Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

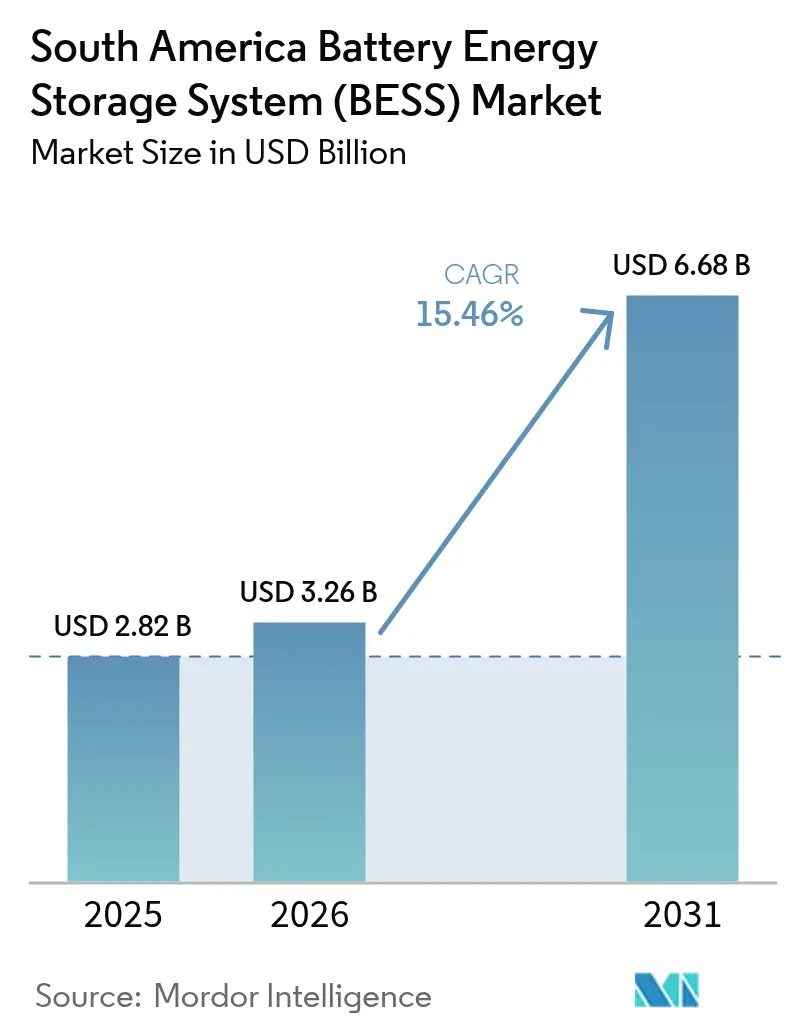

| Base Year Market Size (2025) | USD 2.82 Billion |

| Market Size (2026) | USD 3.26 Billion |

| Market Size (2031) | USD 6.68 Billion |

| Growth Rate (2026 - 2031) | 15.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Battery Energy Storage System (BESS) Market Analysis by Mordor Intelligence

South America Battery Energy Storage System Market size in 2026 is estimated at USD 3.26 billion, growing from 2025 value of USD 2.82 billion with 2031 projections showing USD 6.68 billion, growing at 15.46% CAGR over 2026-2031.

Momentum stems from rising variable-renewable penetration, supportive auction programs in Brazil and Chile, and the region’s shift toward multi-hour firming solutions. Flow-battery pilots, sodium-ion demonstrations, and localized lithium-ion pack assembly illustrate chemical diversification tactics that hedge against critical-mineral volatility. Utility procurement dominates capacity additions, yet microgrids in the mining sector and residential solar-plus-storage bundles are expanding rapidly. Software-centric value capture is accelerating as virtual power plant (VPP) aggregation extracts revenue streams from frequency regulation. Supply-chain localization under Brazil’s 2024 green-industry law is attracting Chinese manufacturers, while fire-safety codes push UL 9540A-certified enclosures into urban substations.[1]Camila Hodgson, “Battery Costs Fall Sharply, Boosting Storage Economics,” ft.com

Key Report Takeaways

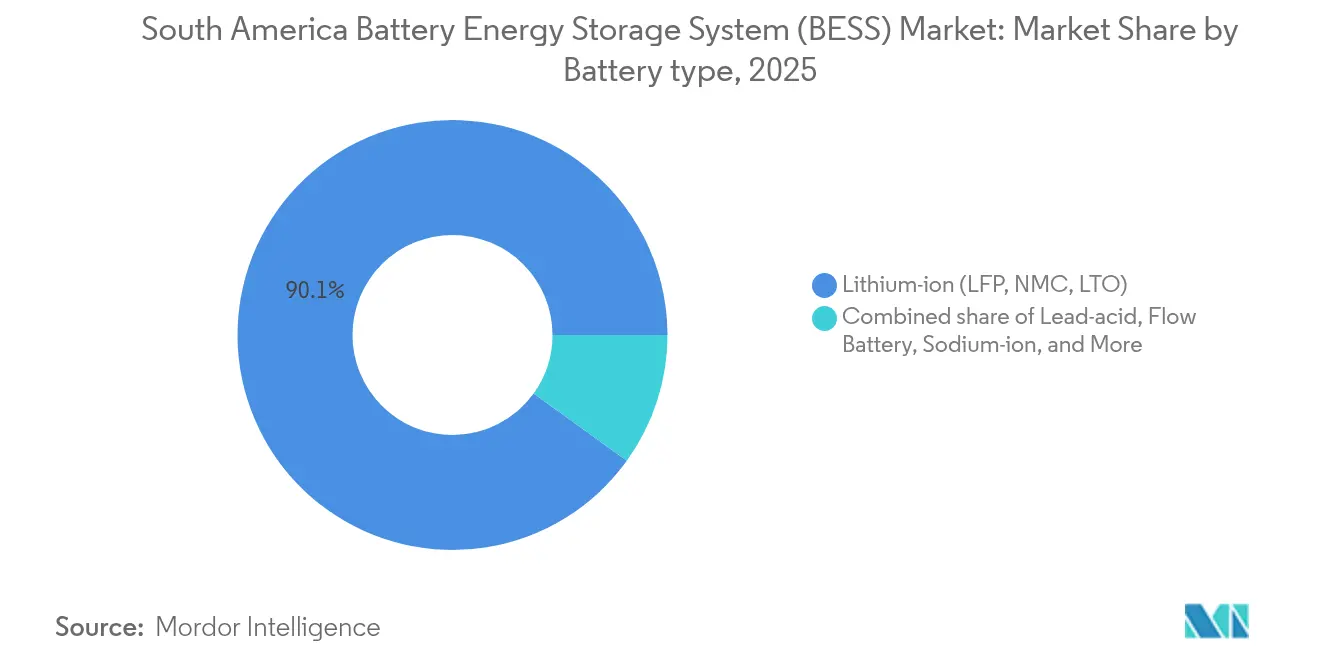

- By battery type, lithium-ion batteries held 90.05% of the South American battery energy storage system market share in 2025, while flow batteries are forecast to grow at a 24.6% CAGR through 2031.

- By connection type, on-grid systems accounted for 79.85% of installations in 2025, whereas off-grid microgrids are projected to expand at a 25.1% CAGR through 2031.

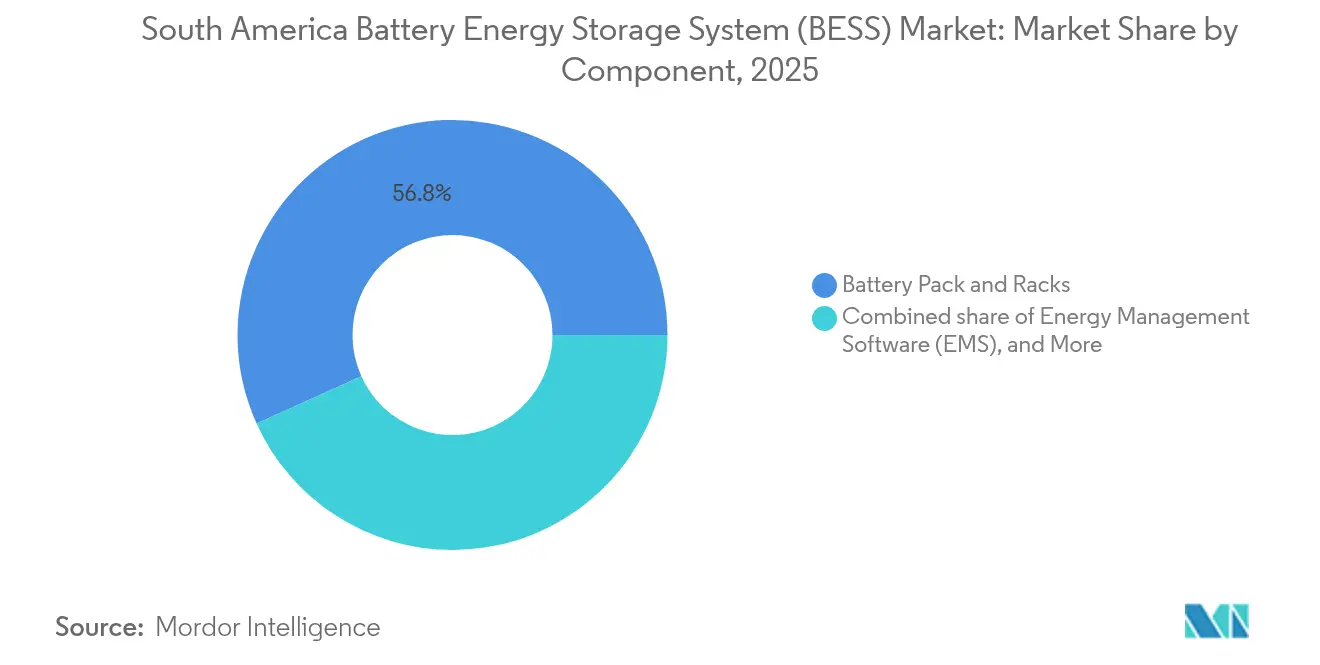

- By component, battery packs and racks captured 56.75% of the 2025 revenue, while energy-management software is expected to advance at a 26% CAGR through 2031.

- By energy-capacity range, 10–100 MWh projects represented 42.15% of 2025 capacity, but systems above 500 MWh are scaling at a 26.9% CAGR through 2031.

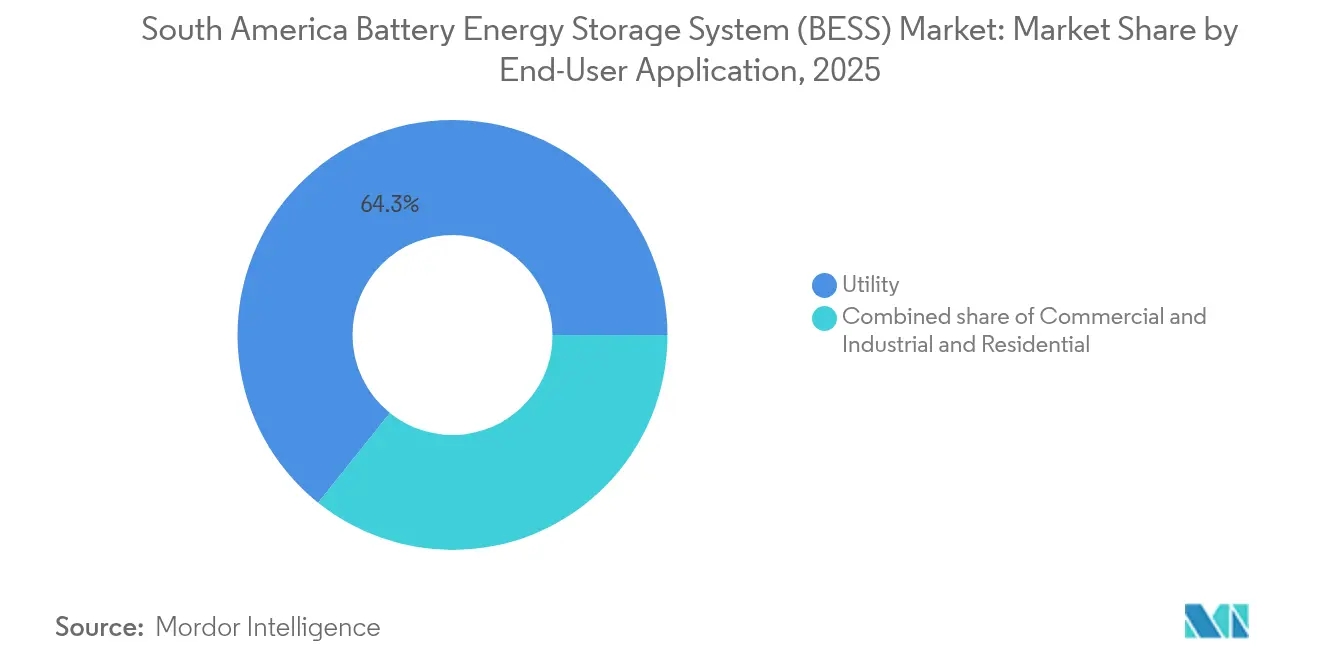

- By end-user, utility buyers accounted for 64.25% of 2025 demand, while commercial and industrial installations are projected to have a 26.7% CAGR to 2031.

- By geography, Brazil held a 37.05% share of the South America battery energy storage system market in 2025; Chile is projected to expand at a 25.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Battery Energy Storage System (BESS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging variable-renewable penetration | +4.2% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Rapid decline in lithium-ion USD/kWh | +3.8% | Brazil, Chile | Short term (≤ 2 years) |

| Utility procurement via 2025 storage auctions | +3.1% | Brazil, Chile | Short term (≤ 2 years) |

| Mining-sector corporate PPAs and microgrids | +2.6% | Chile, Peru, Argentina | Medium term (2-4 years) |

| Brazil’s 2024 green-industry tax incentives | +1.4% | Brazil | Long term (≥ 4 years) |

| Energy-as-a-service & VPP models | +1.2% | Brazil, Chile | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Variable-Renewable Penetration Across Brazil & Chile

Brazil added 8.8 GW of solar and wind energy in 2024, increasing variable renewables to 23% of the grid's supply. Chile's Atacama Desert hosts 4.2 GW of solar that faces midday curtailment, creating lucrative evening-peak arbitrage windows for 4-hour lithium-ion systems. The Chilean grid operator requires solar plants exceeding 100 MW to co-locate storage or face curtailment penalties.[2]Reuters Energy Desk, “Chile Tightens Co-Location Rules for Solar,” reuters.com Brazil's system operator pilots synthetic-inertia services from batteries to replace retiring thermal plants. Argentina's Patagonia wind corridor experiences similar curtailment yet lacks capacity payments, resulting in storage investment remaining off-grid for mines.

Rapid Decline in Lithium-Ion (LFP & NMC) Battery USD/kWh

LFP cell prices declined to USD 115/kWh in 2024, representing a 17% year-over-year decrease, which drove levelized storage costs below USD 150/MWh for 4-hour systems. NMC chemistries fell to USD 128 / kWh, narrowing the cost gap and enabling hybrid stacks that combine LFP bulk capacity with NMC power bursts. Brazil’s 2025 auction caps bids at USD 180 / kWh, a threshold only LFP suppliers can meet profitably. South Korean firms are redirecting NMC output to South American EV plants, creating a secondary supply for stationary integrators. Projections indicate 6-hour systems will match 4-hour costs by 2027, opening seasonal-firming applications.

Emerging Utility Procurement of Ancillary-Service BESS Through 2025 Storage Auctions

Brazil’s 2024 auction awarded 2 GW of storage on 15-year availability payments, with average bids at USD 172 / kWh. Chile’s 13 GWh land-allocation process reserves sites for co-located storage that must provide ramping services. Guaranteed index-linked payments cut project-finance risk and attract pension funds. Argentina has draft rules but lacks final remuneration, keeping developers sidelined. The auction model recasts storage as regulated infrastructure rather than merchant assets.

Corporate PPAs & Micro-Grid Demand From Mining Sector in Andean Region

Codelco contracted 180 MW of solar-plus-storage in 2024, offsetting 320,000 t of CO₂ annually. Peru’s Las Bambas mine deployed a 25 MWh hybrid microgrid that cut diesel costs by 40%. Argentina’s lithium triangle hosts 68 MWh of off-grid storage for brine-evaporation pumps. Mining PPAs bypass utilities, locking electricity below USD 50 / MWh for 20 years. Oversized 8–12-hour batteries deliver autonomy valued over intra-day arbitrage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex & limited project-finance depth | -2.80% | Argentina, Colombia, Peru | Medium term (2-4 years) |

| Regulatory gaps outside Chile & Brazil | -1.90% | Argentina, Colombia, Peru, Uruguay | Short term (≤ 2 years) |

| Supply-chain dependence & mineral volatility | -1.30% | Paraguay, Bolivia | Medium term (2-4 years) |

| Fire-safety and permitting delays | -0.90% | Brazil, Chile, Argentina | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex & Limited Project-Finance Depth

Utility-scale systems cost USD 300–400 / kWh, implying USD 120 million for 300 MWh plants. Argentina’s 1,500-basis-point risk premium blocks international lenders absent guarantees. Colombia’s development bank issued USD 85 million in concessional loans in 2024, meeting a threefold demand. Peru’s miners fund projects on a balance-sheet basis, narrowing participation to investment-grade firms. Brazil’s BNDES limits loans to 70% of capex, forcing higher equity shares.[3] Financial Times Climate Desk, “Financing Gap Hampers LatAm Batteries,” ft.com

Regulatory Gaps / Uncertain Remuneration Outside Chile & Brazil

Argentina lacks frequency-regulation payments, relegating batteries to merchant arbitrage. Colombia’s draft storage rules await grid-code revisions, delaying revenue certainty. Peru permits storage only within hybrid renewable energy projects, barring standalone bids. Uruguay allows day-ahead bids but excludes regulated returns. Protracted interconnection timelines of 18–24 months deter investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Flow-Battery Momentum Challenges LFP Supremacy

Flow batteries are set to grow at a 24.6% CAGR through 2031, reflecting rising demand for 8–12-hour discharge durations that lithium-ion cannot match economically. The South America battery energy storage system market size for flow batteries reached USD 0.28 billion in 2025 and is poised for accelerated expansion as grid codes internalize curtailment costs. ESS Inc.’s 75 MWh iron-flow project in Chile exemplifies 12-hour performance without capacity fade.

Lithium-ion retained a 90.05% share owing to LFP’s cost and thermal advantages in hot climates. Sodium-ion pilots in Brazil aim to localize the supply chain. Niche chemistries such as hybrid super-capacitors serve sub-second response markets. Certification under UL 1973 is becoming mandatory, shaping procurement specifications. The South America battery energy storage system market continues to bifurcate between cost-optimized 4-hour lithium-ion stacks and longer-duration flow solutions.

By Connection Type: Off-Grid Microgrids Accelerate

Off-grid microgrids are forecasted to grow at a 25.1% CAGR, driven by decarbonization in the mining sector and electrification in remote communities. Peru’s rural program aims for 500 solar-plus-storage microgrids by 2027. On-grid systems nonetheless dominate 79.85% of 2025 installs, underpinned by utility auctions in Brazil and market-based procurement in Chile. Hybrid configurations that allow islanding during outages blend both models.

The South America battery energy storage system market benefits from avoided transmission build-outs in off-grid sites, while on-grid projects capture multi-revenue stacking. Interconnection queues in Argentina typically stretch 12–18 months, favoring microgrids due to their time-to-market advantage. Net-metering reforms in Brazil permit behind-the-meter hybrid setups, intensifying distributed demand.

By Component: Software Takes Center Stage

Energy-management software is expanding at a 26% CAGR, outpacing hardware as VPP aggregation unlocks frequency-regulation revenue. Battery packs and racks still account for 56.75% of the revenue share, yet margin compression from Chinese supply challenges affects hardware-centric business models. Power-conversion systems compete on incremental efficiency, while balance-of-plant cost shares rise with urban fire-safety mandates.

Superior dispatch algorithms determine returns, positioning Fluence’s Mosaic and Tesla’s Autobidder as critical differentiators. The South America battery energy storage system market size for software-driven offerings is set to climb as regulatory frameworks recognize performance-based remuneration.

By Energy Capacity Range: Gigawatt-Hour Era Emerges

Systems above 500 MWh exhibit the fastest growth rate of 26.9% CAGR. AES Andes’ 560 MWh project in Chile anchors utility interest in multi-hour firming. The 10–100 MWh band remains the core of 42.15% 2025 capacity, offering scalability for C&I buyers. Brazil’s auction caps project size at 400 MWh, distributing opportunity among many developers.

Gigawatt-hour projects enjoy bulk-procurement discounts, while small-scale systems bear 30–40% cost premiums. The South America battery energy storage system market thus splits between distributed self-consumption assets and utility-scale grid-service platforms.

By End-User Application: Mining Sector Spurs C&I Growth

Utility buyers held 64.25 of % demand in 2025, yet C&I installations are rising at a 26.7% CAGR. Mining operations prioritize 8–12 hours of autonomy and have secured green-bond financing at lower spreads. Residential adoption is scaling through subscription-based EaaS models that defray the upfront costs of $8,000–$ 12,000. Demand-charge reduction yields 18–24% IRRs in Brazil’s high-tariff states.

As the South America battery energy storage system market widens beyond utilities, software sophistication becomes essential for multi-revenue optimization, and regulatory incentives for behind-the-meter storage gain prominence.

Geography Analysis

Brazil commanded 37.05% of the South America battery energy storage system market in 2025, thanks to a 2 GW storage auction and distributed-generation policies that reward behind-the-meter storage. REIDI incentives underpin BYD’s 10 GWh LFP plant, tightening local supply chains. High ambient temperatures favor LFP, influencing tender specs. São Paulo and Minas Gerais host 55% of C&I installs due to elevated tariffs.

Chile is the fastest-growing geography, with a 25.6% CAGR to 2031, supported by a 13 GWh land allocation process and hydrogen strategy mandates. Atacama solar curtailment and synthetic-inertia requirements drive multi-hour storage demand. Mining PPAs displace diesel, while Santiago pilots VPP aggregation. These factors drive the growth of the South American battery energy storage system market across both utility and off-grid segments.

Argentina, Colombia, and Peru remain in the early stages. Argentina’s lithium-triangle mines installed 68 MWh of off-grid storage in 2024, yet the absence of ancillary-service remuneration restricts grid-connected projects. Colombia’s concessional-loan program is oversubscribed. Peru subsidizes rural microgrids but forbids standalone storage bids. The remaining nations account for under 5% of capacity due to their small grids and the lack of auctions.

Competitive Landscape

The South America battery energy storage system market is moderately fragmented. Global integrators Fluence, Tesla, and BYD compete with regional developers Atlas Renewable Energy and AES Andes that leverage local financing expertise. Chinese suppliers vertically integrate EPC delivery, underbidding rivals by 15–20%. Knowledge of permitting timelines offers regional players an edge in Argentina and Colombia.

Energy-management software drives differentiation, with Fluence Mosaic and Tesla Autobidder vying for the 27.3% CAGR software segment. ESS Inc. disrupts with 12-hour iron-flow technology. Regulatory requirements for synthetic inertia and UL 1973 certification raise entry barriers and favor incumbents with compliance records. White-space includes residential solar-plus-storage and EV-battery repurposing pilots led by Acumuladores Moura.

Fire-safety mandates elevate the sophistication of balance-of-plant systems, reinforcing demand for certified enclosures. The strategic split lies between cost-leadership vertical integrators and niche developers serving mining microgrids or VPP aggregation. As auctions proliferate, scale and software acumen become decisive.

South America Battery Energy Storage System (BESS) Industry Leaders

Enel S.p.A.

AES Gener S.A.

BYD Co Ltd

Engie SA

LG Energy Solution

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: BYD has started building a USD 620 million LFP cell plant in Bahia, Brazil, with an annual output of 10 GWh by 2027, leveraging REIDI tax breaks.

- January 2025: BYD has begun constructing a USD 620 million LFP cell plant in Bahia, Brazil, with an annual production capacity of 10 GWh by 2027, utilizing REIDI tax incentives.

- October 2024: Chile initiated a 13 GW land-allocation process for co-located storage projects aimed at reducing curtailment.

- September 2024: Enel Green Power inked a 20-year, 180 MW solar-plus-storage PPA with Codelco, aiming to replace diesel at two copper mines. However, the provided snippets don't mention this deal. Meanwhile, Atlas Renewable Energy and Grenergy have secured notable solar-plus-storage PPAs with Codelco.

South America Battery Energy Storage System (BESS) Market Report Scope

Battery energy storage is considered a critical technology in transitioning to a sustainable energy system. Battery energy storage systems store the generated energy and release it as needed by the end-user. They regulate voltage and frequency, reduce peak demand charges, integrate renewable sources, and provide a backup power supply. Batteries are crucial in energy storage systems, accounting for approximately 60% of the system's total cost.

The South American Battery Energy Storage System Market is segmented by battery type, connection type, component, energy capacity, end-user, and geography. By battery type, the market is segmented into lithium-ion, lead-acid, flow battery, sodium-ion, and other technologies. By connection type, the market is segmented into on-grid and off-grid. By component, the market is segmented into battery packs, racks, PCS, EMS, and Balance of Plant. By energy capacity, the market is segmented into below 10 MWh, 10 to 100 MWh, 100 to 500 MWh, and above 500 MWh. By end user, the market is segmented into Utility-scale, commercial and industrial (C&I), and residential. The report also covers the market size and forecasts for the South America Battery Energy Storage System Market across the major countries. The market sizing and forecasts for each segment are based on the revenue (USD Billion).

By Battery Type

| Lithium-ion (Lithium Iron Phosphate (LFP), Nickel-Manganese-Cobalt (NMC), Lithium Titanate (LTO)) |

| Lead-acid |

| Flow Battery (Vanadium Redox, Zinc-Bromine) |

| Sodium-ion |

| Other Battery Technologies (NiCd, Hybrid Super-capacitors) |

By Connection Type

| On-Grid (Utility Interconnected) |

| Off-Grid (Micro-Grid, Hybrid) |

By Component

| Battery Pack and Racks |

| Power Conversion System (PCS) |

| Energy Management Software (EMS) |

| Balance-of-Plant and Services |

By Energy Capacity Range

| Below 10 MWh |

| 10 to 100 MWh |

| 100 to 500 MWh |

| Above 500 MWh |

By End-user Application

| Utility |

| Commercial and Industrial |

| Residential |

By Geography

| Brazil |

| Chile |

| Argentina |

| Colombia |

| Peru |

| Rest of South America |

| By Battery Type | Lithium-ion (Lithium Iron Phosphate (LFP), Nickel-Manganese-Cobalt (NMC), Lithium Titanate (LTO)) |

| Lead-acid | |

| Flow Battery (Vanadium Redox, Zinc-Bromine) | |

| Sodium-ion | |

| Other Battery Technologies (NiCd, Hybrid Super-capacitors) | |

| By Connection Type | On-Grid (Utility Interconnected) |

| Off-Grid (Micro-Grid, Hybrid) | |

| By Component | Battery Pack and Racks |

| Power Conversion System (PCS) | |

| Energy Management Software (EMS) | |

| Balance-of-Plant and Services | |

| By Energy Capacity Range | Below 10 MWh |

| 10 to 100 MWh | |

| 100 to 500 MWh | |

| Above 500 MWh | |

| By End-user Application | Utility |

| Commercial and Industrial | |

| Residential | |

| By Geography | Brazil |

| Chile | |

| Argentina | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the 2026 value of battery energy storage in South America?

The South America battery energy storage system market size stands at USD 3.26 billion in 2026.

Which country leads regional installations?

Brazil held 37.05% of 2025 capacity, supported by a 2 GW storage auction and distributed-generation incentives.

How fast are flow batteries growing?

Flow-battery deployments are projected to expand at a 24.6% CAGR between 2026 and 2031 as utilities seek longer-duration solutions.

Why are mining companies adopting storage?

Hybrid microgrids cut diesel fuel costs up to 40% and help meet scope-2 decarbonization targets.

What role does software play in storage economics?

Energy-management platforms optimize dispatch across energy, ancillary-service, and capacity markets, driving a 26% CAGR in software revenue.

Which regulation most influences storage growth?

Brazil’s REIDI tax incentives and Chile’s co-location mandate collectively underpin a significant share of upcoming utility-scale projects.

Page last updated on: