Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

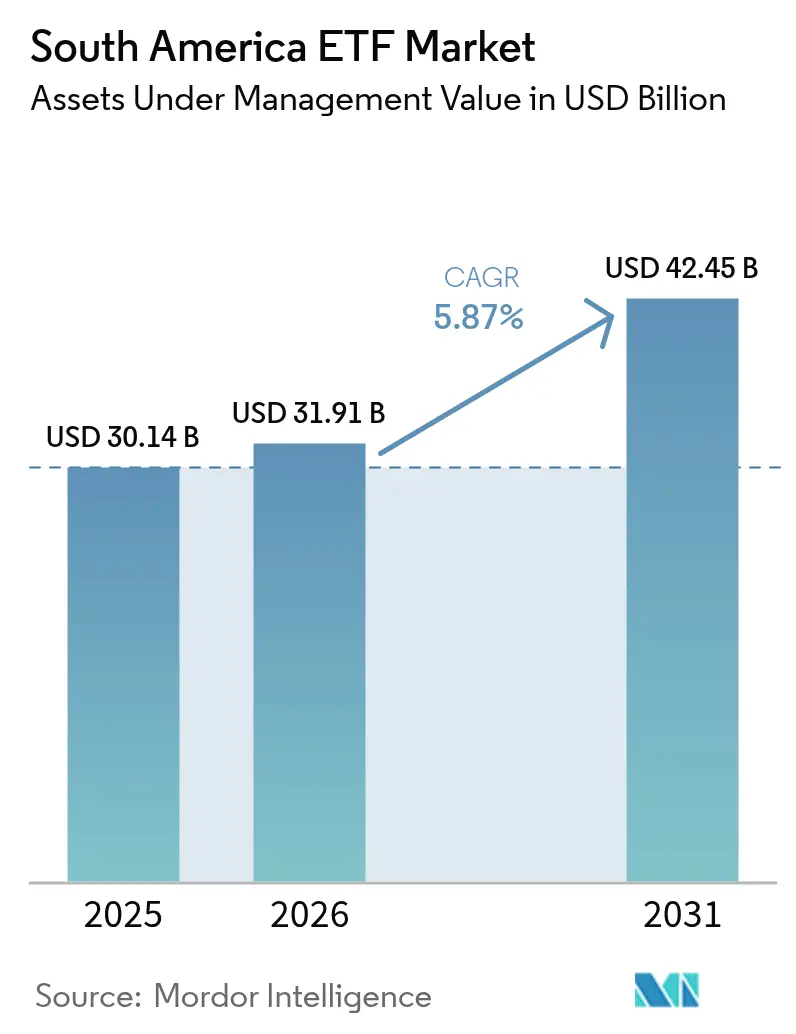

| Base Year Market Size (2025) | USD 30.14 Billion |

| Market Size (2026) | USD 31.91 Billion |

| Market Size (2031) | USD 42.45 Billion |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

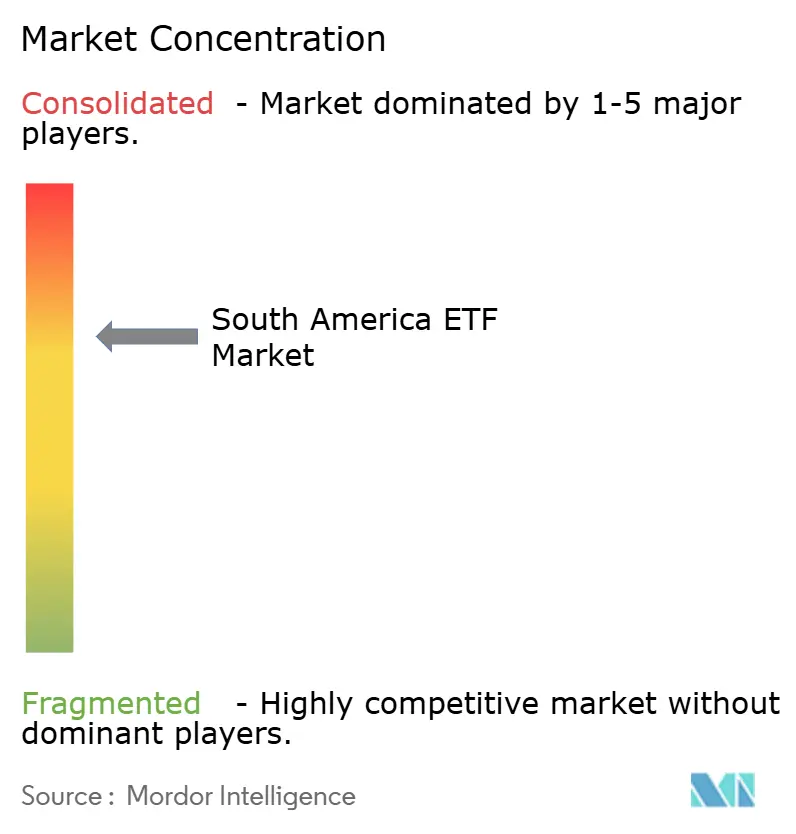

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America ETF Market Analysis by Mordor Intelligence

The South America ETF market size is expected to grow from USD 30.14 billion in 2025 to USD 31.91 billion in 2026 and is forecast to reach USD 42.45 billion by 2031 at 5.87% CAGR over 2026-2031. Intensifying financial-literacy efforts, rapid adoption of digital investment platforms, and pension-fund liberalization underpin this trajectory. Brazil’s deep capital markets ecosystem anchors regional momentum, while Colombia, Chile, and Peru accelerate growth through regulatory overhaul and commodity-linked demand. Retail participation now rivals institutional activity, reshaping asset-allocation patterns and spurring new product launches in currency-hedged, commodity, and active strategies. Against this backdrop, the South America ETF market faces structural liquidity gaps outside Brazil and taxation headwinds that could temper near-term inflows.

Key Report Takeaways

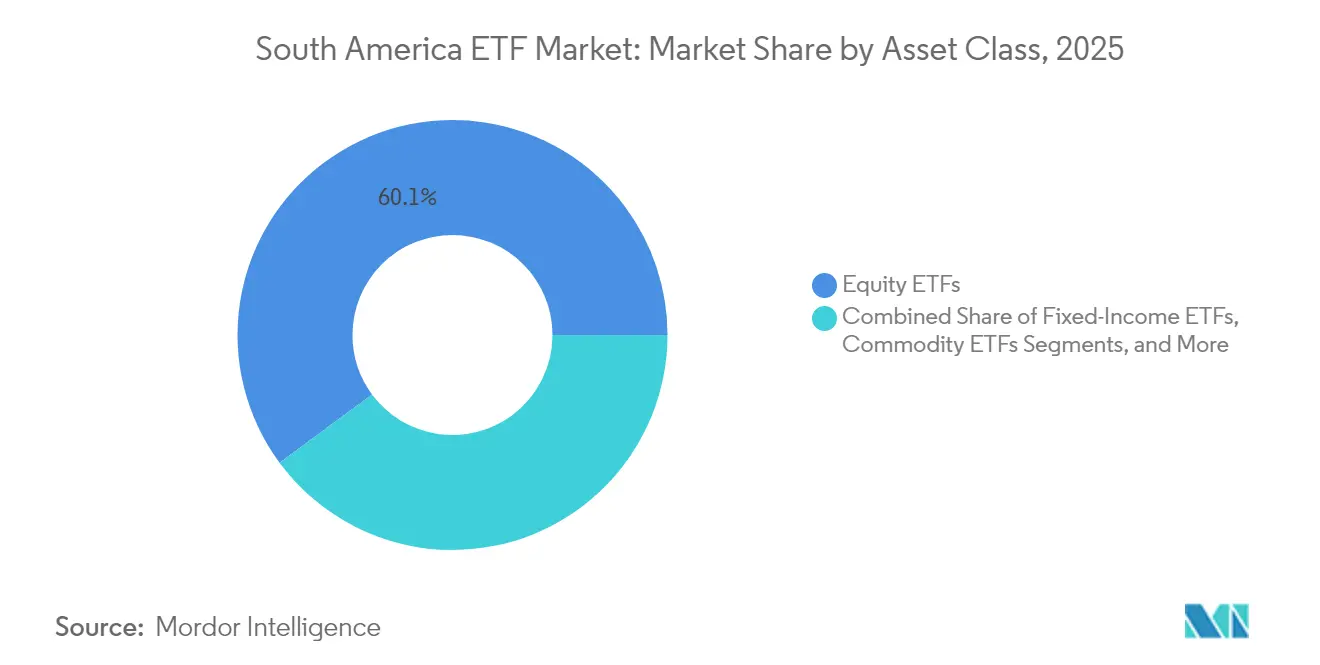

- By asset class, equity ETFs led with 60.12% share of the South America ETF market in 2025; commodity ETFs are projected to expand at a 7.43% CAGR to 2031.

- By investment strategy, passive products held 78.72% of the South America ETF market share in 2025, while active ETFs recorded the highest projected CAGR at 7.96% through 2031.

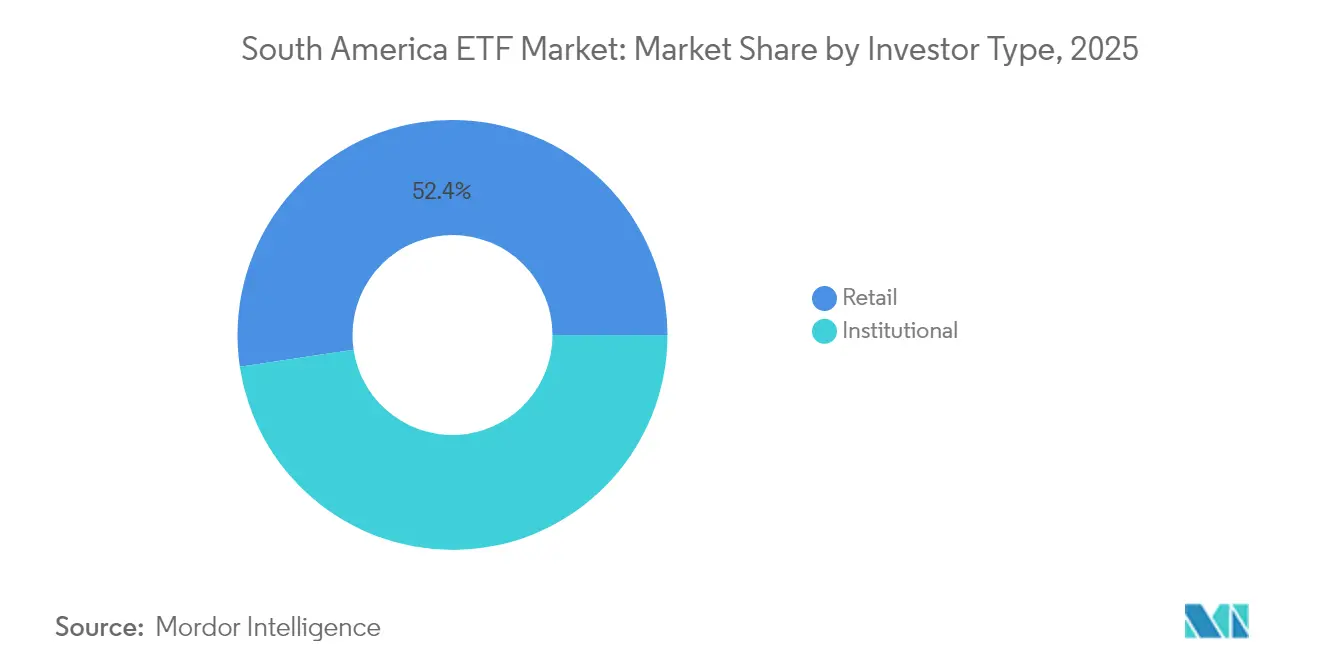

- By investor type, retail investors accounted for 52.35% share of the South America ETF market size in 2025 and are projected to advance at a 6.59% CAGR through 2031.

- By distribution channel, digital platforms captured 41.95% of the South America ETF market in 2025 flows and are forecasted to grow at a 7.11% CAGR to 2031.

- By geography, Brazil dominated with a 62.05% share of the South America ETF market in 2025; Colombia is the fastest-growing country market at a 6.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America ETF Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retail investor boom driven by digital brokers | +1.8% | Brazil, Colombia, Chile | Medium term (2–4 years) |

| Pension-fund reforms accelerating ETF adoption | +1.5% | Chile, Colombia, Peru | Long term (≥ 4 years) |

| Currency-volatility hedging via USD-linked ETFs | +1.0% | Argentina, Brazil, Colombia | Short term (≤ 2 years) |

| Regulatory green-light for active ETFs | +0.9% | Brazil, Chile | Medium term (2–4 years) |

| ESG-linked development-bank mandates | +0.7% | Brazil, Colombia, Chile | Long term (≥ 4 years) |

| Commodity-backed ETF demand amid copper & lithium cycle | +1.2% | Chile, Peru, Argentina | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Retail Investor Boom Driven by Digital Brokers

Digital platforms have lowered minimum ticket sizes and removed trading commissions, bringing 89% of Brazilian investors online, well above the 77% global average. Nearly 1.6 million first-time shareholders entered equities through zero-commission ETF offerings in a single year. Despite heightened confidence, only 26% of these newcomers feel retirement-ready, opening space for hybrid advisory models that blend robo-interfaces with professional guidance. The shift channels large daily volumes into broad-based and thematic ETFs, reinforcing the South America ETF market’s liquidity in Brazil while spotlighting education gaps elsewhere.

Pension-Fund Reforms Accelerating ETF Adoption

Chile’s revised Fund A limits now permit 80% allocation to variable-income assets, while Colombia segments mandatory funds into four risk buckets with explicit foreign-asset ceilings. These frameworks favor ETFs as cost-efficient vehicles for swift rebalancing, especially when local managers pursue global diversification mandates. Peruvian administrators follow suit, lifting alternative-asset caps and invigorating demand for multi-asset ETFs tied to infrastructure and real-estate benchmarks. As cross-border pension assets rise, the South America ETF market deepens its product shelf and fee competition intensifies[1]Organisation for Economic Co-operation and Development, “Pension Markets in Focus 2025,” oecd.org.

Currency-Volatility Hedging via USD-Linked ETFs Fuels Demand

Persistent FX swings—most acute in Argentina and episodic in Brazil—are steering capital toward dollar-linked ETFs. Argentine investors have used such products to shield portfolios as the peso weakened, while Brazilian savers accelerate hedging ahead of projected rate cuts starting December 2025. For affluent households, USD-linked fixed-income ETFs double as cash-management tools, enabling wealth preservation without direct offshore brokerage accounts. This defensive narrative feeds into daily turnover spikes whenever local currencies breach psychological thresholds.

Growing Demand for Commodity-Backed ETFs amid Copper & Lithium Super-Cycle

Chile and Peru collectively supply more than 40% of global copper, while Argentina commands sizable lithium reserves. Investors use commodity-backed ETFs to capitalize on electrification-driven demand, exemplified by the forthcoming inclusion of physical copper in Sprott’s COPP ETF in June 2025. The innovation allows simultaneous exposure to miners and metal, intensifying volume on the Santiago and Lima bourses. As green-energy policies accelerate, these products anchor diversification strategies that link resource wealth to global decarbonization narratives within the South America ETF market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Illiquidity on Secondary Exchanges Outside Brazil | -1.2% | Argentina, Chile, Colombia, Peru, Ecuador | Medium term (2-4 years) |

| Financial-Transaction Taxes (IOF, VAT) Erode Returns | -0.9% | Brazil, Argentina, Colombia | Long term (≥ 4 years) |

| Low ETF Literacy among Mass-Market Investors | -0.7% | Ecuador, Peru, Rest of South America | Medium term (2-4 years) |

| High Concentration of Assets in a Few Issuers & Indices | -0.5% | Brazil, Chile, Colombia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Illiquidity on Secondary Exchanges Outside Brazil

Fragmented market micro-structures in Argentina, Chile, and Peru translate into thin order books and wide bid-ask spreads. Institutional desks, therefore, route block trades through Brazil’s B3 or offshore venues, bypassing local exchanges and perpetuating volume shortages. The liquidity deficit raises tracking-error risk for cross-listed ETFs and deters market-maker participation, slowing the South America ETF market’s expansion beyond its Brazilian hub. Regional exchange alliances aim to harmonize clearing protocols, yet tangible progress remains elusive.

Financial-Transaction Taxes (IOF, VAT) Erode Returns

Brazil’s hike of the IOF tax in 2025 imposed a 3.5% levy on FX transactions, wiping 4.43% off the iShares MSCI Brazil ETF in a single session. Coupled with Colombia’s VAT on securities trading and Argentina’s stamp duties, these fiscal measures cut into net returns, particularly for high-turnover or leveraged strategies. Complex periodic-withholding rules on unrealized gains also raise compliance costs for fund sponsors. Unless policymakers streamline regimes, taxes will continue to depress the South America ETF market’s after-fee yields.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Commodities Drive Future Growth

Equity ETFs controlled 60.12% of the South America ETF market in 2025, reflecting a persistent appetite for diversified exposure to regional corporates. Large-cap trackers and Brazil-small-cap funds remain staples amid widening earnings forecasts. Fixed-income ETFs gained traction as real-rate differentials widened versus developed markets, offering tactical plays for duration management. Real-estate vehicles stay niche, hampered by limited REIT issuance and tax complexity in key jurisdictions.

Commodity vehicles, however, headline future acceleration: they are forecasted to expand at a 7.43% CAGR from 2026-2031, the swiftest pace of any asset class. Chilean and Peruvian copper supply and Argentine lithium reserves make metal-linked ETFs natural hedges against global electrification bottlenecks. The forthcoming physical-plus-equity structure of COPP signals rising product sophistication. Against this backdrop, the South America ETF market size for commodity products is expected to command a growing slice of regional AUM, underpinned by global manufacturers’ strategic stockpiling.

Meanwhile, currency-hedged products burst onto the scene as monetary-policy divergence amplifies FX swings. Argentine savers deploy U.S.-dollar money-market ETFs to preserve purchasing power, while Brazilian high-net-worth clients ladder maturity-based T-bill ETFs to mitigate real-depreciation risk. These cross-border flows underpin resilience in the South America ETF market, even during commodity price drawdowns.

By Investment Strategy: Active Management Gains Momentum

Passive segment held 78.72% of the South America ETF market in 2025, thanks to transparent rules-based methodologies and fee compression. Flagship vehicles linked to broad indices such as the MSCI Brazil provide investors with a one-ticket market entry. Retail brokers emphasize these offerings in model portfolios, citing simplicity and liquidity.

Yet active ETFs are projected to outpace passive peers with an 7.96% CAGR to 2031. Regulatory streamlining, semi-transparent structures, and evidence of alpha in smaller, less-efficient markets fuel this shift. Stock-picking products focusing on value-tilted Brazilian mid-caps or high-yield Andean sovereigns attract advisers seeking differentiated exposure. The South America ETF market size for active mandates is therefore poised for considerable share gains, though product success depends on track-record clarity and tax efficiency. The South America ETF market share captured by active wrappers remains modest today but could rise materially once cross-listing facilitation cuts launch costs.

By Investor Type: Retail Investors Lead Adoption

Retail account holders controlled a 52.35% slice of the South America ETF market in 2025, recording a 6.59% expected CAGR through 2031—the region’s fastest-growing client cohort. Seamless mobile onboarding and micro-investment functionality fuel mass participation, especially in Brazil, where app-based trading crossed 1 billion cumulative transactions in 2025. Gamified interfaces push thematic ETF baskets and recurring-purchase plans, embedding long-term habits among first-time savers.

Institutional investors still dominate block trades and lend crucial depth to the South America ETF market. Pension funds factor prominently: Chilean AFPs lifted foreign allocation allowances to 44% under revised statutes, while Colombian administrators reshuffle equity-bond mixes using ETFs for tactical tilts. Insurance companies adopt short-duration bond ETFs for liquidity buffers that satisfy new IFRS-17 requirements. In aggregate, institutional assets compound at a slower clip than retail but provide ballast during volatility spikes.

By Distribution Channel: Digital Platforms Revolutionize Access

Digital brokers and direct-to-consumer fintechs amassed 41.95% of the South America ETF market share in 2025 and should grow at 7.11% per year to 2031. Push-notification trade alerts, commission-free execution, and fractional share capability entice millennials and Gen Z cohorts. Educational modules integrated into trading dashboards bridge knowledge gaps and encourage product diversification.

Wealth-management hybrids expand share among mass-affluent users demanding tailored tax strategies and goal-based planning. Traditional banks defend relevance by white-labeling ETFs within discretionary mandates. Institutional platforms continue to facilitate large-scale allocations for pension and sovereign funds, though price negotiation intensifies. Ultimately, a multi-channel tapestry emerges, with the South America ETF market accommodating do-it-yourself investors and advisory-led cohorts alike.

Geography Analysis

Brazil commands a 62.05% stake of regional assets in 2025, anchored by B3’s liquidity, a sizable domestic savings pool, and a modernized regulatory code. Consolidated investment-fund equity of BRL 9.3 trillion in November 2024 provides the capital base for ETF seeding and secondary-market depth. CVM’s adoption of consolidated prospectus templates further expedites product approvals, fortifying Brazil’s centrality in the South America ETF market. Tax complexity remains an overhang, however, as IOF adjustments and periodic-withholding regimes distort net returns.

Colombia represents the region’s growth frontier, posting a 6.84% CAGR through 2031. Pension-fund segmentation—Conservative, Moderate, High Risk, Programmed Retirement—promotes asset-liability matching that naturally aligns with age-appropriate ETF portfolios. Heightened political stability and capital-market modernization initiatives attract cross-listing interest from global issuers. As liquidity improves on the Bolsa de Valores de Colombia, the South America ETF market sees a steady pipeline of local-currency and dual-currency listings.

Chile and Peru capitalize on their mining-sector dominance to attract commodity-focused inflows. Santiago’s Bolsa Electrónica enhances order-routing links with Lima to encourage arbitrage and tighter spreads. Regulatory clarity on carbon pricing bolsters demand for green-metal ETFs, aligning with sovereign decarbonization pledges. Argentina, despite macro-volatility, demonstrates resilient equity returns and sustained interest in dollar-denominated ETFs, evidencing investor appetite for asymmetric upside amid reform momentum.

Ecuador and other small jurisdictions lag due to limited brokerage penetration and nascent custody frameworks. Nevertheless, multilateral development programs aim to digitalize settlement infrastructure, suggesting medium-term tailwinds. As EU-Mercosur trade negotiations progress, European asset managers scan for partnership openings, anticipating export-led growth in lithium and agribusiness ETFs. Such milestones would expand the geographic breadth of the South America ETF market and diversify revenue streams away from Brazil-centric flows.

Competitive Landscape

Dominant incumbents include BlackRock’s iShares franchise, XP Asset Management, and Itaú Asset Management, each leveraging proprietary distribution or first-mover lineage. BlackRock maintains product depth across equities, fixed income, and factors, supported by robust market-making agreements that tighten spreads. XP Inc. exploits its 4.7 million-strong retail client base and R$1.3 trillion in assets to launch local-currency ETFs capturing thematic niches such as Chinese equities and domestic gold proxies.

VanEck and DWS scale presence via sub-advisory deals, while Abrdn’s distribution accord with Capital Strategies Partners exemplifies partnership strategies to overcome regulatory hurdles. SPDR’s entry into physically backed metal ETFs signals intensifying competition in commodity segments—an area historically underserved by local providers. As product shelves expand, cost competition escalates, compressing expense ratios and fostering consolidation among smaller issuers unable to shoulder seeding burdens.

Technology acts as a pivotal differentiator. Digital-native issuers employ cloud-based order-management systems and API-driven data feeds to streamline compliance updates and potentiate intraday disclosures. BlackRock targets active-fund expansion, aspiring to join Brazil’s top-10 asset managers within five years by diversifying into fixed income. XP’s in-house robo-adviser plugs model-portfolio ETFs into automated rebalancing, enhancing stickiness. Collectively, these moves amplify the South America ETF market’s competitive intensity and accelerate product innovation cycles[3]BlackRock, “Latin American Investment Trust 2025 Outlook,” blackrock.com.

South America ETF Industry Leaders

BlackRock Inc. (iShares)

VanEck

XP Inc. (XP Asset Management)

ProShares

WisdomTree

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sprott Asset Management announced its Copper Miners ETF (COPP) will add physical copper exposure on June 23, 2025, creating the first ETF with twin exposure to metal and miners.

- May 2025: Brazil’s IOF tax hike sparked a 4.43% drop in the iShares MSCI Brazil ETF (EWZ) to USD 26.30, underscoring regulatory risk to ETF returns.

- February 2025: BlackRock’s Latin American Investment Trust Outlook flagged compelling valuations, and elevated dividend yields across Brazilian equities despite policy uncertainty.

- January 2025: Brazil introduced periodic withholding taxes on unrealized gains for certain funds, with ETFs classified as investment entities taxed at 15% on liquidity events.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South America exchange-traded fund (ETF) market as the combined net asset value of every ETF domiciled in, or formally cross-listed into, regulated exchanges across Brazil, Argentina, Chile, Colombia, Peru, and Ecuador.

Scope Exclusions: Leveraged or inverse notes, closed-end funds, and exchange-traded notes that lack ETF status are outside this scope.

Segmentation Overview

- By Asset Class

- Equity ETFs

- Fixed-Income ETFs

- Commodity ETFs

- Currency ETFs

- Real-Estate ETFs

- Alternative ETFs

- By Investment Strategy

- Active

- Passive

- By Investor Type

- Retail

- Institutional

- By Distribution Channel

- Direct and Digital Retail Platforms

- Financial Advisors and Wealth Managers

- Institutional Channels

- Traditional Banks and Full-Service Brokers

- By Country

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Ecuador

- Rest of South America

Detailed Research Methodology and Data Validation

Primary Research

We interview exchange officials, market-makers, index sponsors, and digital-platform executives from Sao Paulo to Bogota, and survey multi-asset portfolio managers.

These discussions test secondary findings, surface undocumented cross-listing plans, and calibrate growth assumptions with ground-level sentiment.

Desk Research

We start with macro-financial datasets from the World Bank, IMF, and each national securities commission, grounding our view of household savings, trading velocity, and currency swings.

Our analysts then mine exchange bulletins, IOSCO filings, and ETFGI snapshots to map listings, flows, and fee ladders.

Company filings, audited fund prospectuses, and news archives accessed through Dow Jones Factiva and D&B Hoovers confirm assets under management and launch pipelines.

Pension-fund statistics and association white papers refine retail and institutional adoption metrics.

The sources cited illustrate rather than exhaust the references consulted.

Market-Sizing & Forecasting

A top-down assets-in-place rebuild begins with exchange-reported AUM and turnover, which are then segmented by asset class and strategy.

Select bottom-up checks, issuer roll-ups and average fee x asset calculations, validate totals.

Key variables such as quarterly net flows, pension-mandate changes, digital-platform account openings, local-currency volatility, and MSCI-index inclusion feed a multivariate regression that projects values through 2030, with elasticities vetted by interviewees.

Data Validation & Update Cycle

Model outputs pass variance thresholds against independent benchmarks; any anomaly triggers senior-analyst review before sign-off.

Reports refresh once a year, while material events such as tax changes prompt interim updates, and a final data sweep occurs just before publication.

Why Mordor's South America ETF Industry Size & Share Analysis Baseline commands reliability

Published ETF estimates often differ because providers choose unlike fund universes, currency bases, and refresh cadences, and we acknowledge these drivers so users can see how definitions alone swing billions.

The largest gap arises from scope: Mordor includes cross-listed U.S. and European vehicles that trade actively on regional exchanges, whereas several consultancies restrict valuations to locally domiciled funds, freeze exchange rates at survey dates, or ignore secondary-market holdings, widening the divide.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 30.14 B (2025) | Mordor Intelligence | |

| USD 9.24 B (2024) | Global Consultancy A | Omits cross-listed ETFs and funds below USD 50 M AUM |

| USD 9.24 B (2025) | Regional Consultancy B | Counts only primary-market creations; no turnover adjustment |

| USD 22.16 B (2024) | Industry Tracker C | Snapshot AUM only; excludes pipeline and currency effects |

Taken together, the comparison shows that our broader yet clearly articulated scope, transparent variable set, and disciplined annual updates give decision-makers a baseline they can trace, replicate, and stress-test with confidence.

Key Questions Answered in the Report

What is the current value of the South America ETF market?

The South America ETF market size is USD 31.91 billion in 2026 and is projected to rise to USD 42.45 billion by 2031.

Which asset class is expected to grow the fastest within South American ETFs?

Commodity ETFs are forecast to expand at a 7.43% CAGR between 2026 and 2031 due to demand for copper and lithium exposure.

How important are retail investors in the regional ETF landscape?

Retail investors hold 52.35% of assets in 2025 and are advancing at a 6.59% CAGR, making them the largest and fastest-growing investor segment.

Why are active ETFs gaining traction in South America?

Regulatory reforms such as Brazil’s CVM Resolution 175 have streamlined approvals, enabling active strategies to seek alpha in less-efficient local markets and grow at an 7.96% CAGR.

What are the main challenges facing ETF growth outside Brazil?

Secondary-market illiquidity on smaller exchanges and transaction-tax regimes like Brazil’s IOF and Colombia’s VAT can widen spreads and erode net returns.

Which country is projected to record the highest ETF growth rate through 2031?

Colombia leads with a 6.84% CAGR, driven by pension-fund reforms and increased cross-border investment inflows.

Page last updated on: