Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

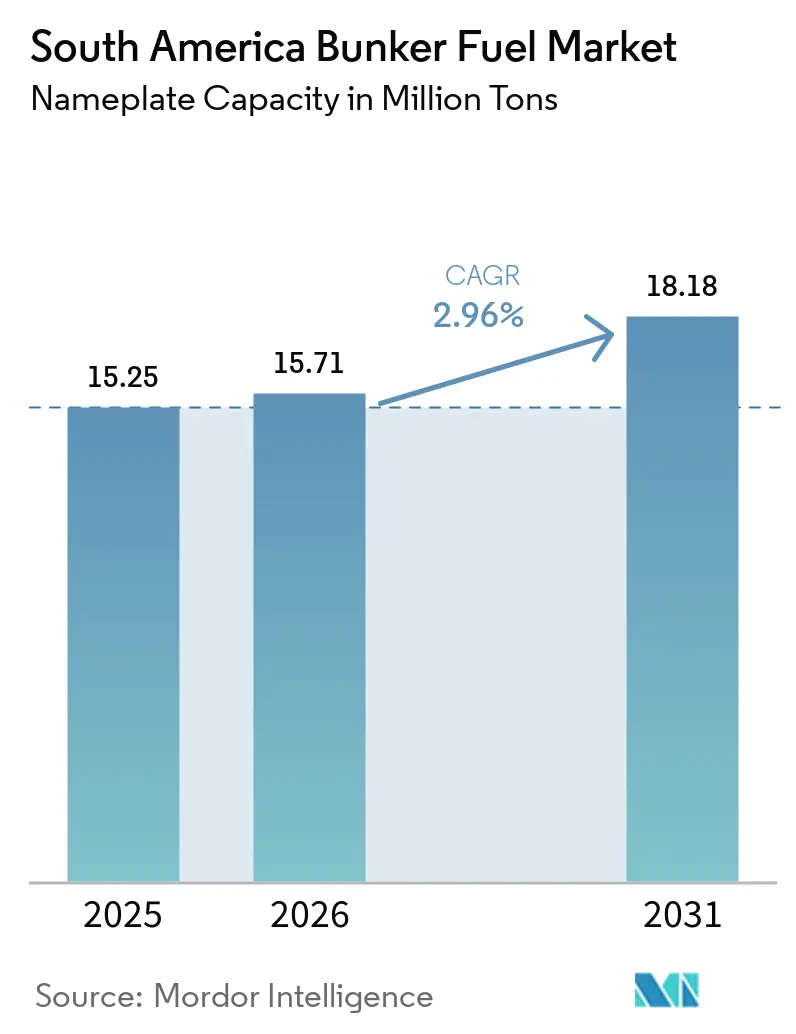

| Base Year Market Size (2025) | 15.25 Million tons |

| Market Volume (2026) | 15.71 Million tons |

| Market Volume (2031) | 18.18 Million tons |

| Growth Rate (2026 - 2031) | 2.96% CAGR |

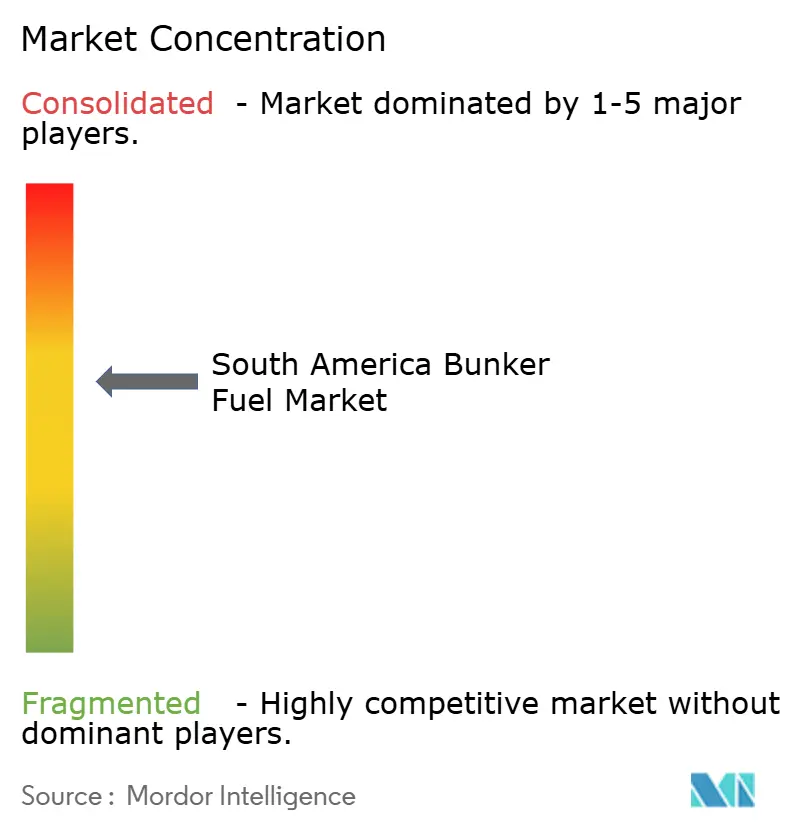

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Bunker Fuel Market Analysis by Mordor Intelligence

The South America Bunker Fuel Market size in terms of nameplate capacity is projected to expand from 15.25 million tons in 2025 and 15.71 million tons in 2026 to 18.18 million tons by 2031, registering a CAGR of 2.96% between 2026 to 2031. This moderate trajectory reflects a maritime-fuel landscape where high-sulfur fuel oil (HSFO) continues to dominate volumes even as liquefied natural gas (LNG) gains momentum in response to International Maritime Organization emission limits and sulfur-tax incentives.[1]International Maritime Organization, “IMO 2020 Global Sulphur Limit,” IMO, imo.org Brazil remains the principal demand center, anchored by pre-salt crude exports and the region’s deepest port infrastructure. Argentina’s growth accelerates as recent policy changes open its ports to third-party suppliers, while Chile and Uruguay position themselves as alternative hubs that benefit from congestion spillovers in Brazil. Competitive intensity is rising because Petrobras’s refinery divestments invite independent traders, digital procurement platforms, and first-mover biofuel suppliers to establish new physical supply chains.

Key Report Takeaways

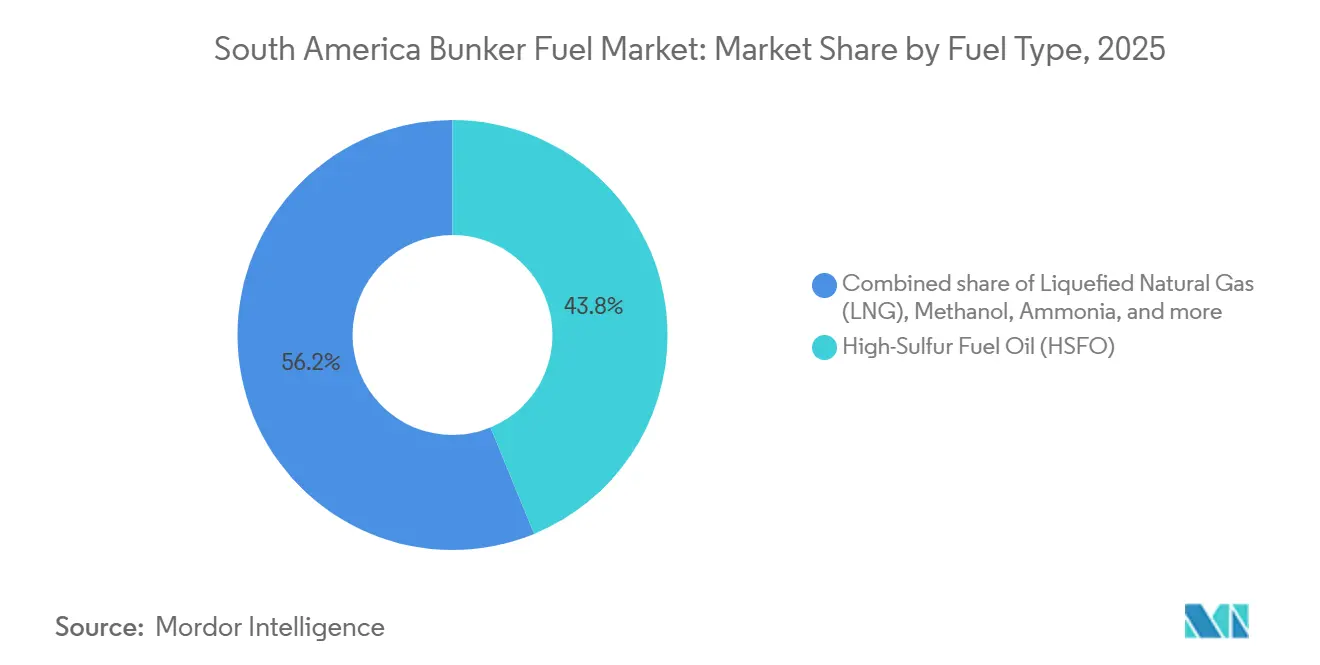

- By fuel type, HSFO led with 43.8% share in 2025, while LNG is forecast to expand at a 13.3% CAGR through 2031.

- By bunkering method, ship-to-ship transfers accounted for 50.2% of 2025 volumes; LNG barge-to-ship delivery is expected to post a 12.5% CAGR between 2026-2031.

- By vessel type, tanker vessels held 29.9% of the South America bunker fuel market share in 2025, whereas container vessels are projected to grow at a 6.9% CAGR to 2031.

- By geography, Brazil commanded 60.3% of regional demand in 2025, whereas Argentina is advancing at a 6.4% CAGR following the removal of bunker-quantity limits in late 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Bunker Fuel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising marine transportation of essential commodities in South America | +0.8% | Brazil, Argentina, Chile; spillover to Uruguay, Peru | Medium term (2-4 years) |

| Supportive IMO-2020 compliant fuel-switching incentives and local sulfur-tax breaks | +0.6% | Brazil (ANTAQ), Argentina (Prefectura Naval), Chile (Directemar) | Short term (≤ 2 years) |

| Accelerating pre-salt crude exports driving bunkering demand at Brazilian and Uruguayan hubs | +0.7% | Brazil (Santos, Rio de Janeiro), Uruguay (Montevideo) | Long term (≥ 4 years) |

| Rapid port-call growth on Asia-South America container loops post-Panama Canal expansions | +0.5% | Brazil (Santos, Paranaguá), Argentina (Buenos Aires), Chile (Valparaíso-San Antonio) | Medium term (2-4 years) |

| Petrobras refinery divestments unlocking third-party physical supply and price competition | +0.3% | Brazil (national), with early gains in Santos, Rio de Janeiro | Medium term (2-4 years) |

| Pilot-scale bio-bunker (B24-B30) certification creating first-mover advantage for low-carbon blends | +0.2% | Brazil (Santos, Paranaguá), Peru (Callao), Colombia (Cartagena) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Marine Transportation Of Essential Commodities In South America

Exports of soybeans, corn, iron ore, copper, and lithium continue to lift voyage counts and sustain bunker demand across major Atlantic and Pacific ports. Brazil shipped 102 million tons of soybeans and 55 million tons of corn in 2024, while Vale moved 380 million tons of iron ore primarily to China.[2]United States Department of Agriculture, “Oilseeds: World Markets and Trade,” USDA, usda.gov Chile exported 5.5 million tonnes of copper and 180,000 tons of lithium carbonate, feeding steady bunker liftings at Valparaíso, San Antonio, and Quintero.[3]Chilean Copper Commission, “Chile Copper Exports 2025,” Cochilco, cochilco.cl Argentina’s Vaca Muerta pipeline project will allow very large crude carriers to load by 2027, creating additional uplift demand at Punta Colorada. Commodity flows remain resilient because longer transit times offset slow-steaming fuel savings. Infrastructure expansions scheduled through 2028 will cement this medium-term influence on the South America bunker fuel market.

Supportive IMO-2020 Compliant Fuel-Switching Incentives And Local Sulfur-Tax Breaks

Regulators introduced cost-relief mechanisms that reward vessels burning lower-sulfur fuels. Brazil’s National Waterway Transport Agency waives port-fee surcharges for fuels at or below 0.10% sulfur, and Argentina’s Prefectura Naval grants dockage-fee reductions for ISO 8217-compliant deliveries.[4]Brazilian National Waterway Agency, “Sulphur Tax Incentive Program,” ANTAQ, antaq.gov.br Chile aligned with IMO 2020 requirements in 2025, accelerating the shift from 3.5% sulfur HSFO to VLSFO and MGO. These measures prompt shipowners to retrofit scrubbers or switch to compliant fuels within the next two years. They also establish a precedent for differentiated port charges tied to carbon intensity, likely supporting emerging LNG and methanol supply chains.

Accelerating Pre-Salt Crude Exports Boosting Demand At Brazilian And Uruguayan Hubs

Petrobras’s pre-salt output reached 2.86 million barrels per day in late 2024, and new floating production units will push capacity above 3.2 million barrels per day by 2026. Each additional Suezmax or Aframax voyage departing Santos or Rio de Janeiro typically takes on 1,200-1,800 tons of bunker fuel, adding roughly 400,000 tons of annual demand by 2028. Uruguay’s Montevideo port, upgraded under a long-term concession, is attracting spillover traffic from Brazilian crude terminals. Sustained Chinese and Atlantic Basin crude imports support a structural rise in tanker-borne fuel demand, bolstering the South America bunker fuel market outlook.

Rapid Port-Call Growth On Asia-South America Container Loops

Liner operators expanded direct Asia services after Panama Canal slot normalization. Maersk’s AE55 and Ocean Network Express’s SAX rotations add more than 120 container-ship calls annually to Santos and Paranaguá. Santos alone handled 4.37 million TEU in the first nine months of 2025, up 7.8% year on year. Additional calls translate into an estimated 180,000 tons of incremental bunker demand each year, primarily served offshore to minimize berth delays. Rising Brazil-China trade volumes and Argentine import liberalization support continued fleet deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent crude-price volatility impacting bunker price stability | -0.4% | Regional, with acute effects in Brazil (Santos, Rio) and Argentina (Buenos Aires) | Short term (≤ 2 years) |

| Delayed LNG bunkering infrastructure build-out across Atlantic and Pacific coasts | -0.3% | Brazil (Santos, Rio Grande), Uruguay (Montevideo), Chile (Valparaíso, Quintero) | Medium term (2-4 years) |

| Quality-control issues: VLSFO/HSFO off-spec rates exceeding 5.9% in region | -0.2% | Regional, concentrated in secondary ports with limited testing facilities | Short term (≤ 2 years) |

| Feedstock competition inflating bio-bunker input costs (soy oil, methanol) | -0.1% | Brazil (Midwest soy belt), Argentina (Rosario, Buenos Aires) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Crude-Price Volatility Impacting Bunker Price Stability

Brent crude oscillated between USD 70 and USD 90 per barrel during 2025, driving 15-20% monthly swings in VLSFO and HSFO prices at Santos and Buenos Aires. Shipowners on fixed freight contracts experience margin pressure and often defer bunkering when local premiums exceed USD 30 per ton relative to benchmark hubs. Only 22% of South American volumes moved under quarterly fixed-price deals in 2025, far below Singapore’s 45% share, which forces traders to hold larger working-capital buffers. Limited derivative liquidity, South America accounts for less than 2% of global marine-fuel swaps, hampers risk-management options.

Delayed LNG Bunkering Infrastructure Build-Out Across Atlantic And Pacific Coasts

Only three of twelve proposed small-scale LNG terminals achieved financial close by end-2025, leaving dual-fuel vessels reliant on truck-to-ship transfers under 80 tons per operation. Maersk and CMA CGM routinely detour to Caribbean or European hubs for LNG bunkering, curtailing regional volumes to roughly 120,000 tons in 2025 despite double-digit demand potential. Uruguay’s GNL Del Plata project will mitigate the shortfall after its expected 2027 start, but Brazil’s Atlantic and Chile’s Pacific terminals remain stalled over offtake agreements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: HSFO Dominance Gives Way To Steady LNG Expansion

High-sulfur fuel oil retained 43.8% of the South America bunker fuel market share in 2025, supported by a large fleet of scrubber-equipped tankers and bulk carriers that can legally consume 3.5% sulfur fuel. LNG volumes, though smaller, are projecting a 13.3% CAGR that will steadily erode HSFO share as more dual-fuel vessels enter service. VLSFO serves container and general-cargo vessels that have not installed exhaust-gas-cleaning systems, while MGO fills niche auxiliary-engine demand where fuel-quality thresholds are strict. Methanol, ammonia, and synthetic fuels remain embryonic because engines and handling infrastructure are limited, yet multiple liner operators have placed methanol-capable vessels on order for post-2027 deployment. Bio-bunkers occupied roughly 1.2% of 2025 volumes and hinge on feedstock economics; cost parity with MGO will determine whether the category scales beyond early-adopter volumes.

The South America bunker fuel market size attributable to LNG could rise from 950,000 tons in 2025 to more than 2 million tons by 2031 if shore-side infrastructure reaches the planned twelve terminals. Delivered LNG in Santos averaged USD 14 per MMBtu in 2025, which equates to a 12-15% fuel-cost saving versus VLSFO on an energy-equivalent basis, although capital amortization for dual-fuel engines narrows the margin over a 20-year horizon. ULSFO retains a niche role for vessels entering emission-control areas outside the region, but limited South American demand keeps blended supply tight. The South America bunker fuel market continues to balance cost, compliance, and infrastructure maturity when allocating bunker-fuel budgets across HSFO, VLSFO, LNG, and emerging alternatives.

By Bunkering Method: Offshore Transfers Sustain Efficiency, LNG Barges Emerge

Ship-to-ship transfers captured 50.2% of 2025 volumes because offshore deliveries minimize port dwell time, a key benefit when Santos terminals average three-day queues. Tankers and container ships alike schedule mid-passage refueling that allows continuous cargo operations and reduces congestion surcharges. Port-to-ship truck and pipeline deliveries remain important for MGO and VLSFO in terminals with refinery connections, but their share is slipping as vessel sizes increase and operators demand quicker turnarounds. Portable tank solutions meet residual demand in remote Chilean and Peruvian locations where fixed assets are absent.

LNG barge-to-ship delivery represents the fastest-growing method, poised for a 12.5% CAGR once Brazil’s Paranaguá and Uruguay’s GNL Del Plata facilities come online. The South America bunker fuel market size linked to LNG barges could triple by 2031 as dual-fuel container vessels schedule synchronized bunkering alongside cargo operations. Regulatory support is improving; Brazil’s ANTAQ published simultaneous cargo and LNG bunkering guidelines in 2024 that align with International Gas Carrier Code safety standards. As infrastructure matures, the mix will tilt toward barges that provide higher throughput and safer handling compared with truck transfers.

By Vessel Type: Tanker Incumbency Faces Container-Ship Surge

Tankers held 29.9% of total consumption in 2025, supported by Vale’s Valemax ore carriers and Petrobras crude exports that require large bunker stems before trans-Atlantic voyages. The segment’s share will soften marginally as slow-steaming offsets part of the added voyage count, but absolute volumes continue climbing with pre-salt output. Container vessels present the fastest expansion at 6.9% CAGR, driven by new weekly loops that employ 10,000 TEU tonnage and require 400-600 tons per call. Bulk carriers, which lift Brazil’s grain and Chile’s copper cargoes, show seasonal spikes tied to harvest cycles, prompting suppliers to pre-stage inventories during second-quarter peaks.

The South America bunker fuel market size for container vessels reached an estimated 4.3 million tons in 2025 and could approach 6 million tons by 2031 if planned port expansions sustain double-digit TEU growth. Offshore support vessels and seismic ships represent a small but strategic category that demands higher-grade fuels such as MGO and ULSFO near offshore installations. Passenger and ro-pax ferries remain niche, concentrated in southern Chilean fjords and Argentine coastal services, yet they exemplify early adopters of bio-fuel blends under corporate carbon programs.

Geography Analysis

Brazil's bunker-fuel ecosystem is anchored by Santos and Rio de Janeiro, where refinery proximity, deepwater access, and pre-salt crude exports underpin steady demand growth. Current volumes exceed 9 million tons and could rise 2% annually if crude output meets Petrobras' guidance. Diverse fuel availability, from HSFO to bio-blends, gives Brazil pricing power, yet refinery divestments are lowering barriers for foreign traders that offer digital ordering and flexible credit terms. Future expansion hinges on LNG terminal completion at Paranaguá and on the successful deployment of blockchain-based delivery notes that reduce dispute risk.

Argentina is regaining a competitive footing after December 2025 reforms scrapped bunker-quantity caps and invited independent suppliers into Buenos Aires and Zona Común. Spot premiums narrowed, and physical supply climbed to nearly 2 million tons as GAC and others entered the market. Vaca Muerta pipeline completion will attract VLCCs that each uplift more than 2,000 tons per voyage, reinforcing a 6.4% forecast CAGR. The main challenge remains macroeconomic stability, because currency and financing volatility can deter sustained supplier presence.

The rest of South America, chiefly Chile, Uruguay, Peru, Colombia, and Ecuador, collectively accounts for just under 30% of regional demand. Montevideo's USD 455 million terminal upgrade positions it as a transshipment and overflow hub, especially when Santos congestion surges. Callao's successful bio-fuel pilot marks the Pacific coast's first low-carbon option, while Valparaíso and San Antonio lag until LNG and VLSFO storage projects reach sanction. Colombia's Caribbean ports explore LNG barges that could interconnect with Trinidad's liquefaction infrastructure, offering dual-fuel vessels a new bunkering waypoint on north-south trades.

Competitive Landscape

The South America bunker fuel market is moderately concentrated. The five largest suppliers, Petrobras, Vitol, Monjasa, Bunker Holding, and World Fuel Services, together held a roughly 58% share in 2025, yet no single company exceeded 18% because Petrobras’s divestments diluted its historical dominance. Integrated majors leverage refinery-to-barge networks to guarantee supply quality, whereas independent traders differentiate through digital procurement, multi-refiner aggregation, and flexible credit. LNG and bio-fuel infrastructure represent the next battleground; only three ports offered LNG bunkering in 2025, creating first-mover advantages for suppliers willing to co-invest in floating storage and regasification units.

Technology adoption is accelerating. Monjasa piloted a blockchain-based bunker delivery note in Santos that cut claim resolution times from 45 days to 7 days, raising liquidity and lowering counterparty risk. Independent distributors such as GAC Argentina and Risler win share with same-day truck deliveries that circumvent barge lead times at Buenos Aires terminals. Verification laboratories Veritas and SGS provide on-site testing that reduces quality disputes, leveling entry barriers for smaller traders. Over the forecast horizon, new LNG terminals and biofuel certifications will redraw supplier ranks, enabling additional global players to enter the South America bunker fuel market as physical capacity scales.

Strategic moves continued through 2025. Vitol deployed specialist bio-fuel barges in Brazil and Colombia with monthly volume targets of up to 7,000 tons, positioning the trader ahead of tighter IMO carbon-intensity rules. World Fuel Services reported 40% growth in online bookings from South American ports, signaling shipowner appetite for transparent pricing and faster confirmations. Petrobras allocated USD 111 billion in capital spending through 2029, partly to expand upstream output that will elevate downstream bunker sales, even as refinery divestment frees market space for newcomers. Competitive intensity will deepen as new LNG and biofuel capacity comes online, particularly in Brazil, Uruguay, and Peru.

South America Bunker Fuel Industry Leaders

Petrobras

Vitol Holding BV

Bunker Holding A/S

World Fuel Services Corp

Peninsula Petroleum Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Adani Ports and Special Economic Zone (APSEZ) announced the acquisition of a 10-year marine services contract for Argentina's first LNG export project. The agreement entails an investment of approximately USD 70 million and focuses on developing LNG-related port and maritime infrastructure in the country. This project is anticipated to enhance Argentina's role in the regional LNG supply chain and foster opportunities for future LNG bunkering and alternative marine fuel services in South America.

- November 2025: At the São Sebastião Waterway Terminal (Tebar) in São Paulo, Petrobras provided three Transpetro ships with bunker fuel that boasts a 24% renewable content. This fuel, enriched with 24% biodiesel, was sourced from Petrobras Biocombustível (PBio).

- January 2025: Viroque Energy, an international energy firm, has launched a new physical bunker supply operation at the port of Cartagena de Indias, Colombia. This move underscores the company's strategic push into the Latin American market.

- April 2024: Monjasa, an international bunkering firm, delivered 510 tons of B30 marine biofuels to the "Infinity Sky," a dry bulk carrier operated by Cargill, at the Port of Callao in Peru. This operation not only marked the inaugural ISCC-certified biofuels supply on South America's Pacific Coast but also laid the groundwork for a scalable second-generation marine biofuels supply chain.

South America Bunker Fuel Market Report Scope

Bunker fuel, often referred to as bunker oil, is a heavy, low-grade fuel primarily used to power large ships and select aircraft. The term "bunker" harks back to early steamships, where storage areas for coal were termed bunkers. Derived as a residual product from crude oil refining, bunker fuel is typically thick and tar-like, known in the industry as Heavy Fuel Oil (HFO). This viscosity necessitates heating for pumping. Traditionally high in sulfur content, the industry is witnessing a shift towards cleaner and lighter marine fuels.

The South America bunker fuel market is segmented by fuel type, bunkering method, vessel type, and geography. By fuel type, the market is segmented into high-sulfur fuel oil (HSFO), very-low-sulfur fuel oil (VLSFO), ultra-low-sulfur fuel oil (ULSFO), marine gas oil (MGO), liquefied natural gas (LNG), methanol, bio-/synthetic fuels, ammonia, and other fuel types. By bunkering method, the market is segmented into ship-to-ship, port-to-ship, LNG barge-to-ship, and portable tanks and containers. By vessel type, the market is segmented into container vessels, tankers, bulk carriers, general cargo vessels, passenger/Ro-Pax vessels, and offshore and specialized vessels. By geography, the market is segmented into Brazil, Argentina, Chile, and the Rest of South America. For each segment, the market sizing and forecasts are provided on the basis of volume (million tons).

By Fuel Type

| High-Sulfur Fuel Oil (HSFO) |

| Very-Low-Sulfur Fuel Oil (VLSFO) |

| Ultra-Low-Sulfur Fuel Oil (ULSFO) |

| Marine Gas Oil (MGO) |

| Liquefied Natural Gas (LNG) |

| Methanol |

| Bio-/Synthetic Fuels |

| Ammonia |

| Other Fuel Types |

By Bunkering Method

| Ship-to-Ship |

| Port-to-Ship (Truck/Pipeline) |

| LNG Barge-to-Ship |

| Portable Tanks and Containers |

By Vessel Type

| Container |

| Tanker |

| Bulk Carrier |

| General Cargo |

| Passenger/Ro-Pax |

| Offshore and Specialized |

By Geography

| Brazil |

| Argentina |

| Chile |

| Rest of South America |

| By Fuel Type | High-Sulfur Fuel Oil (HSFO) |

| Very-Low-Sulfur Fuel Oil (VLSFO) | |

| Ultra-Low-Sulfur Fuel Oil (ULSFO) | |

| Marine Gas Oil (MGO) | |

| Liquefied Natural Gas (LNG) | |

| Methanol | |

| Bio-/Synthetic Fuels | |

| Ammonia | |

| Other Fuel Types | |

| By Bunkering Method | Ship-to-Ship |

| Port-to-Ship (Truck/Pipeline) | |

| LNG Barge-to-Ship | |

| Portable Tanks and Containers | |

| By Vessel Type | Container |

| Tanker | |

| Bulk Carrier | |

| General Cargo | |

| Passenger/Ro-Pax | |

| Offshore and Specialized | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size of the South America bunker fuel market?

The market is worth 15.71 million tons in 2026 and is forecast to reach 18.18 million tons by 2031.

Which fuel type leads bunker demand in South America?

HSFO remains dominant with a 43.8% share in 2025, although LNG is expanding at the fastest pace.

Why is Brazil so influential in regional bunker sales?

Pre-salt crude exports, deep-draft ports, and diversified fuel availability give Brazil 60.3% of regional demand.

How fast is LNG bunkering growing?

LNG bunker volumes are projected to increase at a 13.3% CAGR between 2026 and 2031, pending infrastructure completion.

What challenges limit bio-fuel adoption for ships?

High soybean-oil costs and limited methanol supply keep B24-B30 blends priced USD 100-150 per tonne above conventional MGO.

Which company pioneered blockchain-verified bunker delivery notes in the region?

Monjasa introduced a blockchain BDN platform in Santos that reduced claim resolution times to one week.

Page last updated on: