Shielding Gas For Welding Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.46 Billion |

| Market Size (2031) | USD 8.31 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

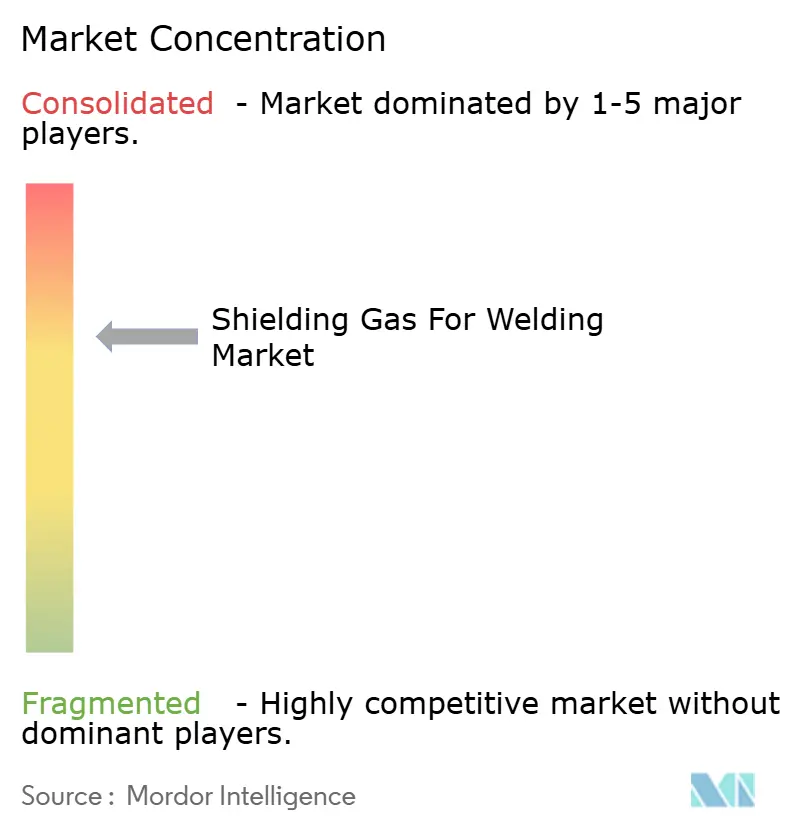

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Shielding Gas For Welding Market Analysis by Mordor Intelligence

The Shielding Gas For Welding Market size is projected to expand from USD 6.14 billion in 2025 and USD 6.46 billion in 2026 to USD 8.31 billion by 2031, registering a CAGR of 5.18% between 2026 to 2031. As manufacturers scale up automated welding cells, they emphasize the need for precise gas-mix control. In the Asia-Pacific region, major infrastructure projects are consuming significant amounts of argon and carbon dioxide blends. Precision aerospace programs are turning to ultra-high-purity supply chains, demanding high-purity argon for their titanium and nickel joints. The growing adoption of wire-arc additive manufacturing is sparking interest in hydrogen-argon blends, known to enhance penetration and minimize porosity in reactive alloys. At the same time, digitalized gas-management services are enabling suppliers to secure long-term contracts and navigate spot-price fluctuations. This trend is bolstering consistent growth in the market for shielding gases used in welding.

Key Report Takeaways

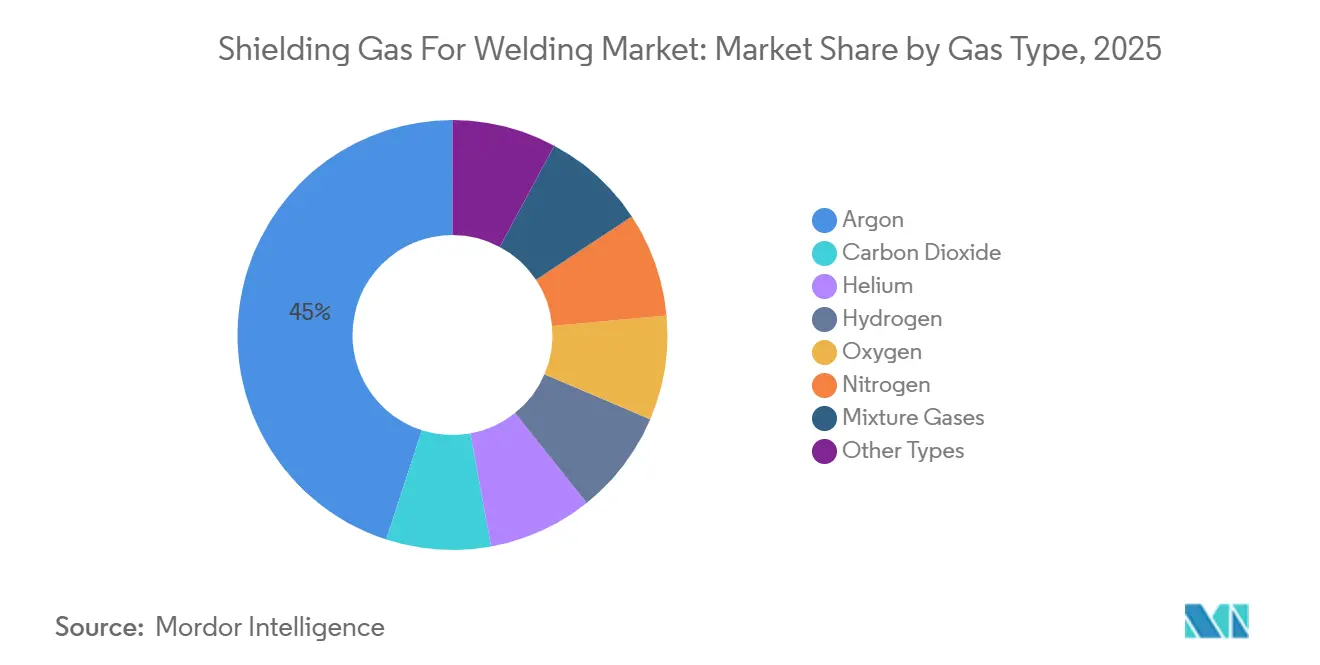

- By gas type, argon led with 45.01% of the shielding gas for the welding market share in 2025. Hydrogen-based blends are forecast to post the fastest 5.75% CAGR from 2026 to 2031 within the shielding gas for welding market size, driven by WAAM adoption.

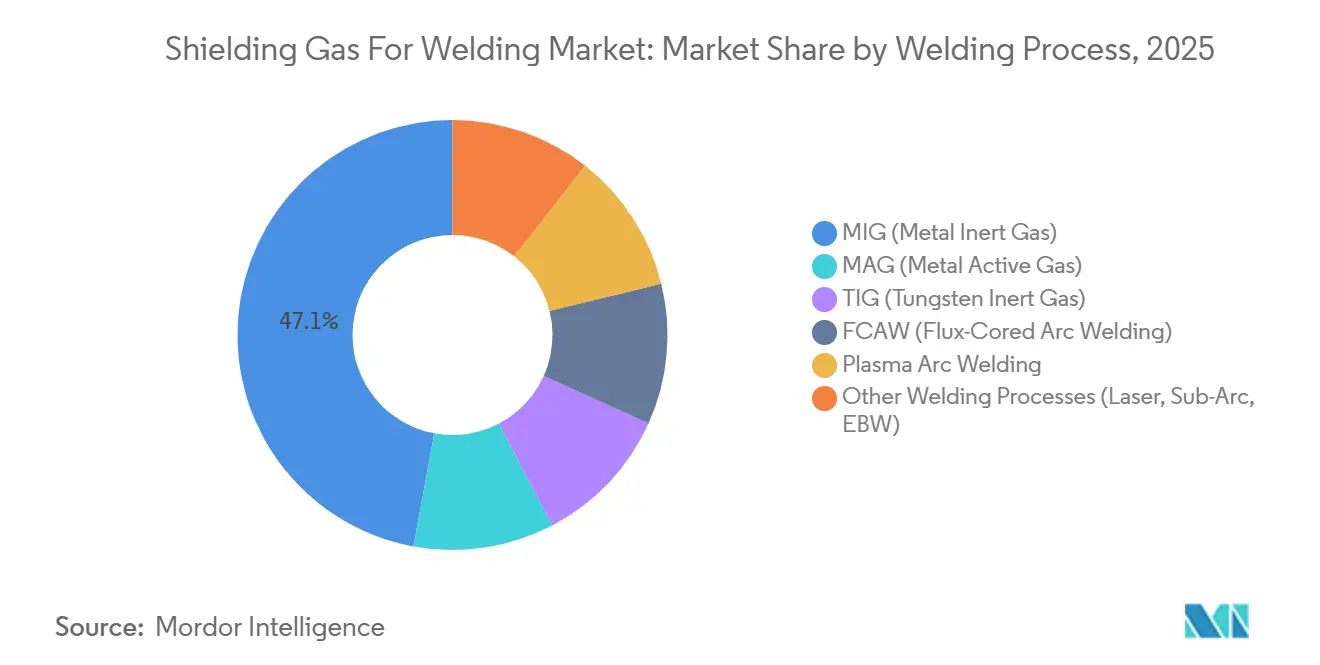

- By welding process, MIG accounted for 47.09% revenue share in 2025, while laser, SAW, and EBW combined are expected to advance at a 6.05% CAGR between 2026 and 2031.

- By application, automotive and transportation captured 25.16% of the shielding gas for welding market size in 2025; aerospace and defense is expected to register the highest 6.28% CAGR between 2026 and 2031.

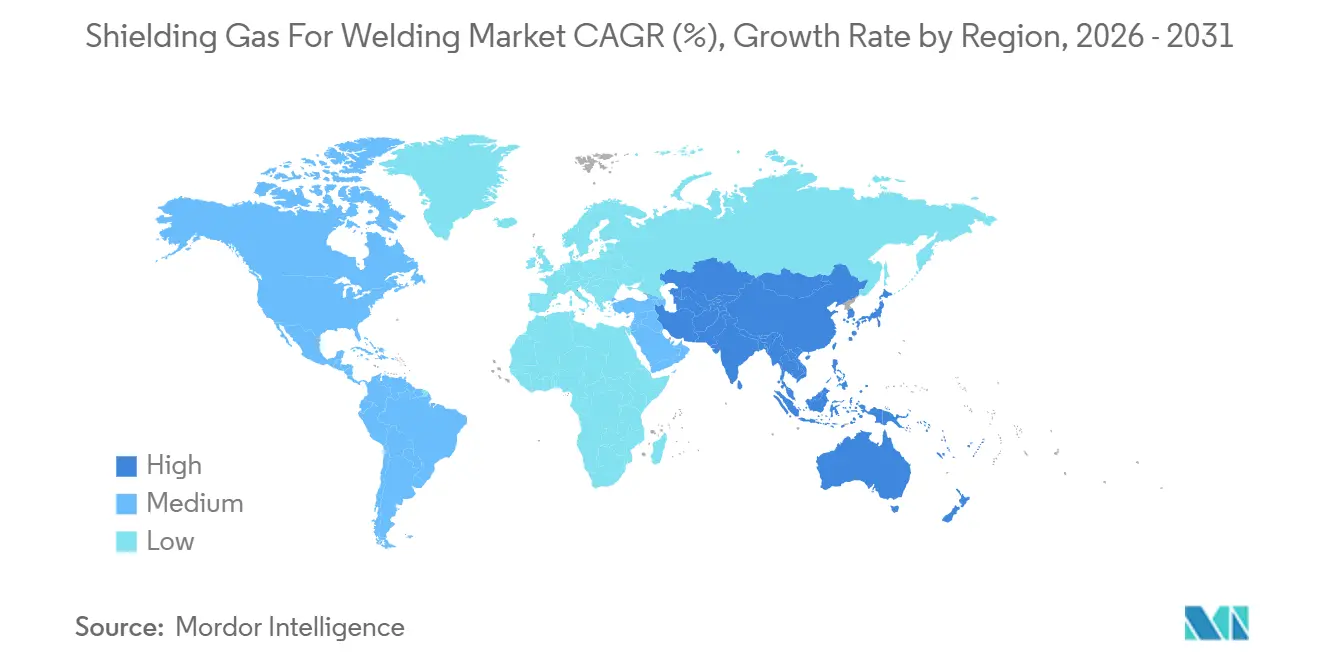

- By geography, Asia-Pacific controlled 39.75% market share in 2025 and is expected to expand at a 6.14% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Shielding Gas For Welding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Automotive, Shipbuilding, and Construction Welding Demand | +1.20% | Asia-Pacific and North America industrial corridors | Medium term (2-4 years) |

| Rapid Uptake of MIG/TIG for Thin-Gauge Precision Components | +0.90% | North America, Europe, Japan | Short term (≤ 2 years) |

| Growing Infrastructure Spending in Emerging Economies | +1.50% | Core Asia-Pacific, spill-over to Middle-East and Africa | Long term (≥ 4 years) |

| Productivity Push via Automated and Robotic Welding Cells | +1.10% | Global, with early adoption in Europe, North America, and Japan | Medium term (2-4 years) |

| Additive Manufacturing (LMD/WAAM) Needs Ultra-High-Purity Shield Gases | +0.70% | North America, Europe, China, and aerospace clusters worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Automotive, Shipbuilding, and Construction Welding Demand

The automotive sector plays a significant role in the base-load consumption of argon-carbon dioxide blends, alongside the shipbuilding and infrastructure sectors. The industry's adoption of automation further emphasizes this importance. For instance, Liebherr's Telfs plant reported a substantial increase in production efficiency after implementing an autonomous robotic welding cell, showcasing how original equipment manufacturers are leveraging robotics to address the shortage of skilled welding labor[1]Induportals Media Publishing, “Liebherr & Yaskawa Implement Fully Autonomous Welding Cell,” Metalworking International, METALWORKINGMAG.COM. In 2024, LNG Canada's project relied on a significant number of pipe welders, utilizing substantial amounts of shielding gas during continuous hours of welding its final seam. India's extensive National Infrastructure Pipeline, along with China's ongoing construction of a vast network of high-speed rail, drives consistent demand for metal inert gas and flux-cored arc welding. This demand, in turn, encourages the establishment of new air-separation units. For structural steel applications, the preferred choice remains argon-carbon dioxide mixtures, as they promote deep penetration and minimize spatter, leading to notable rework savings. The concentration of these large-scale projects not only justifies investments in local air-separation units but also strengthens regional supply chains, bolstering the market for welding shielding gases.

Rapid Uptake of MIG/TIG for Thin-Gauge Precision Components

Fabricators are increasingly turning to digitally controlled inverters, which provide stable tungsten inert gas arcs at low currents and metal inert gas arcs at moderate currents, for processing materials under minimal thickness. Sichuan Morrow’s WSM-400 showcases an ultralow-current tungsten inert gas capability, adept at preventing burn-through on aerospace titanium with extremely thin dimensions. NASA’s PRC-0002 specification underscores the necessity of high-purity argon gas and explicitly bans gas metal arc welding for titanium, amplifying the demand for high-purity gas. While automotive body-panel suppliers are transitioning cosmetic seams to laser welding, tungsten inert gas welding remains crucial for repairs and visible joints, especially in areas inaccessible to lasers. Consequently, the industry's shift towards thinner materials is bolstering a niche, premium segment in the shielding gas market for welding.

Growing Infrastructure Spending in Emerging Economies

Asia-Pacific, holding a significant share in 2025, is poised for further growth as major projects secure multiyear shielding-gas contracts. India's National Infrastructure Pipeline, encompassing roads, railways, and ports, schedules thousands of welded joints per kilometer. Meanwhile, China's high-speed rail extensions similarly boost gas offtake. In North America, substantial public-works funding in 2026 broadens the scope to include bridges and power-transmission lines. On-site storage tanks and cylinder-exchange programs facilitate the movement of bulk argon and argon-carbon dioxide blends, effectively minimizing downtime. Messer's investment in an air separation unit in Arkansas underscores a strategic localized capacity build-out, ensuring commitments to long-term contracts.

Productivity Push via Automated and Robotic Welding Cells

Collaborative and autonomous cells are streamlining cycle times and standardizing shield-gas flow. Panasonic's third TAWERS WG4 line at STADLER has significantly reduced component cycles by incorporating weld-navigation software and high-speed robots. ABB's OmniVance cell features programming that simplifies the teaching process and broadens access to automated metal inert gas and metal active gas welding for small and medium-sized enterprises. In automated settings, stable and predictable gas usage paves the way for managed-service contracts. These contracts, which combine digital flow monitoring with predictive refill logistics, set large suppliers apart in the shielding gas market for welding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Prices and Logistics for Argon/CO₂ Cylinders | -0.80% | Europe, India, and localized United States industrial hubs | Short term (≤ 2 years) |

| Strict Safety and Hazmat Regulations on High-Pressure Gas Handling | -0.50% | North America, Europe; tightening in Asia-Pacific | Medium term (2-4 years) |

| Substitution Threat from Solid-State and Friction-Stir Welding | -0.60% | Automotive hubs in Asia, Europe, and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices and Logistics for Argon/CO₂ Cylinders

In early 2026, argon spot prices experienced significant fluctuations. During the same period, the price of Linde's cylinder refill for shielding gas increased notably, creating cost uncertainties for fabricators. Localized shortages, such as the argon supply constraints in Maharashtra in 2024, compelled emergency sourcing at higher rates and heightened interest in bulk-delivery contracts. Suppliers with regional air separation unit networks have gained leverage. However, increasing logistics expenses are squeezing margins, curtailing the expansion of the near-term shielding gas market for welding.

Strict Safety and Hazmat Regulations on High-Pressure Gas Handling

The Occupational Safety and Health Administration regulations and the Department of Transportation guidelines enforce strict requirements for cylinder storage distances, periodic hydrostatic testing, and comprehensive record-keeping, which contribute to increased ownership costs[2]“29 CFR 1910.253,” CustomsMobile, CUSTOMSMOBILE.COM . Smaller shops depend on supplier-managed exchange programs, sacrificing some operational flexibility as they integrate cylinder assets with prominent gas companies. Compliance expenses are affecting the adoption of innovative high-pressure hydrogen-argon blends and are impacting the market for welding shielding gases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gas Type: Argon Dominance Meets Hydrogen Momentum

Argon retained 45.01% shielding gas for the welding market share in 2025, its inertness aligning with MIG and TIG mainstream processes. Hydrogen-enriched blends are forecast to log the highest 5.75% CAGR between 2026 and 2031. WAAM users achieve significantly deeper penetration on the GH3535 alloy by adding a small percentage of hydrogen to argon. While carbon dioxide remains a preferred choice for cost-sensitive steel fabrication, its pure form reduces elongation compared to argon mixes. This limitation encourages users to adopt blends that balance toughness and bead geometry. In the aluminum WAAM segment, helium finds a niche application, where its addition to argon effectively reduces porosity. Furthermore, specialty ternary mixes are utilized to optimize both thermal conductivity and bead shape. Together, these gas mixtures enhance the value-added segment of the welding shielding gas market, while argon continues to maintain its leadership in terms of volume.

Nippon Sanso’s Operational Excellence initiative, aimed at achieving significant cost savings, highlights a strong belief in argon's continued dominance, especially with investments in onsite air separation unit argon recovery. However, the growing adoption of hydrogen introduces premium-priced formulations, which increase per-cubic-foot revenues, even though the volumes remain relatively small.

By Welding Process: MIG Still on Top, Laser-Hybrid Gaining

MIG controlled 47.09% of 2025 revenue owing to 3-4 kg/h deposition rates and easy automation. However, laser, SAW, and EBW together are forecast at 6.05% CAGR between 2026 and 2031 as fabricators prioritize low heat input and minimal distortion. Hybrid laser-arc welding of nine percent nickel liquefied natural gas steel achieves significantly lower heat input compared to gas metal arc welding. This efficiency reduces both filler consumption and the need for rework. While these advanced processes consume less shielding gas per meter, they necessitate higher purity argon or argon-helium-hydrogen blends due to stringent quality demands. This requirement partially offsets the volume loss but simultaneously elevates the value density of the shielding gas in the welding market.

Tungsten inert gas welding is indispensable for aerospace titanium applications, where the risk of contamination is unacceptable. Plasma arc welding occupies a specialized niche, positioned between tungsten inert gas and laser methods. Meanwhile, flux-cored arc welding retains its prominence in outdoor settings, where wind poses challenges to gas shielding. The diverse array of welding processes, each with distinct gas requirements, fuels continuous innovation in gas mixture design and real-time flow regulation.

By Application: Automotive Volume vs Aerospace Precision

Automotive and transportation’s 25.16% share anchors high-volume consumption, leveraging robotic MIG lines for body-in-white and chassis assemblies. Yet aerospace, expanding at 6.28% CAGR between 2026 and 2031, every titanium joint demands high-purity argon and frequently requires dual-zone shielding, underscoring the disproportionate value of these gases. Orbital gas tungsten arc welding systems, such as the ESAB Model 6, monitor and log parameters like amperage, wire-feed speed, and gas flow for each weld. This not only embeds traceability but also nudges gas suppliers towards adopting sensor-rich delivery systems.

In shipbuilding, a blend of volume and specialty gases is utilized, especially for cryogenic tanks. Here, a specific combination of argon and hydrogen is crucial for optimizing low-temperature impact energy. The construction and infrastructure sectors depend on robust argon-carbon dioxide blends, especially for steel erection in challenging weather conditions, leading to a preference for large-capacity cylinder packs. Heavy fabrication and machinery sectors align with industrial production cycles, providing a consistent yet less volatile demand for shielding gases in welding.

Geography Analysis

Asia-Pacific, with 39.75% share in 2025, grows fastest at 6.14% CAGR between 2026 and 2031. China operates an extensive network of high-speed rail, and India is making significant investments in infrastructure, both driving sustained gas orders. In South Korea, liquefied natural gas shipyards utilize high-purity argon-hydrogen blends for nickel storage tanks. Meanwhile, the auto and electronics sectors in the Association of Southeast Asian Nations boost demand for these cylinders. Nippon Sanso, through its acquisition spree, including Coregas in Australia, broadens its air separation unit presence, aiming to shorten delivery times and shield customers from unpredictable imports.

North America is set to benefit from substantial infrastructure investments targeting bridges, pipelines, and renewable energy towers. Linde’s air separation unit in Oshkosh, scheduled for the latter half of the decade, strategically positions its supply close to Wisconsin’s metals hub. Concurrently, Air Liquide is investing significantly in upgrading its Louisiana facility, bolstering flows for the Gulf Coast's heavy industry. Messer’s air separation units in Berryville and Bryan are designed to reduce transport costs and capitalize on the region's manufacturing expansion.

Europe, while growing at a slower pace, showcases a technology-driven demand, particularly in aerospace, medical devices, and the evolving electric vehicle sector. Nippon Sanso's acquisition of Polaris enhances its modular air separation unit engineering capabilities, allowing better service for specialty gas clients in Germany and Italy. In South America, demands are closely linked to agriculture and mining. Conversely, projects in the Middle East and Africa focus on petrochemical plants and desalination facilities, leading to increased consumption of flux-cored arc welding and submerged arc welding gases in their hot, windy climates.

Competitive Landscape

The shielding gas for welding market is moderately concentrated. There's a noticeable shift in competitive focus towards managed-gas services and digital oversight. Suppliers are now rolling out Internet of Things-enabled regulators, flow meters, and cloud-based dashboards. These tools not only predict consumption but also automate refill scheduling. Through operational excellence initiatives, companies are capturing argon boil-off, automating cylinder filling, and harnessing artificial intelligence for route optimization, solidifying their cost leadership. As a result, pure merchant distributors, especially those without the capital for digital enhancements, face heightened entry barriers. This dynamic keeps market share concentrated, even amidst a growing total demand.

Shielding Gas For Welding Industry Leaders

Linde plc

Air Liquide

Messer SE & Co. KGaA

Air Products and Chemicals, Inc

Taiyo Nippon Sanso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: American Welding & Gas has acquired Grant Hagberg Co., an Indiana-based distributor specializing in bulk and cylinder carbon dioxide, as well as dry ice. Grant Hagberg, located in Indiana, also offers hydrotesting services and fire extinguishers. This acquisition is set to bolster and enhance American Welding & Gas's operations in gas and welding supplies throughout the Midwest.

- January 2024: Linde plc had expanded its long-term agreement with Steel Authority of India Limited to enhance industrial gas supply, including oxygen and nitrogen. This expansion supported steel production efficiency and sustainability while strengthening Linde’s footprint in India’s metals and manufacturing sector. The increased gas supply has boosted shielding gas availability, crucial for welding operations, driving growth in the Shielding Gas for Welding Market across India’s industrial sector.

Global Shielding Gas For Welding Market Report Scope

Shielding gas for welding is a protective gas used during arc welding to prevent atmospheric contamination of the molten weld pool. Common shielding gases include argon, carbon dioxide, helium, and mixtures, which stabilize the arc, improve weld quality, and reduce defects. They are essential in processes like MIG, TIG, and flux-cored welding, ensuring strong, clean, and consistent welds across industries.

The Shielding Gas for Welding Market is segmented by gas type, welding process, application, and geography. By Gas Type, the market is segmented into argon, carbon dioxide, helium, hydrogen, oxygen, nitrogen, mixture gases, and other types. By Welding Process, the market is segmented into MIG (metal inert gas), MAG (metal active gas), TIG (tungsten inert gas), FCAW (flux cored arc welding), plasma arc welding, and other welding processes (laser, sub arc, EBW). By Application, the market is segmented into automotive and transportation, shipbuilding, construction and infrastructure, aerospace and defense, machinery and equipment manufacturing, energy and power, heavy fabrication and metalworking, and other applications (rail, pipeline, repair). The report also covers the market size and forecasts for the Global Shielding Gas for Welding Market in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Argon |

| Carbon Dioxide |

| Helium |

| Hydrogen |

| Oxygen |

| Nitrogen |

| Mixture Gases |

| Other Types |

| MIG (Metal Inert Gas) |

| MAG (Metal Active Gas) |

| TIG (Tungsten Inert Gas) |

| FCAW (Flux-Cored Arc Welding) |

| Plasma Arc Welding |

| Other Welding Processes (Laser, Sub-Arc, EBW) |

| Automotive and Transportation |

| Shipbuilding |

| Construction and Infrastructure |

| Aerospace and Defense |

| Machinery and Equipment Mfg. |

| Energy and Power |

| Heavy Fabrication and Metalworking |

| Other Applications (Rail, Pipeline, Repair) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Gas Type | Argon | |

| Carbon Dioxide | ||

| Helium | ||

| Hydrogen | ||

| Oxygen | ||

| Nitrogen | ||

| Mixture Gases | ||

| Other Types | ||

| By Welding Process | MIG (Metal Inert Gas) | |

| MAG (Metal Active Gas) | ||

| TIG (Tungsten Inert Gas) | ||

| FCAW (Flux-Cored Arc Welding) | ||

| Plasma Arc Welding | ||

| Other Welding Processes (Laser, Sub-Arc, EBW) | ||

| By Applications | Automotive and Transportation | |

| Shipbuilding | ||

| Construction and Infrastructure | ||

| Aerospace and Defense | ||

| Machinery and Equipment Mfg. | ||

| Energy and Power | ||

| Heavy Fabrication and Metalworking | ||

| Other Applications (Rail, Pipeline, Repair) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the shielding gas for welding market?

The shielding gas for welding market stands at USD 6.46 billion in 2026 and is forecast to reach USD 8.31 billion by 2031 at a 5.18% CAGR from 2026 to 2031.

Why is argon the leading shielding gas?

Argon commanded 45.01% share in 2025 because it is inert, widely compatible with MIG and TIG processes, and readily available from ASUs.

Which segment is growing fastest?

Hydrogen-based blends show the highest 5.75% CAGR to 2031 as WAAM users seek deeper penetration and lower porosity in reactive alloys.

How are suppliers tackling price volatility?

Major players bundle managed-gas services with digital flow monitoring, bulk storage, and multi-year contracts to shield customers from spot-pricing swings.

Page last updated on: