Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

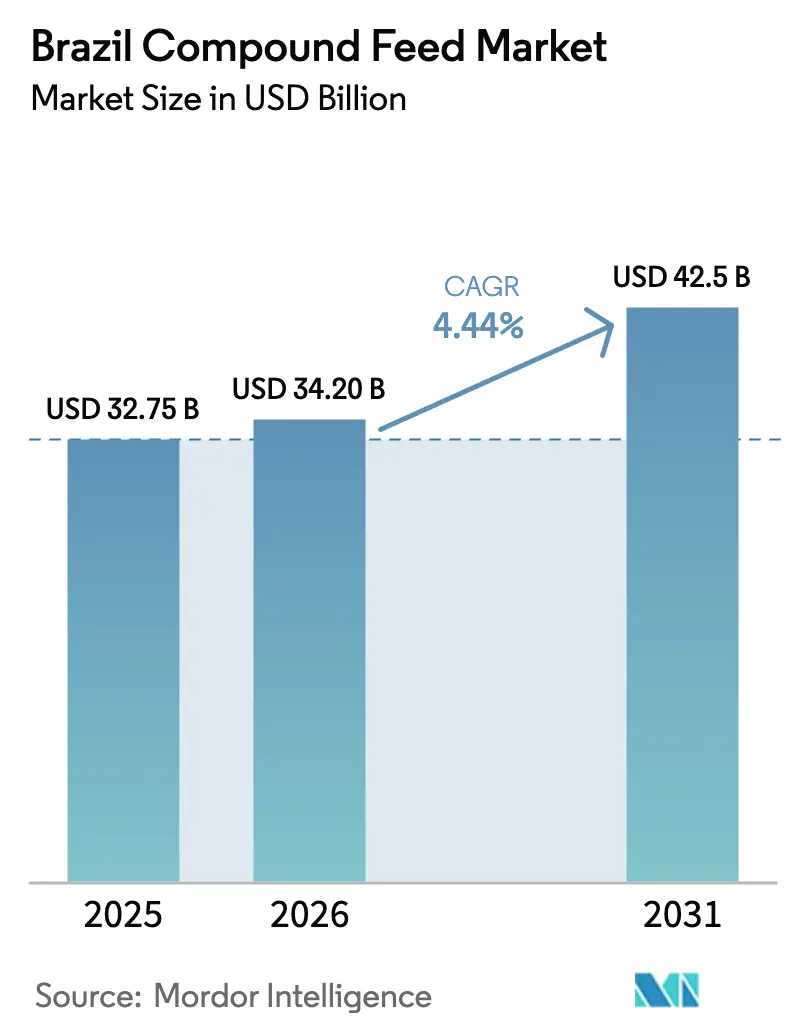

| Base Year Market Size (2025) | USD 32.75 Billion |

| Market Size (2026) | USD 34.20 Billion |

| Market Size (2031) | USD 42.5 Billion |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Compound Feed Market Analysis by Mordor Intelligence

The Brazil compound feed market was valued at USD 32.75 billion in 2025 and estimated to grow from USD 34.20 billion in 2026 to reach USD 42.50 billion by 2031, at a CAGR of 4.44% during the forecast period (2026-2031). Strong grain harvests, captive feed capacity within poultry and swine integrators, and increasing protein consumption among urban households provide a stable demand foundation, mitigating the impact of cyclical fluctuations in global commodity prices. Continued poultry and pork exports support production levels, while the adoption of specialty feed additives and precision nutrition technologies enhances average selling prices by improving efficiency. Government-subsidized credit facilitates mill modernization efforts, even amid depreciation of the Brazilian real, while the growing cost advantage of Brazilian corn over United States corn further strengthens the country's global competitiveness.

Key Report Takeaways

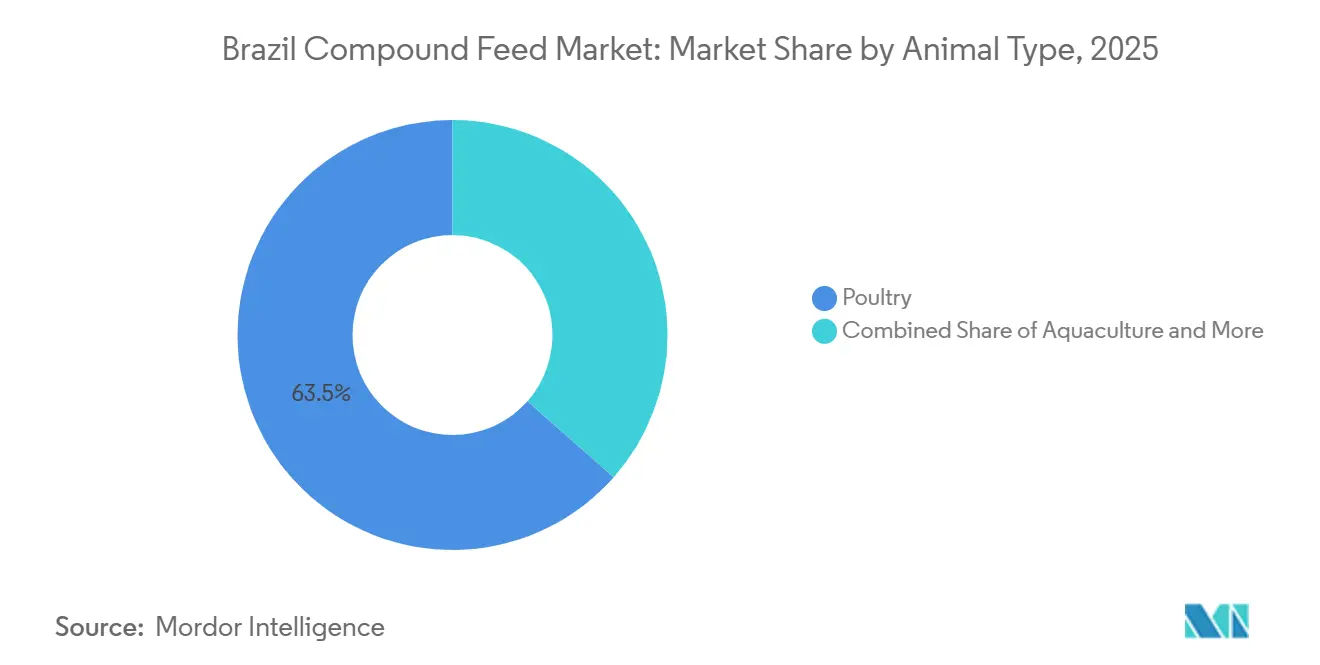

- By animal type, poultry feed accounted for 63.5% of the Brazil compound feed market size in 2025, while aquaculture is projected to expand at a 4.3% CAGR through 2031.

- By ingredient, cereals accounted for a 72.1% share in 2025, and supplements are poised to register a 4.7% CAGR during the forecast years.

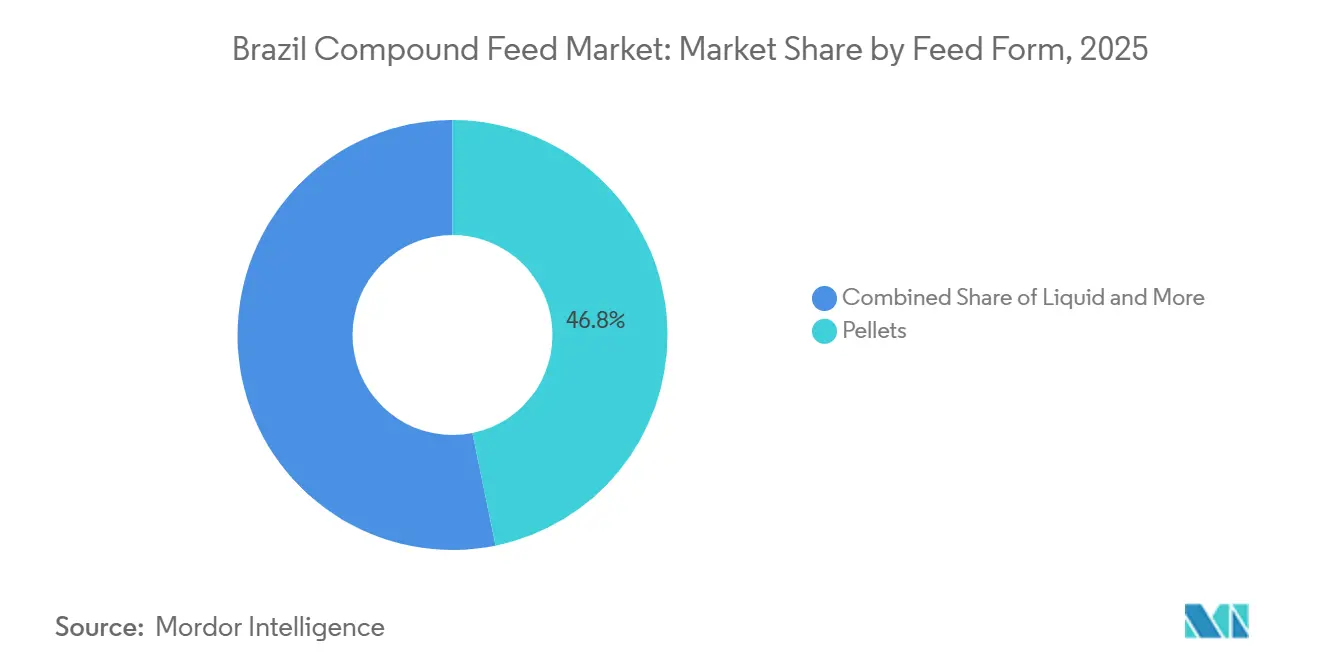

- By feed form, pellets led with 46.8% of the 2025 market size, whereas liquid feed is forecast to grow at a 3.5% CAGR through 2031.

- By functionality, conventional feed captured 74.5% of the 2025 market, yet antibiotic-free formulations are projected to post a 4.2% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Compound Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming poultry and pork export volumes | +0.90% | South and Southeast states | Medium term (2–4 years) |

| Competitive cost advantage from abundant domestic corn and soybean crops | +0.80% | Center West grain belt | Long term (≥ 4 years) |

| Growing domestic demand for animal protein | +0.60% | Urban centers nationwide | Medium term (2–4 years) |

| Adoption of precision-feeding technologies and on-farm data analytics | +0.50% | Large integrated operations nationwide | Medium term (2–4 years) |

| Surge in specialty feed additives | +0.40% | Premium poultry and aquaculture clusters | Short term (≤ 2 years) |

| Government incentives and support for livestock feeding | +0.30% | Rural credit corridors in South, Southeast, Center West | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Booming Poultry and Pork Export Volumes

Brazil’s poultry industry continues to expand its global presence, with shipments reaching record levels in recent years. The United States Department of Agriculture reports that Brazil's chicken meat exports rose from 4,447 thousand metric tons in 2022 to 4,770 thousand metric tons in 2023. Government trade reports highlight strong demand from Middle Eastern and Asian markets, where poultry enjoys a competitive edge. Pork exports have also strengthened, supported by sanitary certifications that open doors to high‑value destinations. Regulatory mandates from Asian countries encourage the use of enzyme-rich and probiotic feed blends, underscoring the importance of specialized additives[1]Source: U.S. Department of Agriculture, “Brazil Grain and Feed Update,” USDA Foreign Agricultural Service, usda.gov. Integrated processors maintain captive feed mills that stabilize costs and ensure a consistent supply. Government agricultural bulletins confirm that southern states remain the backbone of poultry feed output, benefiting from proximity to ports.

Competitive Cost Advantage from Abundant Domestic Corn and Soybean Crops

Brazil’s grain harvests underpin the feed industry’s cost advantage, with official crop reports showing consistent growth in corn and soybean output[2]Source: National Supply Company, “2024-2025 Grain Harvest Forecast,” conab.gov.br. Government agencies note that domestic feed prices remain well below international benchmarks, reinforcing competitiveness. Double‑cropping practices in central states reduce weather risks and secure grain availability for integrators. Soybean crushing capacity has expanded steadily, ensuring a stable supply of protein meal for feed manufacturers. Spot market data from government sources confirms that Brazilian corn trades at a significant discount compared with the United States equivalents. This cost gap directly supports livestock margins and strengthens Brazil’s global position in feed exports.

Growing Domestic Demand for Animal Protein

Government statistics indicate a rising per-capita meat intake, reflecting urbanization and higher disposable incomes. For instance, according to the Organisation for Economic Co-operation and Development (OECD), domestic per capita demand for swine meat was 17.5 kg in 2022, increasing to 18.6 kg in 2024. Beef and pork consumption also continues to grow, and poultry remains the most widely consumed protein, supported by its affordability and positive health perceptions[3]Source: Brazilian Animal Protein Association, “Annual Chicken Export Report 2024,” abpa-br.org. Quick‑service restaurants are expanding their purchases of chicken, driving demand for uniform portioning and strict feed specifications. Dairy intake has increased steadily, with government reports emphasizing the importance of high-energy rations in confined animal feeding operations (CAFOs).

Adoption of Precision Feeding Technologies and On-farm Data Analytics

Government agricultural research institutes report growing adoption of digital platforms that monitor livestock performance. These technologies reduce feed waste and improve efficiency, delivering measurable benefits to producers. Automated feeders are increasingly installed in large poultry operations. Near‑infrared sensors are being deployed to optimize feed formulations and reduce margin losses. Blockchain pilots with major processors are creating verifiable antibiotic‑free claims that enhance export competitiveness. In August 2023, Brazil's Ministry of Agriculture and Livestock introduced the 2023/2024 Crop Plan, allocating BRL 364.22 billion (approximately USD 60 billion) to support national agricultural and livestock development. Government extension services highlight aquaculture trials where precision feeding tools have lowered feed conversion ratios and reduced environmental impacts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile corn and soybean price cycles | -0.7% | Non-integrated mills nationwide | Short term (≤ 2 years) |

| Dependence on imported high-value additives | -0.5% | Enzyme and amino acid supply chains | Medium term (2–4 years) |

| Logistics bottlenecks in road and storage infrastructure | -0.4% | Center West and North corridors | Long term (≥ 4 years) |

| Currency devaluation pressure on equipment and premix imports | -0.3% | Capital expenditure pipelines nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dependence on Imported High-Value Additives

Government trade data confirm Brazil’s reliance on imported feed additives, with the majority of supplies sourced from major global regions. This dependence exposes buyers to freight volatility and currency fluctuations. Sharp increases in methionine prices and shortages of lysine have affected feed formulations. Domestic fermentation capacity remains limited, and new plant approvals require significant investment and regulatory clearance. Government agencies emphasize that near-term substitution of imports is unlikely, thereby maintaining high reliance. This structural dependence continues to shape Brazil’s feed industry strategy.

Logistics Bottlenecks in Road and Storage Infrastructure

Government infrastructure assessments highlight persistent challenges in road and storage capacity. Truck freight costs rise during harvest seasons as silo shortages force on‑farm storage solutions. Many highways in the Center West remain unpaved, adding delays and costs to feed delivery. Vessel queues at major ports increase waiting times, prompting mills to hold higher safety stocks. Government transport authorities confirm that these inefficiencies tie up working capital and raise storage burdens.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Poultry Sustains Leadership While Aquaculture Accelerates

Poultry feed sustained leadership in the Brazil compound feed market, holding 63.5% of revenue share in 2025. Export contracts and integrated milling systems reinforce its dominance, while vertical integration ensures ingredient consistency and compliance with international residue standards. Poultry remains the backbone of Brazil’s feed industry, supported by strong domestic consumption and global demand. Swine and ruminants continue to play supporting roles, but poultry’s scale and efficiency secure its position as the largest segment.

Aquaculture feed is emerging as the fastest‑growing category, advancing at a 4.3% CAGR through 2031. Rising tilapia and shrimp production across key regions drives this growth, supported by the establishment of new feed plants and improved logistics. Specialty formulations for companion animals are also expanding steadily, reflecting consumer preferences for premium nutrition. Confined dairy herds continue to support growth in ruminant feed, while the rapid rise of aquaculture signals Brazil’s expanding focus beyond conventional livestock. This evolution highlights how innovation and sustainability are becoming central drivers of future feed demand.

By Ingredient: Cereals Still Core While Supplements Capture Margin Upside

Cereals remained the core of Brazil’s feed industry, accounting for 72.1% of ingredient share in 2025. Corn remains a staple in monogastric diets, providing the majority of metabolizable energy. Oilseed meals and processing by‑products contribute to balanced rations, but cereals dominate due to availability and cost competitiveness. Cereals will remain central to feed formulations, ensuring stability in supply chains and supporting Brazil’s competitive edge in global protein markets.

Supplements are forecast to expand at a 4.7% CAGR through 2031, capturing margin upside as formulators invest in enzymes, amino acids, and probiotics. These additives enhance feed conversion and sustainability, aligning with export requirements and consumer preferences. Advances in synthetic nutrition and fermentation technologies enable mills to reduce their reliance on costly cereals while maintaining optimal performance. Supplements thus represent the fastest‑growing ingredient segment, reshaping Brazil’s feed industry toward higher efficiency and value‑added formulations.

By Feed Form: Pellet Dominance Coupled With Niche Liquid Feed Uptick

Pellets led the Brazil compound feed market with a 46.8% share in 2025, reflecting greater efficiency and lower waste than mash. Integrated processors continue to expand pellet capacity, reinforcing their role as the dominant feed form. Crumbles remain important for starter diets, while mash persists among smallholders due to lower upfront costs. Pellets will retain their leadership, supported by investments in conditioning technology and export-driven quality standards.

Liquid feed is the fastest‑growing form, advancing at a 3.5% CAGR through 2031. Precision feeding systems in dairy and swine operations drive adoption by incorporating by-products such as whey and molasses. Crumbles gain traction in aquaculture nurseries, while mash maintains relevance in traditional systems. The rise of liquid feed highlights Brazil’s shift toward specialized nutrition and efficiency, complementing pellet dominance and diversifying feed form strategies across species.

By Functionality: Conventional Still Majority While Antibiotic‑Free Gains Ground

Conventional feed formulations retained a 74.5% share in 2025, underscoring their continued importance in Brazil’s domestic market. Cost sensitivity and established practices sustain conventional dominance, even as export markets demand stricter compliance with residue limits. Medicated feed remains relevant for disease management, but regulatory tightening is reshaping its role in this context. Conventional feed will remain the majority segment, although its share will gradually decline as alternatives gain traction.

Antibiotic‑free feed is the fastest‑growing functionality, advancing at a 4.2% CAGR through 2031. Rising demand from European and Asian importers is driving zero-tolerance regimes, prompting mills to adopt enzyme and organic-acid solutions. Producers reformulate rations to meet these standards, maintaining performance while reducing reliance on medicated inputs. Antibiotic‑free growth reflects Brazil’s alignment with global sustainability and animal welfare trends, positioning the industry for long‑term competitiveness in premium export markets.

Geography Analysis

Brazil’s South and Southeast regions accounted for the largest share of the Brazil compound feed market size in 2025, with Paraná, Santa Catarina, and Rio Grande do Sul leading the production. These states benefit from strong port access, integrated poultry and swine complexes, and established grain contracting practices that stabilize costs and ensure consistent supply. Leveraging coastal logistics, established milling capacity, and long‑standing integration models, the South and Southeast remain the backbone of Brazil’s feed industry, supporting both domestic consumption and international shipments while reinforcing the country’s competitive position in global protein markets.

The Center West is the fastest‑growing region, supported by lower corn costs and expanding rail capacity that connect grain belts to export corridors. Investments by multinational feed companies strengthen its role as a rising hub, tilting production toward the interior where grain availability is abundant. Structural advantages in grain supply and logistics, combined with double‑cropping practices and modernized infrastructure projects that reduce freight costs, make the Center West increasingly attractive for integrators. As production shifts inland, the region is positioned to capture a larger portion of Brazil’s feed output and enhance national competitiveness.

The Northeast and North contribute smaller shares but show distinct dynamics that highlight regional diversity. The Northeast is experiencing rapid growth with the expansion of aquaculture, supported by government grants and new mill projects that reduce logistics costs for shrimp and tilapia farmers. The North lags behind due to high trucking costs and infrastructure constraints, which limit profitability in fish feed and delay technology adoption. Regional disparities are anticipated to persist, with growth concentrated in aquaculture‑focused zones. While the Northeast benefits from targeted investment and rising demand for aquatic protein, the North continues to face structural challenges that restrict its ability to scale feed production, leaving its role secondary in the national market.

Competitive Landscape

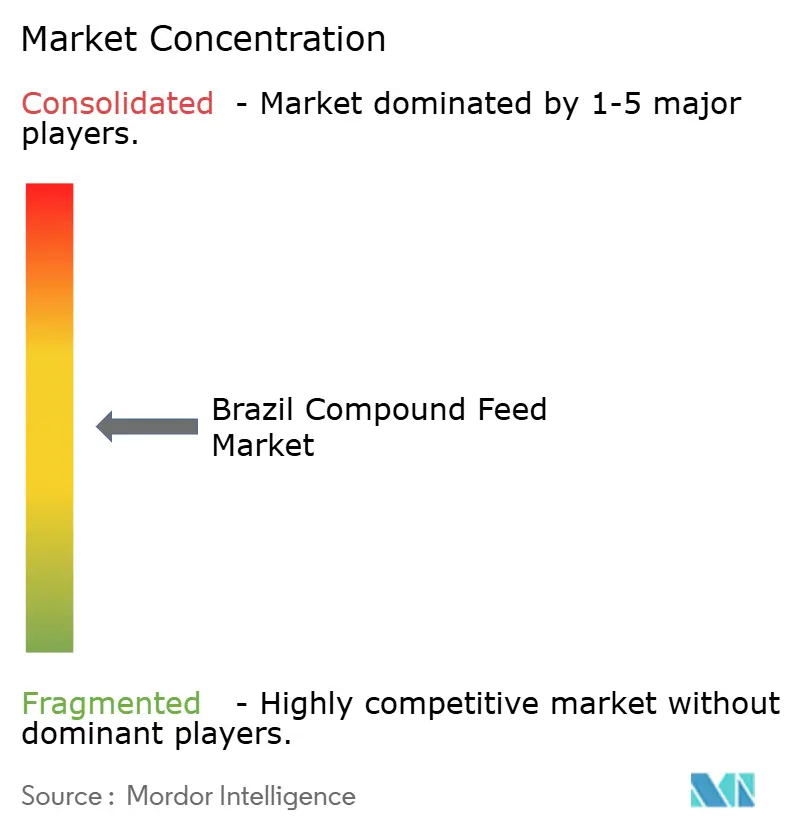

The Brazil compound feed market share remains moderately concentrated, with leading suppliers accounting for a significant portion of the value, while leaving room for smaller players to emerge. Multinational firms such as Archer Daniels Midland Company, Cargill, Incorporated, BRF S.A., Nutreco N.V. (a subsidiary of SHV Holdings N.V.), and Alltech, Inc. leverage integrated grain contracts and digital platforms to secure efficiency, compliance, and visibility across their supply chains. Concentration is projected to persist, although cooperatives and specialty firms will continue to retain opportunities to carve out niches. The balance between global corporations and local disruptors creates a dynamic competitive environment, where scale advantages coexist with innovation‑driven strategies. This moderate concentration ensures stability while allowing new entrants to differentiate through specialized formulations, sustainability credentials, and regional focus.

Regional disruptors emphasize organic and non-genetically modified supply, targeting premium European buyers who demand transparency and sustainability. Multinational additive vendors are localizing production to buffer against currency volatility, while sustainability‑focused innovations gain traction across cattle and aquaculture lines. The rise of localized premix hubs and fermentation facilities further strengthens resilience against global supply shocks. These strategies demonstrate how both cooperatives and multinational suppliers adapt to shifting consumer preferences, regulatory frameworks, and sustainability scorecards, thereby ensuring long-term competitiveness in diverse markets.

The competitive focus is increasingly shifting toward antibiotic‑free and aquaculture segments, reflecting global demand for cleaner protein and sustainable practices. Reformulation strategies, protected acids, and advanced enzymes demonstrate how innovation drives market share retention while meeting tightening residue protocols. As aquaculture expands and antibiotic‑free formulations gain traction, suppliers that prioritize research and development will secure long‑term advantages. This emphasis on innovation highlights the industry’s shift from volume-driven growth to value-added solutions, positioning Brazil as a leader in sustainable feed production.

Brazil Compound Feed Industry Leaders

Archer Daniels Midland Company

BRF S.A.

Nutreco N.V. (SHV Holdings N.V.)

Alltech, Inc.

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Cargill, Incorporated acquired MigPlus to strengthen its position in Brazil’s compound feed sector. The deal expands production capacity and enhances regional reach, supporting growth in animal nutrition and protein supply chains.

- May 2024: Innovad Group, a company in the compound feed market, acquired Oligo Basics, a Brazilian supplier of compound feed solutions. This acquisition expands Innovad Group's presence in Brazil and combines the product portfolios of both companies to provide integrated and natural feed solutions.

- January 2024: JBS S.A. invested in constructing three new feed factories in Seberi, Santo Inácio, and Itaiópolis in Southern Brazil. The investment aligns input supply with the production capacity of its Seara business unit, which expanded significantly in recent years through the company's investment plan. These new units increase Seara's annual feed production by more than 1 million metric tons.

Brazil Compound Feed Market Report Scope

Compound feed is a mixture of raw materials and supplements fed to livestock, sourced from either plant, animal, organic, or inorganic substances, or industrial processing, whether or not it contains additives. While soybean, corn, barley, wheat, and sorghum are the most commonly used raw materials, vitamins, minerals, and amino acids are the most common additives blended to form compound feed. The Brazil Compound Feed Market Report is Segmented by Animal Type (Poultry, Swine, Ruminants, Aquaculture, and Other Animals), by Ingredient (Cereals, Oilseed Meals, Processing By-Products, and Supplements), by Feed Form (Mash, Pellets, Crumbles, and Liquid), and by Functionality (Conventional, Medicated, and Antibiotic-Free). The Market Forecasts are Provided in Terms of Value in USD and Volume in Metric Tons.

By Animal Type

| Poultry |

| Swine |

| Ruminants |

| Aquaculture |

| Other Animals |

By Ingredient

| Cereals |

| Oilseed Meals |

| Processing By-products |

| Supplements |

By Feed Form

| Mash |

| Pellets |

| Crumbles |

| Liquid |

By Functionality

| Conventional |

| Medicated |

| Antibiotic-free |

| By Animal Type | Poultry |

| Swine | |

| Ruminants | |

| Aquaculture | |

| Other Animals | |

| By Ingredient | Cereals |

| Oilseed Meals | |

| Processing By-products | |

| Supplements | |

| By Feed Form | Mash |

| Pellets | |

| Crumbles | |

| Liquid | |

| By Functionality | Conventional |

| Medicated | |

| Antibiotic-free |

Key Questions Answered in the Report

What is the projected value of the Brazil compound feed market in 2031?

The Brazil compound feed market size is forecast to reach USD 42.5 billion by 2031.

Which species accounts for the largest share of feed volume?

Poultry leads with 63.5% of total volume in 2025, reflecting Brazil’s role as the top global chicken exporter.

How are corn and soybean costs affecting feed profitability?

Domestic corn trades at roughly USD 3.20 per bushel, a 33% discount to United States quotes, lowering energy costs and boosting margins.

What growth rate is projected for antibiotic-free formulations?

Antibiotic-free feed is advancing at a 4.2% CAGR through 2031, as European and Asian buyers tighten residue limits.

Page last updated on: