Market Overview

| Study Period | 2021 - 2031 |

|---|---|

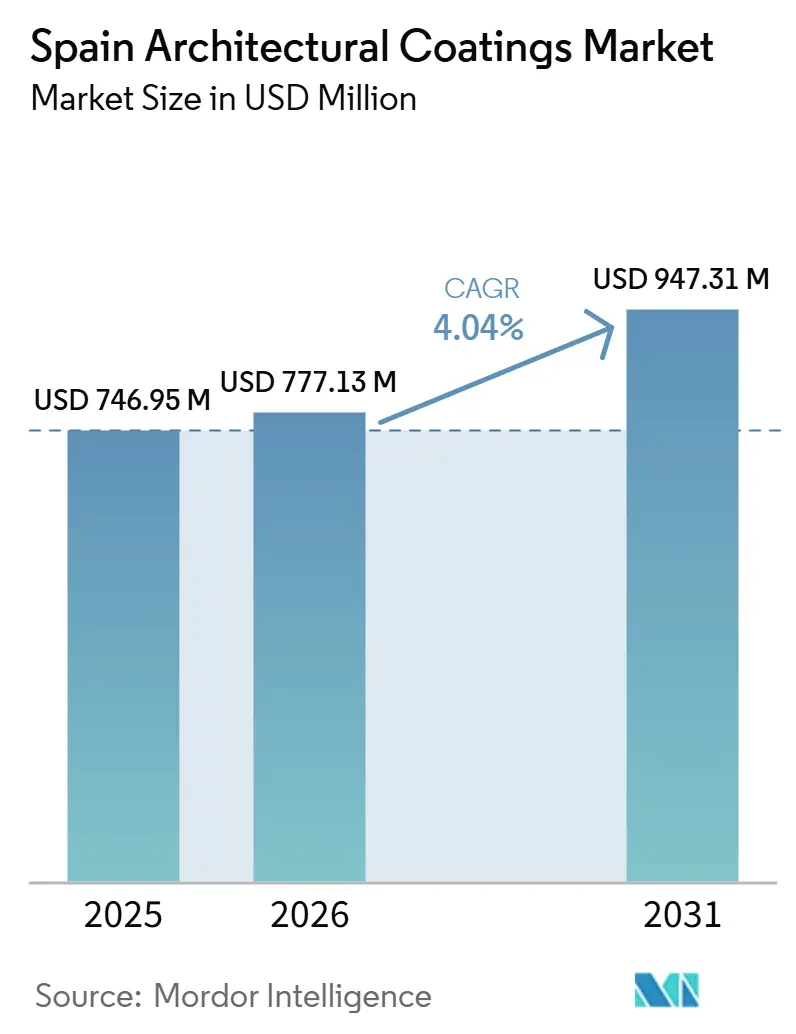

| Base Year Market Size (2025) | USD 746.95 Million |

| Market Size (2026) | USD 777.13 Million |

| Market Size (2031) | USD 947.31 Million |

| Growth Rate (2026 - 2031) | 4.04% CAGR |

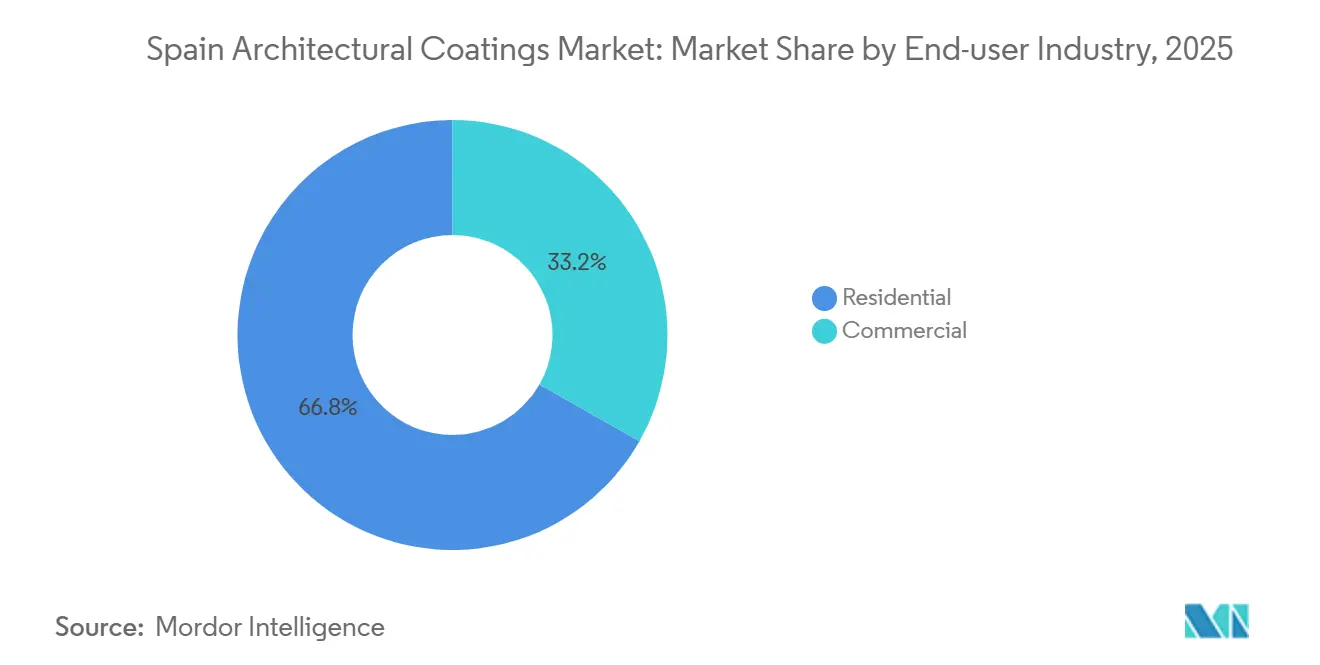

| Fastest Growing Market | Residential |

| Largest Market | Residential |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Architectural Coatings Market Analysis by Mordor Intelligence

The Spain architectural coatings market size was valued at USD 0.75 billion in 2025 and is estimated to grow from USD 0.78 billion in 2026 to reach USD 0.95 billion by 2031, at a CAGR of 4.04% during the forecast period (2026-2031). A multi-billion-euro renovation wave, fueled by European Union (EU) climate mandates and Spain’s National Building Renovation Plan (PNRE 2026), is shifting demand from new construction toward energy-efficient retrofits. Residential repainting dominates because two-thirds of Spanish homes were built before 1980 and now fall under mandatory energy-performance upgrades. Water-borne acrylic systems benefit from the February 2026 EU Ecolabel revision that tightened Volatile Organic Compounds (VOC) and Semi-Volatile Organic Compounds (SVOC) ceilings, while regional tenders in coastal provinces are specifying two-component epoxies and aliphatic polyurethanes with longer recoat intervals. Supply chains remain exposed to volatile titanium dioxide and acrylic-resin prices, yet the opening of new dispersion capacity in Türkiye and upgraded plants in Spain is easing some input risk.

Key Report Takeaways

- By end-user, the residential segment held the 66.78% share of Spain architectural coatings market share in 2025 and is projected to expand at a 4.24% CAGR from 2026 to 2031, remaining both the largest and the fastest-growing end-user slice.

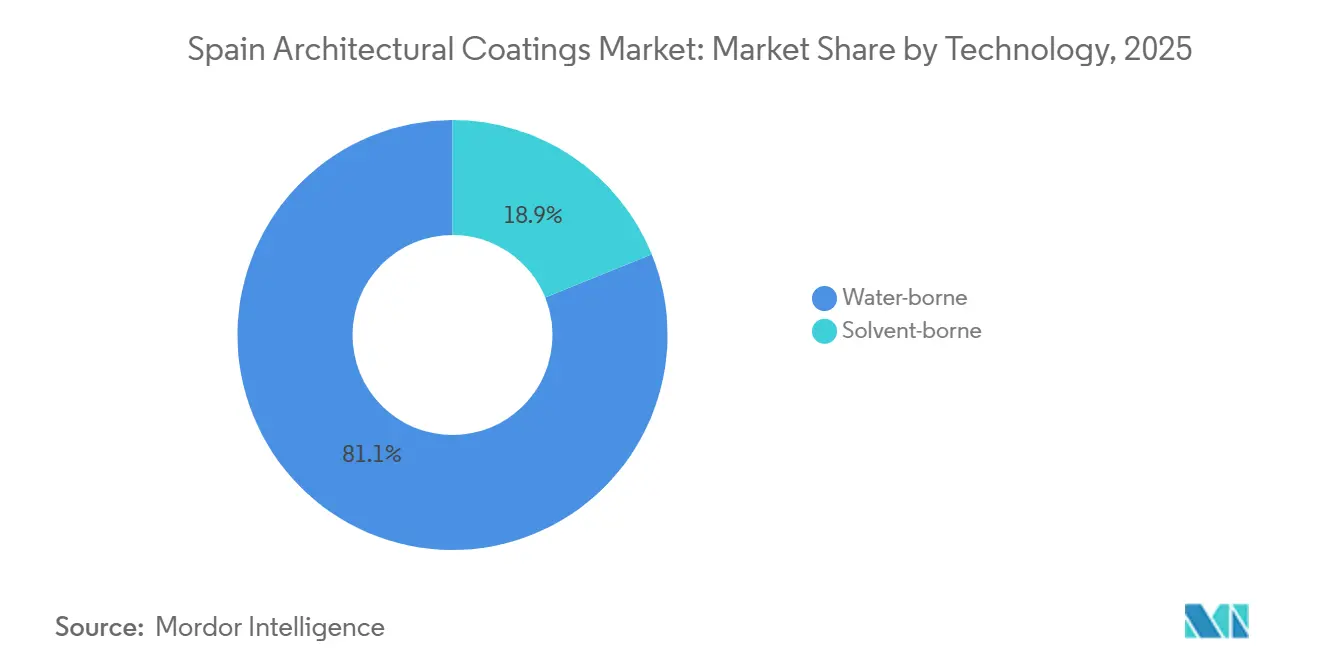

- By technology, water-borne formulations accounted for the 81.12% share of Spain architectural coatings market size in 2025, and they lead segment growth at a 4.44% CAGR from 2026 to 2031 as low-odor products gain preference in occupied dwellings.

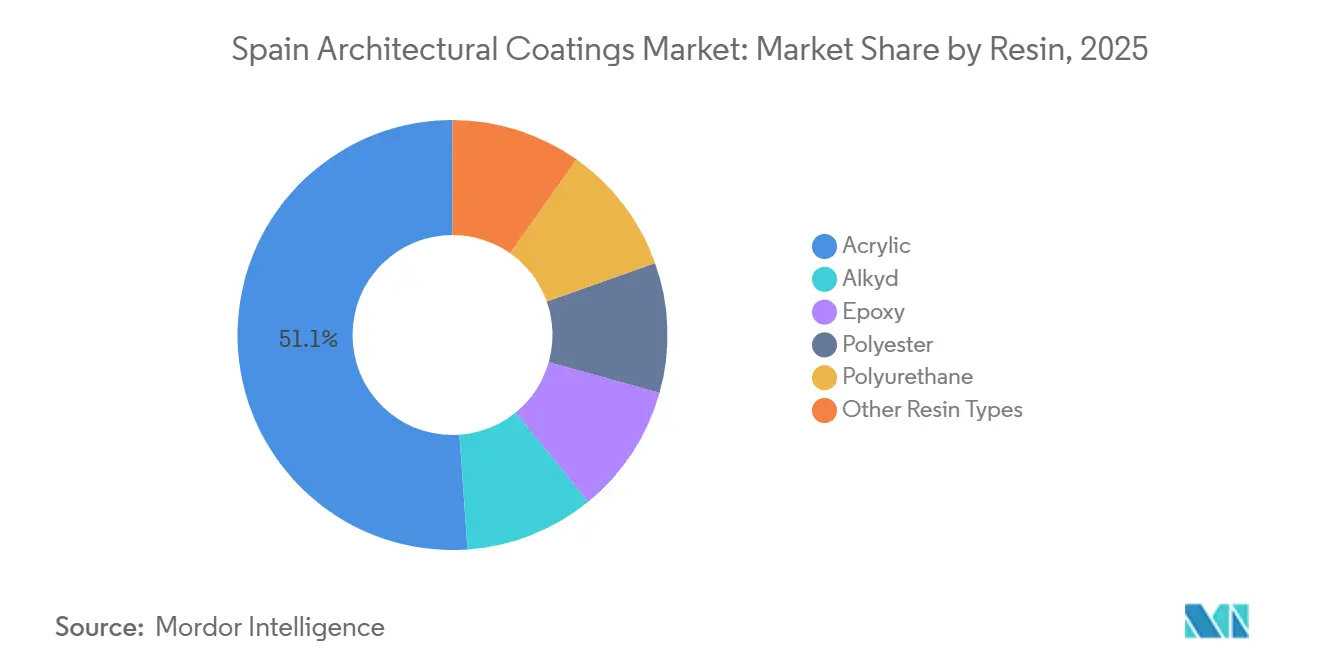

- By resin type, acrylic systems captured 51.16% Spain architectural coatings market share in 2025 and are forecast to rise at a 4.37% CAGR from 2026 to 2031 on the back of superior ultraviolet (UV) stability and compatibility with low-VOC water-borne chemistries.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential-renovation stimulus funds boost repaint demand | +0.8% | National, with concentrated uptake in Catalonia, Madrid, Valencia, Galicia | Short term (≤ 2 years) |

| EU "Renovation Wave" doubles façade upgrade rate through 2030 | +1.2% | National, aligned with PNRE 2026 targets for non-residential and residential stock | Medium term (2-4 years) |

| DIY e-commerce channels widen consumer access and color choice | +0.6% | Urban centers (Madrid, Barcelona, Valencia, Seville) with high broadband penetration | Short term (≤ 2 years) |

| Sharp rise in coastal climate-resilience standards needs high-durability exterior paints | +0.5% | Coastal provinces (Mediterranean arc, Balearic Islands, Canary Islands, Atlantic coast) | Medium term (2-4 years) |

| Smart/photocatalytic coatings encouraged in urban air-quality zones | +0.4% | Major urban air-quality management zones (Madrid, Barcelona, Valencia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Residential-Renovation Stimulus Funds Boost Repaint Demand

Spain has extended its three-tier energy-renovation tax deductions until 2026. Households can now claim grants and deductions from tax, provided their primary energy consumption decreases by at least 30%. Multi-family buildings are rushing to book façade upgrades before the grant window closes in late 2026, signaling a surge in demand. Contractors are increasingly bundling coatings with external insulation composite systems, leading to a notable rise in their contract share. Thanks to the State Housing Plan 2026-2030, government grants are covering 40-80% of retrofit costs for vulnerable households, speeding up project approvals. In response, suppliers are enhancing their just-in-time logistics to align with the accelerated 12- to 18-month renovation cycle, predominantly centered in urban areas.

EU “Renovation Wave” Doubles Façade-Upgrade Rate Through 2030

By 2030, Spain mandates that every non-residential building must surpass the performance of the current bottom 16%. This push aligns Spain's deep-renovation rate with the EU's annual target of 3%. With around 14 million homes poorly insulated, there's a significant market opportunity. In Catalonia's RENOVERTY roadmap[1]RENOVERTY, “Roadmap for Deep Renovation in Catalonia,” renoverty.cat , façade packages, featuring rigid insulation boards topped with acrylics, are now standard, priced between EUR 15 and 30 per m². Suppliers, benefiting from faster cash conversion, gain an edge as coatings are applied early in the retrofit sequence, unlike those tied to window or Heating, Ventilation, and Air Conditioning (HVAC) trades.

Sharp Rise in Coastal Climate-Resilience Standards

Coastal municipalities are turning to high-durability, water-borne epoxies and aliphatic polyurethanes for their metal structures, especially those frequently exposed to salt spray. Recent port tenders have set prices at EUR 19.38 per kg for epoxy primers and EUR 20.00 per kg for polyurethane topcoats. With the national rollout of EU Regulation 2024/3110 slated for 2026-2027, these performance benchmarks are set to be officially recognized. In a bid to offer warranties extending up to 15 years, suppliers are investing in accelerated-weathering tests in line with International Organization for Standardization (ISO) 11507 standards.

Smart / Photocatalytic Coatings Encouraged in Urban Air-Quality Zones

In Valencia, AIMPLAS and its partners are testing DACCO2 coatings on urban furniture[2]AIMPLAS, “DACCO2 Active Coatings Project,” aimplas.net . These coatings capture and mineralize airborne pollutants, aligning with the city's air-quality action plans. While the volumes remain modest, both Madrid and Barcelona have integrated photocatalytic surfaces into their low-emission-zone strategies. This move offers a prime opportunity for suppliers who can showcase effective and economical pollutant reduction in practical trials.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-applicator shortage inflates project lead-times | -0.7% | Rural provinces (Castile and León, Extremadura, Aragon) and aging construction workforce regions | Medium term (2-4 years) |

| Volatile TiO₂ and acrylic resin prices squeeze margins | -0.9% | National, with acute impact on SME formulators lacking hedging capacity | Short term (≤ 2 years) |

| Stricter VOC/SVHC limits raise reformulation costs for SMEs | -0.5% | National, particularly affecting SME manufacturers without in-house R&D | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile TiO₂ and Acrylic-Resin Prices Squeeze Margins

In 2025, disruptions at the Red Sea and Panama Canal led to a re-routing of freight from China to Europe, causing a 15-20% quarter-over-quarter swing in spot prices for titanium dioxide and acrylic resin. While multinationals typically hedge against such input fluctuations, smaller Spanish enterprises often bear the brunt of these shocks. As a response, these Small and Medium-sized Enterprises (SME) are reformulating their products, opting for lower-pigment hybrid binders that prioritize cost stability over hiding power.

Stricter VOC / SVHC Limits Raise Reformulation Costs for SMEs

Starting February 2026, the revised EU Ecolabel will impose stricter limits on VOCs and preservatives. At the same time, looming restrictions on Per- and polyfluoroalkyl substances (PFAS) will necessitate a transition to fluorine-free repellents. While major suppliers tap into global R&D centers to meet these standards, local producers, often without in-house laboratories, grapple with elevated testing costs due to EN 16516 emission protocols and extended certification durations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Residential Rehabilitation Outpaces New Commercial Build

Spain's architectural coatings market, driven predominantly by the residential end-user industry capturing 66.78% of the market, is set to grow at a projected CAGR of 4.24% through 2030. Grants covering up to 80% of retrofit costs, coupled with tax deductions linked to achieving 30% energy savings, are spurring more frequent repaint cycles in apartment blocks. Multi-family managers are opting for water-borne acrylic wall paints for interiors. For exteriors, they prefer breathable silicate or silicone-acrylic façades, which effectively prevent moisture entrapment behind newly installed insulation boards. Contractors are bundling these coatings with external insulation composite systems, priced between EUR 80 to 180 per m², leading to a surge in order aggregation.

In the commercial segment, which includes offices, retail spaces, hotels, and public assets, growth is slower. This is due to stretched permitting cycles and fragmented procurement processes across Spain’s 17 autonomous communities. Renovation efforts in non-residential spaces primarily focus on HVAC and lighting systems, with paints being addressed later. This sequence has tempered volume growth to below 4%. However, hospitals and schools are now specifying antimicrobial, low-odor coatings. Shopping centers are also showing a preference for anti-graffiti finishes. These trends present lucrative opportunities for suppliers offering certified hygienic or protective product lines.

By Technology: Water-Borne Formulations Sustain Regulatory Momentum

In 2025, water-borne coatings dominated Spain's architectural coatings market with 81.12% of the market, and they are projected to grow at a 4.44% CAGR through 2031. Low-odor emulsions enable swift re-occupancy in homes. Meanwhile, the updated EU Ecolabel, capping VOCs at 50 g/l, is steering the industry towards acrylic dispersions. Highlighting a shift towards sustainability, AkzoNobel has reported a 53% post-consumer recycled content in its European paint buckets.

Currently, solvent-borne systems are primarily used in heavy-duty coastal applications. While ports in the Balearic and Canary Islands continue to require aliphatic polyurethane topcoats for steel, tighter national VOC regulations set to take effect after 2026 are anticipated to reduce the solvent share to below 15% by 2031. This is unless specific conditions, like humidity or substrate issues, necessitate a departure from water-borne solutions.

By Resin Type: Acrylic Versatility Drives Dominance

In 2025, acrylic chemistries dominated Spain's architectural coatings market, securing a 51.16% share. Their blend of UV durability and low-VOC compatibility is projected to drive a 4.37% CAGR rise through 2031. In a strategic move, BASF invested EUR 70 million in a Guadalajara Technology Center in 2024, bolstering the local supply of low-carbon acrylic dispersions.

While alkyds are losing ground due to their higher VOC content leading to substitutions, they still play a crucial role in wood primers. Epoxies and polyurethanes, though niche, carve out profitable segments in anti-corrosion applications and high-traffic flooring. Their success is amplified by water-borne technology, adept at adhering to stringent emission standards. Meanwhile, silicone-acrylic hybrids are becoming increasingly popular for breathable façades, effectively directing moisture away from insulated walls.

Competitive Landscape

Spain's architectural coatings market is consolidated in nature. The market is home to global giants like AkzoNobel, BASF, PPG, Sherwin-Williams, Jotun, and Nippon Paint. These multinationals sit alongside regional players such as TITAN, CIN, Barpimo, and Pinturas Decolor. In a notable move, AkzoNobel inaugurated its EUR 32 million plant in Vilafranca in mid-2025. This facility specializes in producing bisphenol-free, water-borne coatings, achieving a 26% reduction in carbon footprints for its metal packaging clientele. Meanwhile, BASF launched a polymer-dispersion line in Dilovası, Türkiye, in October 2025, ensuring a steady supply of low-VOC products to meet the demands of the Iberian market.

Regional players are strengthening their positions by forging closer ties with distributors and enhancing technical services. A significant development saw Barpimo being acquired for EUR 45 million by Tambour Paints. This acquisition not only adds a 90-million-liter plant to Tambour's portfolio but also effectively doubles its footprint in Europe. On the other hand, players like TITAN and CIN are leveraging their expertise in color-matching, catering to heritage façades and offering breathable renders tailored for rural stone structures.

Emerging opportunities are evident in areas like photocatalytic coatings, packaging solutions rooted in circular-economy principles, and maintenance services utilizing digital-twin technology. Suppliers boasting ISO 14025 and EN 15804-compliant Environmental Product Declarations are carving out a significant niche in public procurement. In contrast, those without these certifications face potential exclusion. While tightening regulations on biocides are making water-borne preservation more challenging, they simultaneously pave the way for bio-based antimicrobials that align with BPR timelines.

Spain Architectural Coatings Industry Leaders

AkzoNobel N.V.

CIN, S.A.

DAW SE

Nippon Paint Holdings Co., Ltd.

PPG Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: : The European Commission issued updated EU Ecolabel criteria for decorative coatings, lowering VOC and SVOC thresholds and adding new preservative limits.

- May 2025: AIMPLAS launched the DACCO2 project to develop pollutant-capturing coatings for urban furniture in Valencia.

Spain Architectural Coatings Market Report Scope

Architectural coatings are protective and decorative finishes applied to stationary, on-site structures, such as residential, commercial, and industrial buildings. These products, including paints, stains, sealers, and varnishes, are designed for both exterior and interior surfaces to offer durability, aesthetics, and resistance to environmental damage.

The Spain Architectural Coatings market is segmented by end-user industry, technology and resin. By end-user industry, the market is segmented into commercial and residential. By technology, the market is segmented into solvent-borne and water-borne. By resin, the market is segmented into acrylic, alkyd, epoxy, polyester, polyurethane, and other resin types. For each segment, market sizing and forecasts are provided in terms of value (USD).

By End-User Industry

| Commercial |

| Residential |

By Technology

| Solvent-borne |

| Water-borne |

By Resin Type

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

| By End-User Industry | Commercial |

| Residential | |

| By Technology | Solvent-borne |

| Water-borne | |

| By Resin Type | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms