Smart Room Heater Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.74 Billion |

| Market Size (2030) | USD 2.76 Billion |

| Growth Rate (2025 - 2030) | 9.67% CAGR |

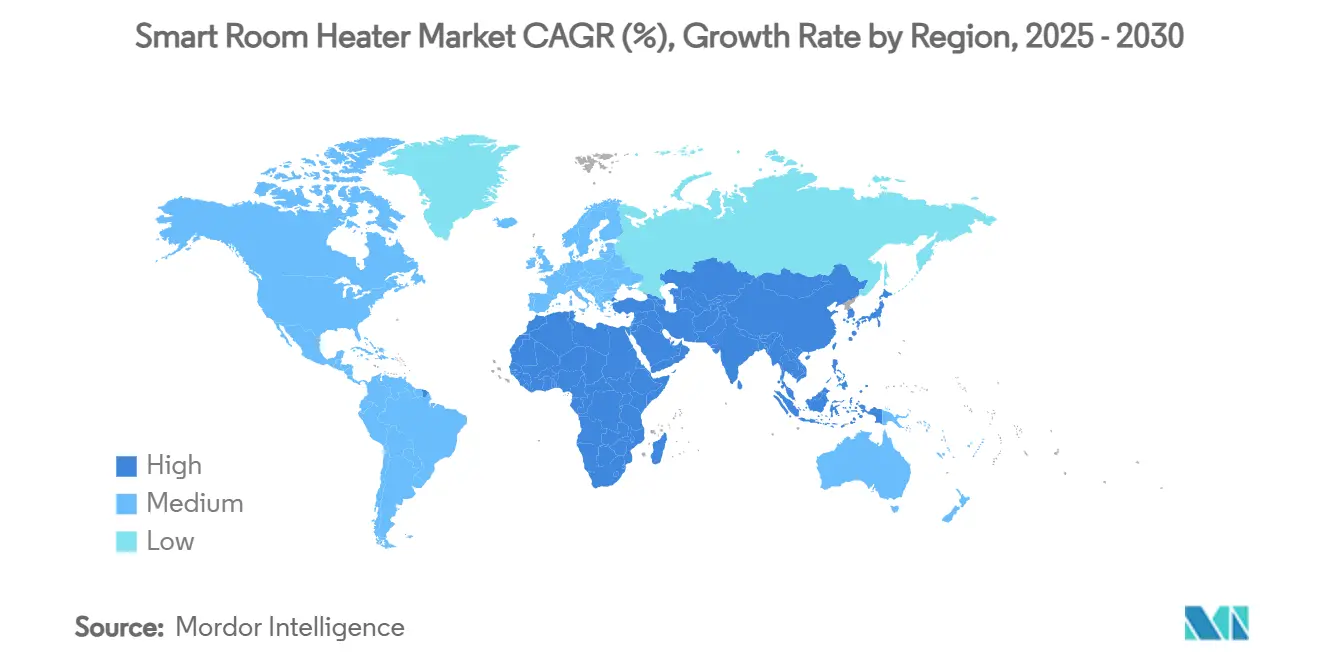

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

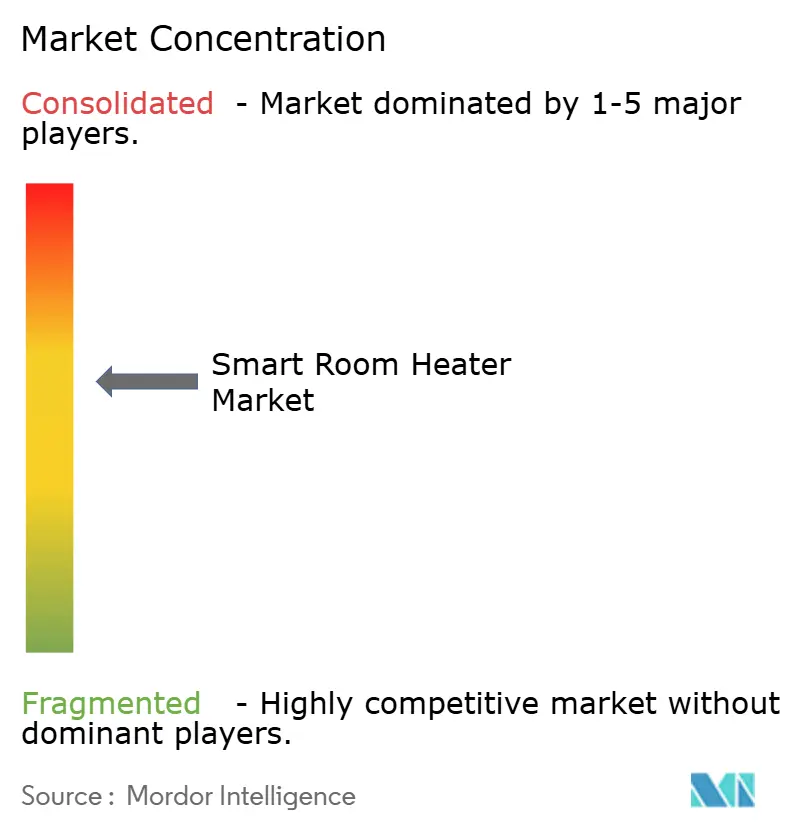

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Room Heater Market Analysis by Mordor Intelligence

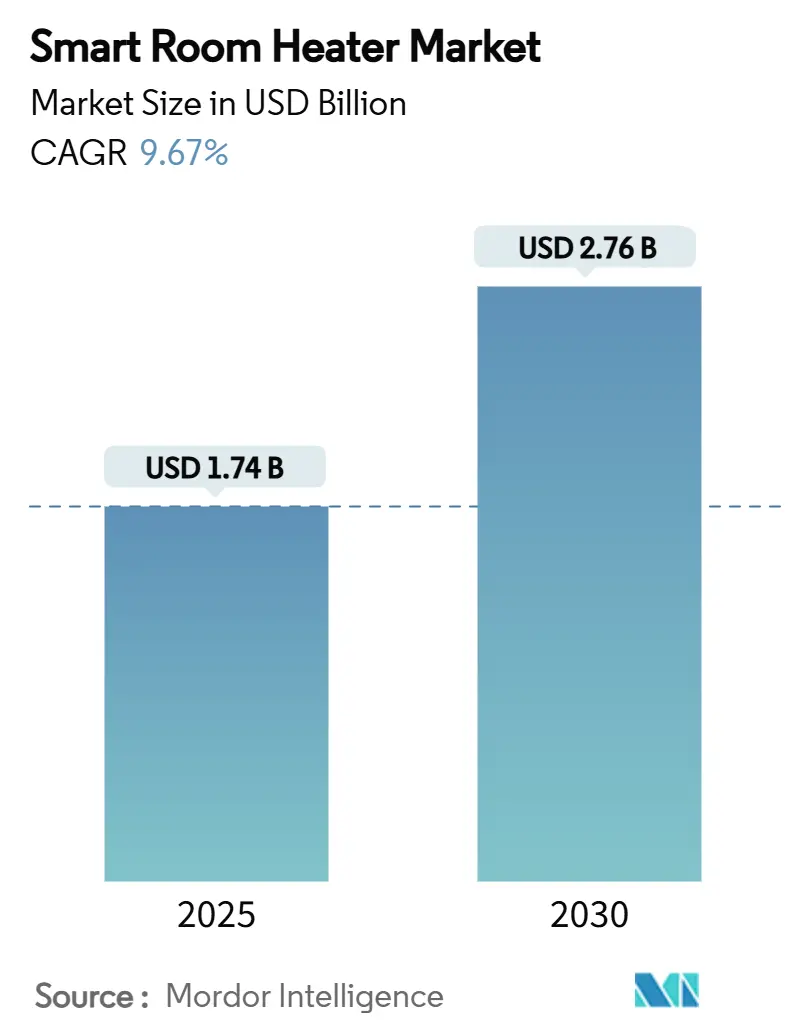

The Smart Room Heater Market size is estimated at USD 1.74 billion in 2025, and is expected to reach USD 2.76 billion by 2030, at a CAGR of 9.67% during the forecast period (2025-2030). Electrification mandates, subsidies for grid‐interactive devices, and falling ceramic PTC component costs underpin the trajectory, while utilities sharpen demand-response tariffs that reward appliances able to preheat during low-price windows. Interoperability gains from the Matter protocol reduce installation friction and encourage multi-vendor ecosystems, which further accelerate replacement cycles among tech-savvy households. Large brands now embed edge AI to fine-tune duty cycles, trimming energy use and extending element life, and cybersecurity upgrades are turning into de facto purchase criteria for public contracts. Competitive intensity is therefore shifting from raw wattage toward holistic value propositions that blend efficiency, connectivity, and data security into a single package.

Key Report Takeaways

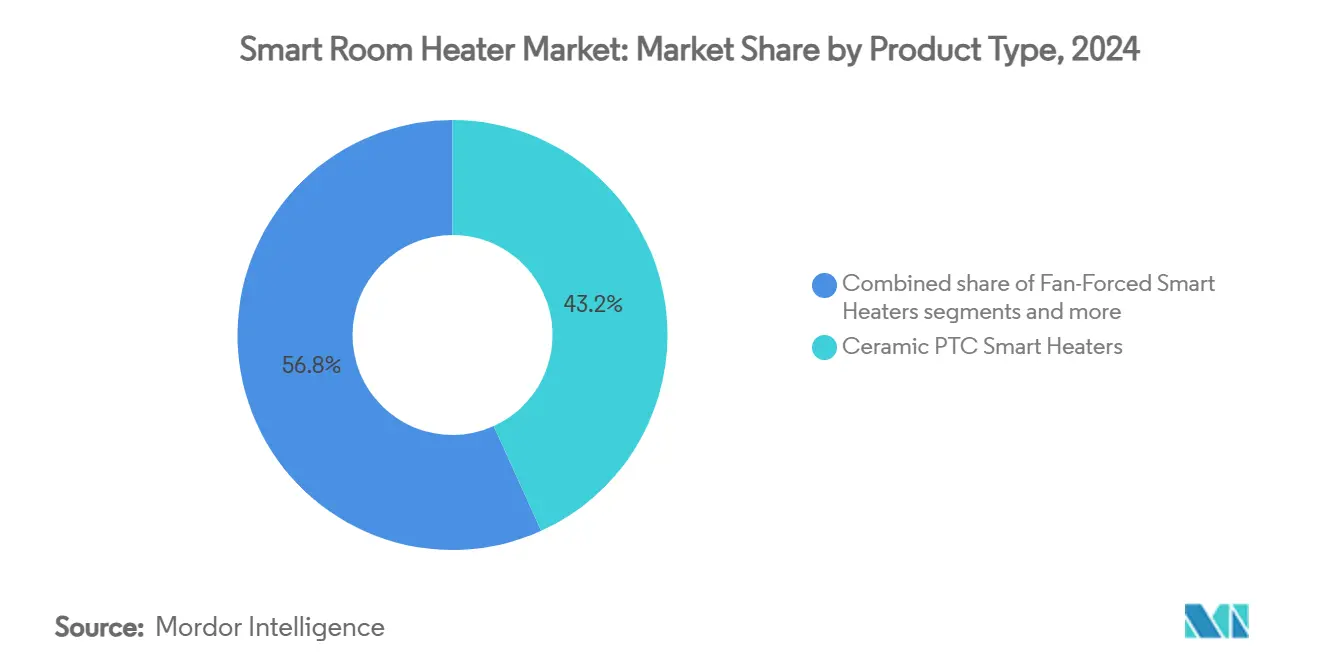

- By product type, ceramic PTC heaters led with a 43.23% smart room heater market share in 2024; infrared and halogen models are projected to expand at an 11.95% CAGR to 2030.

- By connectivity, Wi-Fi captured 64.23% of the smart room heater market in 2024; Matter-enabled devices hold the highest forecast growth at a 10.23% CAGR.

- By power rating, the Less than 1 kW class accounted for 53.12% of the smart room heater market size in 2024; the 1–2 kW class is set to rise at an 11.92% CAGR through 2030.

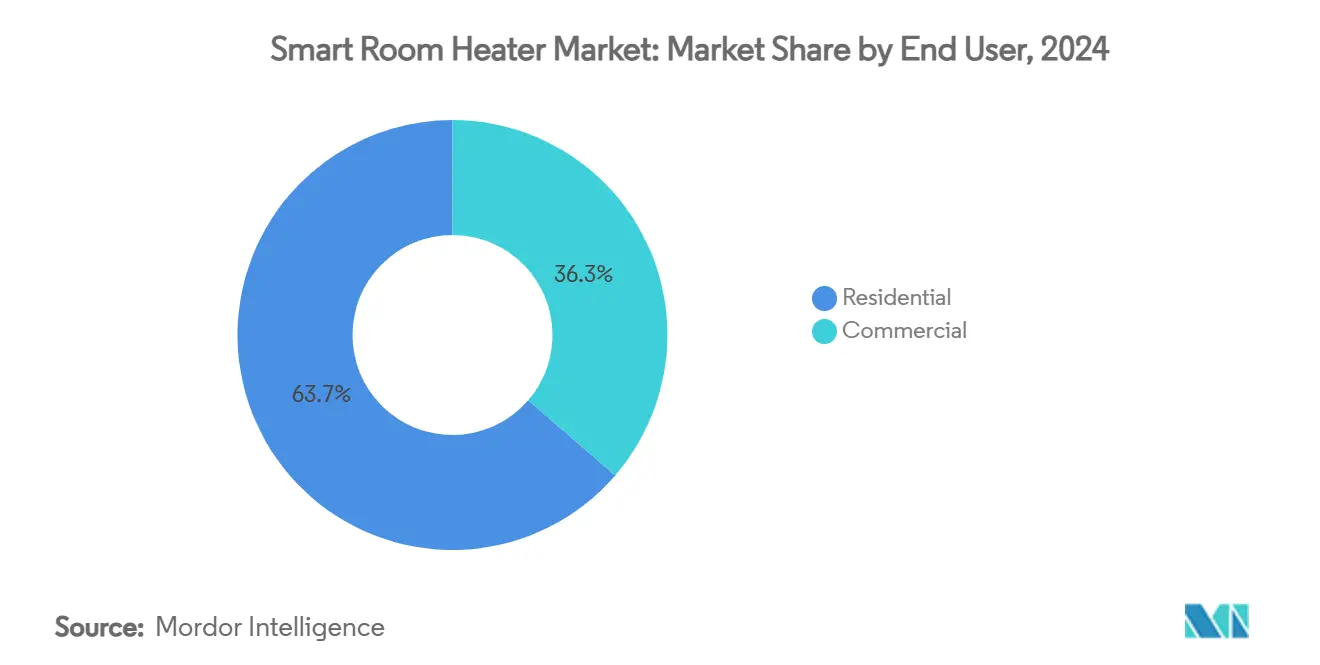

- By end user, residential applications held 63.66% of the smart room heater market share in 2024; commercial installations are anticipated to record a 13.69% CAGR to 2030.

- By distribution channel, B2C captured 71.12% of the smart room heater market in 2024; B2B holds the highest forecast growth at a 12.28% CAGR.

- By geography, North America commanded 39.54% of the smart room heater market in 2024; Asia-Pacific is forecast to post the fastest growth at a 14.52% CAGR.

- Dyson, De’Longhi, Glen Dimplex, Honeywell, and Xiaomi collectively hold major market share of global shipments, leveraging brand equity, retail reach, and firmware sophistication.

Global Smart Room Heater Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid electrification of home-heating in off-gas-grid regions | +2.1% | Global, with concentration in North America rural areas and Nordic regions | Medium term (2-4 years) |

| Regulatory push for IoT-based demand-response (DR) appliances | +1.8% | Europe & North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Mass-customizable ceramic Positive Temperature Coefficient (PTC) elements lowering Bill of Materials (BOM) cost | +1.2% | Global manufacturing hubs, particularly Asia-Pacific | Short term (≤ 2 years) |

| Generative-AI-driven predictive maintenance algorithms | +0.9% | North America & Europe early adoption, global rollout | Medium term (2-4 years) |

| Smart-grid rebates for connected heaters in Nordic markets | +0.8% | Nordic countries (Sweden, Norway, Denmark), expanding to EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification of Home-Heating in Off-Gas-Grid Regions

Governments see electrification of rural housing as a fast route to decarbonization, and off-pipeline towns are switching from oil or propane to high-efficiency space heaters linked to renewables. In China, heat-pump sales rose 12% in 2023, highlighting the appetite for plug-and-play electric comfort solutions [1]International Energy Agency, “Heat Pump Sales 2023,” iea.org. Southeast Asian utilities plan USD 56 billion of rural grid upgrades by 2040, broadening the base for small-format smart heaters. Devices pre-certified for aggregator programs allow operators to shave peaks and reward homeowners with bill credits, translating policy intent into tangible savings. As carbon prices creep upward, electricity gains a cost edge over delivered fuels, pushing penetration even in cold zones that traditionally relied on combustion appliances. Vendors able to prove load-shift capability win early access to pilot subsidies, reinforcing a self-reinforcing loop of scale and cost decline across the smart room heater market.

Regulatory Push for IoT-Based Demand-Response Appliances

The EU Code of Conduct for energy-smart appliances, launched in April 2024, sets interoperability rules that every new electric heater must meet to qualify for eco-design labeling [2]European Commission, “EU Code of Conduct for Energy-Smart Appliances,” ec.europa.eu.. Ten multinational manufacturers, including Arçelik and Electrolux, pledged compliance within twelve months, making connectivity a baseline rather than a premium add-on. Nordic grant schemes pay households up to 10,000 NOK for certified energy-management systems, while U.S. utilities widen time-of-use tariffs that cut invoices for homes participating in automated load curtailment. Product managers, therefore, prioritize open APIs, firmware-over-the-air pipelines, and secure cloud back ends, turning regulatory pressure into a catalyst for digital differentiation in the smart room heater market.

Mass-Customizable Ceramic PTC Elements Lowering BOM Cost

Advances in sintering deliver ceramic matrices that self-regulate at precise temperatures, removing the need for thermal fuses and precious-metal coils. Production lines can toggle resistance curves via software, making “lot-size-one” scheduling viable without expensive tooling swaps. Energy losses fall by as much as 30% compared with tubular elements, which cushions the added bill-of-materials cost of embedded microcontrollers. These efficiencies trickle into retail tags, broadening appeal in price-sensitive provinces and reinforcing ceramic PTC dominance inside the smart room heater market.

Generative-AI-Driven Predictive Maintenance Algorithms

Edge AI chips inside premium heaters analyze vibration, temperature, and voltage curves to predict failures weeks in advance. Carrier and Google Cloud integrate the model outputs into a unified dashboard that also controls rooftop batteries, enabling whole-home energy orchestration. Continuous self-learning adapts to weather forecasts and occupancy schedules, lowering annual heating bills without user intervention. Subscription analytics generate recurring revenue, offsetting commoditization risk and giving AI-enabled brands a pricing umbrella over low-cost challengers in the smart room heater market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High real-time electricity prices in cold climates | -1.5% | Nordic countries, Northern North America, Eastern Europe | Short term (≤ 2 years) |

| Cyber-security vulnerabilities in low-cost Wi-Fi modules | -0.7% | Global, with higher impact in security-conscious markets | Medium term (2-4 years) |

| Fragmented connectivity standards (Matter, Zigbee, Thread) | -0.6% | Global, affecting interoperability and consumer adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Real-Time Electricity Prices in Cold Climates

Volatility in day-ahead power markets pushes heating costs beyond household budgets during winter peaks. Consumers lacking battery storage or demand-response contracts face sticker shock, delaying upgrades to electric units. Governments attempt to cushion the blow with targeted rebates, yet the perception of high running costs lingers. Manufacturers respond by integrating tariff-aware scheduling that pre-heats rooms when prices are low, though awareness of these features remains uneven.

Cyber-Security Vulnerabilities in Low-Cost Wi-Fi Modules

Cheap microcontrollers often ship with default passwords and unencrypted traffic, exposing households to botnet hijacks and privacy breaches. Researchers found hard-coded passwords in multiple mass-market smart heaters, opening doors to botnet assaults. Legislators now draft labeling laws that mirror home-appliance energy stickers, pushing manufacturers to invest in secure elements, encrypted bootloaders, and OTA patch cadences. Compliance costs could squeeze margins for entry-level brands, narrowing SKU portfolios and slowing adoption among cost-sensitive buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ceramic PTC Leads Safety-Centric Design

Ceramic PTC heaters controlled 43.23% of the smart room heater market in 2024, thanks to self-limiting resistivity that halts runaway temperatures without external switches, pleasing safety regulators and insurers alike. Manufacturing clusters in Ningbo and Osaka churn out die-stack variants optimized for 110 V and 230 V mains, supporting cross-region product lines with minimal re-qualification. Infrared and halogen units enjoy 11.95% CAGR prospects by delivering instant radiant warmth for bathrooms and terraces, paired with occupancy sensors that switch off when rooms are empty, amplifying energy savings.

A second growth pocket emerges in fan-forced models that integrate HEPA-grade filters, doubling as air purifiers for allergy sufferers. Oil-filled radiators remain niche, yet school districts choose them for silent overnight operation that avoids draft irritation. Across categories, vendors standardize control boards around a common ARM Cortex MCU, simplifying firmware updates and speeding time-to-market. Consumers gain consistent app UIs regardless of heater type, reinforcing brand cohesion and aiding vendor lock-in within the expanding smart room heater market.

By Connectivity & Control: Wi-Fi Dominance Meets Matter Upswing

Wi-Fi accounted for 64.23% of shipments in 2024 as home routers deliver ready infrastructure and cloud reach. WPA3 rollouts bolster confidence against packet sniffing, and app-based onboarding remains intuitive for mainstream buyers. Matter-ready heaters, however, clock a 10.23% CAGR through 2030 as shoppers prioritize future-proofing. Thread mesh lowers standby power, aligning with EU eco-design rules that cap idle draw at 0.50 W by 2025.

Brands mitigate uncertainty by shipping multiprotocol chips supporting Wi-Fi, Bluetooth LE, and 802.15.4 in one package, but certification cycles multiply, stretching quality-assurance budgets. Early adopters in Germany and the U.K. accept higher MSRPs for assurance that Siri, Alexa, and Google Home continue to see devices after the next firmware wave. Corporate campuses lean toward Zigbee Pro for deterministic latency inside building-automation backbones, but vendor roadmaps suggest gradual migration as Matter supports bridge modes, smoothing the path for the smart room heater market.

By Power Rating: Sub-Kilowatt Units Dominate Remote Workspaces

Heaters under 1 kW held 53.12% of the smart room heater market size in 2024 as work-from-home users opted for personal warmth instead of raising central thermostats. Built-in occupancy detection dims output when chairs are empty, extending element life and reducing breaker trips. The 1–2 kW segment is rising at 11.92% CAGR because ceramic advances permit higher output without commensurate noise or surface temperature, appealing to family rooms and rental flats.

Commercial renovations favor 2–3 kW slim panels that tuck under glazing to counter downdrafts, while high-bay workshops adopt greater than 3 kW infrared bars integrated with presence beacons to heat only occupied zones. Edge analytics schedules soft-start cycles to limit inrush current, avoiding nuisance trips in vintage wiring. The graduated wattage mix caters to diverse building stock, broadening penetration for the smart room heater market.

By End User: Commercial Uptake Outpaces Legacy Trends

Homeowners maintained 63.66% of the smart room heater market share in 2024, lured by low-install complexity and app compatibility with voice assistants. DIY retailers bundle optional subscription dashboards that translate kilowatt-hours into dollar savings, nurturing retention.

Commercial-site demand grows 13.69% CAGR as ESG-driven audits pressure landlords to disclose energy intensity. Heaters tied into BACnet or KNX controllers supply granular zone data for certification under LEED and BREEAM schemes. Hotels deploy AI to pre-condition rooms before check-in, raising comfort ratings without 24-hour operation. Multi-family developers integrate master cloud consoles, enabling remote troubleshooting, a selling point for prop-tech investors hunting digitizable assets within the smart room heater market.

By Distribution Channel: Direct-B2B Builds Recurring Pipelines

Retail still commands a 71.12% share, with e-commerce reviews and influencer unboxing accelerating consumer confidence. Store-within-store kiosks let shoppers compare airflow patterns via augmented reality, shortening decision cycles.

Direct B2B shipments, expanding 12.28% CAGR, cater to spec-driven tenders that request onsite commissioning and five-year data-service bundles. Glen Dimplex exited third-party distributors in Canada to own customer touchpoints, promising 24-hour spare-part dispatch. Manufacturers now run regional demo centers where facility managers test API hooks against their building-management systems before signing multi-year supply deals, reinforcing loyalty and smoothing demand curves in the smart room heater market.

Geography Analysis

North America topped regional rankings with 39.54% of the smart room heater market in 2024 on the strength of utility rebates, ENERGY STAR marketing, and entrenched smart-speaker ecosystems. Resideo’s USD 79.99 Honeywell Home X2S thermostat, unveiled at CES 2025, claims 22% heating-energy cuts and Matter compliance, underlining the push to mainstream connected climate control. Time-of-use spreads in California and Ontario reward devices that preheat ahead of evening surges, while grid operators in Texas roll out 100 MW virtual-heater aggregations for frequency support. Commercial retrofits benefit from state tax credits that treat connected heaters as grid assets, extending demand beyond detached houses.

Asia-Pacific is projected to accelerate at a 14.52% CAGR, buoyed by China’s heat-pump surge and India’s future tenfold AC ownership growth. Domestic appliance giants blend heaters with purifiers and dehumidifiers to meet subtropical comfort expectations, allowing cross-season revenue. Japan’s top three utilities sponsor pilot tariffs that pay apartments to shift heater load when renewable curtailment looms, while Australia’s rooftop-solar glut favors daytime resistive heating as a storage alternative, illustrating diverse policy levers funneling growth toward the smart room heater market.

Europe remains pivotal through ecodesign enforcement and April 2024 interoperability codes. Nordic grants worth up to 10,000 NOK per installation compress payback to under two winters. Germany’s Building Energy Act mandates heat metering per apartment, incentivizing smart panels that export data via M-Bus gateways, and France earmarks low-interest loans for retrofits that cut primary energy 30% or more. Southern nations pursue dual-mode heaters able to deliver cooling, matching Mediterranean climates and diversifying category mix. Political alignment and strict standby caps together steer R&D budgets, reinforcing Europe’s position as a regulatory trendsetter for the smart room heater market.

Competitive Landscape

Competition is moderately concentrated; Dyson, De’Longhi, Glen Dimplex, Honeywell, and Xiaomi collectively hold major market share of global shipments, leveraging brand equity, retail reach, and firmware sophistication. Dyson’s bladeless airflow commands high ASPs, and its adaptive algorithm adjusts the throw angle to minimize stratification, boosting perceived warmth without extra watts. Xiaomi piggybacks is its phone app store to deliver seamless onboarding across phones, routers, and wearables, unlocking cross-selling opportunities. Glen Dimplex’s direct channel switch in Canada tightens feedback loops on failure modes, accelerating iterative firmware fixes and sparking loyalty among professional installers.

Technological rivalry centers on ceramic PTC chemistry, cybersecurity hardening, and radio-stack abstracts that can swap between Matter and proprietary clouds without bricking. Bosch nearly doubled Home Comfort revenue via a USD 8 billion HVAC acquisition, granting leverage to co-develop SoCs tailored for low-power mesh [3]Bosch Group, “Completion of Johnson Controls HVAC Acquisition,” bosch.com. Carrier’s Google alliance shifts value from hardware margins to AI subscriptions, blending predictive maintenance with household battery dispatch, erecting barriers that parts-only rivals struggle to breach.

Smart Room Heater Industry Leaders

Dyson

De’Longhi

Glen Dimplex

Honeywell International

Xiaomi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Carrier Global partnered with Google Cloud to launch AI home-energy management spanning battery-enabled HVAC and connected heaters.

- January 2025: Resideo introduced the Honeywell Home X2S thermostat, Matter-ready and ENERGY STAR certified, priced at USD 79.99.

- January 2025: Rheem’s parent bought Fujitsu’s HVAC unit for USD 1.6 billion to deepen its smart-heating portfolio.

- July 2024: Bosch closed a USD 8 billion HVAC acquisition, almost doubling Home Comfort turnover to EUR 9 billion.

Global Smart Room Heater Market Report Scope

| Fan-Forced Smart Heaters |

| Convection/Panel Smart Heaters |

| Oil-Filled Radiator Smart Heaters |

| Infrared & Halogen Smart Heaters |

| Ceramic PTC Smart Heaters |

| Wi-Fi |

| Bluetooth |

| Zigbee/Z-Wave |

| Matter-Enabled |

| Proprietary RF |

| Less than 1 kW |

| 1-2 kW |

| 2-3 kW |

| Greater than 3 kW |

| Residential |

| Commercial |

| B2C/Retail | Multi-brand Stores (big box retailers, department stores, electronics chain, home improvement centers) |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B/Directly from the Manufacturers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Fan-Forced Smart Heaters | |

| Convection/Panel Smart Heaters | ||

| Oil-Filled Radiator Smart Heaters | ||

| Infrared & Halogen Smart Heaters | ||

| Ceramic PTC Smart Heaters | ||

| By Connectivity & Control | Wi-Fi | |

| Bluetooth | ||

| Zigbee/Z-Wave | ||

| Matter-Enabled | ||

| Proprietary RF | ||

| By Power Rating | Less than 1 kW | |

| 1-2 kW | ||

| 2-3 kW | ||

| Greater than 3 kW | ||

| By End-user | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores (big box retailers, department stores, electronics chain, home improvement centers) |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Directly from the Manufacturers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the value of the smart room heater market in 2025?

The smart room heater market size stands at USD 1.74 billion in 2025 and is projected to reach USD 2.76 billion by 2030.

Which heater technology is most popular today?

Ceramic PTC units dominate with a 43.23% share of 2024 shipments because they self-regulate temperature and meet safety codes.

How fast will Asia-Pacific demand grow?

Asia-Pacific demand is forecast to expand at a 14.52% CAGR through 2030, the fastest among all regions.

Why are Matter-compatible heaters gaining attention?

Matter assures cross-platform interoperability, letting devices work with major smart-home brands without separate hubs.

How does AI improve modern space heaters?

Embedded AI predicts component failures and schedules off-peak heating, cutting downtime up to 75% and lowering energy bills.

Which sales channel is gaining the most momentum?

Direct B2B shipments to commercial customers are rising at 12.68% CAGR because projects need customization and long-term service.

Page last updated on: