Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

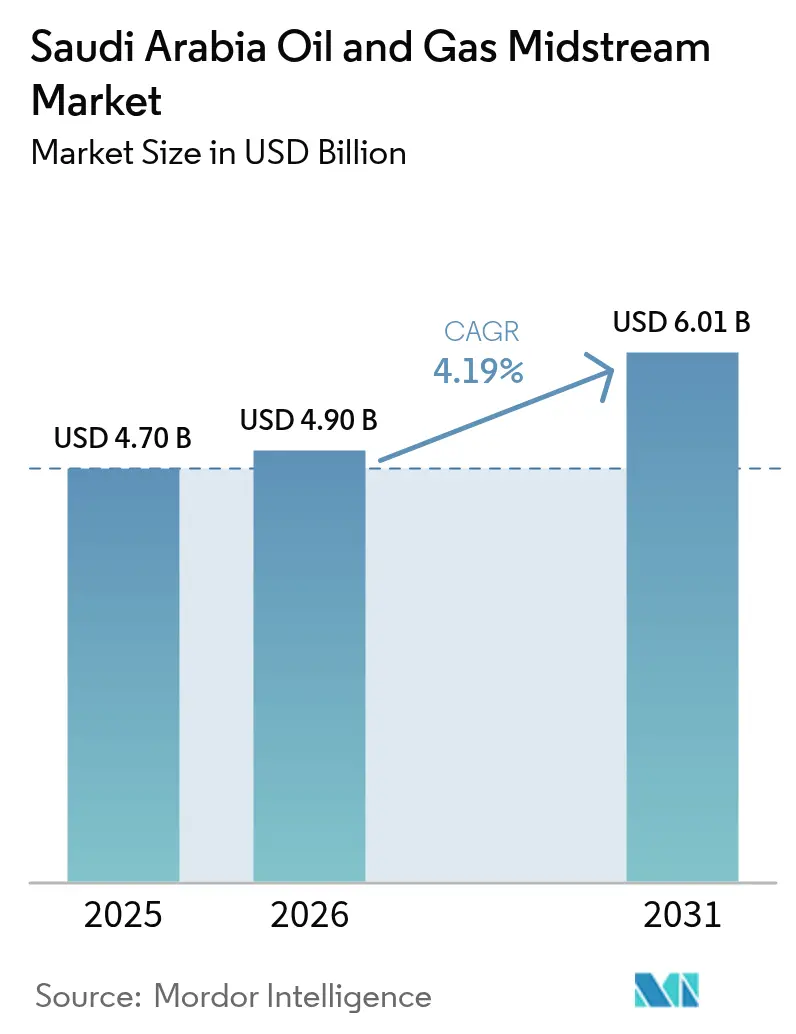

| Base Year Market Size (2025) | USD 4.70 Billion |

| Market Size (2026) | USD 4.9 Billion |

| Market Size (2031) | USD 6.01 Billion |

| Growth Rate (2026 - 2031) | 4.19% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Oil And Gas Midstream Market Analysis by Mordor Intelligence

Saudi Arabia Oil And Gas Midstream Market size in 2026 is estimated at USD 4.9 billion, growing from 2025 value of USD 4.70 billion with 2031 projections showing USD 6.01 billion, growing at 4.19% CAGR over 2026-2031.

Growth reflects the Kingdom’s drive to build a resilient energy value chain under Vision 2030, where new pipeline grids, storage caverns, and export terminals knit upstream resources to expanding refinery and petrochemical hubs. The Saudi Arabia oil and gas midstream market benefits from Saudi Aramco’s USD 25 billion Jafurah shale program, which alone requires 1,500 km of additional gathering and transmission lines for 2.2 trillion cubic feet (Tcf) of recoverable gas. Master Gas System Phase 3 adds 3,000 km of domestic capacity, relieving existing pipelines that are currently running at 85% utilization. Meanwhile, digital-twin rollouts across 2,000 km of critical assets reduce unplanned downtime by 25% and extend inspection intervals. Foreign joint ventures inject USD 15 billion in capital and high-pressure design know-how, helping operators fast-track blue-hydrogen corridors and carbon-capture trunk lines that align with the Saudi Green Initiative.

Key Report Takeaways

- By infrastructure, pipelines led with 57.20% share in 2025 and are projected to post the fastest 6.48% CAGR through 2031, reflecting 3,000 km of new lines tied to Master Gas System Phase 3.

- By product type, crude oil maintained a 51.80% share of the Saudi Arabia oil and gas midstream market size in 2025, whereas LNG is poised for the highest 7.86% CAGR, driven by the Fadhili Gas Plant expansion.

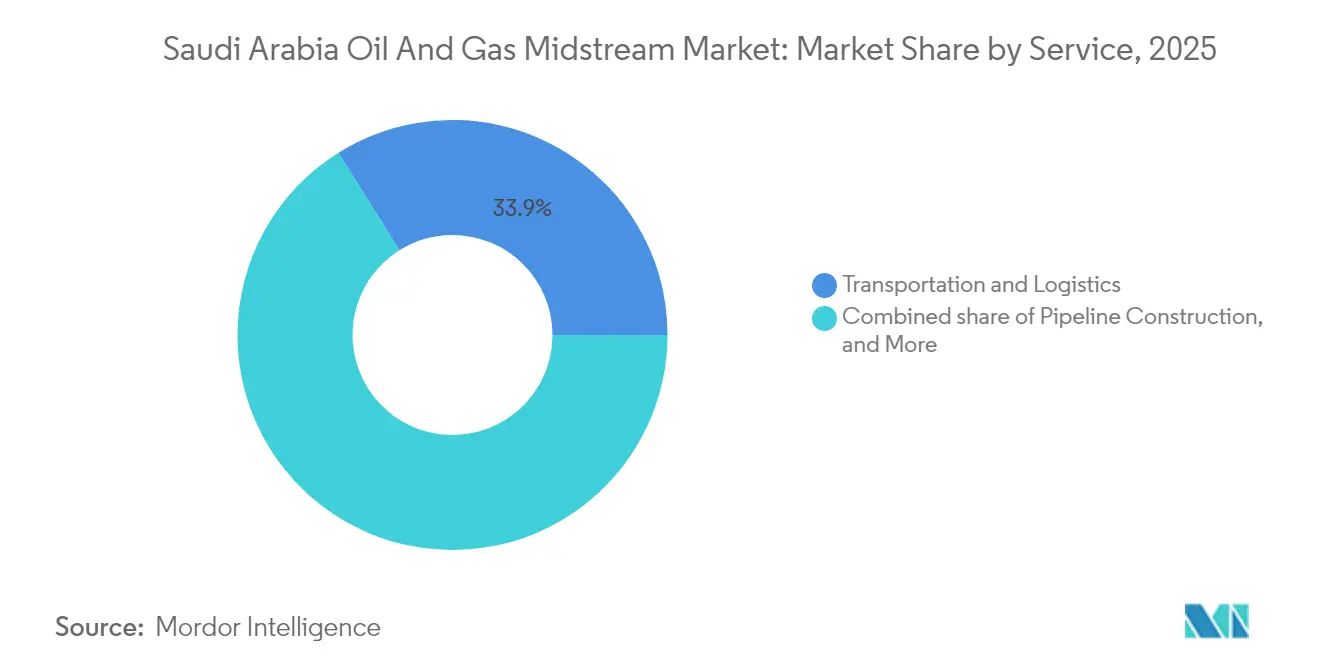

- By service type, transportation and logistics accounted for a 33.90% share in 2025; pipeline construction services delivered the quickest 7.06% CAGR as Jafurah and Amiral projects accelerated build-outs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Oil And Gas Midstream Market Trends and Insights

Drivers Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pipeline utilization for crude, products & gas | +1.20% | Eastern Province and national network | Medium term (2-4 years) |

| Growing domestic gas production & demand | +0.90% | Industrial regions nationwide | Long term (≥ 4 years) |

| Vision 2030 downstream diversification push | +0.80% | NEOM, Jubail, Yanbu | Long term (≥ 4 years) |

| Foreign JV capital inflows for midstream projects | +0.60% | Strategic energy hubs | Medium term (2-4 years) |

| Digital-twin adoption to optimize pipeline integrity | +0.40% | Critical corridors | Short term (≤ 2 years) |

| Planned blue-hydrogen export corridors | +0.30% | Coastal zones & NEOM | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pipeline Utilization for Crude, Products & Gas

The East-West crude link—rated at 5 MMb/d—operated at nameplate levels throughout 2024, while the Master Gas System carried 12 Bcf/d and brushed against design limits.(1)Saudi Arabian Oil Co., “Master Gas System Expansion Updates,” aramco.com Higher refinery runs at Jazan and Jubail, plus new export berths, compound throughput pressure, and drive immediate debottlenecking plans. Fiber-optic sensing and AI-driven hydraulic modeling squeeze incremental capacity from legacy lines, delaying capex-intensive twinning for two to three years. Yet redundancy mandates mean parallel crude lines must still break ground by 2026 to uphold export reliability targets. Over the medium term, the Saudi Arabia oil and gas midstream market will continue to prioritize flow efficiency gains until new steel enters the ground.

Growing Domestic Gas Production & Demand

Jafurah’s unconventional gas is slated to hit 2.2 Bcf/d by 2030 and demands 1,500 km of bespoke gathering, dehydration, and transmission assets engineered for high-H₂S content. Downstream pull comes from ammonia, steel, and power plants switching to cleaner fuels, with the National Industrial Development and Logistics Program serving as the underwriting anchor offtake. Compression ratios and pipe metallurgy specifications exceed conventional norms, raising unit costs 15% yet extending lifecycle integrity. Integrated gas-processing trains complicate maintenance windows, so operators adopt dynamic line-pack modeling to buffer seasonal swings. Coupled with gas-to-liquids pilots, these factors solidify long-term throughput commitments that support the Saudi Arabia oil and gas midstream market.

Vision 2030 Downstream Diversification Push

NEOM’s USD 8.4 billion hydrogen platform requires cryogenic pipelines, export jetties, and safety-rated valves able to contain dense-phase H₂.(2)NEOM, “Hydrogen Project Factsheet,” neom.com Simultaneously, petrochemical build-outs at Jubail and Yanbu need ethylene and propylene corridors linking crackers to polymer units, enlarging the Saudi Arabia oil and gas midstream market footprint beyond crude. Carbon-capture provisions layer CO₂ trunk lines on top of existing rights-of-way, generating economies of scope. Shared utility corridors bundle pipes, power cables, and water mains, cutting trenching costs by 20% and encouraging modular expansion. The integrated master-planning ethos thus locks midstream assets into every industrial mega-site conceived under Vision 2030.

Foreign JV Capital Inflows for Midstream Projects

TotalEnergies’ USD 11 billion commitment to the Amiral complex includes 150 km of olefin pipelines, as well as refrigerated storage caverns. Partnerships with Shell and Chevron add liquefaction and blue-hydrogen know-how, embedding high-pressure, H₂-ready steel grades into designs. Risk-sharing spreads capex and accelerates final investment decisions, trimming typical pipeline schedules from seven to four years. JV agreements include performance-based clauses that reward leak-free operations, encouraging the adoption of real-time corrosion maps. Collectively, outside capital elevates technical standards and broadens the Saudi Arabia oil and gas midstream industry talent pool.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental opposition to new pipelines | -0.80% | Ecologically sensitive corridors | Medium term (2-4 years) |

| Oil-price driven fiscal spending fluctuations | -0.60% | Kingdom-wide | Short term (≤ 2 years) |

| Limited domestic large-diameter pipe manufacturing base | -0.50% | Mega-project segments | Medium term (2-4 years) |

| Rising cyber-security risk to SCADA systems | -0.40% | Critical assets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental Opposition to New Pipelines

Updated statutes can fine violators up to USD 8 million and mandate extensive biodiversity offsets for routes slicing through mangroves or desert reserves.(3)Saudi Environmental Authority, “Pipeline Environmental Regulations 2025,” environment.gov.sa Impact-assessment cycles now span 24-36 months, stretching critical path schedules. Route deviations can inflate capital expenditures (capex) by 15-25%, especially when horizontal directional drilling replaces open-cut trenches. Operators incorporate drone-based wildlife surveys and remote leak-detection cameras to secure permits, raising baseline project budgets yet locking in best-practice benchmarks. In the Saudi Arabia oil and gas midstream market, ESG compliance moves from an optional differentiator to a license-to-operate requirement.

Oil-Price Driven Fiscal Spending Fluctuations

When Brent fell below USD 70/bbl in 2024, budget reallocations postponed non-essential pipeline phases, illustrating the link between hydrocarbon revenue and capital expenditure (capex) release.(4)Ministry of Finance, “Budget Review 2024,” mof.gov.sa Cabinet reviews now gate projects exceeding USD 1 billion, injecting six-month delays during price dips. Forward hedging and sovereign wealth financing blunt volatility, but line-pipe orders still decline when treasury inflows tighten. Contractors respond by adopting modular spreads and flexible workforce rosters. The cyclical fiscal rhythm continues to temper year-on-year growth within the Saudi Arabia oil and gas midstream market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure: Pipeline Networks Drive Expansion

Pipelines delivered 57.20% of 2025 revenue and are poised for the highest 6.48% CAGR, underscoring their centrality to the Saudi Arabia oil and gas midstream market. The Saudi Arabia oil and gas midstream market share for pipelines is expected to expand further as the 3,000 km Master Gas System Phase 3 and 800 km of Jafurah trunk lines come online by 2027. Advanced fiber-optic surveillance reduces unplanned outages by 30%, and domestic mills now account for 60% of line-pipe tonnage, thereby shaving logistics costs.

Terminals held a near-25.10% share in 2025, driven by the Ras Tanura debottlenecking and Yanbu export upgrades that align with twin-line crude flows. Storage facilities accounted for 17.70%, and the industry is pivoting toward underground salt caverns that even out shipping cycles and offer pressure-neutral hydrogen storage potential. Across all assets, digital twins replicate flow dynamics and corrosion rates, guiding predictive digs that stretch maintenance intervals. Collectively, these trends indicate that pipelines will continue to absorb the bulk of capital in the Saudi Arabia oil and gas midstream industry through 2031.

By Product Type: Crude Oil Dominance Faces LNG Challenge

Crude streams retained a 51.80% share in 2025, driven by the 5 MMb/d East-West system and dual-coast export jetties. LNG, driven by the Fadhili Plant, is expected to register an 7.86% CAGR and chip away at oil’s market share, adding multi-bore cryogenic pipelines to the Saudi Arabia oil and gas midstream market size calculus.

Natural gas lines, accounting for a 28.40% share, expand alongside power plants and petrochemical complexes, pivoting away from liquid fuels. Refined-product pipes account for 19.80%, serving inland bunkering depots and jet fuel loops to major airports. Batch scheduling software now maximizes interface cuts, letting single pipes shift between grades with minimal contamination. Looking ahead, the growth of gas and LNG aligns with Vision 2030’s cleaner fuel agenda, while crude oil remains a key anchor for safeguarding foreign exchange earnings.

By Service Type: Construction Surge Outpaces Operations

Transportation and logistics generated 33.90% of 2025 turnover and still represent the backbone of recurring revenue in the Saudi Arabia oil and gas midstream market. Nonetheless, pipeline construction services will achieve a brisk 7.06% CAGR through 2031, buoyed by USD 25 billion earmarked for Jafurah and the USD 11 billion Amiral complex.

Maintenance and repair accounted for roughly a 30.20% share, with digital corrosion coupons and inline inspection robots reducing the mean-time-to-repair by 18%. Storage and handling accounted for 35.90%, encompassing 2 million barrels of new Yanbu tanks completed in 2024. The service mix thus tilts toward greenfield EPC contracts in the short run, but as assets mature, steady-state O&M will reclaim prominence, ensuring balanced value creation across the Saudi Arabia oil and gas midstream industry.

Geography Analysis

Eastern Province, clustered around Dammam, Abqaiq, and Jubail, hosted 69.50% of active trunk lines and processing plants in 2025, translating into the largest slice of the Saudi Arabia oil and gas midstream market. Proximity to the Ghawar and Safaniyah fields, along with well-stocked industrial cities, confers 15-20% opex savings compared to standalone hubs.

Western Province, centered on Yanbu, commanded a 25.40% share, anchored by the East-West Pipeline terminus that feeds the Red Sea shipping lanes. Planned 10 MMt/y blue-ammonia export capacity and NEOM’s hydrogen grid will elevate the region’s Saudi Arabia oil and gas midstream market size in the late forecast horizon.

The Central Region currently holds a near-5.10% market share but exhibits outsized growth potential as Riyadh’s utility corridors extend gas supply to new economic cities. Cross-border links with GCC neighbors remain exploratory, yet they could diversify flows and mitigate single-route risk. The geographic mosaic highlights how twin-coast optionality enhances Saudi export resilience, while upcoming northern projects rebalance asset allocation.

Regulatory Landscape

Saudi Arabia oil and gas midstream activities operate under Ministry of Energy oversight through the Law of Energy Supplies, the Law on the Distribution of Dry Gas and Liquefied Petroleum, and the Law of Petroleum and Petrochemical Products (as maintained in the legislative repository). Across petroleum and petrochemical operations, licensing requirements cover transportation, storage, processing, and import/export, with e-services supporting electronic license issuance and administration.

In 2026, the Ministry of Energy expanded the scope and granularity of gas-network compliance through regulations for residential and commercial gas network activity, including requirements for consumer metering and submission of technical management and safety plans. Tender-based licensing is also being used to structure private participation in LPG filling, storage, and wholesale distribution, with the Ministry awarding eight licenses in June 2026 to named bidders (including UNIGAZ Arabia Company, a consortium of NGC Energy Saudi LLC and Zamil Group Holding Company, and Best Gas Carrier Company (Tazweed)), reinforcing a regulated, permit-led pathway for new midstream capacity additions.

Competitive Landscape

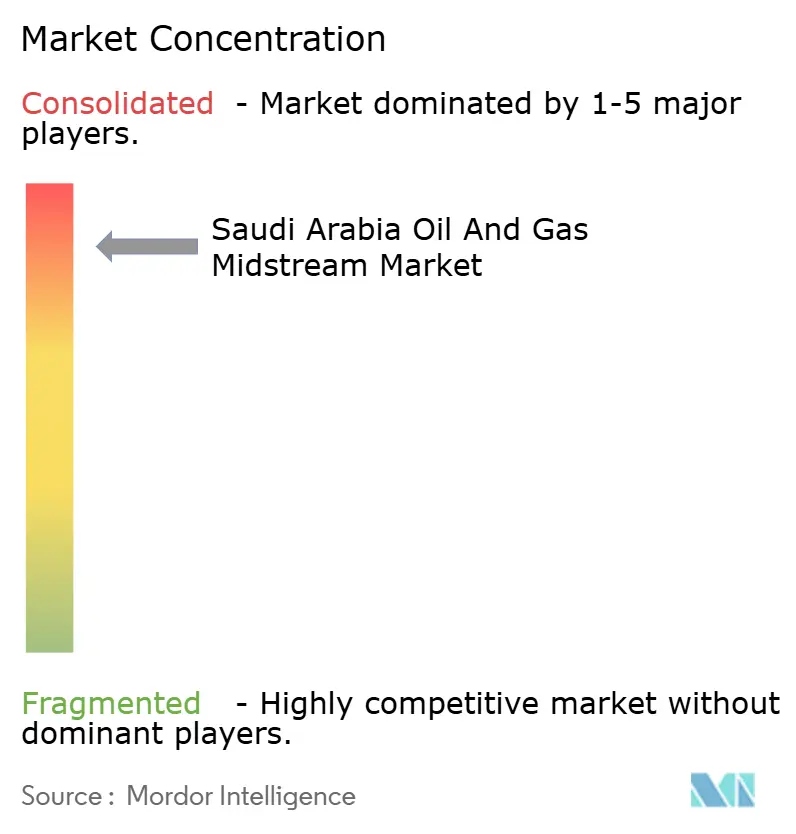

Saudi Aramco directly or via JVs controls roughly 80% of pipelines, terminals, and caverns, situating the Saudi Arabia oil and gas midstream market deep inside a high-concentration quadrant. Integration enables Aramco to synchronize upstream output with refinery crude slates, thereby smoothing throughput swings and maximizing system utilization.

International majors—TotalEnergies, Shell, and Chevron—enter through capital-heavy complexes that bundle pipelines with crackers or hydrogen plants. Their participation brings probabilistic risk-assessment tools and hydrogen-ready steel grades uncommon in legacy specifications, pushing the technology frontier. EPC leaders, such as McDermott Arabia and Saipem Saudi Arabia, leverage automated welding and trenchless drilling to win lump-sum turnkey awards, while East Pipes Integrated Company expands its domestic spool yards, thereby trimming import exposure.(6)TotalEnergies SE, “Amiral Petrochemical Complex Investment,” totalenergies.com

Digital capabilities now weigh as a decisive differentiator. Operators employing twin-model surveillance and AI leak prediction report 20-30% opex cuts and superior safety metrics, deepening barriers for late adopters. White-space niches in CO₂ trunk lines and high-purity H₂ distribution invite specialized entrants, though established incumbents retain regulatory goodwill and financing muscle, sustaining a tight competitive field.

Saudi Arabia Oil And Gas Midstream Industry Leaders

TotalEnergies SE

Medra Arabia

Chevron Corporation

Shell plc

Saudi Arabian Oil Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Unconventional gas and associated processing and transmission infrastructure remains a primary whitespace area, anchored by Saudi Aramco's Jafurah program and linked network expansions under the Master Gas System. Aramco's February 2026 start of operations at the Tanajib Gas Plant (targeting 2.6 billion standard cubic feet per day of raw gas processing capacity in 2026) provides a concrete throughput driver for gathering, compression, and trunkline connectivity, while ongoing offshore pipeline tenders in 2026 (via Aramco's CRPO system) indicate continued pipeline scope for upstream-to-onshore evacuation and coastal tie-ins.

Export-resilience and route-diversification upgrades also create a specific opportunity set around the East-West corridor and Red Sea logistics. In July 2026, Aramco was reported to be evaluating an expansion of the East-West crude oil pipeline capacity to the Red Sea coast by up to 2 million barrels per day, with discussion also covering a second pipe for oil products, which lifts requirements for new pumping, terminal interface capacity, and integrity management across long-distance lines. In parallel, Vision 2030 industrial planning for hydrogen and carbon management corridors points to additional midstream design and conversion work (H2-ready steel grades, CO2 trunk lines, and storage integration) alongside gas and liquids pipeline build-outs across major industrial hubs.

Recent Industry Developments

- July 2026: Saudi Arabia was reported to be in preliminary talks to expand the East-West crude oil pipeline capacity to the Red Sea coast by up to 2 million barrels per day, aimed at strengthening export optionality by bypassing the Strait of Hormuz. The discussions also referenced potential additional infrastructure for oil products, which would broaden the scope beyond crude-only throughput and pull forward terminal, pumping, and pipeline integrity requirements.

- October 2025: Saudi Aramco concluded an approximately USD 11 billion lease and leaseback financing for Jafurah midstream assets with an international consortium led by Global Infrastructure Partners. The structure supports capital recycling while keeping operational continuity, and it underlines the role of infrastructure-style investment models in funding large, long-duration gas midstream build-outs.

- June 2024: Saudi Aramco awarded contracts totaling around USD 25 billion covering phase two of the Jafurah gas development and phase three of the Master Gas System expansion. These awards increased the committed EPC and materials pipeline for new gas processing and transmission capacity, reinforcing pipelines and connected facilities as the core spend areas in the Kingdom's midstream agenda.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Saudi Arabia oil and gas midstream market is defined as the revenue generated from moving, storing, and handling crude oil, natural gas, refined products, and LNG inside the country through pipelines, terminals, and storage facilities, along with the related services.

Scope exclusions: This sizing does not count upstream extraction and drilling activity, and it also does not count downstream refining and retail fuel distribution revenues.

Segmentation Overview

- By Infrastructure

- Pipelines

- Terminals

- Storage Facilities (Underground and Above-ground)

- By Product Type

- Crude Oil

- Natural Gas

- Refined Products

- LNG

- By Service Type

- Pipeline Construction

- Pipeline Maintenance and Repair

- Storage and Handling Services

- Transportation and Logistics

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the starting structure of the model and to anchor it to real operating signals in Saudi Arabia. We relied on public and official sources such as national energy and statistical publications, regulator and ministry updates, port and terminal authority releases, trade and customs datasets, and peer reviewed engineering and energy journals that track midstream infrastructure and utilization.

Along with that, company annual reports, investor presentations, and project award announcements were reviewed to map capacity additions, commissioning timelines, and operational changes that could shift service revenues year to year. Where financial disclosure was limited, we also used paid subscription sources focused on company financials and shipment level import and export movements, to sanity check equipment, pipeline, and material flows tied to new builds. These desk sources are not exhaustive, and many other public documents were referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to validate what the desk sources could not fully explain, especially pricing logic, utilization ranges, and how projects translate into billable midstream services. We spoke with a mix of asset operators, engineering and maintenance providers, logistics and terminal service teams, and industry advisors. Coverage was balanced across the main operating regions so assumptions could be cross checked against on the ground constraints and current operating conditions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 16% | |

| Mid tier: 42% | Functional/Unit leaders: 38% | |

| Smaller Players: 20% | Managers: 46% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up blended logic, where infrastructure and activity indicators were first used to reconstruct the revenue pool and then checked with selective supplier and service roll ups. In practice, the top-down side starts from Saudi midstream activity and asset intensity, including pipeline additions and expansions, storage and terminal capacity changes, and the mix shift between crude, gas, refined products, and LNG handling.

To keep the model grounded, a few repeatable inputs were tracked each year, such as pipeline length and expansion timing, storage and terminal capacity additions, service mix between construction and maintenance, utilization and throughput expectations, and realized pricing ranges for transportation, storage, and handling services. Where a variable could not be observed cleanly, we used interview led ranges and then applied conservative gap fills consistent with comparable Saudi projects and prevailing contract conditions.

Forecasting was done using scenario analysis supported by trend smoothing on the key drivers, since project timing, commissioning slippage, and utilization ramps can move revenues even when the long term direction stays intact. Final totals were then corroborated with bottom-up approximations such as sampled price per unit of service multiplied by expected volumes, along with channel checks on major project activity so outlier years could be corrected before finalizing.

Data Validation & Update Cycle

Validation was done in several steps so the market totals match real world signals and do not overreact to any one data point. Model outputs were compared against independent metrics such as visible project pipelines, capacity commissioning schedules, and observed throughput direction, and any sharp jumps were reviewed and explained before sign off.

When large variances showed up between desk indicators and interview feedback, follow up outreach was triggered to recheck the assumption that caused the gap, usually pricing, utilization, or the timing of a new asset coming online. Reports are refreshed annually, and interim updates are made when material events occur, such as major project awards, commissioning announcements, or policy changes. Before delivery, a final review pass is completed so clients receive the most current view available.

Mordor Intelligence's Saudi Arabia Oil and Gas Midstream Market Sizing Compared With Other Published Estimates

Published market sizes for Saudi Arabia midstream can look far apart, even when they describe similar pipelines and storage assets, because the counting rules and pricing bases are not the same. Differences usually come from what gets included as midstream revenue, whether the estimate leans on physical throughput versus service billing, and how currency timing and price inflation are handled.

The main gap comes from mixing asset value or full hydrocarbon trade value into the market total, where Mordor Intelligence counts only midstream service revenues tied to pipelines, terminals, and storage handling, and then tests the result against capacity additions and expected utilization rather than headline oil and gas value flows.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.90 B (2026) | |

| Industry Research Publisher A | USD 85.30 B (2025) | This figure is much larger because the scope appears to align closer to the value of hydrocarbons handled or a wider industry spend view, rather than isolating billed midstream services like storage, terminal handling, and pipeline transportation revenues. |

| Market Analytics Firm B | USD 82.50 B (2024) | The estimate likely includes broader midstream operations and may blend in higher value pools through different pricing bases and base-year assumptions, which can inflate the total versus a service-revenue-only view tied to Saudi asset utilization. |

The table shows that the spread is driven less by math and more by what is being counted and how it is priced. By keeping the revenue pool tied to observable infrastructure activity, realistic utilization ramps, and interview-validated price ranges, the estimate stays traceable to clear steps that can be repeated year after year.

Key Questions Answered in the Report

What is the current value of the Saudi Arabia oil and gas midstream market?

It stood at USD 4.9 billion in 2026 with a projection to reach USD 6.01 billion by 2031.

Which infrastructure segment is expanding fastest?

Pipelines are growing at a 6.48% CAGR, supported by 3,000 km of new lines under Master Gas System Phase 3.

How significant is LNG within Saudi midstream activities?

LNG is the quickest-rising product segment at an 7.86% CAGR thanks to the Fadhili Gas Plant expansion and planned export terminals.

Why are foreign joint ventures important for Saudi midstream?

They inject USD 15 billion in capital and advanced technologies, accelerating timelines and enhancing hydrogen-ready pipeline designs.

What environmental rules affect new pipeline builds?

Updated laws can levy fines up to USD 8 million and require detailed impact assessments that lengthen approval cycles to 24-36 months.

How exposed is the sector to cyber threats?

Attempted attacks on pipeline SCADA networks rose 40% in 2024, prompting mandatory cybersecurity audits and USD 10-20 million in compliance spending per major asset.

Page last updated on: