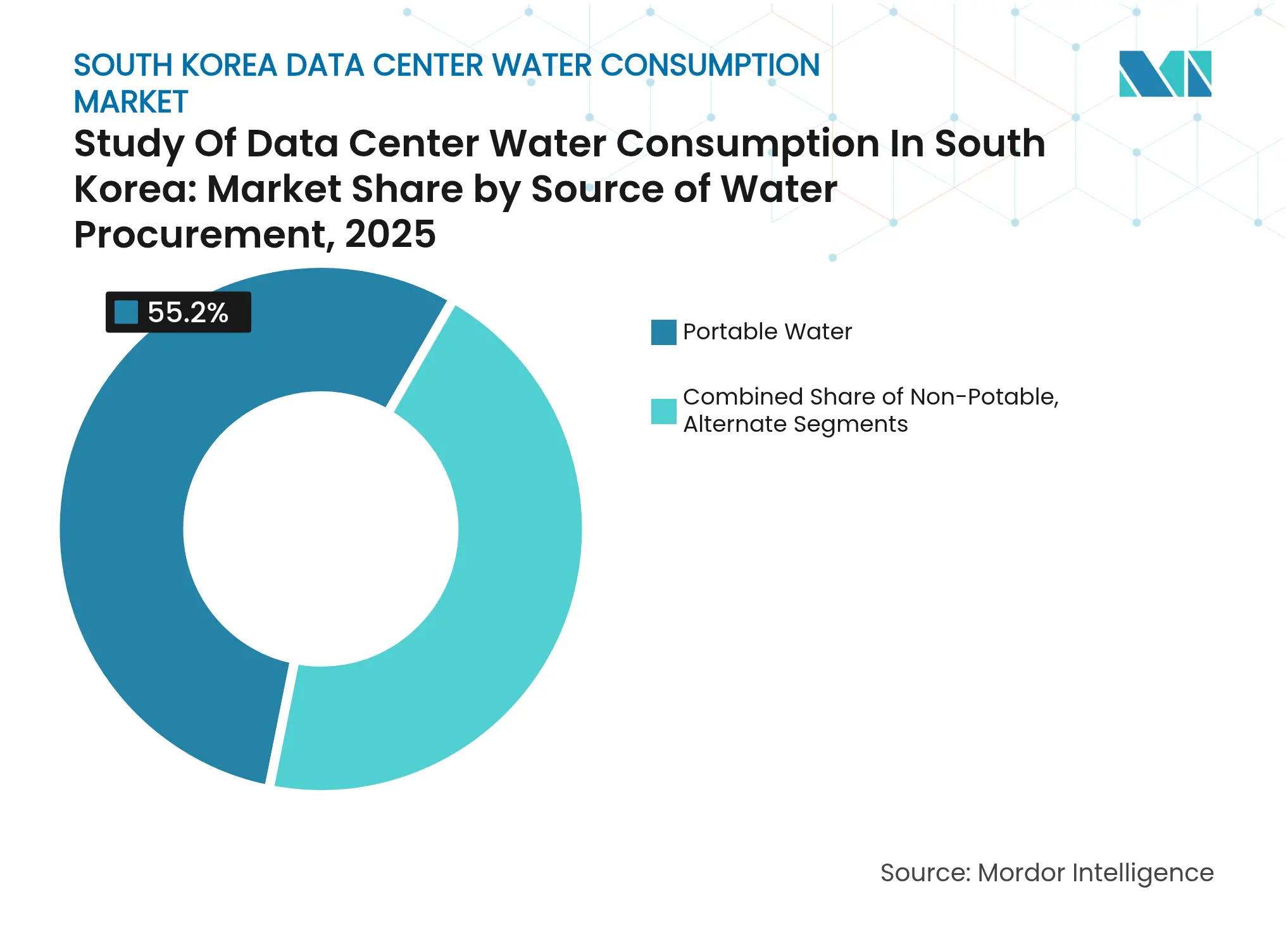

Potable supply delivered 55.20% of the data center water consumption market share in 2025, signalling operators’ continued preference for reliability. The alternate-source segment, however, is forecast to post a 17.08% CAGR, the fastest within the data center water consumption market. Large coastal builds already rely on filtered seawater, while greywater uptake accelerates inside Seoul where municipal pipe networks reach major ICT parks. Seawater systems provide 15–20% efficiency gains and eliminate municipal allocation disputes. Greywater reuse faces infrastructure shortages outside the capital, yet subsidy schemes and stricter potable quotas will push adoption into secondary cities over the next three years.

The segment’s rise is underpinned by performance gains. Lab trials show indirect seawater chillers operating with COP near 4.8 versus 3.2–3.8 for freshwater units. Greywater systems using membrane bioreactors achieve turbidity below 1 NTU, meeting ASHRAE Class W1 cooling-tower criteria. Rainwater harvesting remains marginal but attractive for hyperscaler campuses with large roof areas, especially where storm-water fees can be offset against storage investments. Overall, diversifying supply shields operators from tariff volatility and strengthens ESG credentials inside the data center water consumption market.

Note: Segment shares of all individual segments available upon report purchase

By Data Center Type: Hyperscalers Redefine Demand

Colocation retained 44.70% of 2025 consumption, yet cloud platforms will outgrow every other cohort at an 18.58% CAGR through 2031. Hyperscalers build contiguous blocks of 80–100 MW, collapsing what once took dozens of enterprise rooms into single campuses. This clustering makes water infrastructure a project-critical path item, prompting early engagement with utilities and, increasingly, direct investments in desalination or district-cooling loops. Enterprise sites remain steady but consolidate footprints via hybrid-cloud shifts, moderating their incremental water draw within the data center water consumption market.

Hyperscalers leverage scale to pilot advanced cooling. The 100 MW AWS-SK campus in Ulsan couples LNG regasification cold energy with seawater exchangers in a closed-loop, cutting freshwater needs to zero. Colocation landlords respond by deploying shared cooling towers sized for diurnal peaks, pushing WUE toward 0.9 L/kWh. Smaller enterprise facilities adopt modular edge units below 2 MW that use refrigerant loops and consume negligible water, but these account for a shrinking share of aggregate consumption as cloud elasticity attracts new AI workloads.

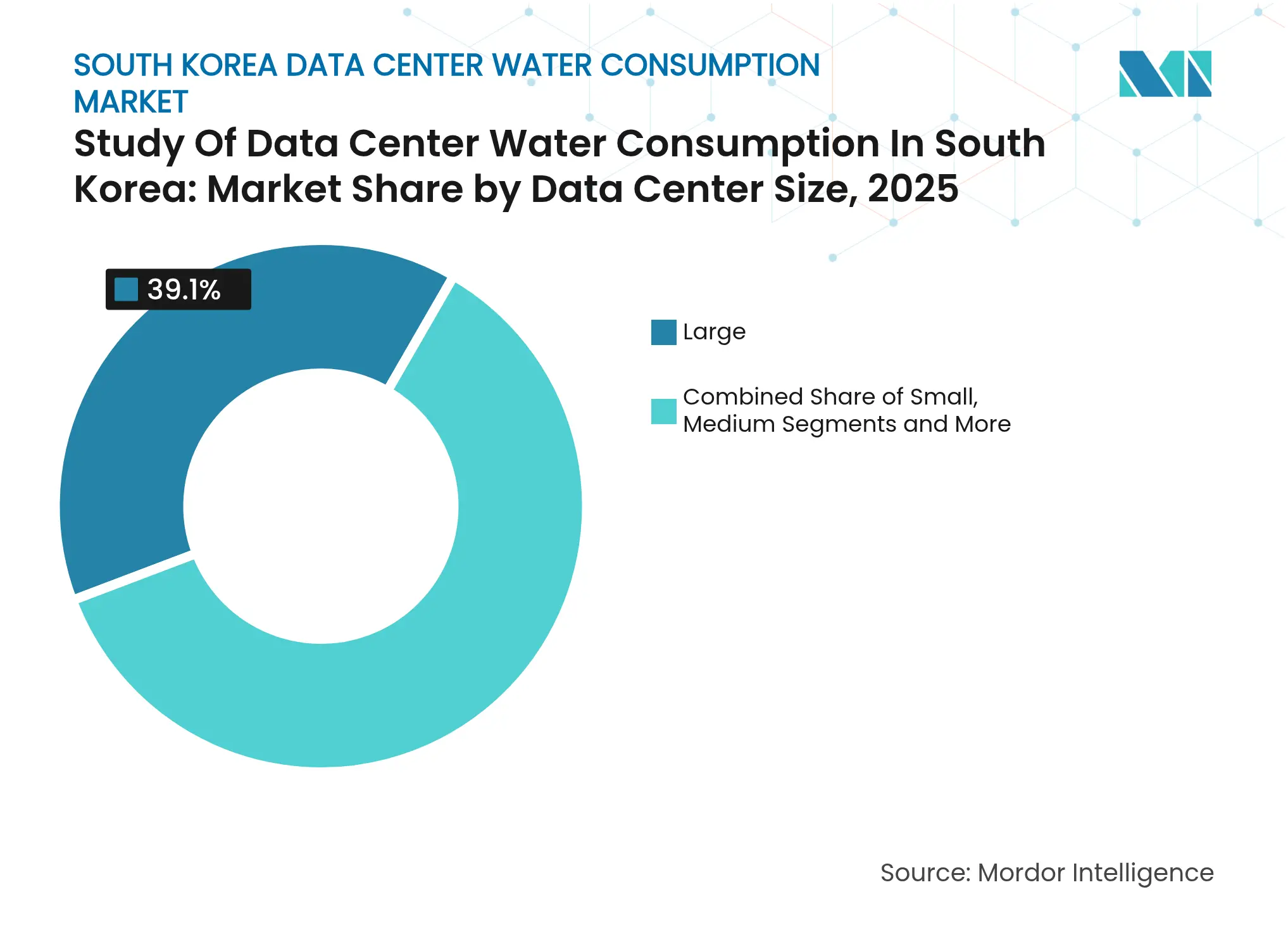

By Data Center Size: Mega-Scale Projects Lead Growth

Large campuses between 10 MW and 25 MW presently represent 39.10% of the data center water consumption market size. Mega-facilities exceeding 50 MW, including the planned 3 GW cluster in Jeollanam-do, are projected to achieve a 19.05% CAGR to 2031, becoming the dominant sink for cooling water. At these scales, developers negotiate multi-decade supply contracts and co-finance municipal treatment plants to secure capacity ahead of construction.

Mega-projects integrate district-cooling and waste-heat recovery, using ammonia absorption chillers or hydrogen-driven fuel-cell stacks that nearly eliminate evaporative loss. Samsung’s hydrogen-powered proof-of-concept reduced total site water use by 70% compared with traditional evaporative towers. Medium facilities from 1 MW to 10 MW adopt air-cooled chillers where climate allows, but their aggregated contribution to national demand slips as hyperscaler clusters absorb the bulk of new AI compute.

Note: Segment shares of all individual segments available upon report purchase

Roughly 59.80% of national consumption concentrates in the Seoul metropolitan area, benefitting from fiber density and proximity to corporate headquarters. Seoul’s city government offers capital rebates covering up to 30% of greywater-pipeline installation, accelerating closure of potable loops for ICT parks. Even with efficiency gains, absolute volumes in the capital keep rising, pressuring the Han River supply grid and leading to allocation quotas that slow permits for new halls.

Coastal hubs—Busan, Incheon, and Ulsan—record faster expansion than the national average as seawater cooling sidesteps inland freshwater stress. Busan leverages its submarine-cable gateways, yet resident opposition to aquifer withdrawals obliges operators to tap deep-sea intakes several kilometres offshore. Incheon’s Songdo district ties data-center chillers into regional district-energy networks, sharing excess cooling with commercial towers and cutting combined WUE to 0.7 L/kWh. Ulsan’s LNG infrastructure furnishes free cold energy, slashing chiller loads and attracting AI clusters that would otherwise face water moratoria inland.

Secondary provinces such as Jeollanam-do and Chungbuk offer inexpensive land and renewable-energy proximity, but lack greywater mains or high-capacity transmission. The planned 3 GW Jeollanam-do complex bundles dedicated desalination and 400 kV grid tie-ins to overcome these deficits. While rural sites can tap local groundwater more easily, tightening extraction quotas and seasonal recharge variability push developers toward closed-loop or hybrid dry coolers, tempering growth until infrastructure scales.

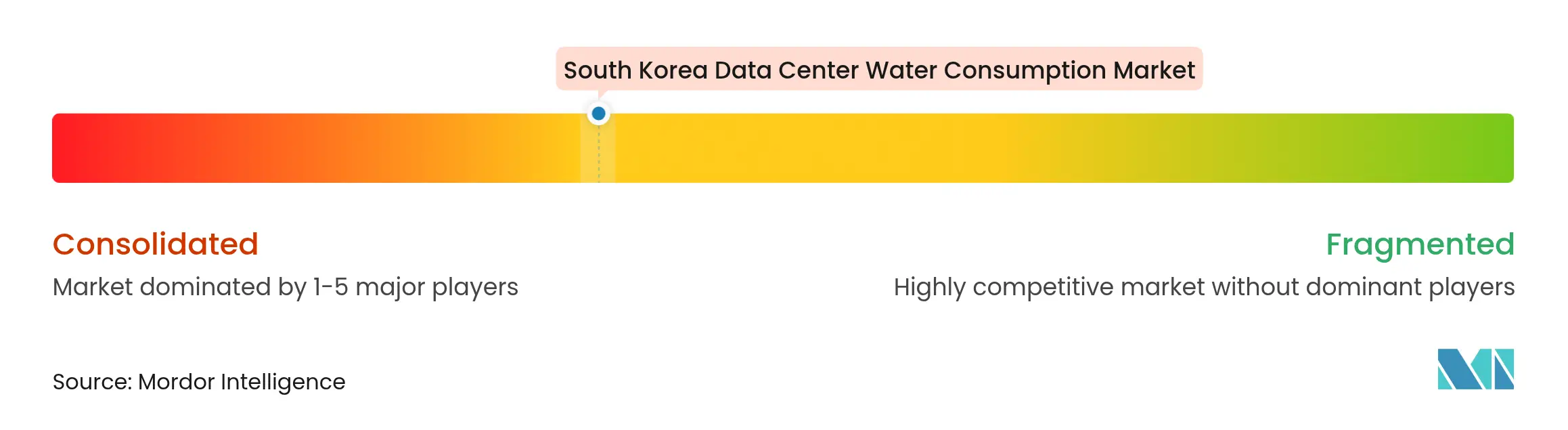

Market Concentration

The data center water consumption market is moderately fragmented; no single operator controls more than 15% of aggregate liters consumed. Domestic telecom incumbents SK Inc. and KT Corporation utilise existing exchanges to host incremental IT loads, but hyperscalers—AWS, Microsoft, Google, and Alibaba—now out-invest local firms as AI demand surges. These entrants form joint ventures to navigate permitting and source water: AWS partners with SK Group, while Microsoft collaborates with LG U+ on seawater-based campuses.

Strategic emphasis has shifted from raw megawatt roll-outs to demonstrable WUE leadership. Samsung aligns with Korea Southeast Power to trial hydrogen fuel cells that export waste heat to nearby industrial users, removing cooling towers entirely. KT pilots two-phase immersion across a 5 MW hall to boost rack density to 120 kW, freeing 30% of existing chiller capacity for expansion. Smaller specialists such as Bespin Global concentrate on AI-optimised thermal-management software that integrates with ISO-compliant metering, allowing clients to report sub-1.0 L/kWh figures to regulators.

M&A interest revolves around water-treatment integrators and greywater-pipeline contractors, signalling a pivot where control over hydrological assets equals prime-site land banks. Vertical integration is visible as SK Inc. acquires minority stakes in a reverse-osmosis membrane maker, while Hyperscale Korea LLC invests in offshore intake infrastructure to future-proof water rights. Vendors able to cut both energy and water intensity gain pricing power as clients internalise the full cost of resource exposure within long-term total-cost-of-ownership models.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. DATA CENTER INDUSTRY OUTLOOK

6. MARKET SIZE AND GROWTH FORECASTS (US USD MN / BILLION L)

7. COMPETITIVE LANDSCAPE

8. MARKET OPPORTUNITIES and FUTURE OUTLOOK

The study tracks the critical applications of water for running a large data centers, such as DC cooling, and power generation. The study also includes key applications based on the Water Consumption in Data Centers. The study also includes the overall water consumption based on the DC footprint across regions in terms of billion liters. Lastly, the study tracks the underlying trends and developments conceptualized by leading industry data center operators and cloud service providers.

The Study of Data Center Water Consumption in South Korea is Segmented by Source of Water Procurement (Potable Water, Non-Potable Water, Other Alternate Sources), by Data Center Type (Enterprise, Colocation, Cloud Service Providers), and by Data Center Size (Mega, Massive, Large, Medium, Small). The Market Sizes and Forecasts are Provided in Terms of Volume (Billion Liters).

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Pricing Strategy for Semiconductor Components

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.