Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

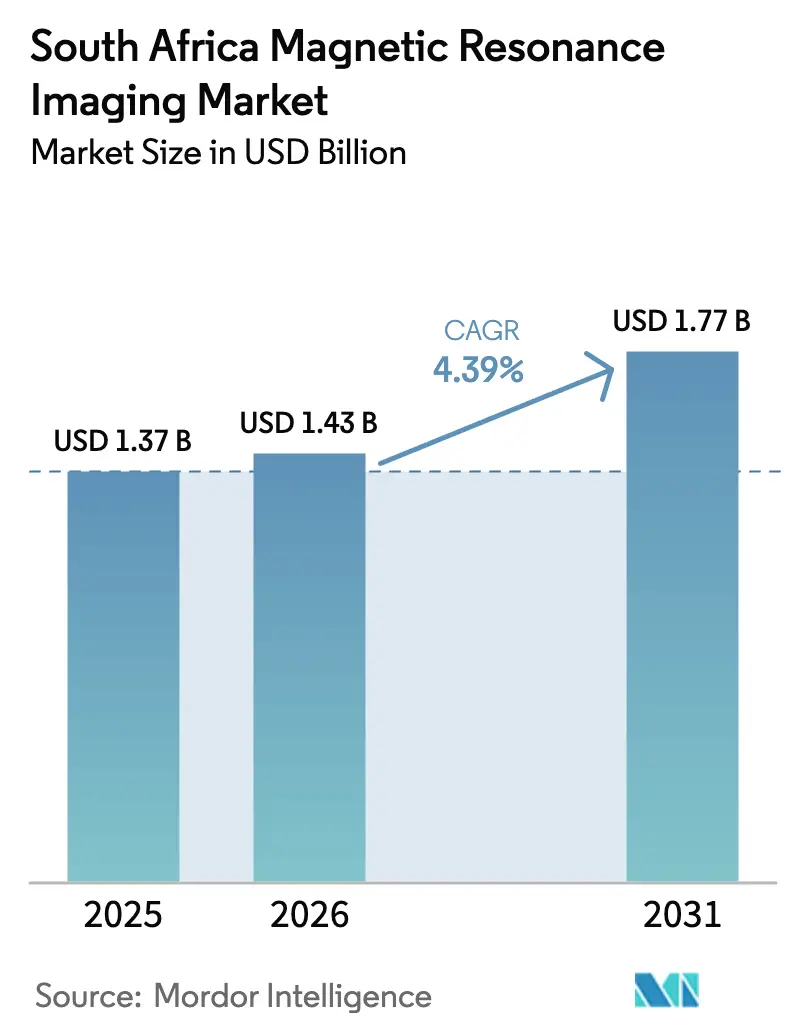

| Base Year Market Size (2025) | USD 1.37 Billion |

| Market Size (2026) | USD 1.43 Billion |

| Market Size (2031) | USD 1.77 Billion |

| Growth Rate (2026 - 2031) | 4.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Magnetic Resonance Imaging Market Analysis by Mordor Intelligence

The South Africa magnetic resonance imaging market size was valued at USD 1.37 billion in 2025 and estimated to grow from USD 1.43 billion in 2026 to reach USD 1.77 billion by 2031, at a CAGR of 4.39% during the forecast period (2026-2031). Rising chronic disease prevalence, expanding private insurance coverage, and government commitment to diagnostic infrastructure combine to lift scan volumes in both urban and peri-urban centers. Technological breakthroughs—helium-free magnets, AI-assisted workflow, and low-field accessibility platforms—are lowering total cost of ownership and broadening use cases, particularly in constrained public facilities. Simultaneously, vendor financing and public-private partnership models are accelerating equipment refresh cycles across provincial health systems. Load-shedding risks and a limited radiologist workforce temper near-term growth yet create a strategic impetus for AI adoption and remote reading networks.

Key Report Takeaways

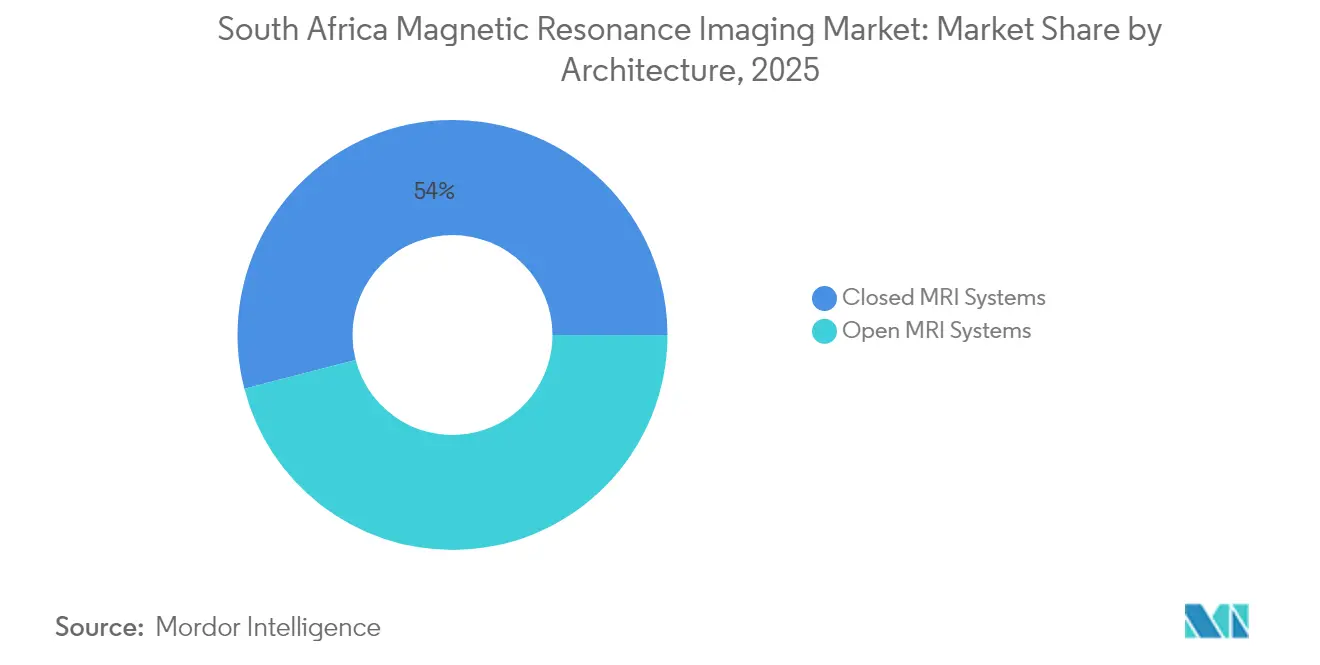

- By architecture, Closed MRI systems led with 54.02% of the South Africa magnetic resonance imaging market share in 2025. Open MRI systems are forecast to expand at a 6.36% CAGR through 2031.

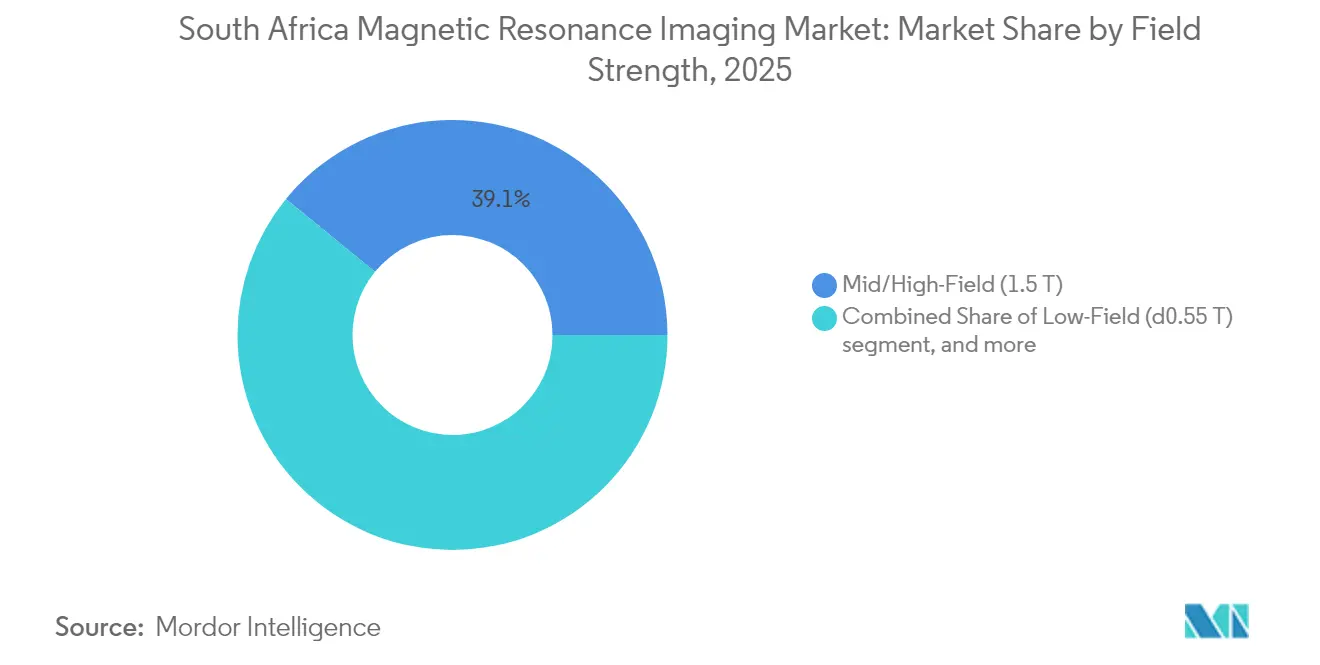

- By field strength, Mid/High-Field 1.5 T commanded 39.10% share of the South Africa magnetic resonance imaging market size in 2025. Low-Field systems (≤0.55 T) are projected to grow at a 5.62% CAGR between 2026-2031.

- By application, Neurology captured 29.02% share of the South Africa magnetic resonance imaging market size in 2025. Cardiology is advancing at a 5.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Magnetic Resonance Imaging Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of chronic diseases | +1.20% | Gauteng, Western Cape, KwaZulu-Natal | Medium term (2-4 years) |

| Technological advancements in MRI hardware and software | +0.80% | Private facilities nationwide | Short term (≤ 2 years) |

| Government imaging-infrastructure investments | +0.70% | Underserved provinces nationwide | Long term (≥ 4 years) |

| Rising private health-insurance coverage | +0.60% | Urban middle-income segments | Medium term (2-4 years) |

| Public-private partnership procurement models | +0.40% | Western Cape, Gauteng | Medium term (2-4 years) |

| Local manufacturing tax incentives | +0.30% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Chronic Diseases

Non-communicable conditions now dominate South Africa’s disease burden, prompting a surge in demand for high-resolution imaging of stroke, cancer, and diabetes complications. Provincial budgets reflect this priority: Gauteng allocated ZAR 61.3 billion, KwaZulu-Natal ZAR 52.1 billion, and Western Cape ZAR 30.2 billion in FY 2022/23, much of which funded diagnostic capacity upgrades[1]TenderAlerts, “Gauteng Health Equipment Status Report 2024,” tenderalerts.co.za. Urban lifestyle shifts accelerate cardiovascular and oncological caseloads, pushing scan volumes in neurology and cardiology. The Department of Health’s Medical Technology Master Plan explicitly tags MRI as essential to tackle this epidemiological transition. Private hospitals mirror this trend, with Life Healthcare reporting 90% growth in Neuraceq doses that rely on MRI-guided protocols.

Growing Technological Advancements in MRI Hardware & Software

Helium-free magnets, AI-embedded consoles, and portable low-field units are reshaping procurement decisions. Philips BlueSeal systems cut helium use from 1,500 L to 0.7 L, easing operating cost anxiety among hospitals faced with erratic supply chains. United Imaging’s October 2024 installation of a 1.5 T scanner at Dr George Mukhari Academic Hospital showcases appetite for new vendors offering competitive pricing[2]OnlineTenders, “Philips BlueSeal Supply Award 2024,” onlinetenders.co.za. AI workflow modules promise shorter exams and preliminary reads, vital in a country with only 700 radiologists nationwide. Despite zero daily AI usage today, 95% of radiologists hold favorable adoption views, indicating pent-up demand once reimbursement and clinical governance align.

Government Imaging-Infrastructure Investments

National Health Insurance roll-out earmarks ZAR 77.8 billion for 197 facility projects over five years, positioning MRI procurement as a universal health coverage cornerstone. Yet execution gaps persist—Gauteng reports four of eight scanners out of service, forcing 607-patient backlogs at Chris Hani Baragwanath Hospital. Corrective actions include comprehensive service clauses in new tenders, such as Western Cape’s 3 T MRI with chiller and injector for Red Cross Children’s Hospital[3]Western Cape Government, “Infrastructure Resilience Audit 2024,” westerncape.gov.za. These purchases elevate imaging equity, especially as the province’s public sector operates just 0.59 scanners per million residents versus OECD norms above three.

Rising Private Health-Insurance Coverage

Medical scheme membership confers immediate MRI access, circumventing nine-month public-queue delays. Insurance growth encourages premium scan protocols and AI add-ons, motivating private groups to expand footprints. Mediclinic’s Diagnostic Imaging arm opened eight facilities within 18 months, capitalizing on insured demand for convenient outpatient imaging. Life Healthcare’s focus on molecular-imaging services, enabled by payer coverage, underscores how insurance catalyzes technology adoption beyond urban hubs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of equipment and maintenance | -1.10% | Rural and public facilities nationwide | Long term (≥ 4 years) |

| Lack of reimbursement and lengthy regulatory approvals | -0.70% | Public procurement nationwide | Medium term (2-4 years) |

| Electricity-supply instability | -0.60% | Load-shedding zones countrywide | Short term (≤ 2 years) |

| Shortage of subspecialty radiologists | -0.50% | Rural provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Equipment & Maintenance

MRI acquisition often requires 30-40% extra capital for shielding, HVAC, and backup power, stretching budgets of provincial hospitals that already run aging fleets. Western Cape’s public network runs only three scanners for six-million residents, showcasing affordability barriers. In Gauteng, half the provincial inventory sits idle due to lapsed maintenance contracts and spare-part shortages. SAHPRA device licensing further adds cost and time, slowing replacements even when funds are available.

Shortage of Subspecialty Radiologists

With about 700 radiologists countrywide, interpretive capacity is the hidden bottleneck. Distribution skews sharply: Western Cape has 19.9 radiologists per 100k population versus Limpopo’s 1.3. Subspecialty depth in cardiac and neuro imaging is thinner still, curbing advanced protocol uptake. Favorable attitudes toward AI—95% positivity—have yet to translate into daily use, signaling opportunity for workflow automation vendors. Private groups are investing in teleradiology platforms to pool scarce expertise across sites, but public-sector roll-out lags behind due to connectivity and credentialing hurdles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Closed Dominance With Open-System Upside

Closed scanners represented USD 0.74 billion of the South Africa magnetic resonance imaging market size in 2025, equating to 54.02% share and anchoring complex neuro-oncology workloads that require high gradient performance. Private tertiary centers lean on closed systems to drive multidisciplinary care pathways, linking MR spectroscopy and functional imaging to surgical planning. Nonetheless, Open MRI systems, smaller at USD 0.63 billion but rising 6.36% CAGR, are carving out niches in pediatrics, bariatric cohorts, and claustrophobic patients.

Open designs also solve floor-loading and room-size constraints in older facilities, easing rural deployment where capital builds are restrictive. Mediclinic selected open magnets for two outpatient clinics launched under its MDI banner, citing shorter install times and patient comfort advantages. As AI guidance removes some image-quality penalties, open platforms are expected to shoulder a growing share of routine musculoskeletal scans, expanding total South Africa magnetic resonance imaging market volume without cannibalizing high-end closed demand.

By Field Strength: Low-Field Renaissance

Mid/High-Field 1.5 T units held 39.10% of the South Africa magnetic resonance imaging market share in 2025, valued at USD 0.54 billion, as they balance image clarity against operating cost. Ultra-High-Field 3 T systems dominate academic neurology and cardiac research but add limited volume. Rapid uptake is instead seen in ≤0.55 T low-field units, expanding 5.62% CAGR, favored by community hospitals seeking lower power draw and less stringent siting requirements in load-shedding-prone districts.

United Imaging’s mid-field installation at Dr George Mukhari Academic Hospital exemplifies a hybrid demand curve—cost-sensitive buyers still insist on 1.5 T fidelity, yet require vendor-bundled service to avoid downtime. Low-field vendors target another segment: mobile imaging fleets deployed through public-private partnerships that rotate scanners among rural clinics. This re-energizes previously stagnant geographic nodes, widening the South Africa magnetic resonance imaging market size without stressing specialist headcount, as basic brain and MSK scans can be batch-read centrally.

By Application: Cardiology Momentum

Neurology retained 29.02% of scans and roughly USD 0.40 billion revenue in the South Africa magnetic resonance imaging market size during 2025 thanks to stroke protocols endorsed by national guidelines. Volume includes epilepsy surgery planning and multiple-sclerosis surveillance. Yet cardiology exams are stretching ahead on growth, adding 5.31% CAGR through 2031 as hypertension and ischemic heart disease rise in younger demographics. AI-based cardiac strain analysis and faster cine sequences shorten exam time, creating throughput gains crucial where scanner slots are scarce.

Oncology scans underpin high-margin contrast usage, while musculoskeletal imaging supports trauma centers and sports medicine practices common in urban private hospitals. Gastrointestinal and hepatobiliary protocols remain niche but benefit from low-field abdominal sequences that tolerate motion artifacts, expanding overall utilization across facility tiers.

Competitive Landscape

Global majors Siemens Healthineers, Philips, and GE Healthcare maintain entrenched relationships with flagship private hospitals, leveraging multiyear service contracts that bundle coil upgrades and software unlocks. Their combined installed base surpasses 60 active units, giving them scale for parts logistics and engineer redeployment. Yet price-sensitive public tenders are increasingly contested by United Imaging and Canon Medical, whose turnkey packages include operator training and three-year service at no extra premium, winning awards such as the Dr George Mukhari installation in October 2024.

Strategic differentiation centers on helium-free cooling, AI post-processing, and remote diagnostics. Philips’s BlueSeal gains mindshare among CFOs fixated on volatile helium import costs, while Siemens’s syngo VirtualCockpit answers the radiologist scarcity dilemma by enabling remote scanner steering. Local distributors add value via B-BBEE compliance and on-site response times under four hours, a critical tender criterion. Market fragmentation persists; the top five vendors collectively hold around 55-60% of active units, leaving meaningful runway for challenger brands that can undercut on price without sacrificing uptime guarantees.

Private hospital groups form the heaviest-weighted buyer bloc. Netcare’s ZAR 1.5 billion capex for FY 2024 earmarks multiple high-field replacements and new sites, reinforcing vendor lock-in yet establishing technology showcases such as AI cardiac workflows at the Kingsway facility. Life Healthcare’s divestiture of Alliance Medical for ZAR 10.2 billion frees balance-sheet capacity to redeploy into domestic imaging, while Mediclinic’s MDI sprint evidences demand for mall-based walk-in centers that decouple scans from inpatient episodes.

South Africa Magnetic Resonance Imaging Industry Leaders

Siemens Healthineers AG

Koninklijke Philips NV

Canon Medical Systems Corporation

GE Healthcare

Esaote SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: United Imaging installed a 1.5 T MRI at Dr George Mukhari Academic Hospital, marking deeper penetration into public procurement.

- November 2024: Netcare Kingsway Hospital commissioned a new MRI facility within the group’s ZAR 1.5 billion FY 2024 capex plan.

- February 2023: At Arab Health 2023, United Imaging announced multiple agreements in the Middle East and Africa, including South Africa, for the uAiFI-powered 1.5T Wide Bore MRI System and PET/MR uPMR 790.

South Africa Magnetic Resonance Imaging Market Report Scope

As per the scope of the report, magnetic resonance imaging is a medical imaging technique used in radiology to produce pictures of the anatomy and the physiological processes of the body. These pictures are further used to diagnose and detect the presence of abnormalities in the body. South Africa Magnetic Resonance Imaging Market is segmented by Architecture (Closed MRI Systems and Open MRI Systems), Field Strength (Low Field MRI Systems, High Field MRI Systems, and Very High Field MRI Systems and Ultra-high MRI Systems), Application (Oncology, Neurology, Cardiology, Gastroenterology, Musculoskeletal, and Other Applications). The report offers the value (in USD) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

By Field Strength

| Low-Field (≤0.55 T) |

| Mid/High-Field (1.5 T) |

| Very-High-Field (3 T) |

| Ultra-High-Field (7 T +) |

By Application

| Neurology |

| Oncology |

| Musculoskeletal |

| Cardiology |

| Gastroenterology |

| Other Applications |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| By Field Strength | Low-Field (≤0.55 T) |

| Mid/High-Field (1.5 T) | |

| Very-High-Field (3 T) | |

| Ultra-High-Field (7 T +) | |

| By Application | Neurology |

| Oncology | |

| Musculoskeletal | |

| Cardiology | |

| Gastroenterology | |

| Other Applications |

Key Questions Answered in the Report

What is the forecast value of the South Africa magnetic resonance imaging market in 2031?

The market is projected to reach USD 1.77 billion by 2031.

Which architecture type is growing fastest in South Africa MRI?

Open MRI systems are expanding at a 6.36% CAGR through 2031.

How large is the radiologist workforce relative to MRI demand?

About 700 radiologists nationwide create interpretive capacity constraints for growing scan volumes.

Which application segment shows the highest growth outlook?

Cardiology leads growth with a 5.31% CAGR expected through 2031.

Why are low-field scanners gaining traction?

They cost less to buy and operate, fit sites with unreliable power, and improve rural access.

What policy program is funding new public-sector MRI capacity?

National Health Insurance allocates ZAR 77.8 billion for 197 facility upgrades over five years.

Page last updated on: