Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

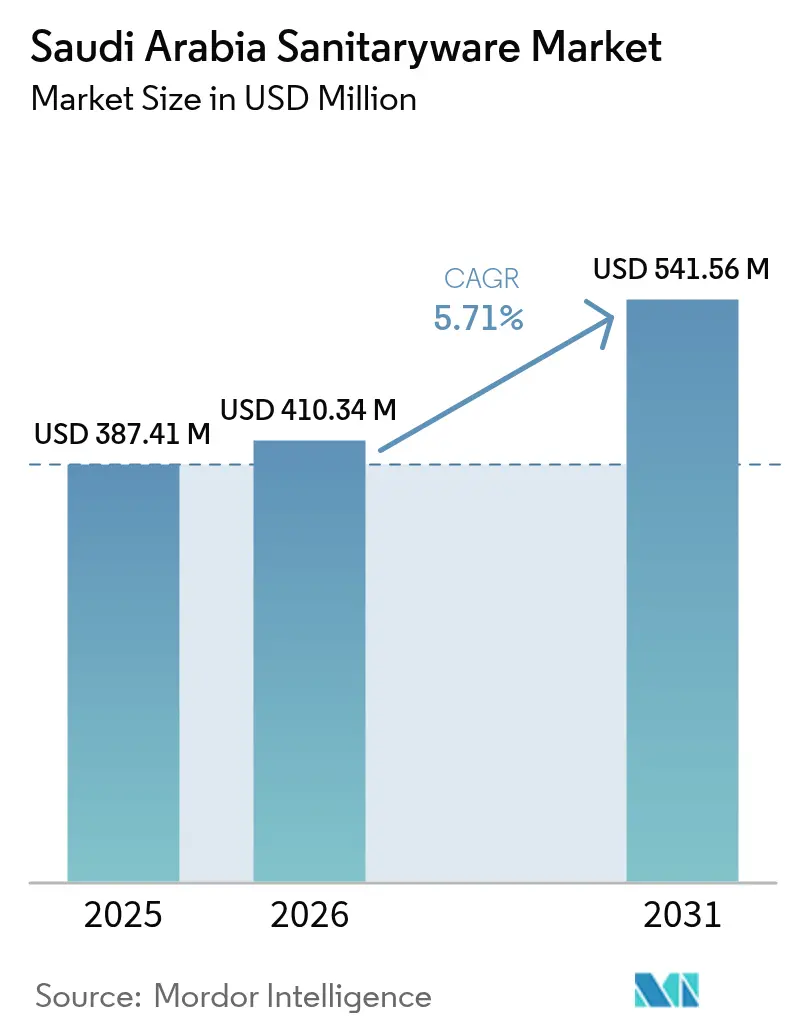

| Base Year Market Size (2025) | USD 387.41 Million |

| Market Size (2026) | USD 410.34 Million |

| Market Size (2031) | USD 541.56 Million |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

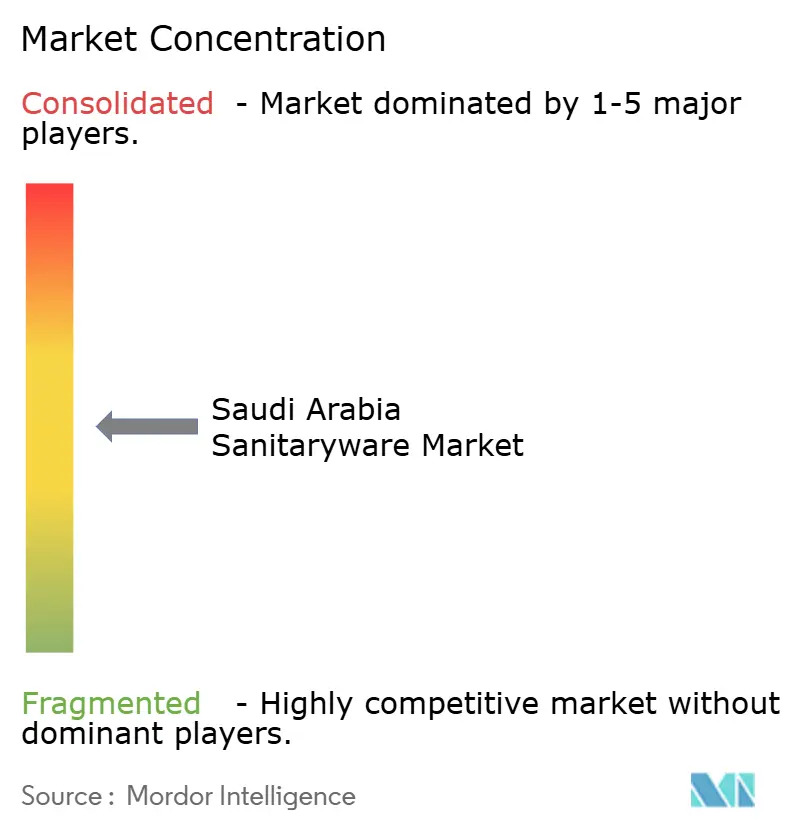

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Sanitaryware Market Analysis by Mordor Intelligence

The Saudi Arabia sanitaryware market size was USD 387.41 million in 2025, USD 410.34 million in 2026, and is forecast to reach USD 541.56 million by 2031, at a 5.71% CAGR over 2026-2031. Growth in 2026 is anchored in the Vision 2030 housing push, large-scale giga-projects, and policy-led localization that lifts in-Kingdom assembly for critical components, which together compress lead times and stabilize project schedule[1] Saudi Vision 2030, “Vision 2030 Overview,” Vision 2030, vision2030.gov.sa. Residential tailwinds remain firm as homeownership rose to 65.4% by end-2024 and public-private pipelines such as ROSHN translate reservations into completions that require full bathroom fit-outs. Structural hospitality demand is reinforced by more than 94,500 rooms under construction and an ambition to reach 358,000 rooms by 2030, reinforcing multi-year procurement of toilets, cisterns, basins, and touchless fixtures for back-of-house and guest suites[2]HospitalityNet Newsroom, “Saudi Arabia Hotel Pipeline,” HospitalityNet, hospitalitynet.org. Water stewardship regulations, including the SASO Water Efficiency Label and GCC-harmonized GSO-WER, continue to influence product mix in favor of dual-flush, low-flow, and concealed systems that meet minimum performance thresholds while reducing consumption. Incremental demand tied to the Pilgrim Experience Program, which drew 18.5 million visitors in 2024 and targets 30 million Umrah pilgrims by 2030, prioritizes heavy-duty sanitaryware upgrades in Mecca and Medina facilities.

Key Report Takeaways

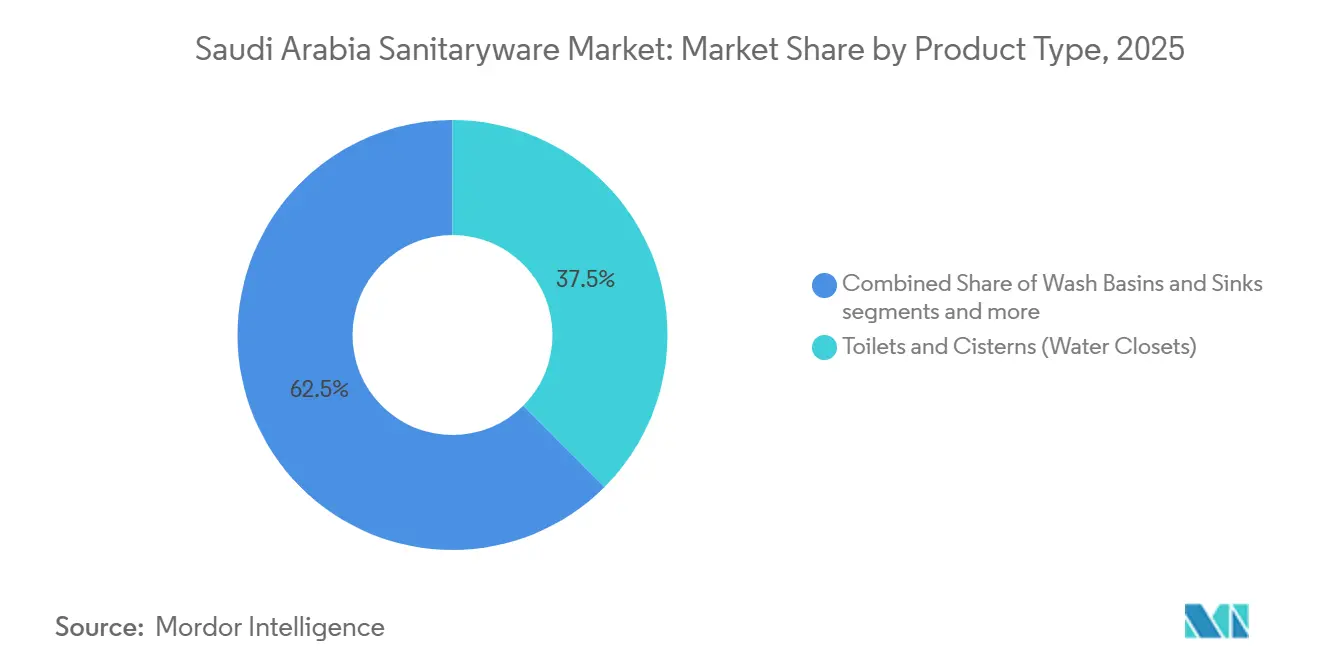

- By product type, toilets and cisterns led with 37.51% share of the Saudi Arabia sanitaryware market in 2025. Wash basins and sinks are projected to grow at a 6.73% CAGR through 2031 in the Saudi Arabia sanitaryware market.

- By material, ceramic held 78.42% share of the Saudi Arabia sanitaryware market in 2025. Solid-surface and composite materials are forecast to expand at a 7.87% CAGR through 2031 in the Saudi Arabia sanitaryware market.

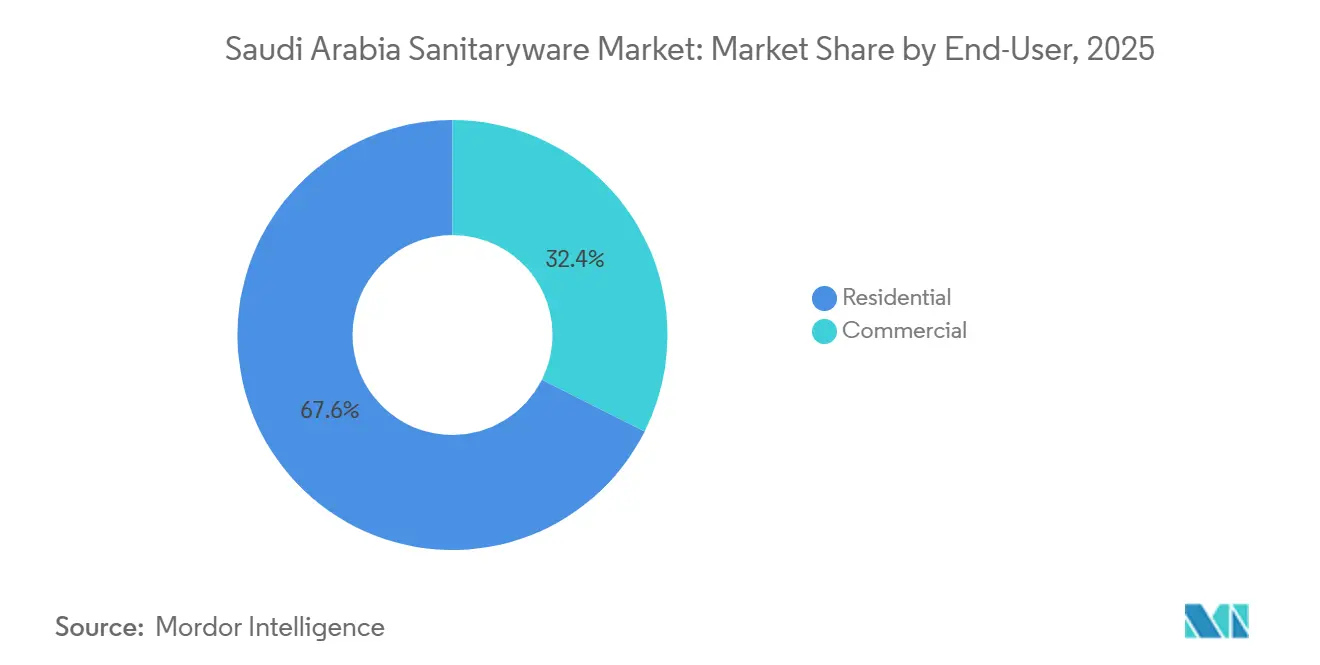

- By end-use, residential accounted for 67.64% of the Saudi Arabia sanitaryware market in 2025. The commercial segment is set to advance at a 7.14% CAGR through 2031 in the Saudi Arabia sanitaryware market.

- By distribution channel, B2C/retail captured 46.76% share of the Saudi Arabia sanitaryware market in 2025. B2B project sales are expected to grow at a 7.01% CAGR through 2031 in the Saudi Arabia sanitaryware market.

- By geography, the Central Region held 34.12% share of the Saudi Arabia sanitaryware market in 2025. The Western Region is poised to grow at a 7.23% CAGR through 2031 in the Saudi Arabia sanitaryware market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Sanitaryware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Housing Push Lifts Residential Installations | + 1.8% | National, concentrated in the Central and Western Regions | Medium term (2-4 years) |

| Hospitality Pipeline Expansion Accelerates Project Demand | + 1.3% | Western Region, Central Region | Medium term (2-4 years) |

| Giga-Projects and Mixed-Use Megadevelopments Sustain Multi-Year Fit-Out Cycles | + 1.4% | National, early gains in Central, Western, Northern | Long term (≥ 4 years) |

| Mandatory SASO Water Efficiency Label Drives Compliant Upgrades and Product Mix Shift | + 0.6% | National | Short term (≤ 2 years) |

| Pilgrim Experience Program Upgrades Facilities in Holy Cities, Boosting Heavy-Duty Sanitaryware | + 0.9% | Western Region | Short term (≤ 2 years) |

| Local Manufacturing/Local-Content Tie-Ups De-Risk Supply and Spur Adoption | + 0.7% | National, early adopters in Central and Eastern Regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Housing Push Lifts Residential Installations

Policy-led housing expansion is the single strongest structural tailwind for the Saudi Arabia sanitaryware market, contingent on sustained mortgage availability, land release, and developer execution pipelines. Homeownership reached 65.4% by the end of 2024, and flagship initiatives such as ROSHN’s large-scale communities translate booked demand into bathroom fit-outs across townhouses and apartments that standardize mid-range, SASO-compliant ceramic suites. The scale of these procurements supports multi-year, fixed-price supply agreements that reduce unit volatility but raise specification discipline, since non-compliant imports risk penalties and rework under SABER enforcement. Developers increasingly pre-qualify suppliers based on documented conformity, local inventory depth, and site support, which favors brands with Saudi legal entities, service teams, and strong relationships with MEP contractors. The near-term opportunity clusters around concealed-cistern compatible wall systems and dual-flush toilets, since verified water-efficiency performance has become a baseline requirement for project approvals. A complementary, underserved pocket of demand is municipal and social-housing retrofits in secondary cities, where high per-capita water use incentivizes upgrades to water-saving fixtures in public facilities[3]Saudi Water Authority, “Water Strategy Annual Report 2025,” swa.gov.sa.

Hospitality Pipeline Expansion Accelerates Project Demand

Saudi Arabia’s pipeline to reach 358,000 hotel rooms by 2030 and the 94,500 rooms currently under construction sustain a predictable cadence of sanitaryware procurement for guest rooms, public areas, and staff facilities, especially in Mecca, Medina, and the Red Sea coast. Hospitality operators favor wall-hung toilets with concealed cisterns, dual-flush actuators, and touchless faucets to improve housekeeping efficiency and reduce operating costs, a shift that directly benefits brands positioned in in-wall systems and high-performance flush technology. The Red Sea Project’s environmental rigor requires desalination-compatible fittings and greywater-ready plumbing, which opens a niche for corrosion-resistant composite basins and premium valve assemblies designed for saline environments. As operators scale pre-openings and back-of-house commissioning, the procurement model rewards vendors with rapid replacement logistics and on-site training, characteristics that tilt selection toward local entities and joint ventures. Seasonal load peaks tied to Ramadan and the Hajj period also cause spares pre-positioning in Mecca and Medina, a logistics staple that suppliers with regional warehouses can serve more reliably than long-haul importers. These conditions collectively reinforce a project-led, specification-driven demand cycle that favors proven system compatibility, SASO label compliance, and established after-sales support

Giga-Projects and Mixed-Use Megadevelopments Sustain Multi-Year Fit-Out Cycles

Vision 2030 giga-projects, including NEOM, the Red Sea Project, Qiddiya, and New Murabba, anchor long-duration sanitaryware demand that extends well beyond 2031 as developments transition from core infrastructure to interior fit-outs. Large packages move from design to execution in phases, and master developers increasingly embed modular bathroom pods into tender documents to compress timelines and lower on-site labor exposure. Vendors that align with modular workflows by coordinating with pod fabricators, standardizing SKUs, and staging just-in-time deliveries gain specification resilience across towers and districts. Local-content clauses in Public Investment Fund tenders steer buyers toward manufacturers with in-Kingdom assembly or joint ventures, a structure that global brands replicate by localizing cisterns and actuators while importing precision cartridges and sensors under permitted channels. This procurement architecture solidifies the Saudi Arabia sanitaryware market’s pivot from pure import distribution to hybrid models that blend local assembly and targeted imports for specialized components. Over the medium term, this mix should stabilize lead times, limit currency exposure for project buyers, and reduce conformity friction at customs checkpoints.

Mandatory SASO Water Efficiency Label Drives Compliant Upgrades and Product Mix Shift

The SASO Water Efficiency Label applies to faucets, showers, toilets, urinals, and cisterns, and its GCC-harmonized GSO-WER rules in effect since 2024 reinforce minimum performance standards that shape product selection in both residential and non-residential projects. Dual-flush performance thresholds, typically 3 liters for reduced flush and 6 liters for full flush, inform bowl geometry, trapway design, and jet configuration to sustain cleanliness at lower volumes without increasing clog risk. Product innovation tracks these requirements, as seen in premium shower toilets and efficient in-wall systems that reduce paper use and support low-volume flush without compromising user experience. Compliance reshapes importer economics too, since lab testing and certification per SKU introduce fixed costs that small-volume traders struggle to amortize across shipments. Pre-shipment and shipment certificates, along with periodic audits, also create time-to-market considerations that reward planning and documentation discipline, especially for SKUs with multiple flow-rate options. While retrofits lag new-build adoption due to wall cavity and drainage constraints in legacy buildings, tightening building-performance policies can unlock a broader replacement cycle for compliant concealed systems over the forecast horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Conformity Assessment (SABER/SALEEM) and WEL Testing Add Cost/Time-to-Market for Imports | -0.5% | National, heavier burden on smaller importers | Short term (≤ 2 years) |

| Intense Price Competition from Import-Heavy, Fragmented Supply Squeezes Margins | -0.7% | National, most acute in mid-tier residential | Medium term (2–4 years) |

| Stringent Water-Flow/Flush Caps Constrain Design Choices and Retrofit Performance in Legacy Buildings | -0.4% | National, concentrated in Central and Western urban centers | Long term (≥ 4 years) |

| Local-Content Weighting in Public Tenders can Disadvantage Non-Localized Brands | -0.3% | National, primarily affecting PIF mega-projects | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Conformity Assessment and WEL Testing Add Cost and Time to Market for Imports

Importers must obtain SABER product and shipment certificates and fund laboratory testing for covered SKUs, which raises entry costs and introduces lead-time risk for businesses with frequent design refreshes or small batch flows. End-to-end approvals can span several business weeks, and penalties for non-compliance elevate the incentive to front-load documentation and vendor pre-qualification. Smaller exporters without robust quality systems encounter audit hurdles more often, which delays containers at major Saudi ports and complicates just-in-time delivery promises. TÜV Rheinland’s SALEEM pre-shipment inspection framework adds another layer of procedural scrutiny and cost for new product lines before arrival in the Kingdom. Although GCC-level harmonization through GSO-WER sets a common baseline, Saudi Arabia retains its own SABER requirements, so importers must plan for country-specific certification even when selling compliant SKUs in neighboring markets. Collectively, the compliance framework favors established brands with scale, paperwork discipline, and local representation, while thinning opportunistic low-volume trading activity and slowing the influx of unverified innovations.

Intense Price Competition from Import-Heavy, Fragmented Supply Squeezes Margins

A delivered-price edge for Asian sanitaryware in the mid-tier residential segment keeps pressure on local manufacturers and distributors, which must counter through shorter lead times, service reliability, and project-driven specification support. Local producers cushion the gap with rapid regional dispatch, but this advantage compresses when developers lock orders months in advance for phased tower completions. With dozens of active distributors and no single player dominating share, competition often shifts to payment terms, training, and after-sales replacement inventory rather than unique product features. Project timing shifts have weighed on some global players’ Saudi results, even as they invest in local capacity to secure future local-content advantages. Energy-cost adjustments that affect kiln operations have triggered price renegotiations and incremental list-price changes during 2026 to preserve margin stability for committed deliveries. As a counterbalance, premium subcategories such as smart toilets, designer finishes, and compatible greywater systems carry higher price points and help distributors offset thinner margins on commodity white-ware lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dual-Sink Vanities and Heavy-Duty Fixtures Propel Basin Uptake

Toilets and cisterns accounted for 37.51% of the Saudi Arabia sanitaryware market share in 2025, reflecting their critical role across residential and commercial bathrooms where code-mandated fixtures cannot be value-engineered out of designs. Wash basins and sinks are set to grow at a 6.73% CAGR through 2031 as open-plan master suites, hospitality-grade double vanities, and coastal installations favor combinations of under-counter basins and wall-mounted faucets that simplify cleaning and resist mold in humid zones. Architects and MEP consultants have increased specifications for concealed systems and water-efficient basins in branded hotel projects and mid-rise clusters, where housekeeping speed and space optimization are important for operator economics. Wall-hung toilets with in-wall carriers support simplified floor cleaning and improve perceived hygiene, a configuration that has gained traction with hotel and office operators aligning with Mostadam certification norms. Urinals continue to serve mosques, office towers, and stadiums, with gradual penetration of waterless units as facility managers balance upfront device costs with maintenance and water bills. Standalone bidets maintain a presence in many homes, yet integrated bidet-toilet combinations are increasing due to space-saving layouts in new apartments, particularly where developers bundle bathroom upgrades as move-in options.

In higher-end villas and five-star hospitality, bathtubs and whirlpools remain niche by volume but central to positioning and guest experience, with acrylic models preferred for weight and installation practicality. Heavy-duty sanitaryware specified for pilgrimage facilities and high-traffic public venues prioritizes vandal resistance, reduced splash patterns, and fast-recovery flush systems to withstand peak usage. SASO water-efficiency labeling has standardized baseline performance and led to wider adoption of dual-flush actuators across project specifications, reinforcing consistency in procurement and installation training. Product bundles that integrate basins, mixers, and concealed carriers now win more project bids because they reduce cross-brand compatibility risks and streamline post-handover service protocols. As a result, category growth is less about a single SKU and more about complete bathroom systems that meet efficiency, hygiene, and maintenance expectations in the Saudi Arabia sanitaryware market.

By Material: Ceramic Dominance Persists, Yet Composites Carve a Niche in Harsh Climates

Ceramic remained the dominant material at 78.42% share in 2025, supported by large-scale capacity, sanitary performance, and proven durability in the temperature and utilization profiles common in Saudi projects. The Saudi Arabia sanitaryware market size allocated to ceramic reflects the material’s non-porous finish that resists staining and simplifies cleaning in hospitals, schools, and public facilities where infection control and high turnover are priorities. Pressed metal retains relevance for budget-sensitive or temporary accommodations that require high impact resistance and low breakage risk, although its bathroom role is limited in premium residential settings. Acrylic and engineered plastics dominate bathtubs and shower trays due to light weight and ease of installation in towers, with thermoforming enabling ergonomic designs that appeal to wellness-focused buyers. Despite these advantages, acrylic’s susceptibility to long-term scratching and UV yellowing limits use in sun-exposed outdoor applications that are common in coastal resorts.

Solid-surface and composite materials are projected to grow at a 7.87% CAGR to 2031 as architects target seamless, mold-resistant vanity tops with integrated basins for coastal humidity and salt-laden air environments. These materials can be thermoformed to fit non-standard alcoves during renovations, an advantage in legacy buildings that lack modern modular dimensions. They also support sustainability objectives when feedstocks include post-industrial content, aligning with strict environmental criteria in flagship coastal developments. On-site fabrication flexibility and consistent surface finishes make composites attractive for premium hospitality, where brand standards require uniform aesthetics across hundreds of identical rooms. In turn, procurement teams seek suppliers that can document material performance under desalination and greywater conditions, tying adoption to lifecycle cost calculations rather than lowest upfront price. This dynamic maintains ceramic as the volume workhorse but opens room for higher-margin composite systems where design integration and environmental performance inform selection in the Saudi Arabia sanitaryware market.

By End-Use: Commercial Hospitality and Office Fit-Outs Accelerate Beyond a Large Residential Base

Residential installations represented 67.64% of volume in 2025, aligning with steady handovers in master-planned communities and mortgage-supported ownership that drives first-fit bathroom demand. Developers continue to standardize mid-range ceramic toilet-basin combinations to balance value and reliability, while offering solid-surface vanity upgrades in premium enclaves to attract dual-income households. Showroom networks that provide immediate stock and same-day replacement for contractor items are now core to purchase decisions, as buyers expect quick resolution of installation snags during handover. Retrofit cycles in legacy homes trail new-build demand due to wall cavity and drainage constraints that complicate concealed-cistern upgrades, pushing many households to defer changes until renovation triggers arise. As bankable pipelines stabilize, residential spending is becoming more disciplined around verified water efficiency, standardized in-wall carriers, and coordinated faucet-basin pairings that reduce service calls and warranty costs.

Commercial applications accounted for roughly a fifth of 2025 volume and are forecast to outpace residential through 2031, lifted by the room pipeline for hotels and the steady expansion of Grade A offices in Riyadh and Jeddah. Hotel guest rooms and back-of-house facilities specify low-flow, concealed systems and durable vitreous china to balance housekeeping efficiency with water stewardship expectations. Office towers increasingly adopt touchless sensor faucets and auto-flush urinals to meet Mostadam benchmarks and corporate ESG commitments, which expands demand for electronic actuators, valves, and compatible power solutions. Retail fit-outs emphasize finish variety and distinctive design for brand expression in premium malls, sustaining price premiums over standard chrome as operators invest in guest experience. Institutional settings such as clinics and schools prioritize antimicrobial surfaces and high-durability devices, reinforcing specification discipline and narrowing the eligible vendor pool to those with documented conformity and training programs.

By Distribution Channel: B2B Project Sales Overtake Retail as Giga-Developments Bulk-Buy

B2C retail captured 46.76% share in 2025, spanning multi-brand home improvement stores, brand-exclusive showrooms, and a modest but growing online channel with augmented-reality visualization tools. Showroom-led sales deliver higher per-piece revenue because they bundle installation, extended warranties, and responsive after-sales service that homeowners value in high-touch categories. While online sales are growing, breakage risk in shipping, last-mile complexities in remote areas, and a tendency for buyers to inspect glaze finishes and ergonomics in person keep digital penetration below broader home categories. Retail momentum remains strongest in large cities with frequent handovers from master developers, where coordinated showroom clusters allow easy cross-comparison and immediate pickup. As stock turns become more predictable, retailers curate assortments around SASO-labeled SKUs and concealment-compatible formats to align with building approvals and contractor preferences.

B2B project channels held 53.24% share in 2025 and are projected to grow faster than retail through 2031, propelled by giga-project fit-outs and Public Investment Fund tenders that embed 30% local-content requirements into awards. Developers structure direct-import programs for container-scale orders of standardized SKUs, moving volume via bonded warehouses and staged deliveries tied to tower sections. Suppliers with in-Kingdom assembly or manufacturing gain scoring advantages in bids, which steers procurement toward brands that localized cisterns and carriers in Dammam and Riyadh facilities. Turnkey fit-out contractors emphasize SABER conformity speed, site training capability, and rapid replacement logistics in vendor selection to protect interior schedules. This discipline gradually reduces pure price-based awards and replaces them with total-cost-of-delivery considerations that align with on-time handovers and reduced snag lists in the Saudi Arabia sanitaryware industry.

Geography Analysis

The Central Region led with 34.12% share in 2025, benefiting from concentrated government investment, New Murabba’s downtown expansion, and the RHQ mandate that moved more than 700 corporate headquarters to Riyadh, each requiring premium office fit-outs. New Murabba’s plan includes 104,000 residential units, 9,000 hotel keys, and significant retail space by 2030, which together sustain multi-year interior demand beyond shell-and-core work. Large master-planned communities around Riyadh continue to translate reservations into handovers, with developers standardizing on dual-flush toilets, concealed cisterns, and coordinated faucet-basin sets that enable faster cleaning and reduced water use. SASO enforcement teams in Central Region municipalities scrutinize installed fixtures prior to occupancy, which effectively pushes out non-compliant imports and advantages suppliers with audited conformity and local stock. As a result, the Central Region remains the most specification-driven hub of the Saudi Arabia sanitaryware market, where premium showrooms, trained installers, and rapid spares availability influence vendor selection for both residential and office towers.

The Western Region held 28% share in 2025 and is projected to grow fastest at a 7.23% CAGR through 2031, paced by the Red Sea Project’s 50-hotel plan, Jabal Omar’s mixed-use expansion near the Grand Mosque, and the Pilgrim Experience Program’s capacity goals. Mecca and Medina hotel clusters emphasize heavy-duty, vandal-resistant sanitaryware to withstand intensive pilgrimage-season turnover and frequent high-pressure cleaning. Jeddah’s coastal redevelopment increases use of desalination-compatible fittings and corrosion-resistant vanity solutions, with architects favoring composite basins in premium hospitality to mitigate salt exposure over time. Municipal procurement in holy cities continues to mandate SABER-certified WEL-compliant fixtures for ablution retrofits, accelerating replacement of older models that do not meet current dual-flush standards. Distribution in the Western Region now includes pre-positioned spares during Ramadan and Hajj, anchoring a service-led advantage for suppliers that can meet same-day replacement targets for critical components.

The Eastern Region accounted for 21% share in 2025, anchored by industrial-city expansion, contractor housing, and office developments clustered around Dammam, Khobar, Dhahran, and Jubail. Localized cistern production in Dammam shortens lead times from weeks to hours, which supports tight commissioning windows in petrochemical and energy projects with 24-hour replacement guarantees. Jubail’s industrial complexes and SPARK favor stainless-steel sinks and high-durability vitreous china in dormitories and administrative blocks, with maintenance contracts emphasizing fast response and standardized spares. Northern and Southern regions together formed a smaller base in 2025 but continue to benefit from border-infrastructure expansion and targeted tourism initiatives, which reinforces gradual adoption of compliant fixtures and higher hygiene standards in public facilities. Across all regions, the enforcement of water-efficiency labeling and project tender rules produces a consistent national baseline that enables vendors to coordinate standardized product families and training programs in the Saudi Arabia sanitaryware market

Competitive Landscape

Saudi Ceramic Company leverages large-scale kiln capacity in Riyadh and a national showroom network to support mega-projects and master-planned communities with fixed-price, multi-year agreements that prioritize on-time delivery and immediate spares. Ceramics continues to position for local-content advantages through a greenfield plant in Yanbu scheduled for Q1 2027, a shift designed to shorten lead times and align with tender scoring that benefits localized production. Geberit deepened its project footprint via an MoU with ROSHN in November 2025 that includes co-developing water-efficient shower toilets and creating a contractor training academy in Riyadh, which embeds its specifications in large-scale residential pipelines achieved first-mover status in localized cistern manufacturing with a Dammam facility that underpins shorter delivery windows and robust after-sales support for project clients.

Price competition remains sharp in mid-tier residential, where imports offer a delivered-price edge and local players respond with speed, service, and specification resilience at large project sites. Project timing affected some multinationals’ Saudi revenue trajectories in 2025, but management teams maintained forward investment in in-Kingdom capacity to secure future tender advantages and de-risk supply. Energy-cost updates affecting kiln operations prompted Saudi manufacturers to adjust pricing guidance in early 2026 and revisit the economics of long-duration supply agreements with mega-projects. In parallel, premium subcategories such as touchless faucets, designer finishes, and smart toilets command strong price points, which distributors use to offset margin pressure on commodity ceramics. The spread of touchless technologies in Grade A offices and five-star hotels is set to continue as Mostadam targets and corporate ESG frameworks prioritize water and hygiene outcomes in building operations.

White-space remains in three areas already visible in 2026 project briefs. Modular bathroom pod integration at giga-projects rewards suppliers who align factory lines with pod fabricators and harmonize SKUs for just-in-time drops to site. Retrofit-ready low-flow kits that can be installed without wall demolition or drainage redesign would address vast legacy stock but require engineered solutions that maintain flush performance within existing bowl geometries. Greywater-compatible plumbing systems will likely gain traction once standardized inspection protocols are updated, enabling broader commercialization for concept-proven configurations. Given SASO’s compliance rules and local-content scoring in PIF tenders, early localizers with training programs, spares coverage, and documentation discipline remain structurally advantaged in the Saudi Arabia sanitaryware market.

Saudi Arabia Sanitaryware Industry Leaders

Saudi Ceramic Company (SCC)

RAK Ceramics (KSA)

Roca Group

Duravit AG

VitrA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Geberit signed an MoU with ROSHN to co-develop water-efficient shower toilets, establish a contractor training academy in Riyadh, and secure preferred-supplier status across the developer’s large pipeline

- November 2025: RAK Ceramics showcased SASO-compliant vitreous-china collections at Saudi Build 2025 in Riyadh and briefed contractors on Yanbu plant progress to support local-content strategies

- June 2025: Geberit introduced AquaClean shower toilets in Saudi Arabia, featuring integrated air-drying, adjustable spray patterns, and an average flush volume reported at 2.5 liters.

- September 2024: GROHE inaugurated a 26,000-square-meter Dammam manufacturing facility with Zamil Plastic Industries, establishing local production of concealed cisterns and employing a new in-Kingdom workforce.

Saudi Arabia Sanitaryware Market Report Scope

Sanitary ware, also known as plumbing ware, is a term used to describe plumbing fixtures, fittings, and other plumbing-related products used in bathrooms and kitchens. The purpose of sanitary ware products is to create a sanitary and visually appealing environment for users.

The Saudi Arabian sanitary ware market is segmented by product, material, distribution channel, and end user. By product, the market is segmented into water closets, wash basins, pedestals, cisterns, and other product types (bathtubs, showers, bidets, etc). By material, the market is segmented into ceramics, metal, plastic, and other materials (porcelain, etc). By distribution channel, the market is segmented into home centers, specialty stores, online, and other distribution channels (dealer franchisees, etc.), and by end user, the market is segmented into residential and commercial.

By Product Type

| Toilets & Cisterns (Water Closets) |

| Wash Basins & Sinks (incl. Pedestal Basins) |

| Bathtubs & Whirlpool Tubs |

| Urinals |

| Bidets |

| Other Products (soap trays, dispensers, etc.) |

By Material

| Ceramic |

| Pressed Metal |

| Acrylic & Plastics |

| Solid Surface & Composite |

By End-Use

| Residential |

| Commercial |

By Distribution Channel

| B2C / Retail | Multi-brand Stores |

| Exclusive Stores | |

| Online | |

| B2B / Project |

By Geography

| Central Region |

| Western Region |

| Eastern Region |

| Northern Region |

| Southern Region |

| By Product Type | Toilets & Cisterns (Water Closets) | |

| Wash Basins & Sinks (incl. Pedestal Basins) | ||

| Bathtubs & Whirlpool Tubs | ||

| Urinals | ||

| Bidets | ||

| Other Products (soap trays, dispensers, etc.) | ||

| By Material | Ceramic | |

| Pressed Metal | ||

| Acrylic & Plastics | ||

| Solid Surface & Composite | ||

| By End-Use | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail | Multi-brand Stores |

| Exclusive Stores | ||

| Online | ||

| B2B / Project | ||

| By Geography | Central Region | |

| Western Region | ||

| Eastern Region | ||

| Northern Region | ||

| Southern Region | ||

Key Questions Answered in the Report

What is the growth outlook for sanitaryware in Saudi Arabia through 2031?

The Saudi Arabia sanitaryware market is projected to rise from USD 387.41 million in 2025 to USD 541.56 million by 2031, at a 5.71% CAGR over 2026-2031.

Which factors are driving new project demand across the country?

Vision 2030 housing, giga-project fit-outs, a large hotel room pipeline, and SASO Water Efficiency Label enforcement are the primary growth drivers for multi-year sanitaryware procurement.

Which product categories are set to grow fastest in the next five years?

Wash basins and sinks are projected to expand at a 6.73% CAGR through 2031 as dual-sink vanities and open-plan suites gain traction, particularly in residential clusters and branded hotels.

How is regulation shaping product selection for new builds and retrofits?

SASO’s Water Efficiency Label and GCC-harmonized GSO-WER constraints drive selection toward dual-flush toilets, low-flow fittings, and concealed cistern systems that achieve mandated performance thresholds.

What regional markets inside the Kingdom will likely grow the fastest?

The Western Region is poised to grow fastest through 2031 due to Red Sea resorts, Mecca and Medina hospitality, and pilgrimage-related upgrades, while the Central Region remains the largest by share.

Page last updated on: