Space Mining Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 3.07 Billion |

| Market Size (2031) | USD 7.39 Billion |

| Growth Rate (2026 - 2031) | 19.21% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Space Mining Market Analysis by Mordor Intelligence

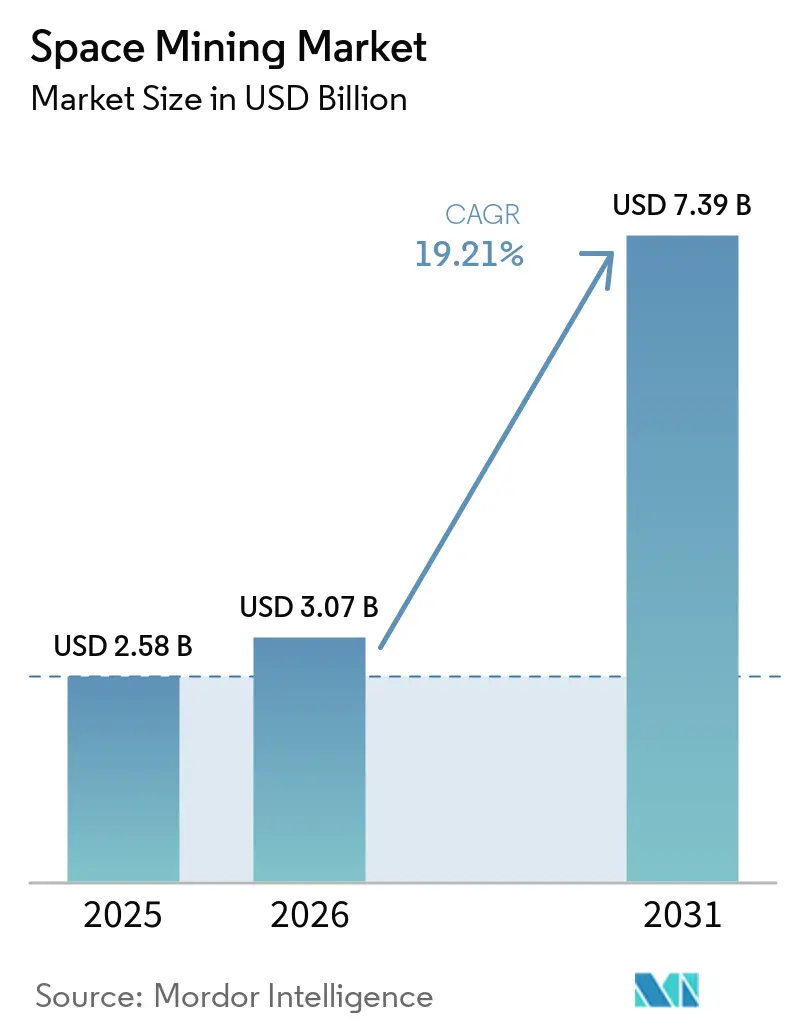

The space mining market size is expected to grow from USD 2.58 billion in 2025 to USD 3.07 billion in 2026 and is forecast to reach USD 7.39 billion by 2031, at a 19.21% CAGR over 2026-2031. Momentum in the space mining market is driven by a steep decline in orbital access costs that shifts the economics of prospecting and in-situ resource utilization from one-off experiments to programmatic missions. A more transparent rules framework, anchored by the Artemis Accords, reduces legal ambiguity around resource extraction while establishing practical safety-zone protocols. Public procurement, particularly NASA’s Commercial Lunar Payload Services, channels multi-year funding to private landers that deliver science payloads and field-test mining-relevant hardware on the Moon. Near-term offtake signals in strategic materials, such as helium-3 for quantum applications, add commercial pull that complements sovereign demand.

Key Report Takeaways

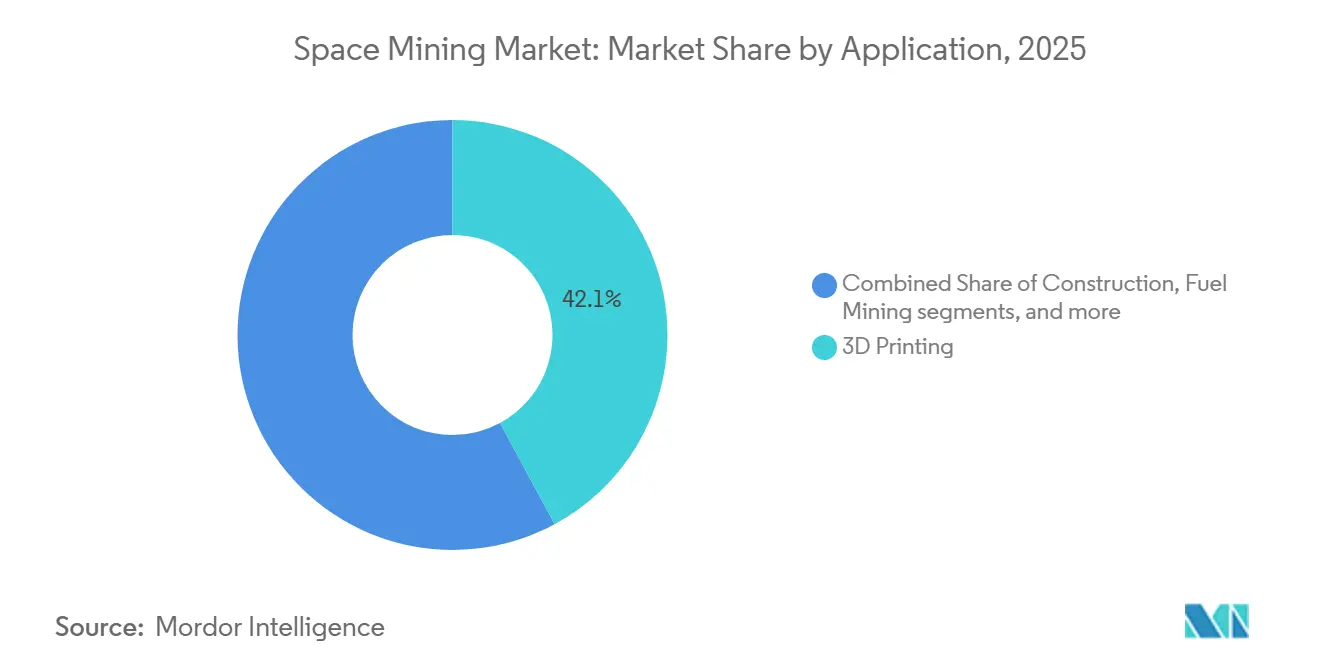

- By application, 3D printing led with 42.12% revenue share in 2025, and construction is forecasted to expand at a 25.85% CAGR through 2031.

- By resource type, water and volatiles accounted for a 47.55% share in 2025, while rare-earth and platinum-group metals (PGMs) are projected to grow at a 23.52% CAGR.

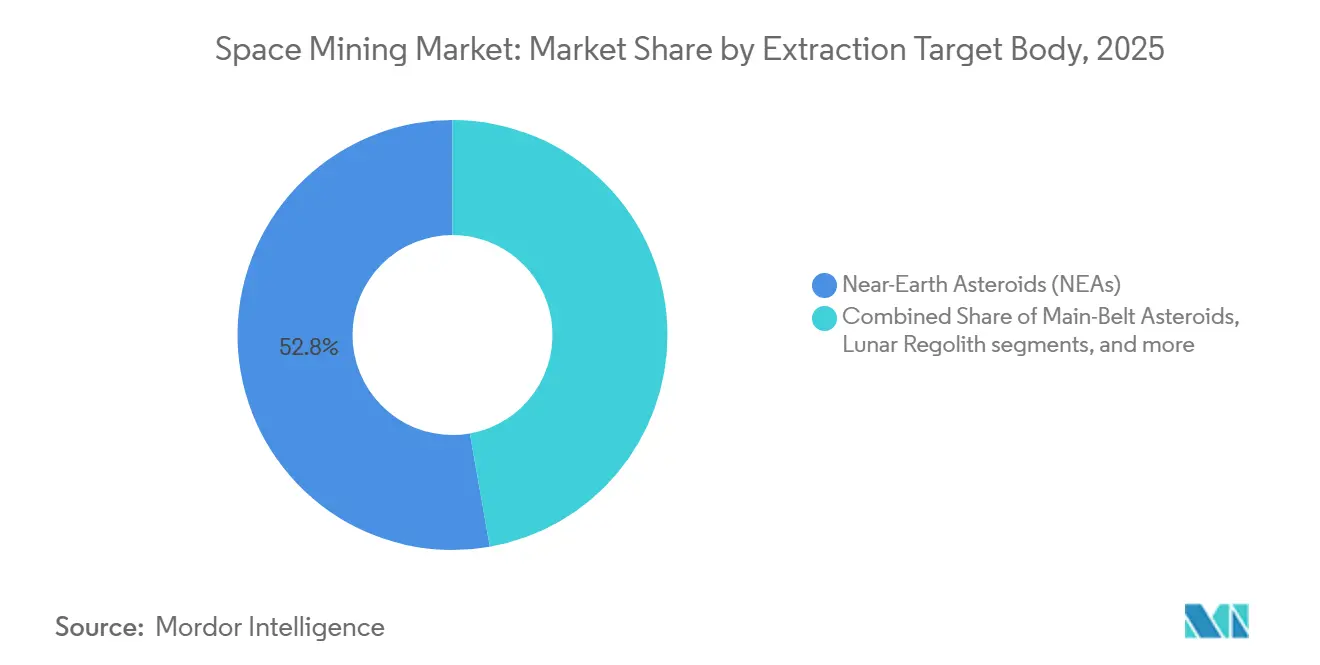

- By extraction target body, near-Earth asteroids accounted for 52.78% of 2025 activity, and lunar regolith is projected to grow at a 26.74% CAGR through 2031.

- By mission phase, spacecraft design and engineering accounted for 44.92% in 2025, and mining operations and logistics are projected to grow at a 24.98% CAGR.

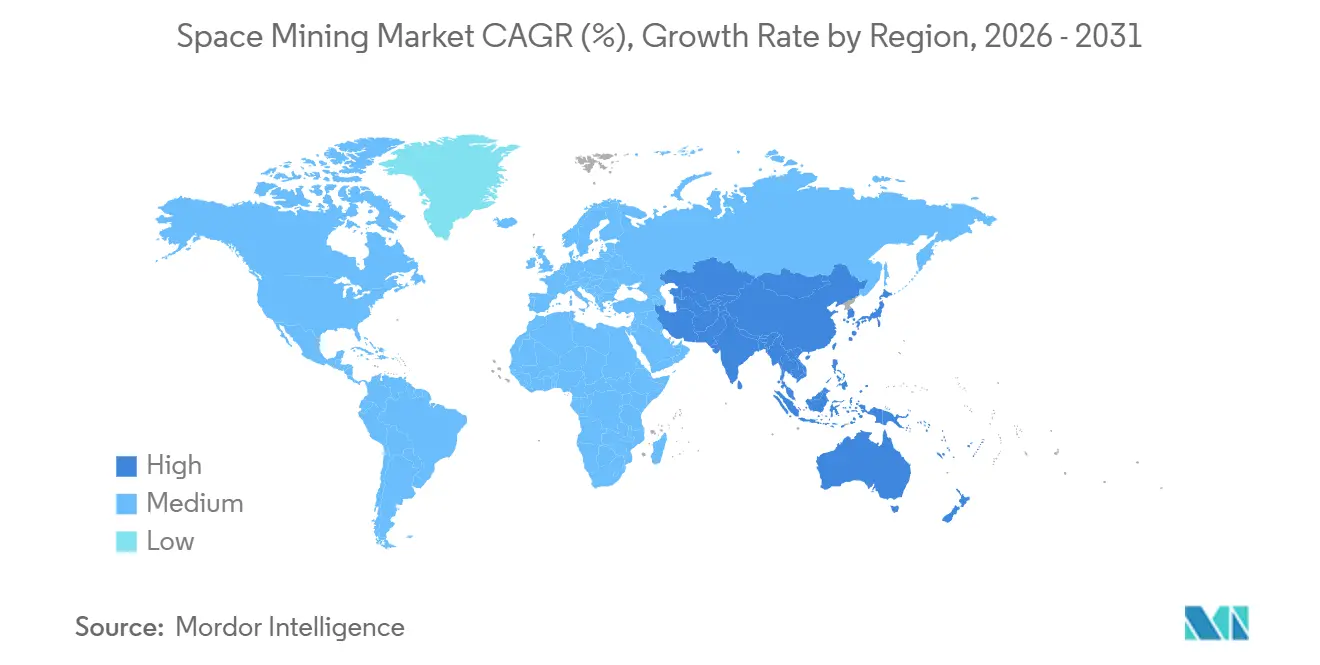

- By geography, North America led with a 36.12% share in 2025, while Asia-Pacific is projected to expand at a 23.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Space Mining Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid decline in launch costs | +4.2% | Global, acute in US and China | Short term (≤ 2 years) |

| Rising demand for PGMs and rare-earths in clean tech | +3.8% | Global, concentrated in OECD and China | Medium term (2-4 years) |

| Government ISRU funding and Artemis Accords | +3.1% | North America, Europe, Asia-Pacific signatories | Medium term (2-4 years) |

| Expansion of private ride-share launch services | +2.4% | Global, led by US commercial sector | Short term (≤ 2 years) |

| Micro-gravity additive manufacturing adoption | +2.9% | Global, early gains in US, China, Europe | Medium term (2-4 years) |

| Emerging off-earth ESG/carbon-credit schemes | +0.9% | Global, nascent regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in Launch Costs Unlocks Economically Viable Missions

Launch costs to low Earth orbit (LEO) fell sharply with reusable launch architectures, creating room for iterative hardware flight tests and phased technology maturation within the space mining market. SpaceX’s reusable Falcon 9 has set a new baseline for price and reliability, lowering the per-kilogram threshold and enabling smaller firms to field prospecting payloads on constrained budgets.[1]SpaceX Editorial Team, “Falcon 9,” SpaceX, spacex.com Private missions that once required agency-scale budgets can now demonstrate drills, spectrometers, and avionics in flight, thereby shortening development cycles and strengthening technical heritage. NASA’s payload-delivery model through Commercial Lunar Payload Services converts prospective mining workflows into funded missions that test landing precision, sampling, and near-surface characterization under contract. Examples such as AstroForge’s prospecting profile and follow-on plans illustrate how commercial teams translate low-cost access into targeted material reconnaissance in the space mining market. The combined effect is a structural drop in program risk per mission, which attracts capital to flight-proven systems that can scale toward in-situ extraction and processing.

Platinum-Group-Metal Deficits and Rare-Earth Shortages Intensify Resource Pressure

The platinum market recorded consecutive annual supply deficits into 2025, reflecting demand pressure from clean energy value chains and restrained output from legacy mines. Persistent deficits sharpen the strategic rationale for diversifying into off-Earth sources, particularly as technology roadmaps for hydrogen and electrification continue to add to demand for catalytic and magnetic materials. Commercial expressions of demand are taking shape at the premium end of materials markets, with helium-3 supply agreements for quantum systems signaling readiness to contract for scarce inputs once credible production emerges. Sustained shortages translate into stronger pricing power for reliable suppliers, which supports early capacity investments in exploration and in-situ processing that the space mining market requires. At the same time, environmental and social constraints on Earth-based expansion heighten the appeal of alternative sources that do not entail land disturbance or community impacts at mine sites, adding a non-price dimension to procurement strategy. The overall dynamic channels capital toward space-enabled material options that can either serve in-orbit demand or be returned when economics permit, strengthening the mid-term case for diversified off-Earth feedstocks within the space mining market.

Government ISRU Funding and Artemis Accords Reduce Regulatory Uncertainty

Policy clarity and procurement commitments lower barriers for commercial operators in the space mining market. The Artemis Accords, which reached 61 signatories by January 2026, affirm that resource extraction is compatible with the Outer Space Treaty’s principles and introduce transparent safety-zone practices that reduce operational conflict.[2]NASA Staff, “The Artemis Accords,” National Aeronautics and Space Administration, nasa.gov NASA’s Commercial Lunar Payload Services allocates multi-year budgets to deliver payloads to the Moon, underwriting precision landing, surface operations, and early in-situ resource utilization experiments. Firefly Aerospace’s awards and mission cadence under CLPS show how milestone-based payments de-risk development for lander and surface systems while generating data relevant to extraction workflows. Parallel investments in ISRU technologies, including lunar propellant plant concepts tracked in NASA’s TechPort, create a technology pipeline for oxygen, hydrogen, and related co-products that underpin in-space logistics. This policy and funding alignment provides private teams with clearer operating assumptions, supports recurring missions, and lays a foundation for scaled activity in the space mining market.

Microgravity Additive Manufacturing Enables Closed-Loop Resource Processing

ISRU methods and microgravity manufacturing form a complementary stack that reduces Earth dependence for structures and consumables in the space mining market. Blue Origin’s Blue Alchemist program advanced a molten-salt electrolysis approach that extracts oxygen from lunar regolith and co-produces metals suitable for construction, aligning propellant production with structural material outputs.[3]Blue Origin Communications, “Blue Moon Mark 1 Lunar Lander,” Blue Origin, blueorigin.com NASA’s TechPort documentation on lunar propellant plant activities highlights process pathways and technology maturation that link resource extraction to fuel production for landers and tugs. Peer-reviewed work synthesizes ISRU options ranging from carbothermal reduction to ilmenite hydrogen reduction for oxygen and metal recovery, which can feed additive manufacturing systems in orbit or on the surface. As these unit operations converge, operators can fabricate landing pads, radiation berms, and replacement parts from local feedstock, thereby reducing launch mass and recurring resupply requirements. The economic effect is a progressive shift from export-oriented concepts to in-space value creation that compounds over time as each mission leaves behind proper infrastructure in the space mining market. This production model favors early movers who validate process reliability and build interoperable interfaces with power, data, and logistics networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extremely high CAPEX and technology risk | -4.1% | Global, acute in emerging markets | Medium term (2-4 years) |

| Uncertain legal and regulatory framework | -2.3% | Global, particularly non-Artemis signatories | Long term (≥ 4 years) |

| Commodity-price volatility and ROI risk | -1.9% | Global, commodity-dependent regions | Short term (≤ 2 years) |

| Space-debris collision hazards | -1.2% | Global, concentrated in LEO operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extreme CAPEX and Multi-Year Payback Periods Strain Project Finance

Demonstration-scale extraction, refining, and logistics systems carry capital intensity and reliability requirements that outstrip traditional project-finance risk tolerances in the space mining market. NASA’s CLPS structure mitigates some exposure through milestone payments tied to clear deliverables, helping teams like Firefly convert early achievements into larger task orders. Even so, long development cycles and the need for reliable thermal, power, and robotic subsystems push breakeven horizons beyond conventional private-debt appetite. Peer-reviewed techno-economic work shows how investment outcomes hinge on discount rates shaped by legal and operational risk, which can swing a project’s net present value from positive to negative when uncertainty is high. As a result, blended finance and sovereign anchor tenancy dominate early phases, while commercial offtake appears first in premium niches like helium-3 for quantum research that tolerate higher prices. The financing constraint caps the number of concurrent projects and slows the rate at which the space mining market can move from experiments to steady-state operations.

Legal Ambiguity Over Property Rights Deters Institutional Investment

Although multilateral consensus has improved, cross-border divergence over property rights continues to elevate legal-risk premiums in the space mining market. The Artemis Accords clarify that resource extraction aligns with existing treaty principles and outline mechanisms to deconflict activities through safety zones, which lowers uncertainty for signatories. However, the absence of a universally accepted dispute-resolution regime or binding arbitration for resource claims keeps transaction costs high for large pools of capital. Techno-economic simulations show that higher discount rates associated with legal risk can erode value even in scenarios with promising operational parameters, underscoring the importance of policy clarity. Companies and agencies respond by structuring missions under clear national regimes and by emphasizing transparency to build precedents that will inform future norms. Until a broader multilateral framework emerges or case law accumulates through incident-free operations, institutional investors will price in legal uncertainty, constraining how fast the space mining market can scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Construction Gains as Permanent-Base Timelines Compress

Construction-oriented ISRU is gaining prominence as agencies and contractors focus on durable surface infrastructure to support recurring missions in the space mining market. Mission designs now include regolith-based materials for landing pads and berms to mitigate dust hazards during arrivals. Blue Origin’s Blue Alchemist program highlights this shift by combining oxygen extraction with the production of metal outputs for construction-grade components. NASA’s CLPS payload procurements are enabling tests of excavation and regolith handling at representative sites, refining equipment designs for construction. These developments reduce resupply mass and costs, positioning construction as a key enabler for sustained presence and extraction campaigns in the space mining market.

Process reliability and modularity are critical for ISRU adoption across various sites and mission architectures. ISRU units for oxygen and metal co-production integrate into systems designed to survive lunar nights, influencing equipment formats. NASA’s TechPort entries outline performance targets for oxygen and hydrogen production and address thermal integration challenges. Early missions also inform dust-mitigation and component-hardening strategies. As fabrication improves, operators aim to locally produce spare parts and fixtures, reducing external dependencies and shifting toward on-site manufacturing of core infrastructure, enhancing value capture within the space mining market.

By Resource Type: Strategic Metals Gain Traction as Clean-Tech Demand Tightens Supply

Resource prioritization focuses on water and volatiles for in-space logistics and strategic metals for high-value terrestrial and in-orbit uses. Water and oxygen are critical for propellant production, life support, and lunar logistics. NASA’s missions target polar volatiles, reducing uncertainties in ISRU yields. Strategic materials like helium-3 and PGMs are gaining traction due to premium pricing and clear offtake signals. Bluefors’ agreement with Interlune highlights buyer interest, improving bankability for extraction systems. The space mining market will initially see water and volatiles dominate, with strategic metals expanding as offtake certainty grows.

Resource extraction processes include molten-salt electrolysis, carbothermal reduction, and hydrogen reduction of ilmenite, validated in pilot contexts. These methods support additive manufacturing or storage systems based on mission needs. Committed buyers for strategic materials add resilience to revenue models. As missions refine composition maps, operators can better align hardware with resource profiles, reducing risks in the space mining market. Sovereign procurement and commercial contracts will influence which resources achieve operational maturity first.

By Extraction Target Body: Lunar Regolith Closes the Gap as Polar Infrastructure Matures

Near-Earth asteroids accounted for 52.78% of 2025 activity, highlighting their role in early prospecting and demonstration missions in the space mining market. Meanwhile, the Moon’s proximity and growing infrastructure are driving activity toward polar regolith. Recurring CLPS flights enable the delivery of drills, spectrometers, and processing units, reducing development cycles. As navigation aids and surface power systems expand, barriers to sustained operations decrease, favoring lunar regolith extraction. This shift rebalances the roadmap toward sites with higher mission cadence, while asteroid opportunities remain part of long-term strategies.

Lunar regolith is projected to grow at a 26.74% CAGR through 2031, driven by infrastructure gains and mission frequency. In-situ propellant concepts and construction ISRU lower costs for follow-on sorties. NASA’s polar missions seed landers and ISRU-relevant payloads, while technology programs set performance targets for fuel production. Operators integrating mobility, excavation, and thermal management can efficiently scale extraction. The space mining market benefits from modular expansion, leveraging shared utilities. Early systems demonstrating consistent throughput could shift portfolio focus toward lunar regolith, supporting risk-managed scaling.

By Mission Phase: Operations and Logistics Expand as the Sector Industrializes

Spacecraft design and engineering accounted for 44.92% in 2025, reflecting heavy up-front investment to master precision landing, surface mobility, and autonomous operations in challenging environments within the space mining market. NASA’s CLPS awards demonstrate how public buyers use milestone payments to catalyze these capabilities and transition suppliers from prototypes to recurring services. Firefly’s lunar landing builds confidence in commercial end-to-end delivery that combines transit, landing, and surface operations under a single provider, aligning directly with extraction workflows. As landers mature, payload integration and mission assurance improve, reducing rework and strengthening the business case for mining-centric sorties. The early dominance of design spend is giving way to a larger share for operations and logistics as mission counts rise in the space mining market.

Mining operations and logistics are set to grow fastest as lander reliability and payload integration reach commercial thresholds. This includes excavation, sample handling, in-situ processing, and cislunar transport and depot refueling once propellant becomes available. NASA TechPort entries for propellant plants and related ISRU systems show the target performance and system integration work underway to bridge from demonstration to industrial cadence.[4]NASA TechPort Team, “Lunar Propellant Production Plant (LP3-TP),” National Aeronautics and Space Administration, nasa.gov Blue Origin’s engineering on surface systems complements lander development, an example of vertical alignment that can compress interface risk for customers. As operations standardize, supply contracts with downstream users, such as helium-3 customers in quantum computing, can be written with clearer service levels and delivery parameters. This progression signals a maturing supply chain in the space mining market, where recurring revenue from operations complements up-front design work.

Geography Analysis

North America accounted for 36.12% of 2025 activity, driven by repeated landings and surface campaigns aligned with in-situ resource utilization goals in the space mining market. The United States’ contracting model accelerates hardware learning curves and expands the supplier base for extraction-relevant payloads. Commercially led surface operations complement agency science objectives and ISRU demonstrations. Lower orbital access costs enable frequent test flights and iterative product cycles across North American suppliers. The region’s base in deep-tech venture capital, aerospace primes, and defense interest in on-orbit refueling further supports demand visibility. Focus on helium-3 with offtake-linked development adds a private-sector pull for strategic materials that aligns with sovereign infrastructure plans. These elements help a steady cadence of missions and technology maturation that reinforce North America’s role in the near term.

Asia-Pacific is the fastest-growing region with a projected 23.62% CAGR through 2031, supported by programmatic funding for high-precision polar landings and private-sector partnerships in resource characterization. Sovereign commitment to targeted surface operations illustrates the region’s focus on advancing navigation, hazard avoidance, and sampling capabilities. Growing interest in polar volatiles and surface construction techniques positions the region to deliver interoperable elements that plug into broader cislunar logistics. The combination of agency-led programs and private teams focused on specialty materials should keep Asia-Pacific on a high growth path through the decade. Supplier ecosystems benefit as recurring lander missions simplify integration and standardize payload interfaces. With mission cadence rising, the Asia-Pacific space mining market is building asset bases that reduce barriers to extraction pilots.

Europe maintained a meaningful presence in 2025 through programs and national initiatives that prioritize sustainable operations and technology validation in the space mining market. Sustainability initiatives shape debris mitigation and mission design norms that will affect long-duration extraction assets. The region’s technical capabilities in in-situ manufacturing and materials research complement ISRU process development and lander operations. European suppliers also contribute to instrument payloads and ground segment services that support lunar missions. As standard-setting gains importance, Europe’s focus on sustainability may confer long-term advantages in licensing and insurance for extraction operators. Commercial activity continues to benefit from partnerships that position European firms as technology providers to global missions. The space mining market in Europe is growing at a measured pace, constrained by procurement fragmentation, but the region’s engineering depth remains a strategic asset.

Competitive Landscape

The competitive field in 2025-2026 is moderately fragmented, with state-backed contractors and venture-funded startups competing across landers, ISRU subsystems, and early offtake niches in the space mining market. NASA’s CLPS awards created a cohort of US providers that combine delivery services with surface operations, advancing readiness for extraction payloads.[5]NASA Staff, “Commercial Lunar Payload Services,” National Aeronautics and Space Administration, nasa.gov Firefly Aerospace’s mission milestones add proof points for commercially led landing and surface activity that feed directly into mining workflows. Vertical integration strategies are emerging, with operators investing in both landers and ISRU processes to control mission-critical interfaces. The space mining market rewards teams that demonstrate repeatable landings, robust surface operations, and clear pathways to in-situ processing.

Blue Origin exemplifies vertical integration through parallel development of landers and ISRU processes that can convert regolith into oxygen and metals, a configuration that links transportation with resource processing. NASA-backed technology programs provide performance targets for propellant production and system integration, which suppliers align with to win roles in future missions. Interlune’s offtake agreements with Bluefors anchor a materials-led route to commercialization that bypasses commodity-grade bulk exports in favor of specialty products, a model well suited to the space mining market’s early phase. AstroForge’s prospecting plans highlight how lean mission profiles can close the loop between reconnaissance and targeted extraction pilots. These strategies converge on the same goal: securing reliable mass payback across multiple flights.

As launch and delivery commoditize, differentiation shifts to post-landing reliability, throughput of resource handling, and the quality of data on deposit characteristics in the space mining market. NASA’s CLPS cadence and transparent contracting terms favor operators that can deliver on schedule with high mission assurance. Suppliers that combine robust surface systems with interoperable power and data interfaces should gain share as customers seek modular, scalable solutions. The presence of premium offtakers in quantum and advanced materials provides a buffer against commodity price swings during the build-out phase. Over the medium term, the space mining market will likely reward firms that convert mission heritage into multi-year service contracts that amortize R&D and integrate with shared cislunar infrastructure.

Space Mining Industry Leaders

Off-World, Inc.

Asteroid Mining Corporation

AstroForge

ispace, inc.

Moon Express, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ispace, Inc., a global lunar exploration company, announced its selection to implement the "High Precision Landing Technology in the Lunar Polar Regions" project under the second phase of Japan's Space Strategy Fund. This technology will be utilized in ispace's Mission 6, with development currently in progress.

- January 2026: The Sultanate of Oman became the 61st nation to sign the Artemis Accords, a US-led non-binding multilateral framework aimed at guiding sustainable and responsible civil space exploration.

- March 2025: The China University of Mining and Technology revealed a six-legged space-mining robot designed for lunar and asteroid anchoring tests in simulated low-gravity environments.

Global Space Mining Market Report Scope

Space mining is the exploitation of materials from the moon, other planets in the solar system, their satellites, asteroids, and near-Earth objects. The market demand has been estimated based on firm investments and revenues.

The space mining market is segmented by application, resource type, extraction target body, mission phase, and geography. By application, the market includes extraterrestrial commodities, construction, human life sustainability, fuel mining, and 3D printing. By resource type, it is categorized into water and volatiles, rare-earth and platinum group metals, and structural elements. By extraction target body, the market covers near-Earth asteroids (NEAs), main-belt asteroids, lunar regolith, and Mars moons (Phobos, Deimos). By mission phase, it is divided into spacecraft design and engineering, launch services, and mining operations and logistics. The report covers market sizes and forecasts for the space mining market across major countries in different regions. For each segment, the market size is provided in terms of value (USD).

| Extraterrestrial Commodity |

| Construction |

| Human Life Sustainability |

| Fuel Mining |

| 3D Printing |

| Water and Volatiles |

| Rare-Earth and Platinum Group Metals (PGMs) |

| Structural Elements |

| Near-Earth Asteroids (NEAs) |

| Main-Belt Asteroids |

| Lunar Regolith |

| Mars Moons (Phobos, Deimos) |

| Spacecraft Design and Engineering |

| Launch Services |

| Mining Operations and Logistics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Extraterrestrial Commodity | ||

| Construction | |||

| Human Life Sustainability | |||

| Fuel Mining | |||

| 3D Printing | |||

| By Resource Type | Water and Volatiles | ||

| Rare-Earth and Platinum Group Metals (PGMs) | |||

| Structural Elements | |||

| By Extraction Target Body | Near-Earth Asteroids (NEAs) | ||

| Main-Belt Asteroids | |||

| Lunar Regolith | |||

| Mars Moons (Phobos, Deimos) | |||

| By Mission Phase | Spacecraft Design and Engineering | ||

| Launch Services | |||

| Mining Operations and Logistics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and growth outlook for the space mining market?

The market size of the space mining market is USD 3.07 billion in 2026 and is projected to reach USD 7.39 billion by 2031 at a 19.21% CAGR.

Which policy frameworks most reduce legal risk for space resource extraction?

The Artemis Accords clarify that resource extraction aligns with existing treaty principles and promote transparent safety zones, which lower legal uncertainty for signatories.

What near-term technologies are most critical to scaling the space mining market?

Precision landing, surface mobility, and ISRU processes such as molten-salt electrolysis for oxygen and metals, plus propellant plant integration and additive manufacturing, are central to scaling operations.

Which regions are leading and which are growing fastest in the space mining market?

North America led in 2025 supported by NASA’s CLPS program, while Asia-Pacific is the fastest-growing region through 2031 as Japan advances high-precision polar landing capabilities.

How are companies turning early missions into commercial traction?

Teams combine CLPS-backed deliveries with ISRU demonstrations and offtake-linked strategies, such as helium-3 supply agreements, to lower financing risk and build recurring operations in the space mining market.

What risks most constrain investment in the space mining market?

High CAPEX, long payback periods, and legal uncertainty over property rights elevate discount rates and slow scaling, though milestone-based public funding and policy clarity help mitigate these factors.

Page last updated on: