Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

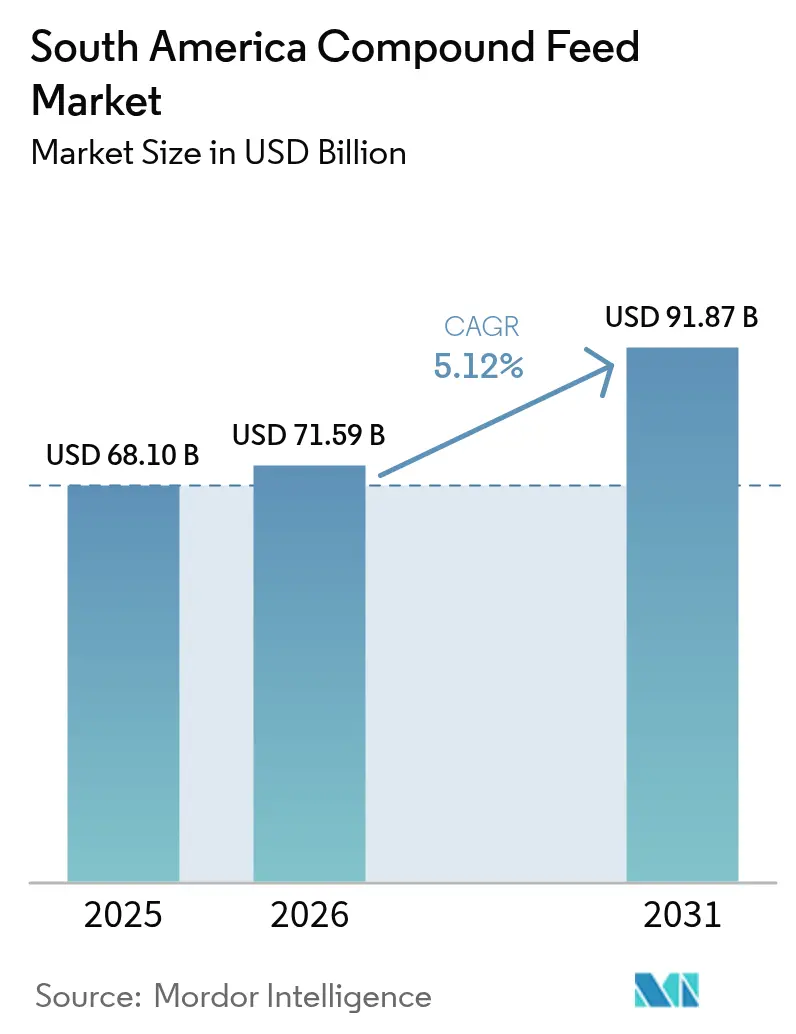

| Base Year Market Size (2025) | USD 68.1 Billion |

| Market Size (2026) | USD 71.59 Billion |

| Market Size (2031) | USD 91.87 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Compound Feed Market Analysis by Mordor Intelligence

South America compound feed market size in 2026 is estimated at USD 71.59 billion, growing from 2025 value of USD 68.1 billion with 2031 projections showing USD 91.87 billion, growing at 5.12% CAGR over 2026-2031. Strong export-oriented poultry, pork, and beef supply chains are integrating backward into nutrition to secure consistent quality and hedge against fluctuations in commodity costs. Brazil’s fast-track approval process for enzymes and probiotics gives early adopters a cost advantage, while Argentine integrators rely on forward grain contracts to mitigate currency risk. Aquaculture’s rapid expansion, tightening antibiotic-residue limits, and carbon-linked certifications further diversify demand, favoring mills that invest in functional additives and traceable soy. Competitive intensity is moderate, with scale economies, research and development partnerships, and sustainability credentials shaping strategy across the South America compound feed market.

Key Report Takeaways

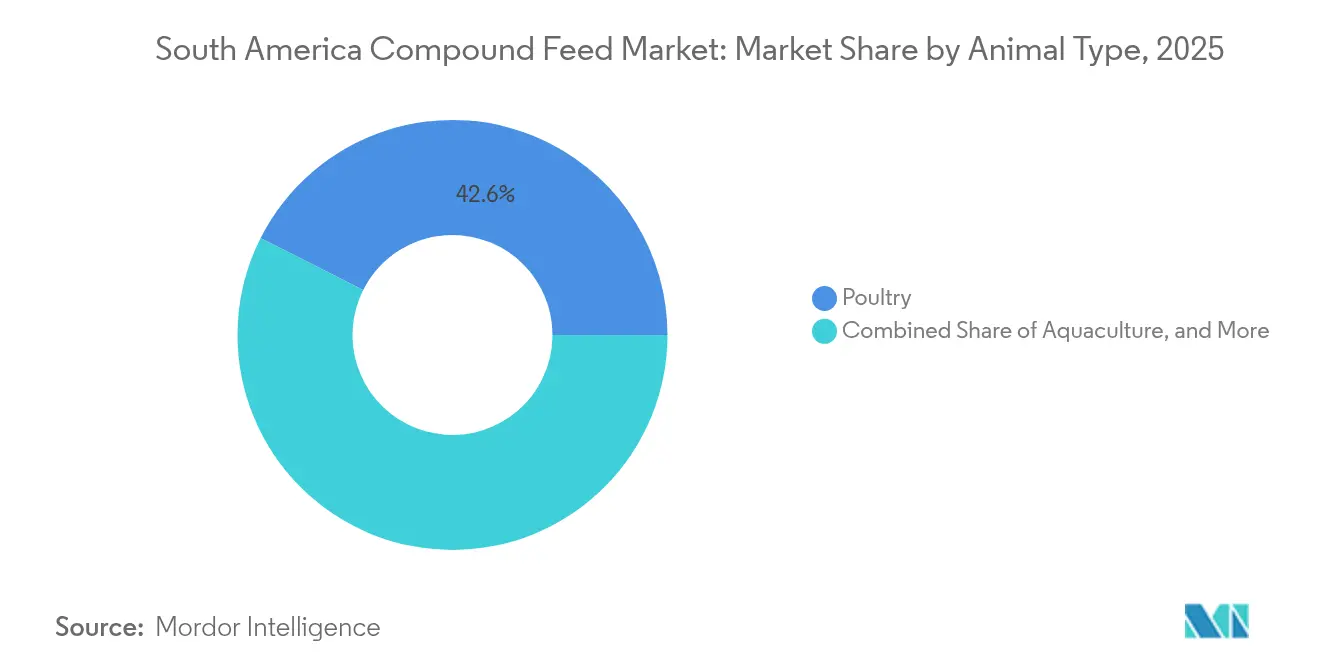

- By animal type, poultry led with 42.55% of South America compound feed market size in 2025, while aquaculture is forecast to expand at a 7.42% CAGR to 2031.

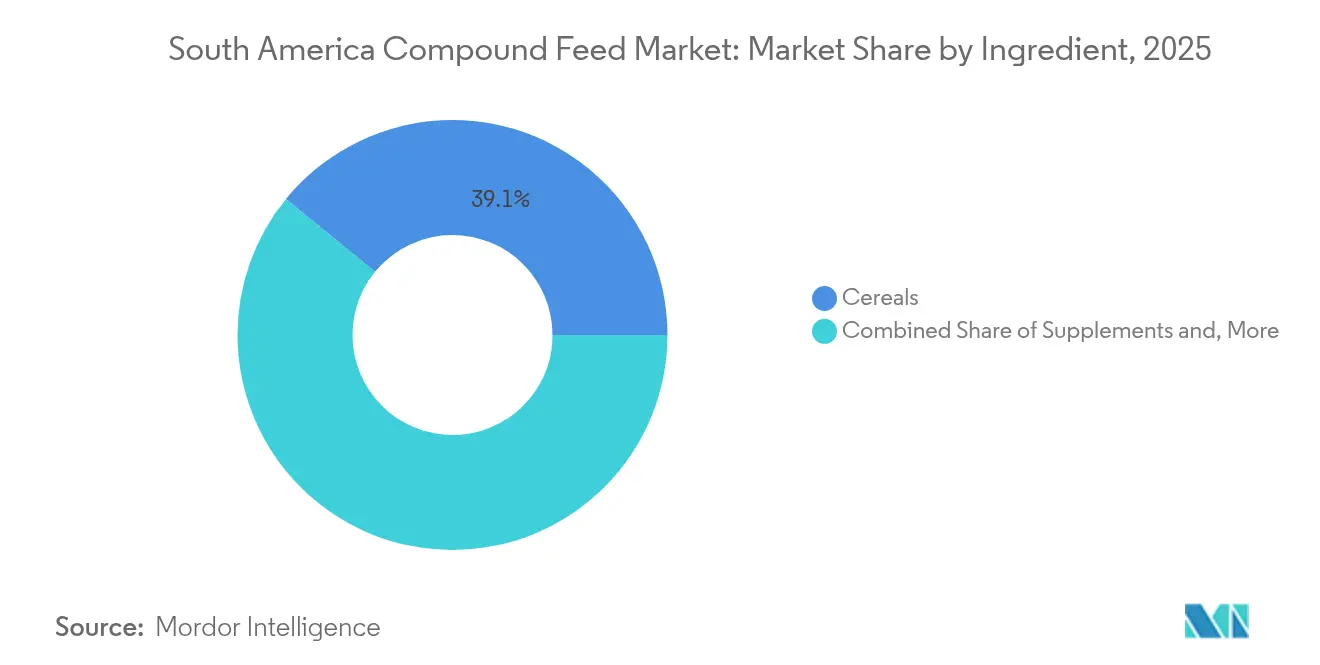

- By ingredient, cereals accounted for a 39.10% share of the South America compound feed market size in 2025, and supplements are projected to advance at an 7.68% CAGR through 2031.

- By geography, Brazil accounted for 61.65% of the 2025 revenue, and Argentina is poised to grow at a 5.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Compound Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (+) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising livestock production and export demand | +1.2% | Brazil dominance, with spillover to Argentina and Paraguay | Medium term (2-4 years) |

| Adoption of nutritional and specialty feed additives | +0.9% | Brazil and Argentina core, expanding to Chile and Colombia | Long term (≥ 4 years) |

| Government programs that incentivize animal protein supply chains | +0.7% | Brazil federal and state programs, Argentina provincial credits | Short term (≤ 2 years) |

| Expansion of integrated feed milling capacity | +0.8% | Brazil southern states, Argentina pampas region | Medium term (2-4 years) |

| Aquaculture boom in Amazon basin and coastal fisheries | +0.6% | Brazil northern states, Ecuador and Chile coastal zones | Long term (≥ 4 years) |

| Carbon-credit linked sustainable feed initiatives | +0.4% | Brazil and Argentina pilot projects, with EU buyer linkage | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Livestock Production and Export Demand

Brazil exported 4.9 million metric tons of chicken meat in 2024, solidifying its position as the world's leading exporter and creating a structural demand for high-performance broiler feed [1]Source: United States Department of Agriculture Foreign Agricultural Service, “Brazil Chicken Meat Exports,” usda.gov. This export intensity compels integrators to optimize feed conversion ratios below 1.60, a threshold that necessitates the precise formulation of amino acids and enzymes. Argentina's pork shipments to China rebounded in 2024 after disruptions from African swine fever eased, prompting local millers to expand their swine-feed lines with synthetic lysine and threonine blends. The feedback loop between export competitiveness and feed quality means that any disruption in ingredient supply or formulation consistency immediately erodes margin at the farm gate. Cattle ranching in Brazil's Center-West continues to intensify, with feedlot finishing now accounting for over 30% of the slaughter volume. This shift replaces pasture grazing with concentrated rations, driving demand for high-energy pellets.

Adoption of Nutritional and Specialty Feed Additives

Enzyme inclusion rates in poultry feed exceeded 85% penetration in Brazil's southern states in 2024, reflecting a strategic shift toward phytase and xylanase combinations that unlock phosphorus and energy from plant-based ingredients. This trend reduces reliance on inorganic phosphate supplements, which are subject to price volatility tied to global fertilizer markets. Probiotic strains, such as Bacillus subtilis and Lactobacillus acidophilus, gained traction in swine rations after field trials demonstrated improved gut health and reduced mortality in weanling pigs. The regulatory pathway for novel additives in Brazil follows Ministry of Agriculture guidelines that require efficacy data from local trials, a barrier that favors multinational ingredient suppliers with established research infrastructure.

Government Programs That Incentivize Animal Protein Supply Chains

Brazil's National Program for Agricultural Credit (Pronaf) allocated BRL 71 billion (USD 14.2 billion) in 2024 for rural financing, with a dedicated line for feed mill modernization that carries interest rates 4 percentage points below commercial benchmarks. This subsidy structure enables regional cooperatives to install automated batching systems and expand storage capacity, narrowing the operational gap with multinational competitors. Argentina's provincial governments in Córdoba and Santa Fe extended tax exemptions on feed-ingredient imports through 2025, a measure designed to offset the inflationary impact of currency devaluation on input costs. These fiscal incentives lower the effective cost of feed production, resulting in improved farm-level profitability and higher livestock retention rates.

Expansion of Integrated Feed Milling Capacity

JBS S.A. and BRF S.A. companies collectively operate 32 feed mills across Brazil, with a combined annual capacity exceeding 12 million metric tons, a scale that allows them to negotiate volume discounts on corn and soybean meal directly with crushing plants. This vertical integration model insulates these firms from spot-market price spikes and enables them to formulate rations tailored to proprietary poultry and swine genetics. Cargill commissioned a 500,000-metric-ton feed facility in Mato Grosso in late 2024, positioning the plant within 200 kilometers of major soybean-crushing operations and reducing inbound freight costs by an estimated 8%. The strategic logic behind these mega-mills is straightforward: fixed costs per ton decline as throughput increases, and proximity to ingredient sources reduces the working capital tied up in inventory. Smaller commercial mills face a structural disadvantage in this environment, as they lack the balance-sheet capacity to forward-contract grain on a large scale or invest in automation that reduces labor intensity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in commodity and feed ingredient prices | -0.8% | Brazil and Argentina soy-corn belt, import-dependent markets | Short term (≤ 2 years) |

| Stringent environmental and land-use regulations | -0.5% | Brazil Amazon and Cerrado regions, Argentina northern provinces | Medium term (2-4 years) |

| Logistics bottlenecks and port congestion | -0.3% | Brazil Santos and Paranaguá ports, Argentina Rosario corridor | Short term (≤ 2 years) |

| Consumer shift toward plant-based protein | -0.2% | Urban centers in Brazil, Argentina, and Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Commodity and Feed Ingredient Prices

Corn futures on the Chicago Board of Trade traded in a USD 4.20 to USD 5.80 per bushel range during 2024, a 38% swing that forced feed millers to adjust formulations weekly to maintain target margins. Soybean meal prices in Brazil's domestic market surged to BRL 2,400 per metric ton (USD 480 per metric ton) in mid-2024, following a drought in Rio Grande do Sul that reduced crushing volumes by 18%. This price volatility compresses feed margins because livestock contracts are often locked in months ahead of delivery, leaving millers exposed to input-cost inflation without a corresponding revenue adjustment. The financial strain is most acute for commercial mills serving independent farmers, as these customers lack the balance-sheet flexibility to absorb sudden feed-price increases and may delay orders or switch to lower-cost rations that compromise animal performance. Integrated producers partially mitigate this risk by hedging their grain purchases through futures contracts, but this strategy requires treasury expertise and capital reserves that smaller players often cannot afford.

Stringent Environmental and Land-Use Regulations

Brazil's Forest Code requires rural properties in the Amazon biome to maintain 80% native vegetation cover, a mandate that restricts soybean expansion and tightens the supply of domestically sourced meal for feed production. Enforcement intensified in 2024, with federal agencies blocking credit access for farms found in violation, a policy that reduced the area available for soy cultivation by an estimated 1.2 million hectares. Argentina's northern provinces implemented land-use zoning in 2024, which prohibits the conversion of agricultural land in high-conservation-value forests. This measure limits the geographic footprint for feed-crop production and raises the cost of compliance for millers sourcing from these regions. The regulatory influence extends to traceability requirements, with the European Union's Deforestation Regulation (EUDR) mandating the collection of geolocation data for all soy and beef imports starting in 2025 [2]Source: European Commission, “EU Deforestation Regulation,” europa.eu . Feed millers exporting to the European Union-bound livestock operations must now invest in supply-chain mapping and third-party audits, which add an estimated USD 5 to USD 8 per metric ton to the cost of certified feed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Poultry Dominance Meets Aquaculture Surge

Poultry feed captured 42.55% of South America's 2025 compound feed market, a dominance rooted in Brazil's broiler export machine and Argentina's resurgence in egg production. Broiler integrators demand feed-conversion ratios below 1.60, a target that requires precision balancing of metabolizable energy and digestible amino acids, pushing millers to adopt near-infrared spectroscopy for real-time ingredient analysis. The poultry segment's maturity means growth will come from incremental efficiency gains rather than volume expansion, a dynamic that favors ingredient suppliers offering novel enzymes or gut-health additives over commodity grain traders. Swine feed benefits from Argentina's renewed pork exports to China, with formulations shifting toward synthetic lysine and low-crude-protein diets that reduce nitrogen excretion and comply with emerging environmental standards.

Aquaculture feed is expected to expand at a 7.42% CAGR through 2031, driven by the fastest growth among animal types, as tilapia cage farming scales up in Brazil's reservoirs and shrimp production intensifies in Ecuador's coastal provinces. The aquaculture segment's outperformance reflects a structural arbitrage: fish convert feed into body mass more efficiently than terrestrial livestock, with tilapia achieving feed-conversion ratios of nearly 1.20 compared to 1.60 for broilers and 2.80 for cattle. This efficiency advantage positions aquaculture as a lower-cost protein source, particularly in regions where water resources are abundant and support intensive production. Regulatory frameworks are catching up, with Brazil's Ministry of Fisheries issuing new guidelines in 2024 for aquafeed labeling that mandate disclosure of fishmeal and fish-oil content, a transparency measure aimed at addressing sustainability concerns .

By Ingredient: Cereals Lead, Functional Supplements Accelerate

Cereals accounted for 39.10% of ingredient revenue in 2025, with corn and wheat serving as the primary energy sources in most rations across poultry, swine, and ruminant applications. Brazil's second corn crop, harvested in the first quarter, supplies the bulk of domestic feed demand, yet logistics bottlenecks during peak harvest compress prices in producing regions while elevating costs in deficit areas. Cakes and meals, primarily composed of soybean meal, serve as the primary protein source. Crushing plants in Mato Grosso and Argentina's Pampas region operate at near-full capacity to meet both export and domestic demand. By-products, including wheat bran and rice hulls, provide cost-effective fiber and energy, particularly in ruminant rations where digestive physiology can tolerate lower-quality ingredients.

Supplements are projected to grow at an 7.68% CAGR through 2031, driven by prebiotics and probiotics that are replacing antibiotic growth promoters as residue limits tighten across export markets. Within the supplements category, vitamins remain a stable revenue contributor, with synthetic A, D, and E blends sourced primarily from European and Chinese manufacturers. Amino acids, particularly lysine, methionine, and threonine, are seeing adoption rates above 90% in poultry and swine feed as nutritionists optimize least-cost formulations that reduce crude-protein levels without sacrificing growth performance. Enzymes, including phytase and xylanase, unlock nutrients from plant-based ingredients and reduce the environmental footprint of livestock operations by lowering phosphorus and nitrogen excretion.

Geography Analysis

Brazil held 61.65% of South America compound feed market in 2025, a share underpinned by the world's largest broiler export program, a cattle herd exceeding 230 million head, and a swine sector that targets Asian buyers. The country's feed industry benefits from domestic corn and soybean production, which supplies over 90% of ingredient needs, insulating millers from import price volatility and currency risk. Brazil's southern states, including Paraná, Santa Catarina, and Rio Grande do Sul, are home to significant poultry and swine operations, with feed mills strategically located near crushing plants and port terminals to minimize logistics costs.

Argentina will expand at a 5.98% CAGR through 2031, driven by the fastest geographic growth, fueled by grass-fed beef exports, a resurgent pork sector, and a poultry industry that serves both domestic and regional buyers. The country's feed market is shaped by peso volatility, which forces millers to hedge ingredient costs through forward contracts with United States grain exporters and complicates pricing for livestock producers operating on thin margins. Argentina's Pampas region, encompassing the provinces of Buenos Aires, Córdoba, and Santa Fe, is home to the majority of the country's feed-milling capacity. The proximity to soybean-crushing plants and cattle feedlots reduces inbound freight costs. The government extended tax exemptions on feed-ingredient imports through 2025, a measure designed to offset inflationary pressures and support farm-level profitability.

Rest of South America, including Colombia, Peru, Chile, and Ecuador, held significant share, the fastest geographic growth. Chile's salmon aquaculture industry consumed over 900,000 metric tons of feed in 2024, with formulations increasingly incorporating algae-based omega-3 oils to replace fishmeal and address sustainability concerns from European retailers. Colombia's dairy sector is intensifying, with farmers adopting total mixed rations and precision feeding systems that improve milk yields and reduce methane emissions per liter produced. Peru's poultry industry is modernizing, with integrators investing in automated feed-delivery systems and biosecurity protocols that support higher stocking densities and faster turnover.

Competitive Landscape

The South America compound feed market is highly consolidated with major players like Cargill Inc., Kemin Industries, Marfrig Global Foods (BRF), JBS S.A., and Aurora Alimentos. These leading companies are focused on acquiring feed mills and small manufacturing for expansion of the business in local as well as foreign markets. Also, the leading companies focused on the expansion of the business across regions and setting up a new plant for increasing production capacity as well as a product line. The companies are also increasing the production capacities of their existing plants.

South America Compound Feed Industry Leaders

Cargill, Incorporated

ADM

JBS S.A.

BRF S.A

Alltech, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cargill announced an investment to expand its feed-milling complex in Campinas, Brazil, adding to annual capacity and installing near-infrared spectroscopy systems for real-time ingredient analysis. The facility will serve poultry and swine integrators in São Paulo and Minas Gerais states, reducing logistics costs and enabling faster formulation adjustments based on animal performance data.

- January 2024: JBS invested in constructing three new feed factories in Seberi, Santo Inácio, and Itaiópolis in Southern Brazil. The investment aligns input supply with the production capacity of its Seara business unit, which expanded significantly in recent years through the company's investment plan. These new units increase Seara's annual feed production by more than 1 million metric tons.

- January 2023: Evonik introduced an enhanced version of its Biolys animal feed product in Castro, Paraná, Brazil. The new Biolys formulation contains 62.4% L-lysine (an 80% ratio to Lysine HCl), an improvement over its previous version, which contained 60% L-lysine (a 77% ratio to Lysine HCl). The product incorporates beneficial components from its fermentation process, delivering additional nutrients and energy benefits for livestock, particularly swine and poultry.

South America Compound Feed Market Report Scope

Compound feed is a combination of different concentrate feed ingredients in suitable ratios. Frequently used ingredients in compound feed include brans, protein meals/cakes, grains, agro-industrial by-products, minerals, and vitamins. The South American Animal Feed Market is Segmented by Animal Type (Ruminants, Poultry, Swine, Aquaculture, and Others) Ingredients (Cereal, Cakes & Meals, By-Products, and Supplements) Supplements (Vitamins, Amino Acids, Enzymes, Acidifiers, Probiotics, Prebiotics, and Other Supplements) and Geography (Brazil, Argentina, and Rest of South America). The report offers market size and forecasts in terms of Value (USD) and Volume (Metric Tons).

By Animal Type

| Ruminants |

| Poultry |

| Swine |

| Aquaculture |

| Other Animal Types |

By Ingredient

| Cereals | |

| Cakes and Meals | |

| By-products | |

| Supplements | Vitamins |

| Amino Acids | |

| Enzymes | |

| Prebiotics and Probiotics | |

| Acidifiers | |

| Other Supplements | |

| By Geography | Brazil |

| Argentina | |

| Rest of South America |

| By Animal Type | Ruminants | |

| Poultry | ||

| Swine | ||

| Aquaculture | ||

| Other Animal Types | ||

| By Ingredient | Cereals | |

| Cakes and Meals | ||

| By-products | ||

| Supplements | Vitamins | |

| Amino Acids | ||

| Enzymes | ||

| Prebiotics and Probiotics | ||

| Acidifiers | ||

| Other Supplements | ||

| By Geography | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the South America compound feed market by 2031?

The market is projected to reach USD 91.87 billion by 2031.

Which animal type is growing fastest in South America feed demand?

Aquaculture feed is forecast to register the highest CAGR of 7.42% between 2026 and 2031.

How large is Brazil's share in regional compound feed revenues?

Brazil accounted for 61.65% of South America's feed revenue in 2025.

What is driving pellet dominance in South American feed forms?

Pellets reduce waste, improve feed conversion, and withstand long-distance transport better than mash, giving them a 51.35% share in 2025.

Page last updated on: