Spain Payment Gateway Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

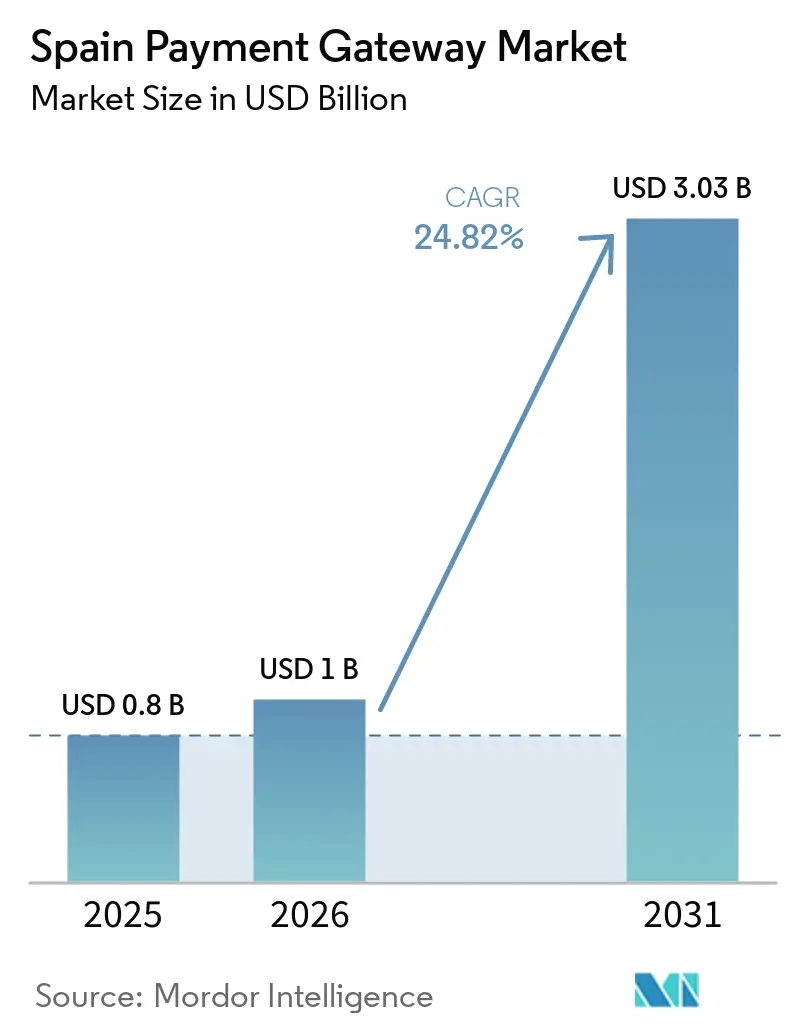

| Base Year Market Size (2025) | USD 0.8 Billion |

| Market Size (2026) | USD 1 Billion |

| Market Size (2031) | USD 3.03 Billion |

| Growth Rate (2026 - 2031) | 24.82% CAGR |

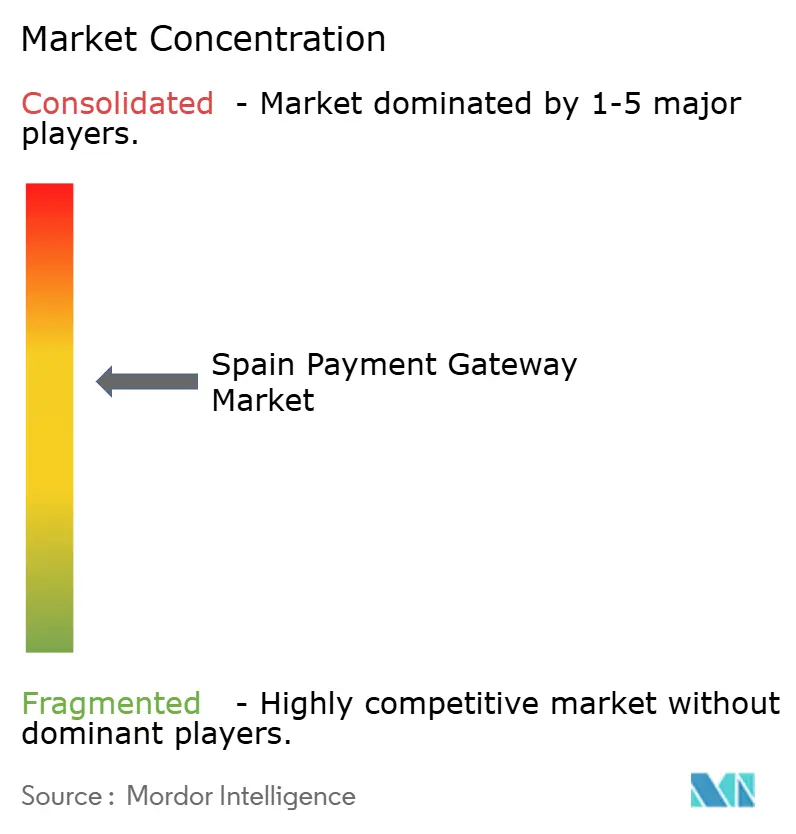

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Payment Gateway Market Analysis by Mordor Intelligence

The Spain payment gateway market size is expected to grow from USD 0.80 billion in 2025 to USD 1.00 billion in 2026 and is forecast to reach USD 3.03 billion by 2031 at 24.82% CAGR over 2026-2031. Rising instant-payment adoption, the mainstream success of Bizum, and sizeable EU funding for SME digitalization form the core growth catalysts. Mandatory SEPA Instant rails scheduled for late-2025 will provide real-time settlement nationwide, while the Kit Digital subsidy lowers entry barriers for small firms deploying e-commerce checkouts. Strong cross-border tourist spending, near-universal smartphone penetration, and AI-powered fraud screening further expand addressable volumes for the Spain payment gateway market. Competitive intensity is increasing as bank-backed schemes such as Wero challenge global processors on domestic turf, pressing gateways to differentiate through omnichannel experiences, analytics, and value-added services rather than speed alone. [1]European Payments Council, “Transforming Payments in Spain: The Impact of Instant and International Payments,” europeanpaymentscouncil.eu

Key Report Takeaways

- By payment method, cards dominated with 44.30% revenue share in 2025, whereas digital wallets are forecast to expand at a 27.14% CAGR to 2031.

- By gateway type, hosted gateways accounted for 68.20% of the Spain payment gateway market share in 2025, while non-hosted/API models are projected to grow at a 26.12% CAGR through 2031.

- By enterprise size, large enterprises held 59.20% of the Spain payment gateway market size in 2025; SMEs record the fastest projected CAGR at 28.76% to 2031.

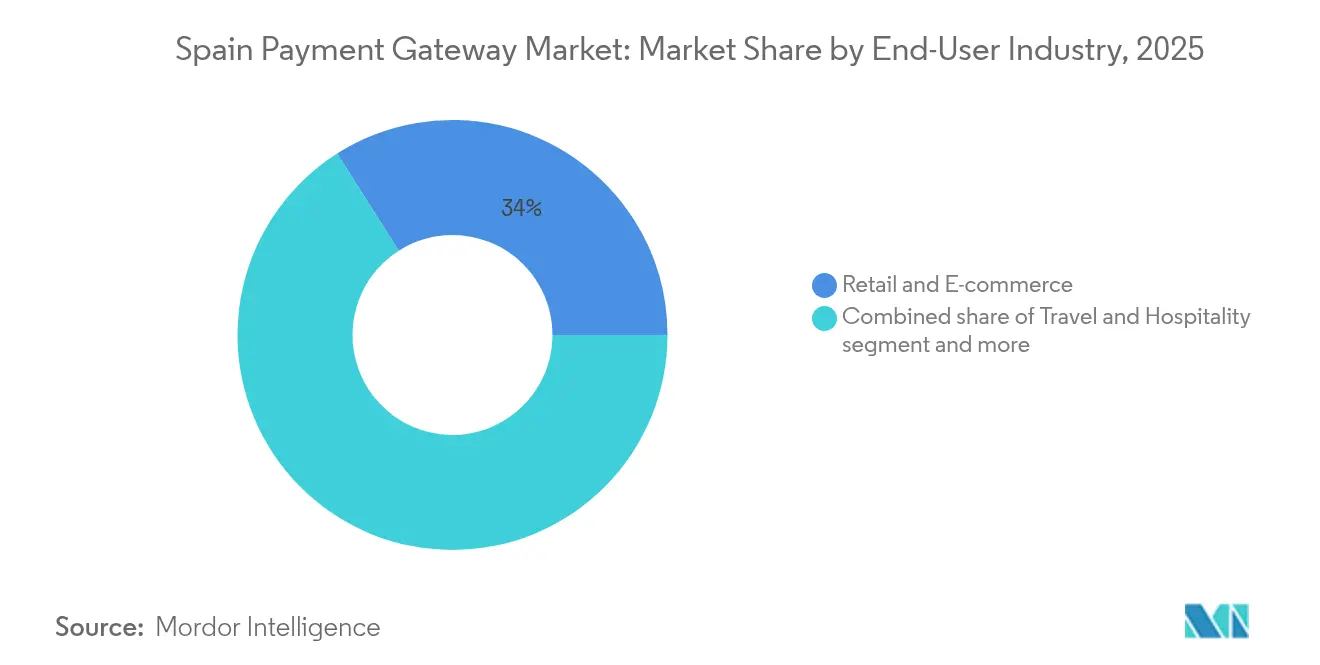

- By end-user industry, retail & e-commerce led with a 34.02% share in 2025, whereas media & entertainment is advancing at a 27.93% CAGR through 2031.

- By transaction channel, desktop held 54.10% of 2025 volumes, yet mobile payments are set to rise at a 29.65% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Payment Gateway Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mobile-wallet usage post-Bizum integration with large merchants | 4.20% | National, with concentration in Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| EU Digital Payments Package funding for SMEs | 3.80% | National, with rural area focus | Short term (≤ 2 years) |

| Mandatory instant-payment rails (SEPA Inst) go live Q4-2025 | 5.10% | National, aligned with EU framework | Short term (≤ 2 years) |

| Tourism rebound pushes cross-border card volumes | 2.90% | Coastal regions, Balearic and Canary Islands | Medium term (2-4 years) |

| AI-driven fraud-screening lowers gateway switching-costs | 2.30% | National, with fintech hub concentration | Long term (≥ 4 years) |

| "Green receipts" tax incentives for e-invoicing | 3.10% | National, phased implementation by company size | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Mobile-Wallet Usage Post-Bizum Integration with Large Merchants

Bizum’s pivot from peer-to-peer transfers to in-store and online merchant payments expands acceptance beyond banking apps. The 2025 launch of Bizum Pay will enable NFC contactless payments directly from current accounts, leveraging existing POS terminals and eliminating card network fees. Large retailers that embed Bizum at checkout report lower cart-abandonment and higher repeat purchase rates. With 26 million users—60% of Spain’s banked population—Bizum now underpins nearly half of all account-to-account transactions. As smartphone penetration nears 97% by 2029, mobile-first gateways that integrate Bizum seamlessly are positioned to capture incremental volumes within the Spain payment gateway market.

EU Digital Payments Package Funding for SMEs

Spain’s EUR 3.067 billion Kit Digital scheme reimburses SMEs for e-commerce platforms, cybersecurity, and certified billing software. More than 530,000 grants had been approved by late-2024, creating a self-reinforcing surge in online acceptance tools. Many micro-merchants that previously relied on cash now onboard gateways bundled with invoicing and accounting modules, widening the Spain payment gateway market’s merchant base and lifting total processed value.

Mandatory Instant-Payment Rails (SEPA Inst) Go Live Q4-2025

From January 2025 all Spanish payment service providers must offer credit transfers that settle in ≤ 10 seconds. Spain already enjoys 78% bank participation in the SCT Inst scheme and processes 53% of credit transfers instantly, far above the 15% EU average. Universal real-time capabilities push gateways to add liquidity dashboards, smart routing, and working-capital tools rather than compete on speed alone, accelerating product innovation inside the Spain payment gateway market. [2]Directorate-General for Financial Stability, “Clarification of Requirements of the Instant Payments Regulation,” finance.ec.europa.eu

Tourism Rebound Pushes Cross-Border Card Volumes

International arrivals reached 9.49 million in May 2024, a 14% year-on-year rise, while visitor spend rose 22% to nearly EUR 12 billion (USD 13.56 billion). Higher-spending tourists from the United States and China drive foreign-card volumes, forcing gateways to optimize currency conversion and fraud management. Payment providers that embed multi-currency pricing and dynamic currency conversion capture incremental interchange and FX income, reinforcing growth across the Spain payment gateway market.

AI-Driven Fraud Screening Lowers Gateway Switching Costs

Spanish fintech such as Acoru deploy machine-learning risk engines that pre-score transactions in milliseconds, reducing false positives and chargeback rates. As merchants witness conversion uplifts, willingness to switch processors increases, pressuring incumbents to embed similar AI toolkits within their platforms. Competitive churn spurs service innovation and price competition, enlarging total processed volumes but compressing margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 3-D Secure 2.0 friction on conversion rates | -2.80% | National, with higher impact on e-commerce segments | Short term (≤ 2 years) |

| Interchange-fee cap squeezes PSP margins | -1.90% | National, aligned with EU regulations | Medium term (2-4 years) |

| Cyber-crime surge in account-to-account payments | -2.10% | National, with concentration in urban fintech hubs | Short term (≤ 2 years) |

| Bank-led push for EPI ONE threatens independent gateways | -3.40% | European, with direct impact on Spanish market | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

3-D Secure 2.0 Friction on Conversion Rates

Universal application of 3-D Secure 2.0 under PSD2 can cut completed transactions by up to 20% when risk-based exemptions are ignored. Spanish merchants therefore rely on gateways equipped with adaptive risk scoring that triggers step-up authentication only for high-risk flows. Providers able to sustain compliance while preserving one-click experiences gain share, whereas those lacking granular controls risk merchant attrition within the Spain payment gateway market.

Interchange-fee cap squeezes PSP margins

The EU cap limits domestic debit interchange to 0.2% and credit to 0.3%, restricting revenue on card processing in Spain. Gateways must fund scheme fees, PCI overhead, and fraud guarantees from a shrinking take-rate. Pressure has accelerated M&A, bank-processor alliances, and diversification into services such as data analytics and working-capital loans. Margin compression favours scale operators with optimized cost bases and dampens profitability expectations across the Spain payment gateway market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Method: Digital Wallets Accelerate Despite Card Dominance

Cards maintained a 44.30% share of the Spain payment gateway market in 2025 as 85% of residents held at least one debit or credit card. Nonetheless, digital wallets are growing at a 27.14% CAGR and are on track to seize a far larger slice of the Spain payment gateway market size by 2031 thanks to Apple Pay’s 30% usage and Google Pay’s 27% penetration.

The momentum stems from seamless tokenized checkout, biometric authentication, and widening merchant acceptance. Bizum and SEPA instant transfers provide a zero-fee alternative for both consumers and merchants, while BNPL wallets boost average ticket values in high-discretionary segments. Together these trends compress card margins yet expand overall processed value, sustaining double-digit expansion of the Spain payment gateway market.

Cards remain indispensable for travel bookings, car rentals, and corporate expenses, bolstered by loyalty schemes and global acceptance rails. Still, issuers are integrating card credentials into wallets to defend volumes, blurring lines between traditional plastic and mobile tokens. The impending digital euro pilot could later introduce public-sector wallet options, but private wallets presently lead innovations such as dynamic spending controls and inline couponing.

By Gateway Type: Non-Hosted Solutions Gain Merchant Control

Hosted gateways captured 68.20% of 2025 revenues due to their plug-and-play deployment and outsourced PCI scope. Yet non-hosted/API models are advancing at a 26.12% CAGR as data-driven merchants seek full branding control and granular analytics. The shift adds depth to the Spain payment gateway market because API gateways often bundle value-added modules that raise average revenue per merchant.

Large platforms leverage custom checkout flows, network tokenization, and intelligently routed authorizations to lift approval rates. Non-hosted architectures expose raw transaction data that merchants mine for cohort analysis, lifetime-value tracking, and real-time fraud insights. Hosted providers respond with hybrid offers—embedded checkout widgets plus optional server-to-server calls—in an effort to retain SME customers migrating upward.

Adoption is visible in fashion marketplaces and subscription media apps that demand localized payment methods alongside global ones. API gateways also simplify experimentation with payment orchestration, allowing merchants to route traffic dynamically between acquirers for optimal cost and reliability, reinforcing competitive churn inside the Spain payment gateway market.

By Enterprise Size: SME Digitalization Drives Fastest Growth

Large enterprises held 59.20% of the Spain payment gateway market share in 2025, buoyed by omni-channel deployments across retail chains, airlines, and utilities. These firms require sophisticated token vaults, multi-currency settlement, and acquirer redundancy, services generally priced at premium take-rates.

The growth spotlight, however, sits with SMEs whose 28.76% CAGR through 2031 outpaces all other cohorts. More than 500,000 micro-firms have tapped Kit Digital vouchers, channelling grants into storefront builders, POS upgrades, and cybersecurity suites that bundle gateway connections. As invoice digitization becomes mandatory, SMEs increasingly demand end-to-end platforms that integrate billing, tax reporting, and payments, unlocking new recurring revenue for the Spain payment gateway market.

Regional banks promote white-label gateways tailored to small merchants, pairing local support with embedded cash-flow lending. Fintechs counter with pay-as-you-go packages requiring no fixed fees. Competitive variety widens choice, accelerates onboarding, and elevates digital acceptance in provinces that historically favoured cash and bank transfer.

By End-User Industry: Media & Entertainment Leads Innovation

Retail & e-commerce in Spain led 2025 with a 34.02% revenue share, driven by Spain’s USD 35.5 billion online retail spend. Dynamic offers like BNPL, pay-by-link, and loyalty wallet integration underpin its continued weight in the Spain payment gateway market. Travel & hospitality follows closely, sparked by tourist rebounds and the re-opening of long-haul routes.

Media & entertainment, the fastest-growing vertical at a 27.93% CAGR, benefits from streaming, gaming micro-transactions, and creator-economy monetization. Subscription platforms need agile retry logic, seat-based billing, and cross-border settlement in multiple currencies, pushing them toward API-centric gateways. Banks and insurers modernize premium payment collections through instant transfers, while education and utilities adopt gateways to digitize historically paper-based receivables.

Large merchants increasingly request contextual checkout—buying cinema tickets within chat apps or paying for gaming add-ons directly in console stores. Gateways that expose SDKs for in-app purchases and Web3 token support expand relevance, sustaining overall growth of the Spain payment gateway market size.

By Transaction Channel: Mobile Commerce Transformation Accelerates

Desktop still processed 54.10% of gateway transactions in 2025, reflecting entrenched laptop shopping behaviour. Yet mobile volumes are scaling at a 29.65% CAGR as handset capabilities rival desktops and 5G becomes ubiquitous. Early-2025 will see Bizum Pay delivering NFC in-store transactions that settle instantly, bypassing card rails while leveraging existing terminals.

One-touch biometrics, push notifications for abandoned carts, and integrated loyalty accelerate conversion on mobile apps. QR code acceptance spreads across bars and markets, aided by low-cost SoftPOS solutions running on Android devices. Providers optimize SDK size, offline fallback, and local token storage to minimize latency and elevate approval rates, feeding the upward trajectory of the Spain payment gateway market.

Checkout-on-delivery for grocery and quick-commerce platforms shows high affinity with instant account-to-account solutions, shifting wallet share away from cash. As mobile screen sizes grow, rich media catalogues and augmented-reality product previews become more common, driving higher transaction values and reinforcing the mobile channel’s expansion.

Geography Analysis

Spain commands outsized influence within southern Europe’s gateway ecosystem thanks to its 53% instant credit-transfer adoption versus the EU’s 15% average. Madrid and Barcelona serve as fintech nuclei, concentrating venture funding, developer talent, and early-adopter merchants. Valencia’s smart-city projects widen real-time payments in public transport and municipal services.

Coastal economies anchored by the Balearic and Canary Islands register superior foreign-card activity amid a tourism resurgence that lifted visitor spend 22% in May 2024. High seasonality forces gateways to scale elastically and price cross-border acquiring competitively. Rural regions, historically cash-oriented, benefit from Kit Digital grants that subsidize POS upgrades and broadband rollouts, expanding the Spain payment gateway market into long-tail merchant segments.

Spanish banks back the European Payments Initiative, positioning Wero to interlink with domestic Bizum rails and extend acceptance across Belgium, France, and Germany. Cross-border instant pilots such as EuroPA underscore Spain’s role in pan-EU interoperability. The Bank of Spain’s CBDC sandbox with Cecabank and Abanca highlights commitment to next-generation rails, although citizen appetite for a digital euro remains modest. Geography-specific drivers collectively anchor Spain as a payment innovation testbed and export hub.

Competitive Landscape

The Spain payment gateway market hosts a balanced mix of international giants, domestic processors, and emergent consortia. Stripe, Adyen, and PayPal maintain brand recognition and developer mindshare, but local processor Redsys cleared 19.7 billion transactions worth EUR 505 billion in 2024, retaining deep bank integrations.

European sovereignty pushes banks toward collective plays. Wero enrolled 40 million users across its launch markets and eyes Spain for 2026, promising lower fees through direct bank connectivity. Unicaja’s 2025 agreement with Fiserv will co-create omni-channel solutions tailored to Spanish merchants, reflecting a broader trend of bank-processor alliances.

Technology differentiation centers on fraud AI. Acoru’s risk engine eliminates friction for low-risk shoppers, while Worldline’s Digital Security Suite deploys behavioural analytics in milliseconds. Margin pressure from interchange caps motivates gateways to upsell analytics dashboards, payout advances, and working-capital loans. Consolidation is likely, especially among niche players lacking scale to absorb compliance and security investments. [4]Redsys, “Annual Transaction Statistics 2024,” redsys.es

Spain Payment Gateway Industry Leaders

Adyen N.V.

PayPal Holdings Inc.

Redsys Servicios de Procesamiento S.L.

Stripe Inc.

Bizum S.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Unicaja Banco and Fiserv signed a strategic agreement to co-develop omnichannel payment solutions for Spanish merchants.

- January 2025: Instant Payments Regulation came into force, requiring all providers to process credit transfers within 10 seconds

- November 2024: SeQura partnered with Stripe to expand BNPL options for Spanish e-commerce.

- October 2024: Bizum announced Bizum Pay, an NFC contactless solution launching mid-2025.

Spain Payment Gateway Market Report Scope

A payment gateway is a technology that retailers use to enable client debit or credit card purchases. The primary function of an online payment gateway is to authorize the exchange of money between a retailer and a customer. Making an online purchase and authorizing transactions between sellers and buyers is crucial.

The Spain payment gateway market is segmented by type (hosted and non-hosted), enterprise (small and medium enterprise (SME) and large enterprise), and end-user (travel, retail, BFSI, media and entertainment, other end users). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Cards |

| Digital Wallets |

| Account-to-Account (Bizum, SEPA Inst) |

| Buy-Now-Pay-Later |

| Hosted |

| Non-Hosted / API |

| Large Enterprise |

| Small and Medium Enterprise |

| Retail and E-commerce |

| Travel and Hospitality |

| Banking, Financial Services and Insurance |

| Media and Entertainment |

| Others (Education, Utilities, etc.) |

| Mobile |

| Desktop / Other |

| By Payment Method | Cards |

| Digital Wallets | |

| Account-to-Account (Bizum, SEPA Inst) | |

| Buy-Now-Pay-Later | |

| By Gateway Type | Hosted |

| Non-Hosted / API | |

| By Enterprise Size | Large Enterprise |

| Small and Medium Enterprise | |

| By End-User Industry | Retail and E-commerce |

| Travel and Hospitality | |

| Banking, Financial Services and Insurance | |

| Media and Entertainment | |

| Others (Education, Utilities, etc.) | |

| By Transaction Channel | Mobile |

| Desktop / Other |

Key Questions Answered in the Report

What is the current size of the Spain payment gateway market?

The market is valued at USD 1.00 billion in 2026 and is projected to reach USD 3.03 billion by 2031.

Which payment method is growing the fastest in Spain?

Digital wallets are expanding at a 27.14% CAGR, outpacing all other methods thanks to widespread Apple Pay, Google Pay, and Bizum adoption.

How will SEPA Instant affect gateways operating in Spain?

From Q4-2025 all credit transfers must settle in ≤ 10 seconds, shifting competition from speed to value-added services such as liquidity tools and analytics.

Why are SMEs important to gateway growth?

More than 500,000 SMEs have tapped Kit Digital subsidies, driving a 28.76% CAGR in SME gateway adoption as they digitize sales and invoicing processes.

What are the main challenges facing Spanish gateway providers?

Mandatory 3-D Secure 2.0 can depress conversion by up to 20%, and EU interchange caps compress processing margins, forcing gateways to innovate and diversify revenue.

How large is the opportunity in mobile payments?

Mobile volumes are forecast to rise at a 29.65% CAGR, underpinned by 97% smartphone penetration and the mid-2025 rollout of Bizum Pay’s NFC functionality.

Page last updated on: