Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

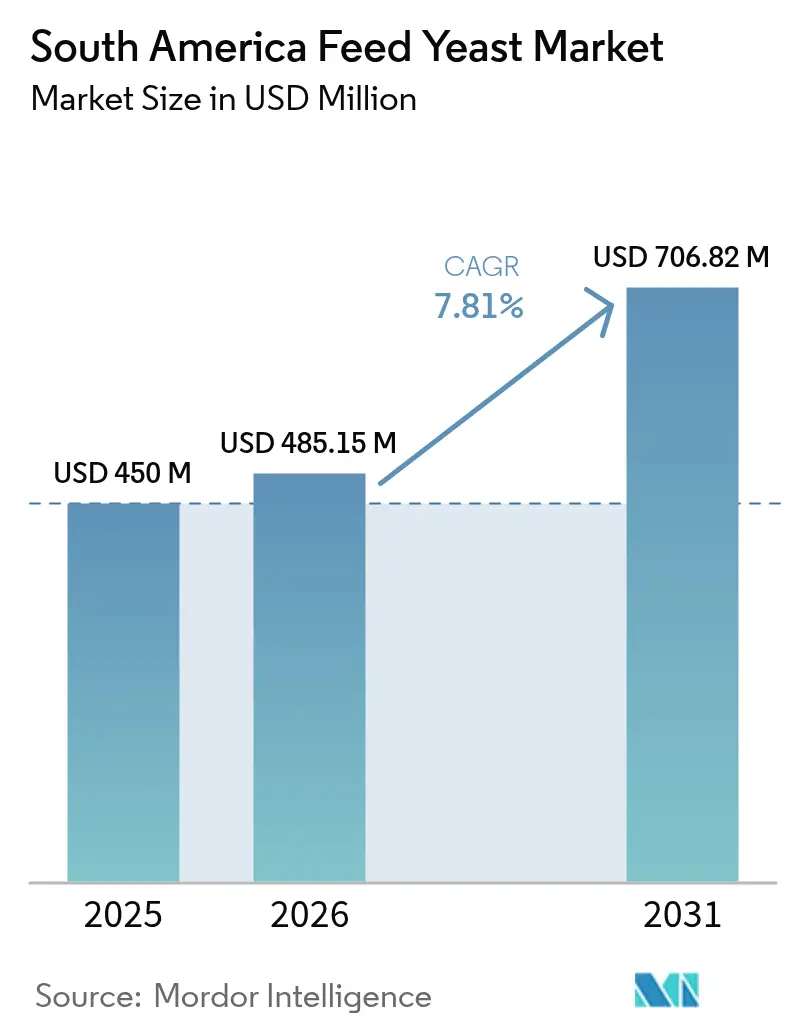

| Base Year Market Size (2025) | USD 450 Million |

| Market Size (2026) | USD 485.15 Million |

| Market Size (2031) | USD 706.82 Million |

| Growth Rate (2026 - 2031) | 7.81% CAGR |

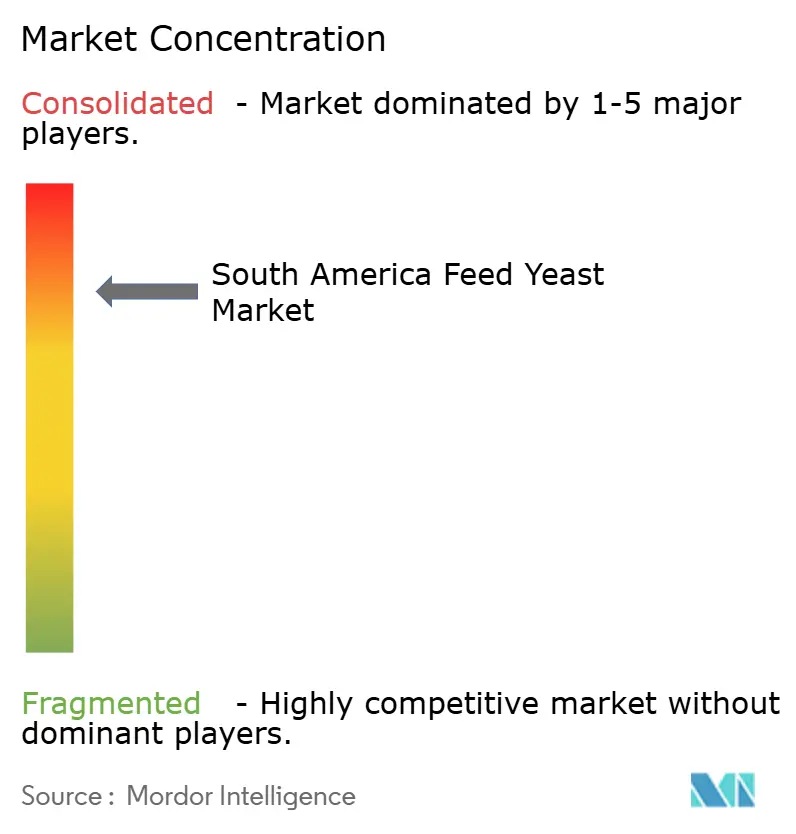

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Feed Yeast Market Analysis by Mordor Intelligence

South American feed yeast market size in 2026 is estimated at USD 485.15 million, growing from 2025 value of USD 450 million with 2031 projections showing USD 706.82 million, growing at 7.81% CAGR over 2026-2031. The rise comes as regulators curb antibiotic growth promoters, prompting livestock producers to switch to natural additives that protect animal health and export eligibility. Brazil leads growth thanks to plentiful sugarcane-ethanol sidestreams that cut production costs, a mature poultry export complex, and extensive fermentation know-how[1]Source: Energy Research Office, “Sugarcane and Ethanol Yearbook 2024,” epe.gov.br. Demand also benefits from the rapid scaling of aquaculture in Peru, regulatory convergence across MERCOSUR, and retailer pressure for traceable, ESG-aligned feed inputs. Nonetheless, the South American feed yeast market faces cost volatility tied to molasses and corn syrup, capital-intensive drying facilities, and freight bottlenecks at Amazonian and Plata ports that can disrupt just-in-time deliveries.

Key Report Takeaways

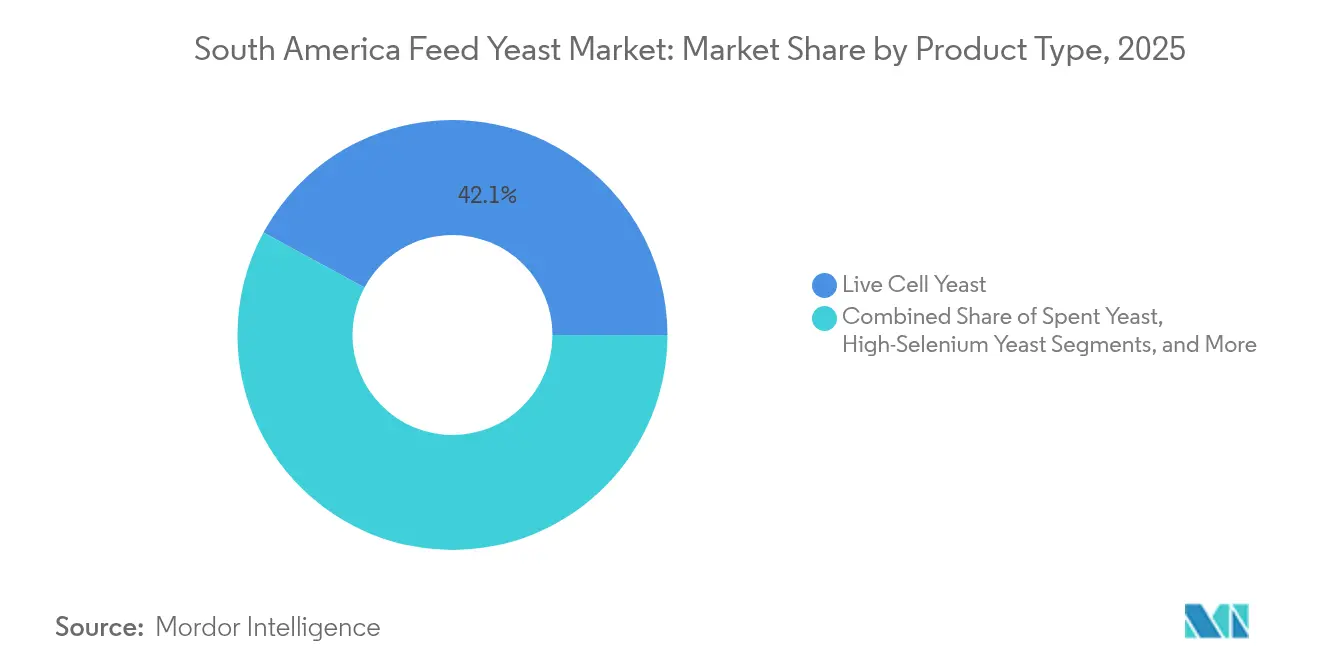

- By product type, live cell yeast held 42.10% of the South America feed yeast market share in 2025, while yeast derivatives are forecast to grow at a 10.79% CAGR through 2031.

- By form, instant yeast commanded 45.60% of the South America feed yeast market size in 2025; liquid slurry formats will post the fastest 11.27% CAGR between 2026-2031.

- By animal type, poultry dominated with a 36.60% share in 2025; aquaculture is set to expand at a 9.65% CAGR to 2031.

- By functional objective, Gut health and immunity commanded 46.50% of the South America feed yeast market size in 2025; Heat-stress mitigation will post the fastest 11.07% CAGR between 2026-2031.

- By geography, Brazil accounted for 53.60% revenue share in 2025, and Peru will register the quickest 9.75% CAGR over the forecast period.

- The top five suppliers controlled 66.40% regional share in 2025, with Lallemand Animal Nutrition leading at 18.20%, ADM follows at 15.70%, Cargill commands 12.80% via feed mill co-locations, DSM-Firmenich owns 11.30% after capacity upgrades, and Nutreco rounds out the group at 7.90%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Feed Yeast Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing livestock production volumes | +1.8% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Poultry-export boom from Brazil and Chile | +1.2% | Brazil, Chile | Short term (≤ 2 years) |

| Ban on antibiotic growth promoters (AGPs) | +1.5% | Brazil, Argentina, Chile, Colombia | Medium term (2-4 years) |

| Sustainability push toward natural additives | +0.9% | Brazil, Chile, Colombia | Long term (≥ 4 years) |

| Sugarcane-ethanol sidestreams enabling low-cost single-cell yeast | +1.3% | Brazil, Colombia | Short term (≤ 2 years) |

| Blockchain feed-traceability mandates by meat packers | +0.6% | Brazil, Argentina, Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Livestock Production Volumes

South America’s share of global animal protein output keeps climbing. Between 2000 and 2018 regional poultry tonnage more than doubled, while pork output rose 64.3%. Brazil alone now consumes 2,539 million bushels of corn annually for feed, underscoring the scale at which producers are searching for efficiency boosters. National feed associations forecast further expansion in 2025, with chicken exports from Brazil projected to rise by 1.9%. Those volumes amplify interest in yeast supplements that improve gut integrity and feed conversion. The South American feed yeast market, therefore, gains a structural demand floor as herd and flock sizes climb.

Poultry-Export Boom from Brazil and Chile

Export-driven integrators must satisfy residue-free protocols set by buyers in the United States and the European Union[2]Source: USDA Foreign Agricultural Service, “Brazil Poultry Export Requirements,” usda.gov. Chile’s vertically integrated firms, such as Agrosuper, also chase premium export niches that reward natural feed profiles. As Brazil’s grain output stays on a record-setting path, companies lock in raw material security to capitalize on shifting U.S.–China trade flows. In this premium channel, yeast commands higher margins than synthetic growth promoters, reinforcing the growth outlook for the South American feed yeast market.

Ban on Antibiotic Growth Promoters (AGPs)

Four of the five largest meat-producing countries in South America have outlawed or tightly restricted antibiotic growth promoters deemed critical for human medicine. Brazil is drafting residue-monitoring rules that heighten scrutiny of antibiotic use in animal protein supply chains. As probiotics, phytogenics, and prebiotics dominate 65% of alternative-additive research, yeast is firmly positioned as a proven probiotic option. These regulatory tailwinds underpin sustained adoption in the South American feed yeast market.

Sustainability Push Toward Natural Additives

Supermarkets and food service groups impose sustainability metrics linked to regenerative agriculture, favoring feed ingredients that recycle biomass and lower carbon footprints. South American additive rules, rooted in Codex standards yet adapted for local botanicals, give yeast products regulatory flexibility. Brazilian miller-cum-ethanol producer Tereos highlights carbon-saving fermentation routes that resonate with ESG-oriented buyers. Such narratives strengthen brand value for suppliers in the South American feed yeast industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront fermentation and drying CAPEX | -1.1% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Volatile molasses and corn syrup pricing | -0.8% | Brazil, Argentina, Peru | Short term (≤ 2 years) |

| Competition from bacterial probiotics and enzymes | -0.7% | Brazil, Chile, Colombia | Medium term (2-4 years) |

| Logistics chokepoints at Amazonian and Plata ports | -0.5% | Brazil, Argentina, Peru | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Fermentation and Drying CAPEX

Greenfield yeast plants that meet GMP standards cost tens of millions of USD. DSM-Firmenich’s facility in Sete Lagoas illustrates the capital hurdle newcomers must clear. Port upgrade needs to add further spending as 58 Brazilian terminals require dredging for post-Panamax traffic. These factors deter entrants and preserve incumbent power within the South American feed yeast market.

Volatile Molasses and Corn Syrup Pricing

Corn traded near BRL 60.75 (USD 11.06) per sack in 2024 amid climatic setbacks and farmer stockholding. Ethanol plants now consume 722 million bushels of Brazilian corn, siphoning supply from additive producers farmdocdaily.illinois.edu. Molasses prices likewise swing with global sugar cycles, compressing margins for yeast makers locked into long-term contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Live Cell Dominance Faces Derivative Challenge

Live cell yeast generated the largest slice of the South American feed yeast market size in 2025, accounting for 42.10% of sales. Producers favor its proven benefits in rumen fermentation and pathogen exclusion. Yeast derivatives, though still a smaller base, are accelerating at a 10.79% CAGR thanks to Beta-glucan-rich fractions that bind aflatoxin B1 and improve villus height in broilers. In 2025, spent brewer’s yeast supplied a 28.30% share, leveraged by low input costs, while dry inactive formats provided a 15.70% share, mainly to aquafeed.

Looking ahead, high-selenium yeast is gaining traction, growing 9.38% annually as integrators bundle micronutrient delivery with probiotic action. Modified Beta-D-glucans now capture zearalenone and T-2 toxin efficiently. Suppliers responding with multi-functional derivatives can capture premium niches and reinforce conversion to value-added SKUs in the South American feed yeast market.

By Form: Instant Products Lead Amid Liquid Innovation

Instant yeast maintained 45.60% of 2025 revenue due to ease of batching and long shelf life. The segment anchors baseline demand for feed premixes across Brazil and Argentina. Liquid slurry is the star performer, forecast to expand 11.27% annually through 2031 as automated mills seek micro-dosing accuracy without dust loss. Active wet yeast still holds a 24.80% share for high-viability uses, though chilled logistics limit its reach to nearby farms.

Liquid’s momentum stems from stabilizers that extend viability beyond 90 days, and findings that liquid Saccharomyces boulardii reduces heat-stress markers in finishing pigs. Suppliers that master aseptic packaging and cold chain distribution can tap the fast-growing channel inside the South American feed yeast market.

By Animal Type: Poultry Leadership Amid Aquaculture Surge

Poultry used 36.60% of regional shares in 2025 as exporters implement antibiotic-free regimens demanded by Europe and the United States. Yeast improves feed conversion, immunity, and carcass yield, cementing its role in broiler integrator protocols. Aquaculture, led by Peru’s booming fishmeal sector, will post a 9.65% CAGR to 2031 as cage farming expands beyond anchovy stocks.

Ruminants capture a 26.70% share through rumen pH stabilization, methane moderation, and milk-yield uplift. Swine contributes 18.10%, wherein trials show a 25.52% gain in ADG under heat stress after yeast culture inclusion. Pet food is the emerging frontier, climbing 7.78% annually as urban owners seek functional treats with beta-glucans.

By Functional Objective: Gut Health Drives Multi-Benefit Demand

Gut health solutions dominate at 46.50% shares in 2025 due to the orders as the antibiotic ban tightens. Formulators bundle mannooligosaccharides and beta-glucans to block pathogens while sparing beneficial flora. Growth-performance boosters remain central, especially in Brazil, where a 1-point FCR gain lifts exporter margins. Mycotoxin binding has surged, given recurring aflatoxin events; yeast beta-glucans showed strong sequestration of Fusarium toxins in recent broiler studies.

Heat-stress mitigation is gaining urgency as average barn temperatures climb at 11.07% CAGR. Yeast fermentate reduced vaginal temperature in feedlot heifers during summer spells. Multi-benefit additives that combine these functions command price premiums, lifting average selling prices in the South American feed yeast market across most channels.

Geography Analysis

Brazil anchored 53.60% of the South American feed yeast market revenue in 2025 due to unmatched supplies of molasses, vinasse, and corn ethanol sidestreams that lower the cost of goods. Record sugarcane crushing of 713 million metric tons and 35.3 billion L of ethanol output created abundant fermentation feedstock. Domestic feed compounders produced 2% more tonnage in 2024, and chicken exports are forecast to climb 1.9% in 2025. Brazil’s blockchain pilots, such as BovChain, further raise traceability norms, reinforcing demand for certified yeast inputs.

Argentina captured a 17.20% share and is on track for a 7.52% CAGR. Beef exporters benefit from pastured systems and new nutrition regulations that favor natural additives. Harmonization under MERCOSUR eases cross-border trade, though Plata river port congestion can hinder peak-season deliveries. Competition policy enforcement adds oversight yet supports a level playing field for yeast suppliers.

Peru is set for the region’s fastest 9.75% CAGR on the back of aquaculture stimulus programs and restored tax incentives. The nation already hosts the world’s biggest fishmeal complex, so as it shifts toward high-value farmed fish, soluble yeast proteins and liquid slurry formats gain traction. Government institutes also promote pasture upgrades that complement ruminant yeast usage.

Competitive Landscape

Oligopolistic characteristics define the South American feed yeast market: the top five companies hold a 67% share. Lallemand Animal Nutrition leads with 18.5%, leveraging proprietary strains and regional production lines. ADM follows at 16.0%, integrating yeast with its vast grain network. Cargill commands 13.0% via feed mill co-locations, while DSM-Firmenich owns 11.5% after capacity upgrades. Nutreco rounds out the group at 8.0%, bundling yeast into Trouw premixes.

Strategically, incumbents pursue vertical integration: Lesaffre’s 70% stake in Biorigin secured low-cost Brazilian capacity and direct access to cane-based substrates. DSM-Firmenich simultaneously divested non-core yeast extracts to sharpen the focus on high-growth animal nutrition. Emerging players differentiate through thermotolerant strains or waste-stream substrates, though high capex and regulatory registrations remain barriers. The competitive narrative is shifting from price to proven functional performance, with companies sponsoring farm-scale trials to quantify FCR savings and health outcomes.

Technology partnerships also matter: cloud-enabled monitoring tools integrate yeast inclusion data with performance dashboards, deepening supplier-integrator ties. M&A activity Phibro buying Zoetis’ medicated feed additives or Innovad securing Oligo Basics shows the quest for broader portfolios and localized service teams. Such moves reinforce the moderate concentration profile of the South American feed yeast industry.

South America Feed Yeast Industry Leaders

Archer Daniels Midland Company

Cargill, Incorporated

Lallemand Inc.

dsm-firmenich AG

Nutreco N.V. (SHV Holdings)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Phibro Animal Health acquired Zoetis’ medicated feed additive lines, adding 37 products sold in 80 countries.

- October 2024: Lesaffre purchased 70% of Brazil-based Biorigin to expand functional yeast derivatives and localize production capacity.

- May 2024: Innovad Group acquired Oligo Basics, strengthening Brazilian technical support for natural additives.

South America Feed Yeast Market Report Scope

Feed yeast refers to yeast strains specifically used in animal nutrition to support growth, digestion, and overall health. Yeast provides various benefits, including improved gut health, enhanced feed efficiency, and better immune system functioning in livestock. The South American Feed Yeast Market is segmented by Type into Live Yeast, Spent Yeast, and Yeast Derivatives; By Form into Dry, Instant, and Fresh; By Animal Type into Ruminants, Poultry, Swine, and Other Animal Types and By Geography. The report offers the market sizes and forecasts in value (USD) for all the above segments.

By Product Type

| Live Cell Yeast |

| Spent Yeast |

| Dry/Inactive Yeast |

| Yeast Derivatives (Beta-glucan, MOS, etc.) |

| High-Selenium Yeast |

| Others |

By Form

| Active (Wet) |

| Instant |

| Fresh Cake |

| Liquid Slurry |

By Animal Type

| Ruminant |

| Poultry |

| Swine |

| Aquaculture |

| Companion Animals (Pets) |

By Functional Objective

| Gut Health and Immunity |

| Growth Performance |

| Mycotoxin Binding |

| Heat-Stress Mitigation |

| Others |

By Geography

| Brazil |

| Argentina |

| Chile |

| Peru |

| Colombia |

| Rest of South America |

| By Product Type | Live Cell Yeast |

| Spent Yeast | |

| Dry/Inactive Yeast | |

| Yeast Derivatives (Beta-glucan, MOS, etc.) | |

| High-Selenium Yeast | |

| Others | |

| By Form | Active (Wet) |

| Instant | |

| Fresh Cake | |

| Liquid Slurry | |

| By Animal Type | Ruminant |

| Poultry | |

| Swine | |

| Aquaculture | |

| Companion Animals (Pets) | |

| By Functional Objective | Gut Health and Immunity |

| Growth Performance | |

| Mycotoxin Binding | |

| Heat-Stress Mitigation | |

| Others | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What is the current value of the South America feed yeast market?

The South American feed yeast market is valued at USD 485.15 million in 2026 and is projected to reach USD 706.82 million by 2031.

Which country leads regional demand?

Brazil commands 53.60% of revenue owing to abundant sugarcane-ethanol by-products and a dominant poultry export sector.

Which product segment is growing fastest?

Yeast derivatives are set to expand at a 10.79% CAGR between 2026 and 2031 due to strong mycotoxin-binding performance.

How strict are antibiotic regulations in South America?

Four of the five largest meat-producing nations have banned critically important antibiotic growth promoters, boosting yeast adoption.

Page last updated on: