Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

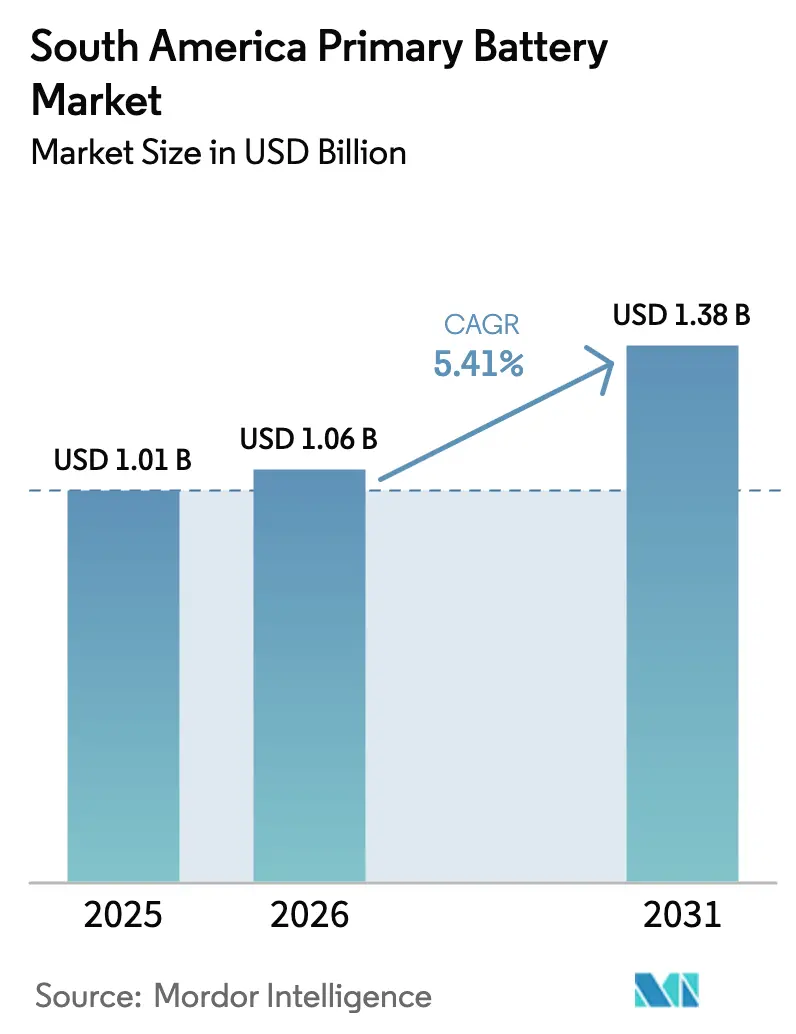

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Primary Battery Market Analysis by Mordor Intelligence

The South America Primary Battery Market size was valued at USD 1.01 billion in 2025 and is estimated to grow from USD 1.06 billion in 2026 to reach USD 1.38 billion by 2031, at a CAGR of 5.41% during the forecast period (2026-2031).

Robust consumer-electronics replacement demand, expanding IoT deployments in agribusiness, and disaster-preparedness stockpiling keep single-use chemistries relevant even as rechargeables gain ground. Alkaline formats anchor volume in remote controls and toys, while primary lithium variants capture premium niches that require long shelf life and wide operating temperatures. Special-shape prismatic cells are gaining momentum in industrial sensors and wearables that cannot accept standard cylindrical geometries. Regulatory tightening on heavy-metal content is accelerating a pivot toward mercury-free alkaline, lithium, zinc-air, and silver-oxide options.

Key Report Takeaways

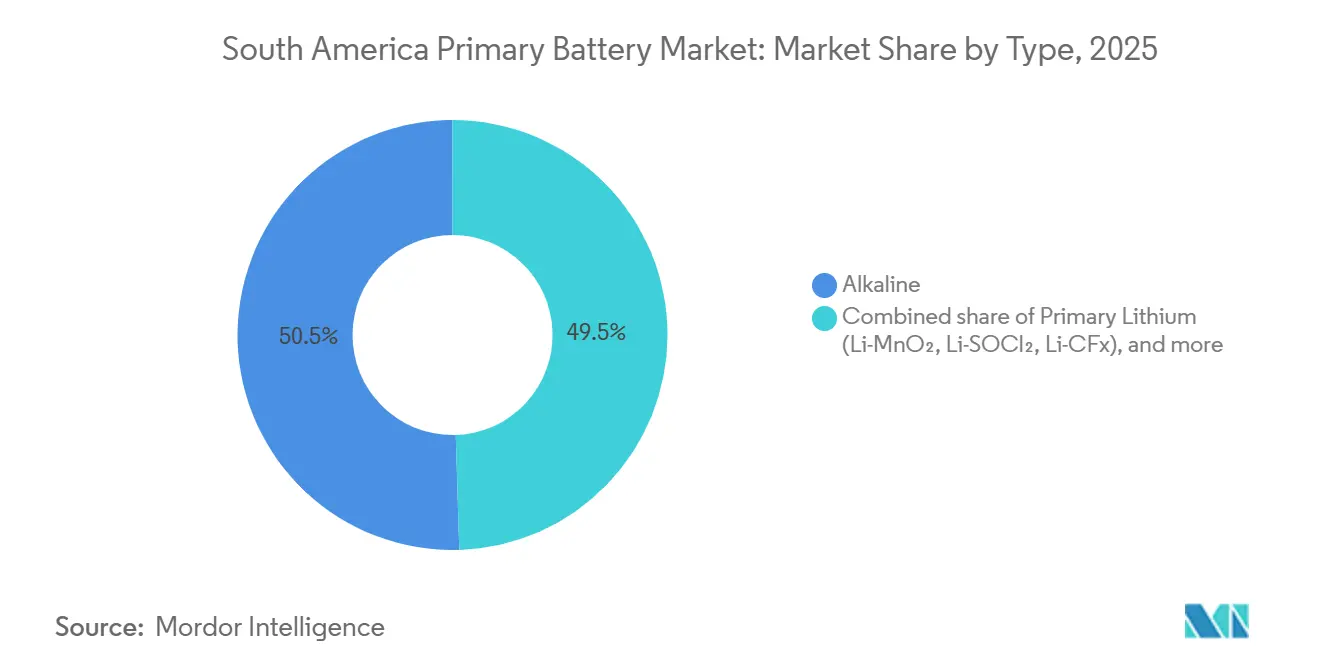

- By type, alkaline cells led with 50.5% revenue share in 2025; primary lithium chemistries are forecast to expand at an 8.7% CAGR through 2031.

- By form factor, cylindrical batteries held 59.8% of volume in 2025, whereas special-shape prismatic and custom cells are advancing at a 9.6% CAGR.

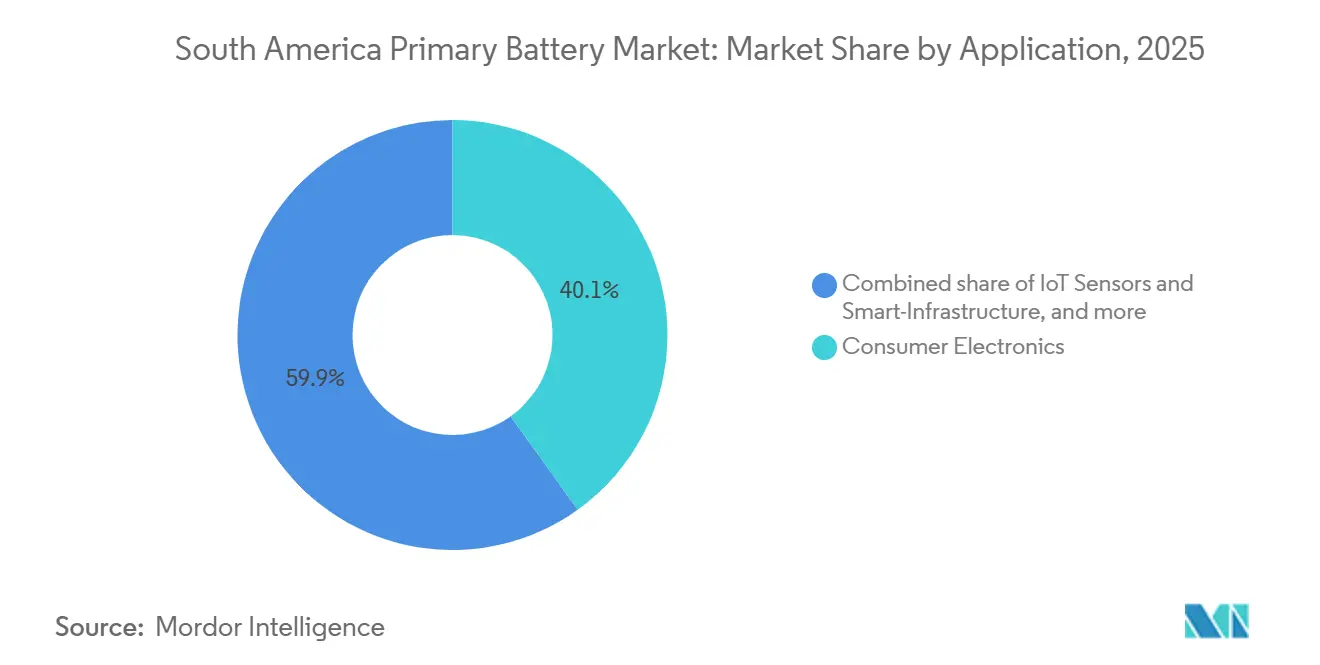

- By application, consumer electronics commanded a 40.1% share of the South America primary battery market size in 2025, while IoT sensors and smart infrastructure are growing at a 10.2% CAGR to 2031.

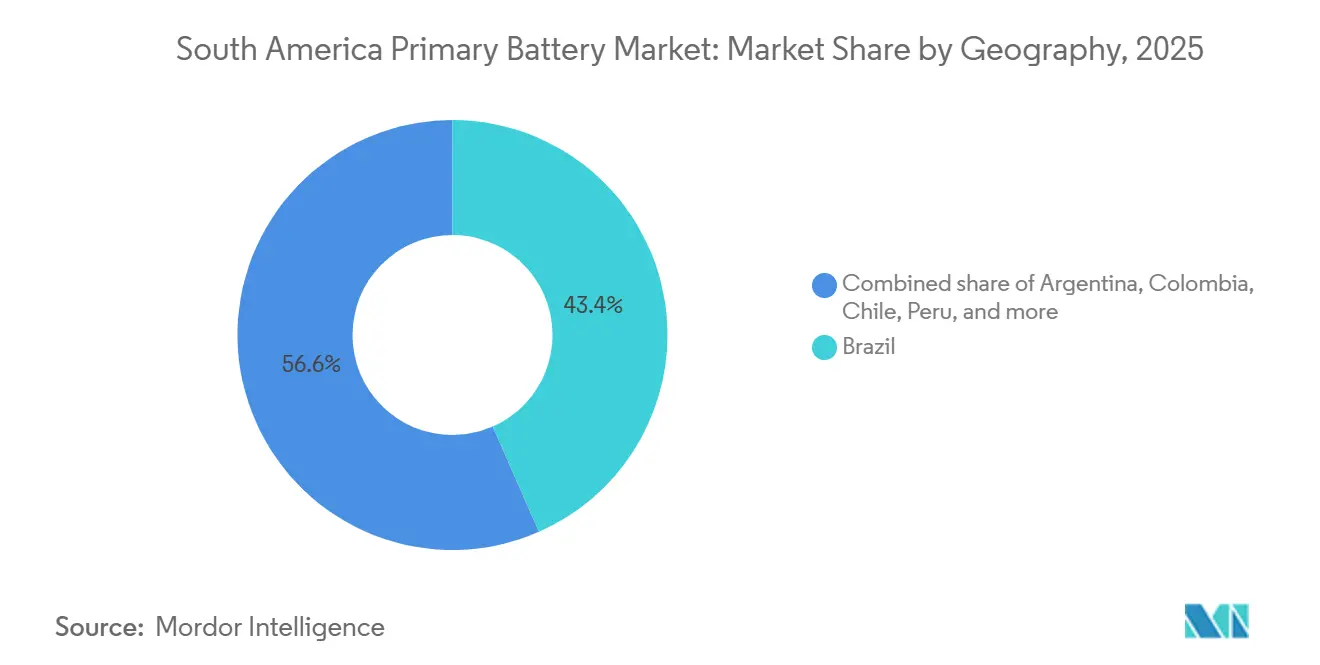

- By geography, Brazil accounted for 43.4% of regional revenue in 2025; Chile is the fastest-growing geography at a 9.9% CAGR through 2031.

- Duracell, Energizer, and Panasonic collectively controlled an estimated 55%–60% South America primary battery market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Primary Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding consumer-electronics penetration | +1.2% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Government incentives for rural off-grid electrification | +0.8% | Brazil, Peru, Colombia | Long term (≥ 4 years) |

| Proliferation of battery-powered IoT sensors in Brazilian agribusiness | +1.5% | Brazil (Cerrado) | Short term (≤ 2 years) |

| Growing demand for primary cells in critical medical devices | +0.9% | Regional metro hospitals | Medium term (2-4 years) |

| Disaster-preparedness kits amid extreme-weather events | +0.7% | Chile, Peru, Colombia | Short term (≤ 2 years) |

| Tactical communications upgrades in Andean defense procurements | +0.5% | Peru, Colombia, Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Consumer-Electronics Penetration

Smartphone adoption passed 70% of adults in 2025, and accessories ranging from wireless gaming controllers to LED flashlights still depend on alkaline AA and AAA cells.[1]GSMA Intelligence, “Mobile Economy Latin America 2025,” gsma.com Retail partnerships with Lojas Americanas and Carrefour Brasil lifted Energizer’s Latin America alkaline shipments by 9% in fiscal 2025. Price-sensitive buyers in Colombia and Peru continue to favor disposable batteries over upfront rechargeable costs. Seasonal toy demand during Christmas and Carnival further sustains replacement cycles. Although USB-rechargeable peripherals are gaining shelf space, entrenched device ecosystems delay rapid substitution.

Government Incentives for Rural Off-Grid Electrification

Brazil allocated BRL 450 million (USD 90 million) in 2024 to distribute solar-battery kits across indigenous territories, pairing photovoltaic modules with primary lithium cells that buffer cloudy intervals. Chile’s SEC mandated sub-zero-rated backup cells for off-grid sites in Aysén and Magallanes in 2025, favoring Li-SOCl₂ chemistry. Peru supplied 12,000 LED lamps and radio kits to Loreto households the same year, creating a recurring D-cell replacement stream. These initiatives produce lumpy tenders but cement last-mile distribution networks that later benefit retail sales.

Proliferation of Battery-Powered IoT Sensors in Brazilian Agribusiness

Eighteen percent of large soy farms in Mato Grosso had deployed soil-moisture and weather sensors by 2024, according to Embrapa.[2]L. Oliveira, “Battery-Powered Agritech in the Cerrado,” Embrapa Technical Report 2024, embrapa.br Li-MnO₂ coin cells in LoRaWAN transmitters offer 5-10 year lifespans, eliminating field-service visits. GPS cattle collars using Li-SOCl₂ packs withstand humid pastures for eight-year duty cycles, reducing labor on herds exceeding 10,000 head. JBS piloted blockchain traceability tags powered by primary lithium in 2025 across 245 Brazilian facilities. Export-market traceability mandates and remote-location realities underpin the segment’s double-digit growth.

Growing Demand for Primary Cells in Critical Medical Devices

Implantable cardiac monitors, pacemakers, and neurostimulators require primary lithium chemistries to meet stringent FDA and ANVISA voltage and safety profiles.[3]FDA, “Battery Safety in Implantable Devices,” fda.gov Brazil’s public health system added 22,000 covered implant procedures in 2024, boosting medical-grade cell demand. Portable diagnostics, handheld ultrasound scanners, and glucometers favor alkaline or silver-oxide button cells for stockroom stability.[4]World Health Organization, “Global Medical Devices Market 2025,” who.int An aging population is lifting hearing-aid adoption, with zinc-air cells dominating for capacity and cost. Rayovac Brasil posted double-digit zinc-air revenue gains in 2025 through audiology-clinic partnerships.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid substitution by rechargeable chemistries | -1.3% | Brazil, Argentina, Chile | Short term (≤ 2 years) |

| Stricter disposal rules on cadmium / mercury content | -0.6% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Port-logistics and import-tariff volatility | -0.4% | Brazil (Santos, Paranaguá) | Short term (≤ 2 years) |

| Pilot battery-sharing kiosks in Argentina | -0.2% | Buenos Aires, Córdoba | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Substitution by Rechargeable Chemistries

USB-rechargeable LED flashlights, gaming controllers, and wireless speakers are replacing disposable-battery models in major Brazilian and Chilean retailers. Energizer’s fiscal-2025 Latin America alkaline volume slipped 4%, partly offset by higher prices and lithium-primary growth. Urban households with stable grids can charge overnight, accelerating the shift, while rural areas remain alkaline-centric. Consumer education remains limited, delaying total-cost-of-ownership awareness in lower-income segments.

Stricter Disposal Rules on Cadmium / Mercury Content

Brazil’s CONAMA Resolution 401 tightened cadmium limits in button cells to 0.002% by weight in 2024 and mandated retailers to take back schemes. Chile introduced producer-responsibility legislation in 2025, targeting a 45% recovery rate by 2028. Manufacturers incur 2%-4% higher production costs to shift toward mercury-free designs, and importers must finance reverse logistics. Duracell partnered with Recicladora Ambiental to pilot 500 supermarket collection bins in 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Lithium Chemistries Outpace Alkaline in Specialized Niches

Alkaline batteries maintained 50.5% of 2025 revenue thanks to ubiquitous AA and AAA devices in retail channels. In contrast, primary lithium chemistries are projected to grow 8.7% annually through 2031, powering medical implants, industrial IoT nodes, and defense radios that need decade-long service lives. Zinc-air cells dominate the hearing-aid segment as the population aged 65+ expands 3.2% per year. Regulatory pressure on mercury content accelerates the phase-out of zinc-carbon variants.

Silver-oxide cells, priced three to five times higher than alkaline, serve precision watches and gas detectors in Chile’s mines. Specialty chemistries like lithium-iron-disulfide target extreme temperatures in Patagonian and Andean defense applications with a commercial launch slated for 2026. As a result, the South America primary battery market size for lithium chemistries is set to widen its footprint, even as alkaline remains the volume leader.

By Form Factor: Special Shapes Surge for Industrial IoT

Cylindrical cells accounted for 59.8% of shipments in 2025, anchored by legacy device compatibility in consumer electronics. D-cell demand persists in flashlights and emergency lanterns distributed via rural-electrification programs.

Special-shape prismatic and custom cells are rising at a 9.6% CAGR because industrial and medical OEMs require slim designs for sensors and wearables. Flat prismatic lithium cells sealed into soil probes withstand harsh Cerrado field conditions without housings that fit cylindrical forms. Coin and button cells fuel implantables and watches, benefiting from silver-oxide and zinc-air chemistries. Premium pricing offsets lower volumes, improving supplier margins relative to commoditized cylindrical SKUs.

By Application: IoT Sensors Eclipse Consumer-Electronics Growth

Consumer electronics still held 40.1% of the South America primary battery market in 2025, but the segment inches forward as rechargeables cannibalize alkaline replacements. IoT sensors used in precision agriculture, mining telemetry, and smart-city infrastructure are advancing at a 10.2% CAGR, propelling the South America primary battery market size for this niche ahead of legacy consumer gadgets.

Industrial OEMs choose Li-SOCl₂ cells for 10-year maintenance-free operation in remote meters and factory sensors. Medical applications, although smaller in volume, command premium pricing for implant-grade lithium and zinc-air button cells that satisfy safety and longevity mandates. Defense and aerospace remain high-margin corners, with Saft and Ultralife shipping Li-SOCl₂ packs for Andean tactical radios and maritime beacons.

Geography Analysis

Brazil contributed 43.4% of regional revenue in 2025, combining great consumer-electronics demand with expanding agribusiness IoT deployments that depend on lithium primary cells. Port congestion in Santos and Paranaguá lifts landed costs 12%-18% above North American benchmarks, squeezing distributor margins and tilting industrial tenders toward price-aggressive Chinese brands. CONAMA’s stricter disposal rules are nudging retailers toward mercury-free products and imposing take-back compliance overhead.

Chile is the fastest-growing market at 9.9% CAGR through 2031, fueled by copper-mining telemetry, renewable-energy monitoring, and disaster-preparedness stockpiling. The SEC’s 2025 specification for sub-zero-rated backup cells in Magallanes and Aysén solidified demand for Li-SOCl₂ formats. Extended producer-responsibility mandates compel importers to finance collection kiosks, adding logistical complexity but giving early movers a reputational edge.

Argentina’s market is volatile due to currency depreciation and tariff swings, yet pilot battery-sharing kiosks in Buenos Aires and Córdoba hint at future disruption if scaled nationally. Colombia and Peru are emerging segments, driven by disaster-relief stockpiles and rural electrification programs that distribute battery-powered radios and lanterns. Smaller economies such as Uruguay, Bolivia, and Paraguay exhibit heterogeneous demand profiles tied to electrification rates and mining or agricultural activity, keeping supply chains fragmented.

Regulatory Landscape

South America primary-battery suppliers are facing tighter heavy-metal rules and more formalized take-back obligations, which is pushing a shift toward mercury-free alkaline and primary lithium formats. This also increases compliance and reverse-logistics costs for importers and retailers, particularly in supermarket and pharmacy channels where collection-network requirements come with additional documentation.

In Brazil, CONAMA Resolution 401 tightened cadmium limits in button cells to 0.002% by weight in 2024 and reinforced retailer take-back requirements. Argentina updated its market access framework in June 2026 via Joint Resolution 1/2026 (published in the Boletin Oficial), setting a new technical regime for commercialization of primary batteries and moving away from pre-authorization toward sworn declarations of conformity supported by post-market audits via the Trámites a Distancia (TAD) platform. In Chile, extended producer-responsibility legislation introduced in 2025 targets a 45% recovery rate by 2028, shifting more end-of-life cost responsibility onto producers and importers and favoring players that can scale collection and sorting.

Competitive Landscape

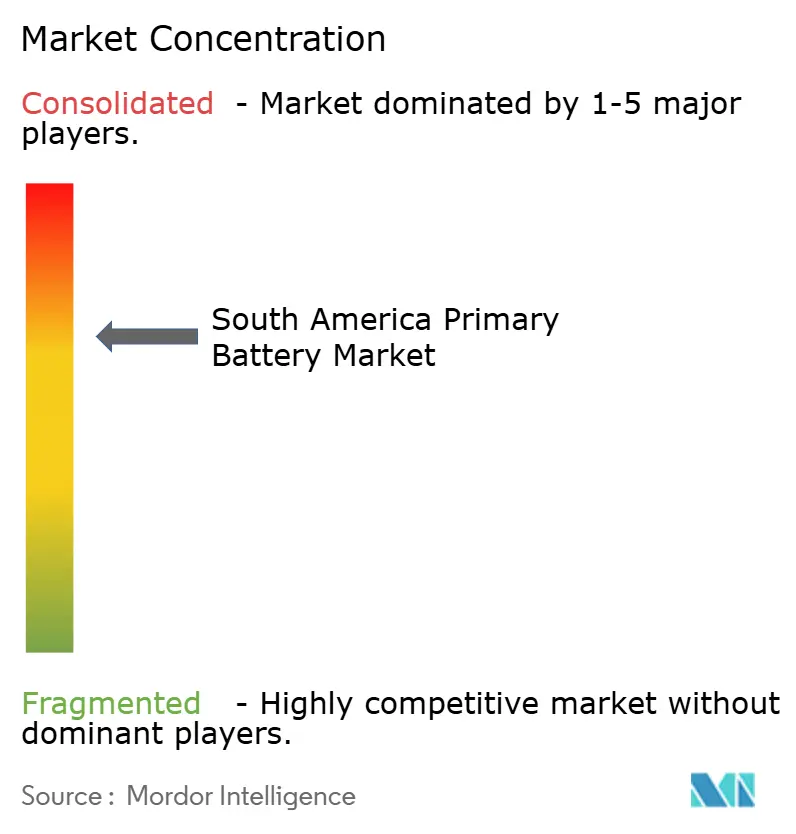

The South America primary battery market is moderately concentrated. Duracell, Energizer, and Panasonic control roughly 55%-60% of retail alkaline volume via supermarket and pharmacy channels. Chinese manufacturers Ningbo Hi-Watt, Shenzhen MUSTANG, and Zhongyin undercut incumbents by 15%-25% in industrial tenders, leveraging low manufacturing costs and flexible payment terms.

Saft and Ultralife command high-margin defense and aerospace niches with Li-SOCl₂ packs certified for harsh-environment radios and beacons; Saft’s 2025 Latin America defense sales rose 12% on Chilean and Colombian contracts. Rayovac Brasil benefits from Zona Franca tax incentives in Manaus, enabling localized assembly that tempers tariff exposure.

Technology differentiation in alkaline remains slight, so shelf placement and promotions dominate retail competition. In contrast, proprietary cathode recipes and long-life guarantees generate pricing power in lithium segments. Patent filings, such as Ultralife’s 2024 Li-CFx formulation that extends implantable runtime 18%, signal ongoing innovation, especially for medical markets. Agritech startups bundling sensors with multiyear battery-replacement contracts represent a nascent competitive layer as service models gain traction among large soy and cattle producers.

South America Primary Battery Industry Leaders

Energizer Holdings Inc.

Duracell Inc.

Panasonic Corp.

GP Batteries International Ltd.

Camelion Battery Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Industrial and OEM demand is creating whitespace for long-life primary lithium solutions in remote monitoring, where total cost is shaped more by site visits than by cell price. That pull is visible in Brazilian agribusiness digitization, with Embrapa reporting that 18% of large soy farms in Mato Grosso deployed soil and weather sensors by 2024, and in traceability pilots such as JBS deploying primary-lithium-powered tags across 245 facilities in 2025. For suppliers, Li-SOCl2 and Li-MnO2 cells with multiyear guarantees, plus custom prismatic formats for embedded sensors, offer a clearer route to premium contracts than commoditized AA/AAA categories.

Regulatory tightening on collection and heavy-metal limits also supports a second opportunity around compliant product portfolios and reverse-logistics execution as a service for retailers and importers. Brazil's CONAMA Resolution 401 retailer take-back obligations and Chile's producer-responsibility framework, with a 45% recovery target by 2028, create demand for collection infrastructure, audit-ready documentation, and changes to packaging and labeling. Differentiation is also showing up in brand moves, including Energizer's recyclable, plastic-free packaging rollout (announced January 2026, with broader international deployment including South America later in 2026), which shifts attention to retail shelf readiness and sustainability claims alongside chemistry.

Recent Industry Developments

- May 2026: Energizer announced recyclable, plastic-free paper-based packaging for its batteries, with an initial Walmart rollout followed by a broader international expansion that includes South America. The change supports retailer sustainability requirements and can improve shelf execution, while also pressuring competitors to refresh packaging and compliance documentation across the region.

- January 2026: Duracell launched its Optimum AA and AAA alkaline battery line in Brazil. The introduction targets performance-focused consumer segments and supports premium pricing strategies in a market facing private-label pressure and rechargeable substitution.

- August 2024: Duracell introduced a child-safety focused lithium coin battery range (CR2032, CR2025, CR2016) featuring a bitter coating and child-resistant packaging. This product update aligns with tightening safety expectations for button and coin cells and supports differentiation in higher-margin specialty formats.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues generated from non-rechargeable (primary) batteries sold and used across South America for everyday and professional power needs. Revenue is counted at the point of sale into the region and tracked in USD for consistency.

Scope exclusions: We exclude rechargeable batteries, battery packs built mainly for secondary chemistries, and revenues from chargers or power-management electronics.

Segmentation Overview

- By Type

- Alkaline

- Primary Lithium (Li-MnO₂, Li-SOCl₂, Li-CFx)

- Zinc-Air

- Zinc-Carbon/Chloride

- Silver-Oxide and Others

- By Form Factor

- Cylindrical (AA, AAA, C, D)

- Coin and Button Cells

- Prismatic/Packaged

- Others (Special shapes)

- By Application

- Consumer Electronics

- Industrial and OEM

- Medical and Healthcare

- Defence and Aerospace

- IoT Sensors and Smart-Infrastructure

- By Geography

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by anchoring the demand pool for disposable batteries in South America, then mapping where volumes likely flow by country and use case. We relied on public and official references such as UN Comtrade trade statistics, World Bank macro indicators, national statistics offices in key countries, customs and tariff schedules, and technical publications and standards that clarify battery formats and chemistries.

To make the model usable in real conditions, we reviewed company filings, investor presentations, and reputable press coverage to track product mix changes (for example, alkaline versus primary lithium) and retail channel movement. Where available, we also used paid subscriptions for company financials and intelligence, patent lookups, and shipment-level import and export reads to cross-check trade direction and pricing signals. The sources listed here are illustrative rather than exhaustive, and we also used other public documents and datasets to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with manufacturers, distributors, retailers, and large institutional buyers that regularly procure disposable cells for devices and field equipment. We covered the main South American demand centers, then checked assumptions around format mix (cylindrical versus coin and button), application pull (consumer electronics, industrial and OEM, medical, defense, and IoT), and the typical price bands seen in-country, so gaps from desk inputs could be closed with realistic ranges.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 17% | APAC: 47% |

| Mid tier: 43% | Functional/Unit leaders: 28% | EMEA: 35% |

| Smaller Players: 21% | Managers: 55% | Americas: 18% |

Market-Sizing & Forecasting

Sizing begins with a top-down build that reconstructs regional consumption using observable signals, including import and export flows for relevant battery categories, country-level device ownership and replacement behavior, and macro indicators tied to retail activity. Those totals are then corroborated with selective bottom-up checks, such as sampled price points by format, distributor channel checks, and supplier roll-ups where public revenue disclosures and product mix commentary allow a clearer read.

In the model, we keep the calculations grounded with practical variables, including the share of alkaline versus primary lithium in household purchases, the penetration of coin and button cells in small electronics, replacement frequency assumptions for common devices, and local currency movement that can change USD pricing even when unit demand is stable. Forecasts are mainly produced using scenario analysis. Those scenarios are guided by what interviewees expect for consumer electronics demand, industrial procurement cycles, and the pace of adoption for small IoT sensors in infrastructure and agriculture. When bottom-up signals are incomplete for smaller countries, we fill gaps using validated proxy ratios from similar markets, then re-check the outcome against trade and pricing direction.

Data Validation & Update Cycle

Validation is done through repeated cross-checks, so the final market value does not rely on a single dataset or one expert view. We compare model outputs against independent indicators such as trade trends, visible price movements, and country demand narratives gathered during interviews. Anomalies are flagged for review before sign-off.

A second analyst review is used to re-test key assumptions, including format mix and ASP progression. If a number sits outside the expected range without a clear explanation, re-contact is triggered to reconcile the assumption. Reports are refreshed annually, and interim updates are completed when a material event affects demand, pricing, or import availability. Before delivery, a fresh pass is run so clients receive the latest updated view based on the newest public releases and confirmed market signals.

Mordor Intelligence's South America Primary Battery Market Size Compared With Other Published Estimates

Different published estimates for this market can look far apart because the scope is not always treated the same, and the pricing logic can be handled in different ways. We usually see gaps driven by what battery types are counted, whether the numbers reflect end-market consumption or broader supply value, and how exchange rates and inflation are translated into USD over time.

Some sources expand the scope into rechargeable chemistries or count battery systems that sit outside disposable cells, which lifts the value. For Mordor Intelligence, the market is limited to primary (non-rechargeable) batteries in South America, and the estimate is checked using format-level mix and application demand signals that can be refreshed each year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.01 B (2025) | |

| Trade Journal A | USD 5.30 B (2024) | The figure likely includes broader battery categories beyond primary cells, and the pricing basis is not clearly linked to country-level ASP checks or trade-direction validation. |

| Industry Bulletin B | USD 1.12 B (2026) | The estimate appears to start from a later year and may apply uniform growth and currency assumptions across countries, with limited evidence of format-mix adjustments by application. |

The comparison indicates that most of the spread comes from including adjacent battery categories and from simplifying price and currency treatment across South American countries. Our model keeps the total traceable to clear volume proxies and defensible price bands, and it can be repeated when trade, device demand, or format mix shifts.

Key Questions Answered in the Report

How large is the South America primary battery market in 2026?

The market stood at USD 1.06 billion in 2026, with the trajectory continuing towards USD 1.38 billion by 2031 at a 5.41% CAGR.

Which battery chemistry is growing fastest across South America?

Primary lithium chemistries, led by Li-MnO? and Li-SOCl?, are forecast to expand at 8.7% annually through 2031, driven by medical devices and IoT sensors.

Why is Chile the fastest-growing market in the region?

Copper-mining telemetry, disaster-preparedness stockpiling, and off-grid renewable monitoring push Chile to a 9.9% CAGR, the highest in South America.

What role do IoT sensors play in future battery demand?

IoT applications in agribusiness, mining, and smart cities are advancing at 10.2% CAGR, increasingly influencing product mix toward long-life lithium cells.

How are disposal regulations affecting battery suppliers?

Brazil and Chile have introduced strict take-back and heavy-metal limits, prompting suppliers to shift toward mercury-free chemistries and invest in recycling logistics.

Which companies dominate retail sales of primary batteries?

Duracell, Energizer, and Panasonic collectively control around 55%-60% of retail alkaline volume through supermarket and pharmacy channels.

Page last updated on: