Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

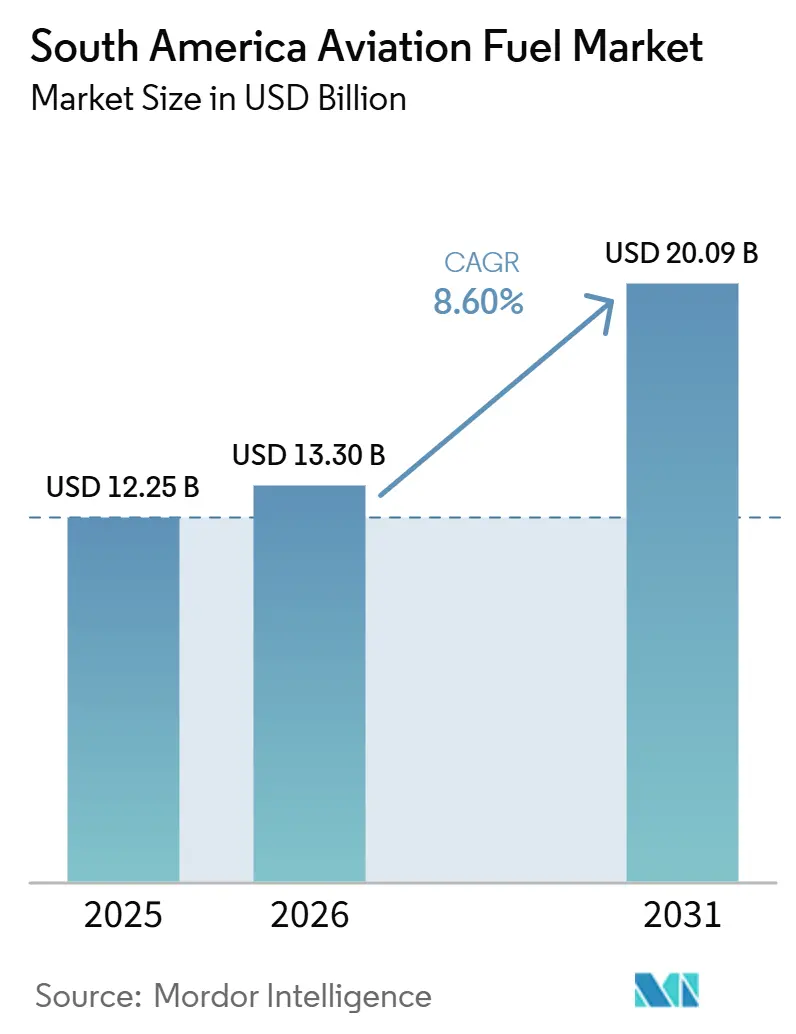

| Base Year Market Size (2025) | USD 12.25 Billion |

| Market Size (2026) | USD 13.30 Billion |

| Market Size (2031) | USD 20.09 Billion |

| Growth Rate (2026 - 2031) | 8.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Aviation Fuel Market Analysis by Mordor Intelligence

The South America Aviation Fuel Market size was valued at USD 12.25 billion in 2025 and is estimated to grow from USD 13.30 billion in 2026 to reach USD 20.09 billion by 2031, at a CAGR of 8.60% during the forecast period (2026-2031). The market is entering a more binding phase because Brazil’s Future Fuel Law starts to convert SAF demand from a voluntary option into a compliance requirement, while international aviation is moving under a stricter CORSIA framework in the same period, which changes procurement planning across airlines, refiners, and airport fuel operators. Demand conditions are also improving because Latin America and Caribbean airlines posted 8.6% year-on-year RPK growth in Q1 2026, while Brazil’s domestic RPK rose 11.4%, which supports higher aircraft utilization and stronger jet fuel offtake across the region. At the same time, airport expansion and fuel handling upgrades in Brazil and Peru are improving the operating base needed for larger aircraft movements, denser schedules, and more reliable fuel storage and delivery systems. Cost remains the main friction point because SAF still carries a steep premium over conventional jet fuel, and that burden is magnified in countries where airline revenues are local but fuel purchasing is linked to USD pricing. Even with those constraints, the South America aviation fuel market is set up for sustained expansion because traffic growth, regulation, refinery adaptation, and airport modernization are all moving in the same direction.

Key Report Takeaways

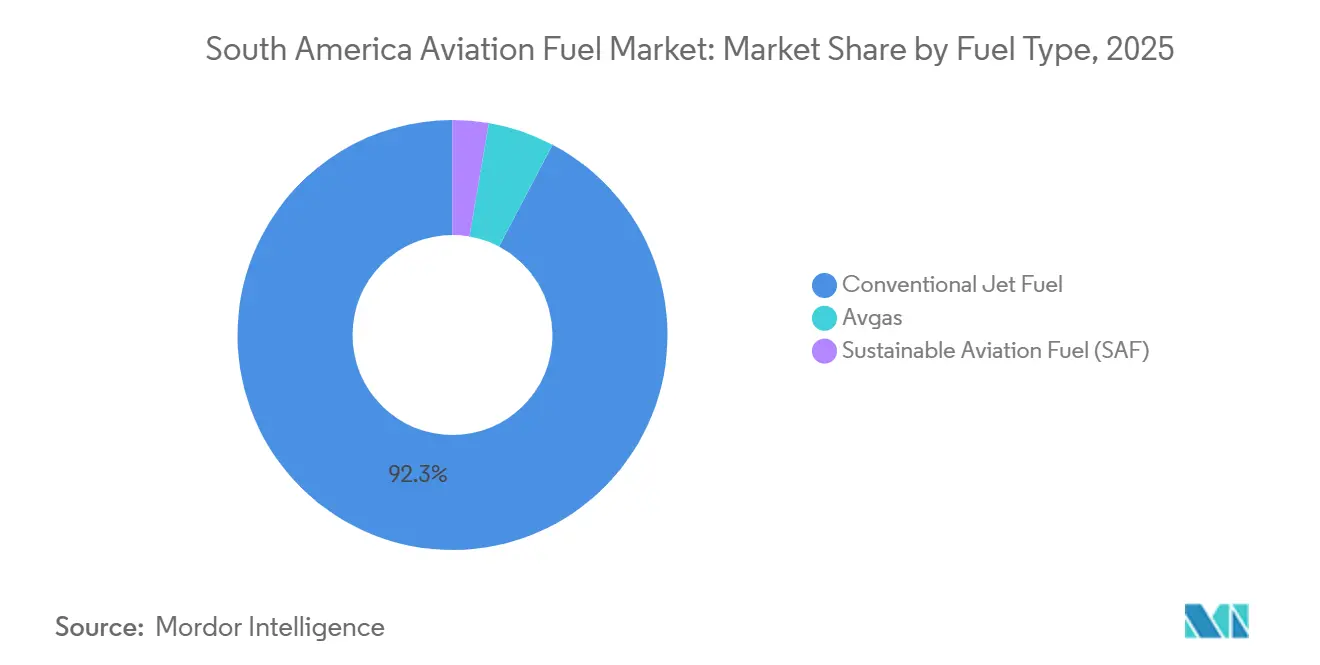

- By fuel type, conventional jet fuel held 92.3% of demand in 2025, while SAF is forecast to expand at a 28.6% CAGR through 2031.

- By aircraft type, narrow-body aircraft accounted for 58.7% of demand in 2025, while cargo and freighters are projected to grow at a 12.5% CAGR through 2031.

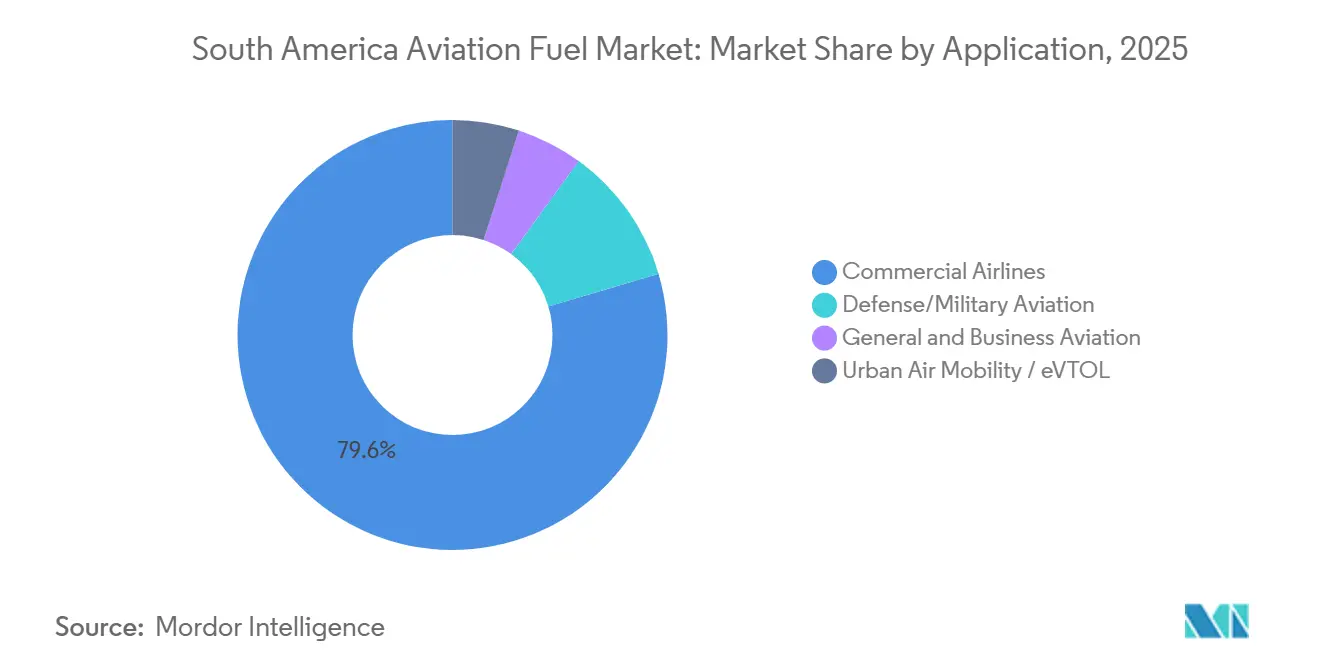

- By application, commercial airlines represented 79.6% of demand in 2025, while defense and military aviation is expected to grow at an 11.7% CAGR through 2031.

- By geography, Brazil held 42.9% of regional demand in 2025 and is also the fastest-growing national market with a 9.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Aviation Fuel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovering air passenger traffic post-pandemic | +2.50% | Regional, strongest in Brazil, Colombia, and Chile | Medium term (2-4 years) |

| Expanding low-cost carriers and route liberalization | +1.80% | Brazil, Colombia, Argentina, Chile, and Peru | Medium term (2-4 years) |

| Rising disposable income and middle-class growth | +1.20% | Regional, with the highest uplift in Brazil and Colombia | Long term (≥ 4 years) |

| Airport infrastructure modernization programs | +1.00% | Brazil, Peru, Chile, and Colombia | Medium term (2-4 years) |

| eVTOL and regional air-taxi projects boosting Jet-A1 demand | +0.50% | Brazil, with early spillover to Argentina and Chile | Long term (≥ 4 years) |

| Green-corridor commitments accelerating SAF uptake | +1.80% | Brazil, Colombia, Chile, and Uruguay | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recovering Air Passenger Traffic Fuels Jet-A1 Demand

South America’s airline sector has moved beyond a simple rebound and into a broader expansion phase that is now giving the South America aviation fuel market a firmer demand base. Latin America and Caribbean airlines recorded 8.6% year-on-year RPK growth in Q1 2026, and Brazil’s domestic market grew 11.4% in the same period, which shows that traffic growth is still running ahead of many earlier expectations. Load factors have also stayed high, with the regional market reaching 85.9% in November 2025, which points to tight capacity and stronger aircraft utilization rather than a short-lived spike in bookings. When airlines keep aircraft in the air longer and fill more seats, fuel demand rises in a direct and predictable way across trunk routes, connecting routes, and airport turnarounds. This is why the South America aviation fuel market is benefiting not only from more passengers, but also from a more intensive use of available fleets and airport slots.

Expanding Low-Cost Carriers and Route Liberalization Widen the Fuel Market

Low-cost carrier growth is widening the South America aviation fuel market by pushing service beyond the main capital-city corridors and into secondary airports that need regular fuel supply. Argentina’s liberalization push helped lift seat capacity by 8.5% in Q1 2026, which shows how policy change can quickly translate into more aircraft activity and more frequent departures. (1)International Air Transport Association, “Air Passenger Market Analysis March 2026,” IATA, iata.org This matters because each new route does more than add passengers; it creates a repeat fuel-demand point that needs storage, delivery coordination, and supplier reliability. The effect is especially visible in domestic and short-haul flying, where single-aisle fleets run high daily utilization and turn fuel into one of the most immediate operating variables. As liberalization spreads, the South America aviation fuel market should see demand broaden geographically rather than remain tied only to the largest hubs.

Green-Corridor Commitments Accelerating SAF Uptake

Green-corridor planning is turning SAF from a pilot concept into a real supply and compliance issue for the South America aviation fuel market. Brazil’s ANAC and ANP launched the Conexão SAF forum in 2024, which gave the market a formal technical platform for coordination across regulation, certification, and supply-chain development. Petrobras then made the first domestically produced SAF delivery in Brazil in December 2025, which established a commercial reference point for local production and airport distribution. In February 2026, Petrobras selected Topsoe’s HydroFlex technology for the Boaventura Energy Complex, a project designed to process 1 million tonnes of feedstock annually and strengthen future regional supply depth. Colombia’s SAF roadmap and government-backed coordination with Ecopetrol show that this movement is no longer limited to one country, which broadens the long-term demand path for the South America aviation fuel market.

Airport Infrastructure Modernization Programs Drive Long-Term Fuel Infrastructure Demand

Airport expansion programs are raising the physical operating ceiling of the South America aviation fuel market because passenger terminals, aprons, and refueling systems need to grow together. In Brazil, Aena secured BRL 5.7 billion, or USD 1.04 billion, in financing from BNDES to modernize 11 airports, including Congonhas, which supports higher aircraft throughput and more reliable airport-side fuel operations. In Peru, Fraport opened the new terminal at Jorge Chávez International Airport in May 2025 after a USD 2 billion expansion that lifted annual capacity to 40 million passengers, strengthening Lima’s role as a regional hub. These projects matter because they support more movements, denser scheduling, and better fuel handling discipline at airports that already anchor regional connectivity. Over time, these upgrades should help the South America aviation fuel market grow with fewer operational bottlenecks at the airport level.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited regional SAF production capacity | -0.80% | Regional, most acute in Argentina, Peru, and Chile | Medium term (2-4 years) |

| Currency volatility increasing fuel-price risk | -0.50% | Argentina, Brazil, and Colombia | Short term (≤ 2 years) |

| Fossil-fuel dominated energy mix and policy inertia | -0.40% | Regional, strongest drag in Venezuela, Bolivia, and Peru | Long term (≥ 4 years) |

| Fuel-pipeline bottlenecks to remote airports | -0.30% | Brazil Amazon basin, Peru, and Bolivia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Regional SAF Production Capacity Creates Near-Term Supply Risk

The South America aviation fuel market is moving into mandated SAF consumption before the region has built a wide enough production base to supply it comfortably. Petrobras has established the first domestic delivery benchmark in Brazil, but the regional supply chain is still early and remains concentrated in a small number of projects and planned capacity additions. This creates a narrow supply window in which early compliance can depend on a small producer set, limited co-processing volumes, and gradual refinery adaptation rather than deep market liquidity. The MIT, LATAM, and Airbus work on Latin American decarbonization also points to the value of book-and-claim structures, because smaller national markets will struggle if they must wait for full local physical supply before participating in SAF procurement. Until production spreads beyond a few anchor projects, the South America aviation fuel market will face a supply-side constraint that can slow adoption even where regulation is already clear.

Currency Volatility Increasing Fuel-Price Risk for Operators

The South America aviation fuel market also carries a structural pricing risk because jet fuel is linked to USD while a large share of airline revenue is earned in local currency. IATA’s Q1 2026 chartbook showed Brazil with a 14.5% Selic rate and 4.1% inflation, which kept financial conditions tight and currency risk highly visible for operators in the region. (2)International Air Transport Association, “Quarterly Air Transport Chartbook Q1 2026,” IATA, iata.org When local currencies weaken, airlines feel the full pressure in fuel bills even if the underlying oil market has not changed much. This burden is often harder on smaller carriers and regional operators because they have less flexibility in hedging, less pricing power, and fewer ways to spread costs across a broad network. The result is that the South America aviation fuel market can still grow in volume while airline margins remain exposed to short-term exchange-rate swings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Dominant Base, Transformative Upside

Conventional jet fuel accounted for 92.3% of South America aviation fuel market size in 2025, which shows that the region still runs on a deeply established fossil-fuel base. This dominance is tied to the installed reality of the market, because airport fuel systems, distribution assets, and most refinery output are already aligned with Jet A-1 and related aviation kerosene specifications. The segment should therefore remain the main source of supply over the near term, even as regulation starts to reshape procurement behavior around lower-carbon alternatives. Avgas remains a small but durable niche because general aviation, agricultural flying, and interior connectivity still depend on aircraft types that do not move with the same fuel profile as the main airline fleet.

SAF is the fastest-growing fuel type, with South America aviation fuel market size for this segment projected to expand at a 28.6% CAGR from 2026 to 2031. The growth rate looks high because the starting base is still small, but the underlying shift is real as Brazil’s policy framework and CORSIA compliance pressures begin to turn SAF into a planning requirement rather than a symbolic purchase. Petrobras strengthened that path with its first domestic SAF delivery in December 2025, proving that certified local supply can move from refinery output into airport distribution. The Boaventura project and Raízen’s certification pathway also show that the South America aviation fuel industry is building around feedstock access, co-processing, and ethanol-based routes rather than waiting for a single technology outcome.

By Aircraft Type: Narrow-body Leads, E-commerce Fuels Cargo Growth

Narrow-body aircraft held 58.7% of South America aviation fuel market share by aircraft type in 2025, reflecting the region’s heavy reliance on short-haul and medium-haul domestic flying. That structure is logical because many of the busiest routes in Brazil, Colombia, Chile, and Peru are designed around high-frequency single-aisle operations rather than long-haul wide-body deployment. It also makes fuel demand more stable, since narrow-body fleets tend to post repeat utilization patterns, dense daily schedules, and predictable turnaround needs at the largest airports. Even where international connectivity is improving, the core operating rhythm of the South America aviation fuel market still rests on narrow-body traffic.

Cargo and freighters are the fastest-growing aircraft category, with the South America aviation fuel market size for this segment forecast to rise at a 12.5% CAGR through 2031. The segment is growing from a smaller base, but it is benefiting from stronger cargo relevance in regional trade flows, time-sensitive freight, and e-commerce-linked distribution networks. This adds a separate fuel-demand layer because dedicated cargo fleets do not map neatly to passenger traffic cycles and can keep flying even when airline schedules shift. As a result, the South America aviation fuel market is gaining a more diversified aircraft-demand profile, where cargo growth increasingly supports fuel volumes alongside passenger aviation.

By Application: Commercial Lead Intact, Urban Mobility Reshapes Long-Term Demand

Commercial airlines consumed 79.6% of market volume in 2025, which confirms that scheduled passenger transport remains the main application base of the South America aviation fuel market. This segment benefits from broad domestic demand, the continued rebuilding of international links, and the central role of air travel in a region where geography often limits practical surface alternatives. General and business aviation adds a resilient layer because private flying, charter activity, and corporate mobility continue to matter in markets tied to agribusiness, mining, energy, and long-distance executive travel. Together, these uses keep conventional aviation fuel demand broad even before SAF blending becomes material.

Defense and military aviation is the fastest-growing application segment, with an 11.7% CAGR projected from 2026 to 2031. The main reason is that military fleet modernization across parts of the Southern Cone is lifting fuel needs per mission and increasing the operational intensity of newer platforms. Urban air mobility is still negligible in direct fuel use, but the surrounding support ecosystem matters because Brazil is already moving toward commercial eVTOL certification and related infrastructure development. As test activity, certification work, and supporting airport infrastructure expand, the South America aviation fuel market will see indirect demand benefits through maintenance movements, crew positioning, and secondary-airport support activity.

Geography Analysis

Brazil held 42.9% of the South America aviation fuel market share in 2025 and is projected to grow at a 9.3% CAGR through 2031. The country leads because its geography makes air transport essential, its domestic network is the largest in the region, and its biofuel base gives it the strongest starting point for SAF supply development. Brazil also has the clearest regulatory setup, with the Future Fuel Law and the Conexão SAF framework creating more certainty for refiners, airlines, and airport fuel operators than any other market in the region. Petrobras reinforced that lead with the first commercial delivery of domestically produced SAF in December 2025, which gives Brazil an early operational advantage in both conventional supply depth and renewable fuel readiness.

Argentina and Colombia form the next tier, but they are moving through different demand patterns and policy conditions. Argentina gained support from air transport liberalization, with seat capacity rising 8.5% in Q1 2026, which helps demand even though currency pressure and fuel logistics still limit the speed of expansion. Colombia is becoming more important because it already has a formal SAF roadmap under Resolution 090/2025, which gives the country a clearer pathway for long-term fuel diversification. The cooperation between Aeronáutica Civil and Ecopetrol also gives Colombia a practical base for early SAF execution rather than a purely conceptual policy stance.

Chile and Peru are the most infrastructure-led growth stories in the western corridor of the region. Peru stands out because the new Lima terminal has already lifted the operational scale of the country’s main hub, which supports more movements and improves the fuel handling environment for future growth. Peru also has a meaningful long-term SAF resource base, but commercialization still needs stronger policy support, logistics coordination, and clearer investment execution. Chile is moving more gradually, with a credible long-range path for cleaner aviation fuels but a near-term market that remains centered on conventional jet fuel demand. Across the rest of South America, smaller national markets continue to depend mainly on conventional supply and are likely to adopt SAF more slowly because scale, infrastructure, and local production are less developed than in Brazil and Colombia.

Competitive Landscape

The South America aviation fuel market is moderately fragmented, although Petrobras holds a stronger structural position than any other supplier because it combines refining, logistics, and early certified SAF capability in Brazil. Its lead matters because Brazil is the region’s largest fuel market, and a company that can produce, certify, and distribute from within that national system starts with a clear operating advantage. Petrobras demonstrated that advantage in December 2025 when it delivered the first domestically produced SAF in Brazil through the REDUC refinery chain. It extended that position again in February 2026 by selecting Topsoe’s HydroFlex technology for the Boaventura project, which shows how incumbents are scaling by adapting existing industrial systems rather than waiting for entirely new infrastructure.

Shell through Raízen, along with BP and TotalEnergies, remains relevant where airport access, distribution reach, and supply agreements matter more than refinery ownership alone. Raízen is especially well placed because it already holds ISCC CORSIA Plus certification for ethanol-based SAF pathways, giving it a credible bridge between Brazil’s sugarcane base and future airline procurement needs. That means competition is not only about today’s jet fuel volumes, but also about who controls certification, feedstock conversion routes, and the ability to serve future SAF demand with compliant product. This split keeps the South America aviation fuel market active on both fronts, with conventional distribution still decisive today and renewable positioning becoming more important each year.

The clearest white space remains at secondary airports and thinner logistics corridors, where storage, trucking, and delivery reliability are weaker than at the largest hubs. ANP’s review of aviation fuel distribution rules is important because it could open the door to new logistics models and some degree of airline self-supply, which would create room for additional participants in Brazil’s fuel chain. Book-and-claim structures add another route into the market because emerging SAF suppliers can sell environmental attributes without matching every airport delivery point physically, which is useful in a region with uneven infrastructure. Even with Petrobras in a leading role, no company controls the entire regional chain across all countries, airports, and fuel types. That is why the South America aviation fuel market still behaves as a contested field rather than a closed one, especially as regulation, airport upgrades, and SAF qualification standards continue to evolve.

South America Aviation Fuel Industry Leaders

Repsol SA

BP PLC

Shell PLC

Pan American Energy SL

Petroleo Brasileiro SA (Petrobras)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Eve Air Mobility demonstrates full-scale eVTOL prototype for Brazilian government, targeting 2027 certification: Eve Air Mobility flew its engineering prototype before President Lula and ANAC leadership at Embraer's Gavião Peixoto facility, completing 35 flights since December 2025. BNDES has provided more than BRL 1.4 billion (approximately USD 246 million) in financing since 2022. Brazil's National Urban Air Mobility Policy is under active public consultation, positioning the country as the first market for commercial eVTOL service.

- February 2026: Petrobras selects Topsoe for Boaventura SAF and renewable diesel complex: Petrobras appointed Topsoe as technology provider (HydroFlex® technology) for the Boaventura Energy Complex in Itaboraí, Rio de Janeiro, designed to process 1 million tonnes of feedstock annually from vegetable oils, animal fats, and waste. Subject to FID, it would become one of Brazil's largest dedicated SAF production facilities.

- December 2025: Petrobras delivers first domestically produced SAF in Brazil; REDUC becomes Latin America's first CORSIA-certified SAF refinery: 3,000 m³ of ISCC-CORSIA-certified SAF delivered to distributors at Galeão International Airport, produced at the Duque de Caxias refinery using soybean or technical corn oil co-processed with mineral kerosene. CO₂ reduction up to 87% in the renewable fraction.

South America Aviation Fuel Market Report Scope

Aviation fuels are specialized liquid substances specifically designed for use in aircraft propulsion systems. These fuels are crucial for powering various types of aircraft, from commercial airliners to military jets. The primary function of aviation fuels is to provide the necessary energy to support combustion within aircraft engines, generating thrust for propulsion.

The South America Aviation Fuel Market is segmented into fuel type, aircraft type, application, and geography. By fuel type, the market is segmented into Conventional Jet Fuel, SAF, and Avgas. By aircraft type, the market is segmented into Narrow-body, Wide-body, Regional Jets and Turboprops, and Cargo/Freighters. By application, the market is segmented into Commercial Airlines, Defense/Military, General Aviation, and Urban Air Mobility/eVTOL. The report also covers the market size and forecasts for aviation fuel in 5 countries across South America. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Fuel Type

| Conventional Jet Fuel |

| Sustainable Aviation Fuel (SAF) |

| Avgas |

By Aircraft Type

| Narrow-body |

| Wide-body |

| Regional Jets and Turboprops |

| Cargo/Freighters |

By Application

| Commercial Airlines |

| Defense/Military Aviation |

| General and Business Aviation |

| Urban Air Mobility / eVTOL |

By Geography

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Fuel Type | Conventional Jet Fuel |

| Sustainable Aviation Fuel (SAF) | |

| Avgas | |

| By Aircraft Type | Narrow-body |

| Wide-body | |

| Regional Jets and Turboprops | |

| Cargo/Freighters | |

| By Application | Commercial Airlines |

| Defense/Military Aviation | |

| General and Business Aviation | |

| Urban Air Mobility / eVTOL | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the 2031 outlook for aviation fuel demand in South America?

The South America aviation fuel market is forecast to reach USD 20.09 billion by 2031 from USD 13.30 billion in 2026, which implies an 8.6% CAGR over 2026 to 2031 and reflects both traffic growth and tighter SAF compliance needs.

Why is Brazil the most important country in this space?

Brazil held 42.9% of regional demand in 2025 and is projected to grow at a 9.3% CAGR, supported by its large domestic aviation base, stronger regulation, and the region’s most advanced SAF production moves.

Which fuel segment is expanding the fastest?

SAF is the fastest-growing fuel type with a projected 28.6% CAGR through 2031, even though conventional jet fuel still held 92.3% of total demand in 2025.

Which aircraft category drives the largest fuel demand?

Narrow-body aircraft led with 58.7% of demand in 2025 because the region’s route structure is still centered on short-haul and medium-haul domestic flying.

What is the main near-term challenge for suppliers and airlines?

The key challenge is that SAF demand is rising faster than regional production depth, while USD-linked fuel pricing and local currency volatility keep airline fuel costs under pressure.

How are airport projects affecting fuel demand across the region?

Airport modernization in Brazil and Peru is raising terminal capacity, improving aircraft handling, and strengthening the storage and delivery base that supports both conventional jet fuel and future SAF distribution.

Page last updated on: