Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

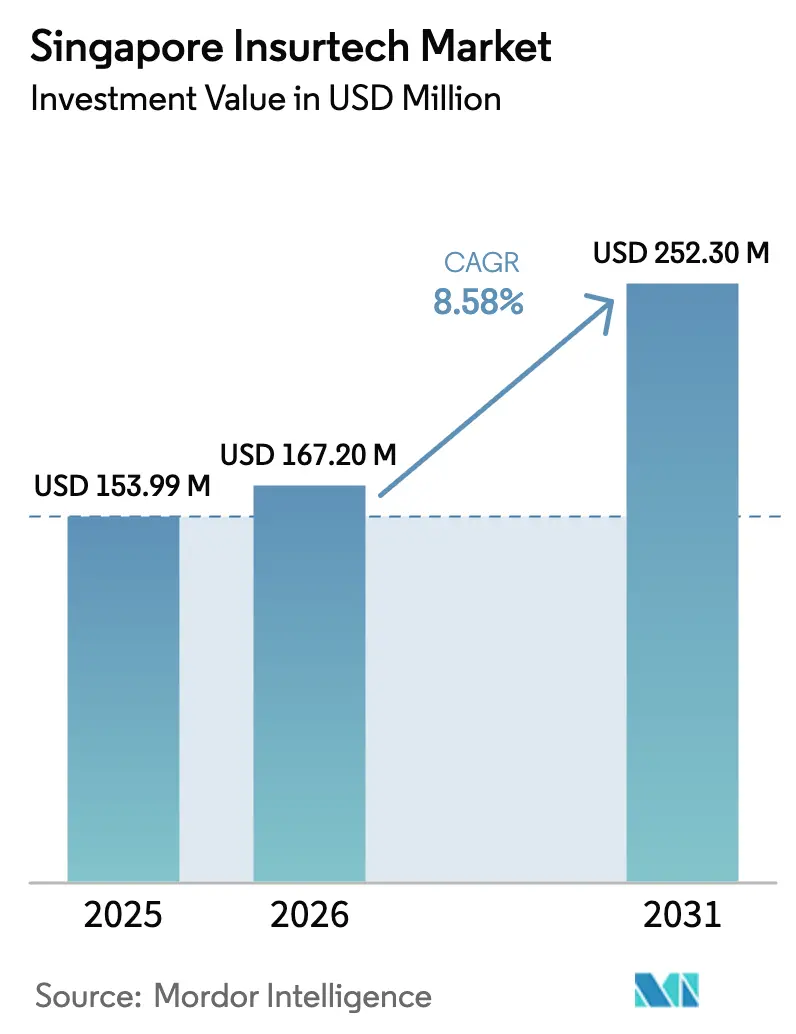

| Base Year Market Size (2025) | USD 153.99 Million |

| Market Size (2026) | USD 167.20 Million |

| Market Size (2031) | USD 252.30 Million |

| Growth Rate (2026 - 2031) | 8.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Insurtech Market Analysis by Mordor Intelligence

The Singapore Insurtech Market size in terms of investment value was valued at USD 153.99 million in 2025 and is estimated to grow from USD 167.20 million in 2026 to reach USD 252.30 million by 2031, at a CAGR of 8.58% during the forecast period (2026-2031).

Structural tailwinds support this path, including 98.4% internet penetration and 97% smartphone ownership, which keep digital channels central to acquisition and claims servicing in Singapore. Policy support remains strong, with the Monetary Authority of Singapore’s Financial Sector Technology and Innovation 3.0 scheme allocating USD 116.8 million (SGD 150 million) over three years, plus a separate USD 77.9 million (SGD 100 million) commitment focused on quantum computing and artificial intelligence capabilities, funding streams that lower innovation risk for incumbents and startups alike. Product innovation cycles in embedded insurance are accelerating as large carriers expand platform partnerships, illustrated by new, AI-optimized embedded distribution models introduced in 2025 that compress decision and claims timelines at the point of sale.

Key Report Takeaways

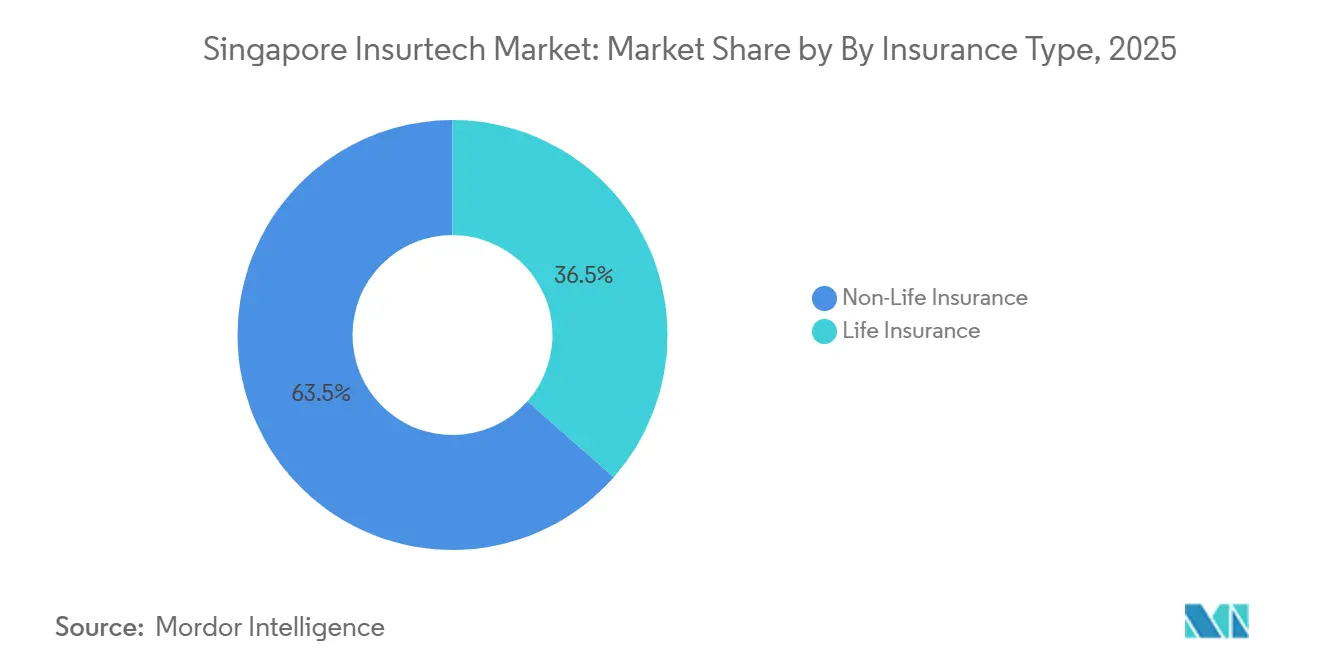

- By insurance type, Non-Life Insurance led with 63.50% of the Singapore insurtech market share in 2025 and is forecast to expand at a 10.65% CAGR through 2031.

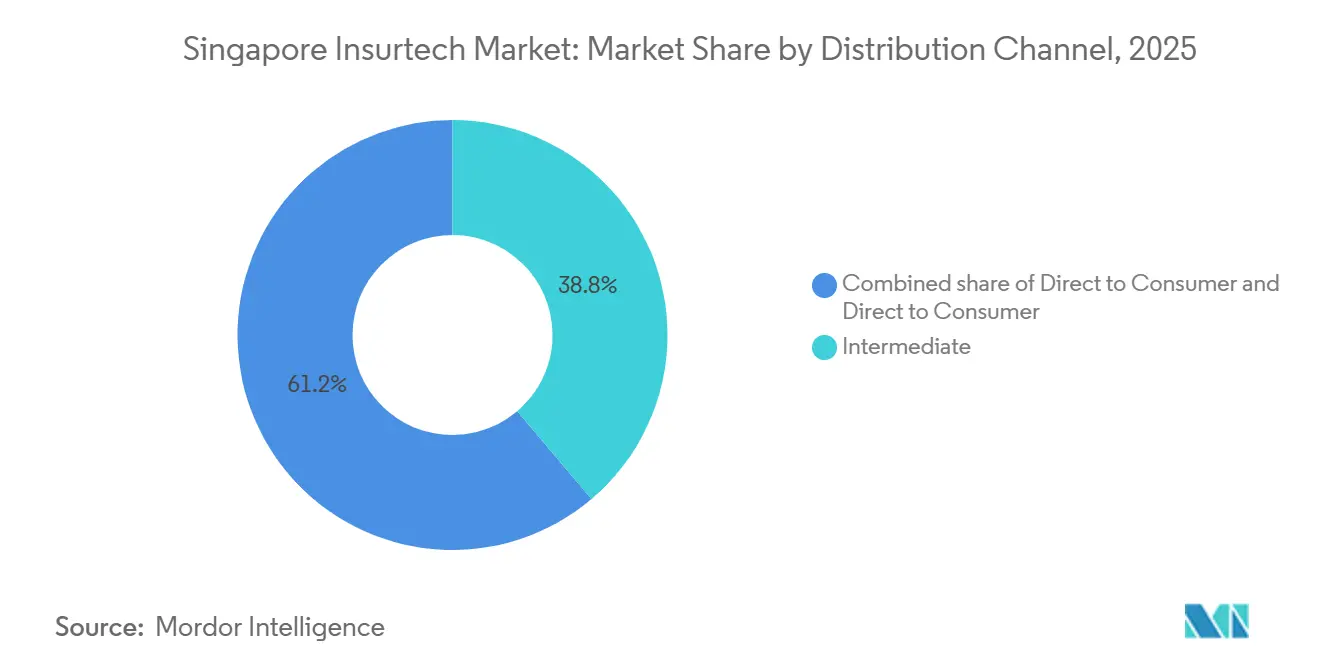

- By distribution channel, the Intermediate segment held 38.80% of the Singapore insurtech market size in 2025, while Embedded is projected to grow at a 9.65% CAGR through 2031.

- AIA Group, Prudential, Manulife, Great Eastern, and NTUC Income collectively shaped the Singapore insurtech market through their scale, digital partnerships, and expanding technology‑enabled distribution models.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Insurtech Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Adoption & Smartphone Penetration | +1.2% | National | Short term (≤ 2 years) |

| Regulatory Support & MAS Initiatives | +1.8% | National | Medium term (2-4 years) |

| Demand for Personalized Insurance Solutions | +1.5% | National | Medium term (2-4 years) |

| AI, ML & Advanced Analytics Enablement | +2.0% | National | Long term (≥ 4 years) |

| Supportive Fintech Regulatory Ecosystem | +1.3% | National | Medium term (2-4 years) |

| Rising Insurtech & Venture Investments | +0.8% | National, spillover to SEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital Adoption & Smartphone Penetration

Singapore’s connectivity provides a strong foundation for digital insurance distribution, with mobile connections reaching 162.6% of the population and wireless broadband subscriptions at 182.2% as of January 2025[1]Infocomm Media Development Authority (IMDA), “Statistics on Telecom Services for 2025 (Jan–Jun),” IMDA, imda.gov.sg. The finance and insurance sector contributes to a broader digital economy that reached USD 99.65 billion (SGD 128.1 billion) in 2024, equal to 18.6% of GDP, signaling a steady shift of customer journeys to digital interfaces, equivalent to USD 94.8 billion at recent average exchange rates. Full, standalone 5G coverage, achieved nationwide by 2025, enables telematics, computer vision-based claims assessments, and secure mobile submissions that reduce cycle times. These infrastructure advantages reinforce the Singapore InsurTech market by advancing real-time data capture, decisioning, and service workflows at scale.

Regulatory Support & MAS Initiatives

Targeted public funding and regulatory design have promoted live testing at manageable risk, backed by the MAS FinTech Regulatory Sandbox, Sandbox Express, and Sandbox Plus, which together broadened access to controlled pilots and non-routine models such as embedded or parametric insurance[2]Monetary Authority of Singapore, “FinTech Regulatory Sandbox,” Monetary Authority of Singapore, mas.gov.sg. The Financial Sector Technology and Innovation 3.0 scheme allocates USD 116.8 million (SGD 150 million) to sector-wide capacity building, while the 2024 top-up of USD 77.9 million (SGD 100 million) targets quantum and AI needs, further nudging the stack toward secure, explainable automation. The November 2025 consultation on Guidelines on AI Risk Management signals a shift from principles to lifecycle controls, requiring clear AI inventories, risk assessments, and oversight, with the consultation running to January 31, 2026. This evolving supervision increases clarity for the Singapore insurtech market by setting predictable guardrails for algorithmic use while encouraging safe deployment paths.

Demand for Personalized Insurance Solutions

A digitally fluent base expects tailored pricing and frictionless service, given Singapore’s 98.4% internet penetration and a large share of commerce on mobile channels. Carriers are responding with micro-coverage linked to daily activities, illustrated by SNACK by Income, which ties small premium contributions to triggers such as transit usage or fitness events inside a mobile lifestyle journey. Singlife and Doctor Anywhere introduced DA Healthwise Plus, integrating telemedicine with personal accident coverage and transparent pricing for consultations: general practitioner video visits at USD 10.12 (SGD 13.00) and specialist video visits at USD 54.50 (SGD 70.00), using recent average exchange rates. Chubb’s AI optimization engine launched in November 2025 to personalize embedded products at the point of sale within partner platforms, compressing decision steps and enabling smarter cross-sell inside non-insurance ecosystems[3]Chubb, “Chubb Unveils AI-Powered Optimization Engine,” Chubb, news.chubb.com. The Singapore insurtech market benefits as context-aware offerings align with user intent during checkout or in-app flows.

AI, ML & Advanced Analytics Enablement

Carriers in Singapore are scaling AI in underwriting and claims, supported by a maturing regulatory path that emphasizes transparency, fairness, and human oversight in model risk management. Prudential’s deployment of Google’s MedLM in Singapore and Malaysia demonstrates the push toward large language model use in the review of medical documentation and the automation of benefits validation, while maintaining human review loops. MAS convenes industry collaboration on AI safety and adoption, including technical guidance and shared learning that aligns model operations with TRM and data governance practices. The progression from pilots to production is now tied to lifecycle governance, which favours teams with strong data controls and observability built into pipelines. As these practices mature, the Singapore insurtech market should see broader deployment of machine learning in personalized pricing, fraud analytics, and claim adjudication.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity & Data Privacy Risks | -0.9% | National | Short term (≤ 2 years) |

| Regulatory Compliance Complexity | -0.6% | National | Medium term (2-4 years) |

| Legacy Insurer Resistance to Digital Models | -1.1% | National | Long term (≥ 4 years) |

| Limited Consumer Awareness in Select Segments | -0.4% | National, gig economy focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity & Data Privacy Risks

Threat activity remains elevated, with ransomware incidents and phishing attempts rising in 2024 and repeated supply chain exposures during 2025 that affected both insurers and banks. Income Insurance disclosed a May 2025 breach involving a third-party vendor, affecting at least 146 policyholders’ personal data, reinforcing the need for stronger vendor risk management and incident response playbooks. In April 2025, two banks reported customer data compromises linked to a service provider, highlighting that interdependencies can magnify adverse outcomes when controls fail outside the core insurer perimeter. PDPA rules require breach notification within 72 hours in defined circumstances and impose significant penalties, including up to 10% of annual turnover or USD 0.78 million (SGD 1 million), whichever is higher, intensifying compliance and capital planning needs for data-intensive services. The Singapore insurtech market must prioritize identity-centric security and data minimization to balance scale with resilience in light of these regulatory and operational realities.

Legacy Insurer Resistance to Digital Models

Legacy platforms and siloed data estates can slow cloud adoption, reduce release frequency, and complicate real-time analytics needed for usage-based pricing and instant claim assessment. Many incumbent environments must migrate core functions while maintaining uninterrupted service for large policyholder bases, which forces parallel operations that extend timelines. Operating models and incentives can favour incremental changes rather than the rebuilds needed to capture the full benefit of APIs and automated workflows. These conditions contrast with those of cloud-native challengers, which are designed for modular services and faster partner integration. The Singapore insurtech market, therefore, moves at different speeds, with incumbents balancing risk, cost, and continuity against the urgency to modernize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Non-Life Commands Both Share and Velocity

Non-Life Insurance accounts for 63.50% of value in 2025 and is projected to grow at a 10.65% CAGR through 2031, reflecting faster uptake of cyber, travel, and device-protection products that fit mobile commerce and mobility contexts. Global carriers continue to expand embedded offerings through partner ecosystems, and recent platform activity showcases automatic claims triggers and in-app evidence collection that shorten cycle times. Distribution elasticity in retail, travel, and device channels gives non-life product suites more frequent customer touchpoints in Singapore. As multi-product platforms mature, the Singapore insurtech market increases its capacity to bundle and cross-sell coverage based on customer behaviour signals. Near-term momentum should benefit Non-Life as contextual distribution evolves along with improved data access and consent frameworks.

Life Insurance holds the remaining value in 2025 and continues to face longer development cycles, although digitization of underwriting, claims, and policy servicing is advancing across leading incumbents. The use of advanced analytics in medical claims triage shows potential to free capacity and improve speed without compromising oversight. Singapore’s aging profile raises the relevance of health and protection coverage, and digital advice alongside human channels can improve financial planning outcomes. The Singapore insurtech market prioritizes transparent, mobile-first experiences to sustain engagement as Life products diversify through riders and wellness-linked benefits. Near-term focus in Life will remain on automating operations, streamlining distribution, and integrating data responsibly within the regulatory guidelines.

By Distribution Channel: Embedded Ascends While Intermediates Persist

The Intermediate channel leads with a 38.80% share in 2025, given the role of licensed advisers, brokers, and bancassurance for complex products. Direct-to-Consumer models expand where digital issuance and services reduce friction and costs, supported by mobile onboarding and conversational assistance. Embedded insurance is the fastest-growing distribution channel, with a 9.65% CAGR through 2031, as carriers integrate offers into e-commerce, travel, and banking journeys through AI-enhanced, real-time personalization. A broadening set of embedded partnerships across digital banks, retailers, and travel platforms signals a durable shift toward context-triggered protection. The Singapore insurtech market benefits as partners leverage stable identity, payments, and consent frameworks to scale distribution.

API-first carriers continue to invest in orchestration layers that simplify partner onboarding and product changes without manual rework. Examples include instant policy activation for travel bookings or device protection claims validated by photo-based evidence flows that auto-populate forms within partner apps. Another embedded vector is mobility and super-app ecosystems that embed short-duration products tied to rides or deliveries, which use location and transaction context to refine coverage. The Singapore insurtech industry is also expanding device lifecycle partnerships that pair financing with protection and upgrade programs as a single offer across channels. Together, these developments improve unit economics for digital distribution and keep the Singapore insurtech market focused on embedded growth while intermediated advice stays relevant for high-consideration needs.

Geography Analysis

Singapore’s national context concentrates distribution, regulation, and infrastructure in one jurisdiction, which shortens experimentation cycles for new business models and supports faster deployment of secure data pipelines. Programs like the FinTech Regulatory Sandbox and Sandbox Plus enable controlled tests and grant support for regulated propositions, providing clearer routes from pilot to production. SGFinDex scaled to 150,000 users and 620,000 data retrievals by July 2025 for insurance, showing real uptake in data portability within a consented and auditable framework. In this setting, the Singapore insurtech market applies identity standards and API practices to streamline customer onboarding and multi-carrier visibility. These foundations help de-risk cross-partner workflows that rely on secure exchange and verification.

Singapore’s connectivity profile, including nationwide 5G and high smartphone adoption, positions it as an ideal venue for testing telematics, computer vision claims, and micro-duration insurance tailored to platform transactions. Global incumbents and technology-led entrants continue to pick Singapore as a base to build regional alliances that extend into e-commerce and travel aggregators. This activity amplifies the Singapore insurtech market by aligning business development with a regulator-led strategy that elevates trusted identity and data governance. Strong baseline trust in digital public infrastructure reduces friction costs and compresses launch timelines.

M&A and capital flows underscore the role of Singapore as a hub. Singapore also supports alternative risk transfer with an insurance-linked securities platform and grant scheme that helped catalyze catastrophe bond issuance totalling USD 4 billion from late 2018 to late 2024. These attributes help the Singapore insurtech market function as a scale-up location where regional partnerships, funding, and regulatory clarity intersect.

Competitive Landscape

Large incumbents are modernizing insurance, while tech-driven entrants focus on embedded and device-linked coverage. Four major insurers in Singapore - AIA Singapore, Income Insurance, Prudential Assurance Singapore, and Great Eastern Life - operate under stricter capital and planning requirements, which shape their investment strategies. Embedded leaders are deepening integrations, such as Zurich’s platform partnerships with aggregators and e-commerce, and Chubb’s AI engine for tailored point-of-sale offers. Prudential’s MedLM use for claims in Singapore and Malaysia highlights the use of generative models in production workflows with human oversight. These developments reflect Singapore’s insurtech market's balancing act between modernization and scaling.

Strategic priorities include inorganic growth, platform expansion, and AI compliance. Bolttech’s June 2025 funding and May 2025 partnership with Sumitomo on device lifecycle programs expand access via retail and financial channels. MAS initiatives in AI risk management and TRM guidelines promote transparent, auditable models, accelerating adoption among firms with lifecycle governance. Regulatory clarity supports confident deployments in Singapore’s insurtech market.

Growth focuses on ecosystem design and multi-product experiences within API-first frameworks. Income’s SNACK delivers behavior-linked micro-coverage, while DA Healthwise Plus integrates telemedicine and protection for better access. Super-apps and mobility services offer short-duration policies for rides or deliveries, generating data to refine pricing and claims. As carriers align with platform partners, Singapore’s insurtech market embeds products that streamline purchases and claims while ensuring compliance and customer trust.

Singapore Insurtech Industry Leaders

AIA Group

Nippon Life Group

Life Insurance Corporation of India (LIC)

China Life Insurance Group

Ping An Insurance Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Chubb unveils an AI-powered optimization engine on its Chubb Studio platform at the Singapore Fintech Festival, enabling real-time analysis of customer data to deliver personalized insurance offerings seamlessly integrated into digital distribution partners' platforms, compressing underwriting decisions from days to seconds.

- October 2025: Zurich Insurance in Asia Pacific announced winning ‘Best Embedded Insurance Innovation’ and ‘Best EV Insurer’ at the (Re)inAsia Asia Consumer Insurance Awards 2025. Recognized for Zurich Edge’s digital-first solutions and innovative electric mobility insurance, Zurich has established over 90 partnerships across sectors, leveraging its Zurich Edge Platform for tailored, efficient, and customer-centric offerings.

- June 2025: Bolttech raised USD 147 million in its Series C funding round, reaching a USD 2.1 billion valuation. New investors Sumitomo Corporation and Iberis Capital joined earlier Series C backers Dragon Fund and Baillie Gifford. Operating in 35+ markets with 700+ distribution partners, Bolttech offers over 6,000 insurance products. Tokio Marine, MetLife, and MUFG participated in prior rounds but were not part of the final June 2025 closing.

- May 2025: Sumitomo Corporation announces an investment in bolttech and a joint venture targeting device lifecycle management across Southeast Asia, combining Sumitomo's consumer finance expertise with bolttech's insurance and distribution capabilities to offer installment sales, upgrade programs, and protection plans with a goal of reaching 10 million customers by 2030.

Singapore Insurtech Market Report Scope

The Singapore insurtech market refers to the organized industry of technology-driven insurance solutions operating within Singapore’s highly regulated and digitally advanced ecosystem. Concentrated distribution, regulation, and infrastructure in one jurisdiction shorten experimentation cycles and accelerate deployment of secure data pipelines. Programs such as the FinTech Regulatory Sandbox and Sandbox Plus enable controlled testing and grant support for regulated propositions, providing clearer routes from pilot to production. SGFinDex, which scaled to 150,000 users and 620,000 data retrievals by July 2025, demonstrates real uptake in data portability within a consented and auditable framework. These foundations allow the Singapore insurtech market to apply identity standards and API practices to streamline customer onboarding, enhance multi-carrier visibility, and de-risk cross-partner workflows.

The market is segmented by insurance type, distribution channel, and geography. By insurance type, it includes life insurance and non-life insurance, reflecting differences in product design, risk coverage, and customer demand. By distribution channel, the market is divided into direct-to-consumer, intermediated, and embedded models, highlighting the shift toward digital-first and platform-integrated insurance offerings. The report offers market size and forecasts for the Singapore insurtech market in terms of transaction volume and/or revenue (USD) for all the above segments.

By Insurance Type

| Life Insurance |

| Non-Life Insurance |

By Distribution Channel

| Direct to Consumer |

| Intermediate |

| Embedded |

| By Insurance Type | Life Insurance |

| Non-Life Insurance | |

| By Distribution Channel | Direct to Consumer |

| Intermediate | |

| Embedded |

Key Questions Answered in the Report

What is the current size and projected value of the Singapore insurtech market?

The Singapore insurtech market stands at USD 167.20 million in 2026 and is projected to reach USD 252.3 million by 2031 at an 8.58% CAGR.

Which insurance type leads and grows fastest in Singapore?

Non-Life Insurance leads with 63.50% in 2025 and is also the fastest growing, forecast to expand at a 10.65% CAGR through 2031.

Which distribution channel is gaining the most momentum in Singapore insurtech?

Embedded distribution is the fastest-growing at a 9.65% CAGR through 2031 as carriers scale in-app and checkout-based offers with AI-driven personalization.

How is MAS regulation shaping AI use for insurers?

MAS is moving toward lifecycle AI oversight with a November 2025 consultation covering inventories, risk materiality, fairness, transparency, and human oversight, with feedback open until January 31, 2026.

What cybersecurity events recently influenced Singapore insurers?

In 2025, Income Insurance reported a vendor-related data breach affecting 146 policyholders, and two banks disclosed customer data compromises tied to a third-party provider, reinforcing supply chain risk focus.

Which recent deals and launches matter for embedded insurance in Singapore?

Notable moves include Bolttech’s USD 147 million funding and Chubb’s AI optimization engine for embedded personalization introduced in November 2025.

Page last updated on: