Refrigerated Air Dryer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

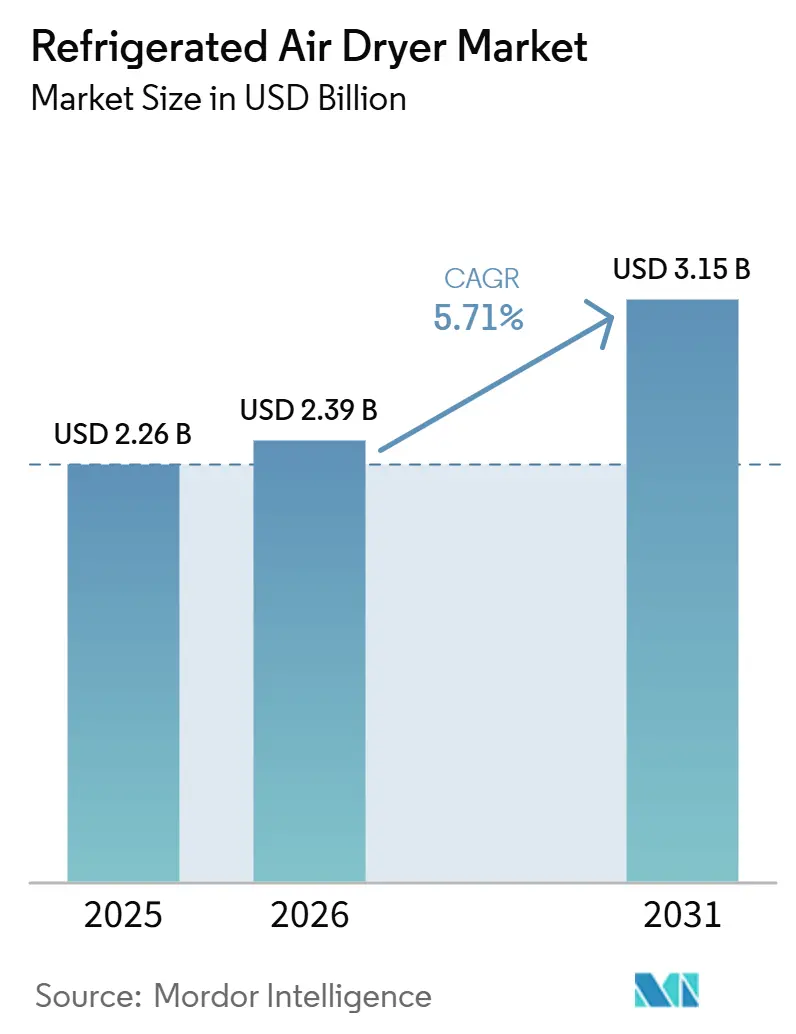

| Market Size (2026) | USD 2.39 Billion |

| Market Size (2031) | USD 3.15 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

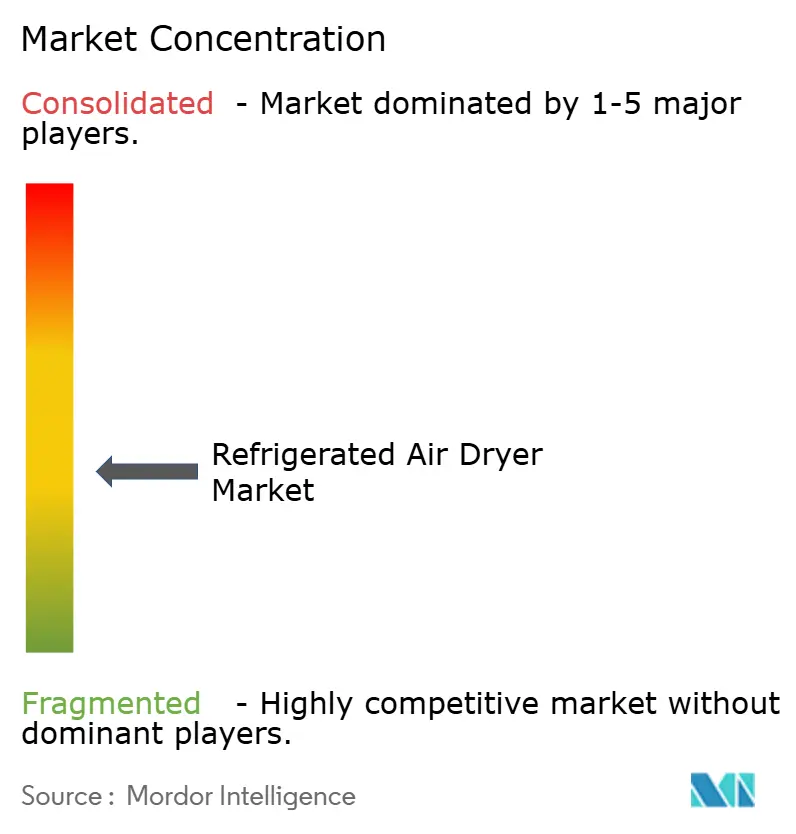

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Refrigerated Air Dryer Market Analysis by Mordor Intelligence

The Refrigerated Air Dryer Market size is expected to increase from USD 2.26 billion in 2025 to USD 2.39 billion in 2026 and reach USD 3.15 billion by 2031, growing at a CAGR of 5.71% over 2026-2031. Rising pressure to eliminate moisture-driven product recalls, stricter ISO 8573‐1 water-vapor limits, and escalating electricity tariffs are the primary forces steering purchasing toward premium, energy-efficient models. Semiconductor fabs funded by the CHIPS and Science Act demand sub-zero dew points to safeguard photolithography tools, while food and pharmaceutical auditors now treat compressed air as a validated, product-contact utility. Utility incentives in California, Ontario, and Germany pay back up to half of the incremental cost of variable-speed-drive (VSD) dryers, accelerating the shift away from conventional cycling designs. Against this backdrop, manufacturers with IoT-enabled service platforms are outpacing price-led rivals because buyers rank total cost of ownership above upfront price.

Key Report Takeaways

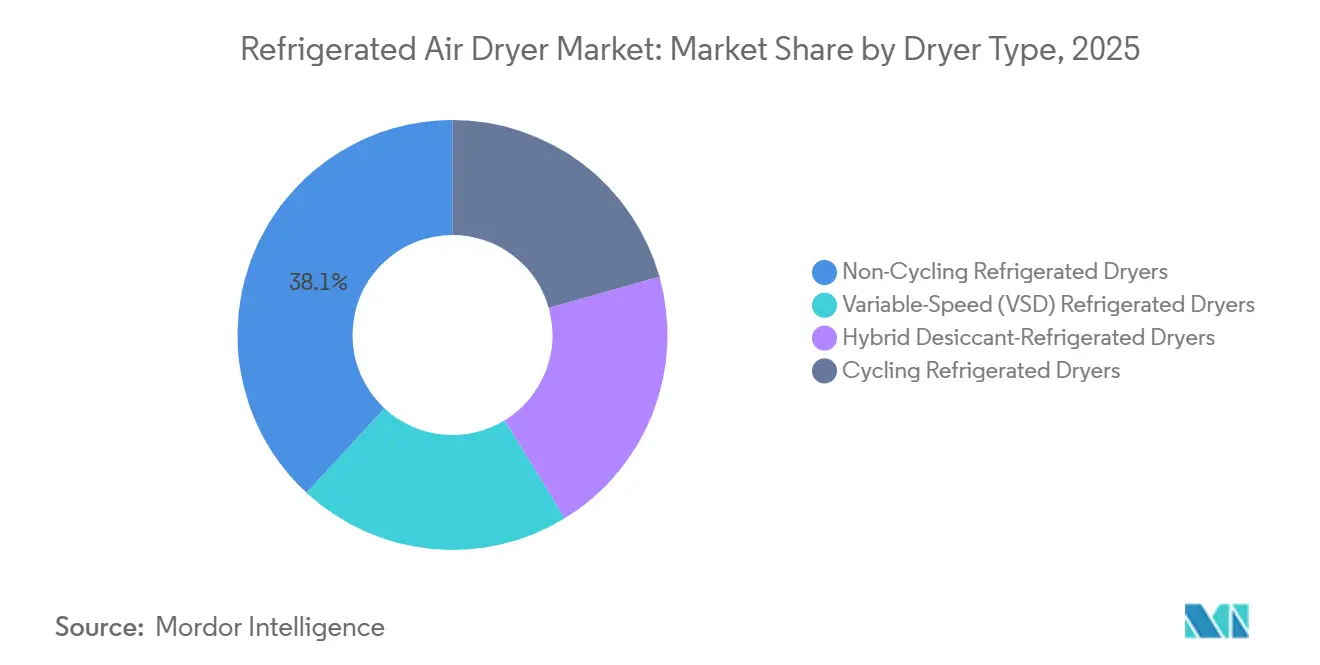

- By dryer type, non-cycling units held 38.12% of the refrigerated air dryer market share in 2025, whereas variable-speed (VSD) refrigerated dryers are advancing at a 5.92% CAGR during the forecast period (2026-2031).

- By refrigerant type, HFC-based (R-134a and R-404A) accounted for 47.55% share of the refrigerated air dryer market size in 2025, while natural/hydrocarbon (R-290 and CO₂) are expanding at 6.11% CAGR during the forecast period (2026-2031).

- By cooling method, air-cooled units led with 64.22% revenue share in 2025; water-cooled models are poised for a 5.94% CAGR during the forecast period (2026-2031).

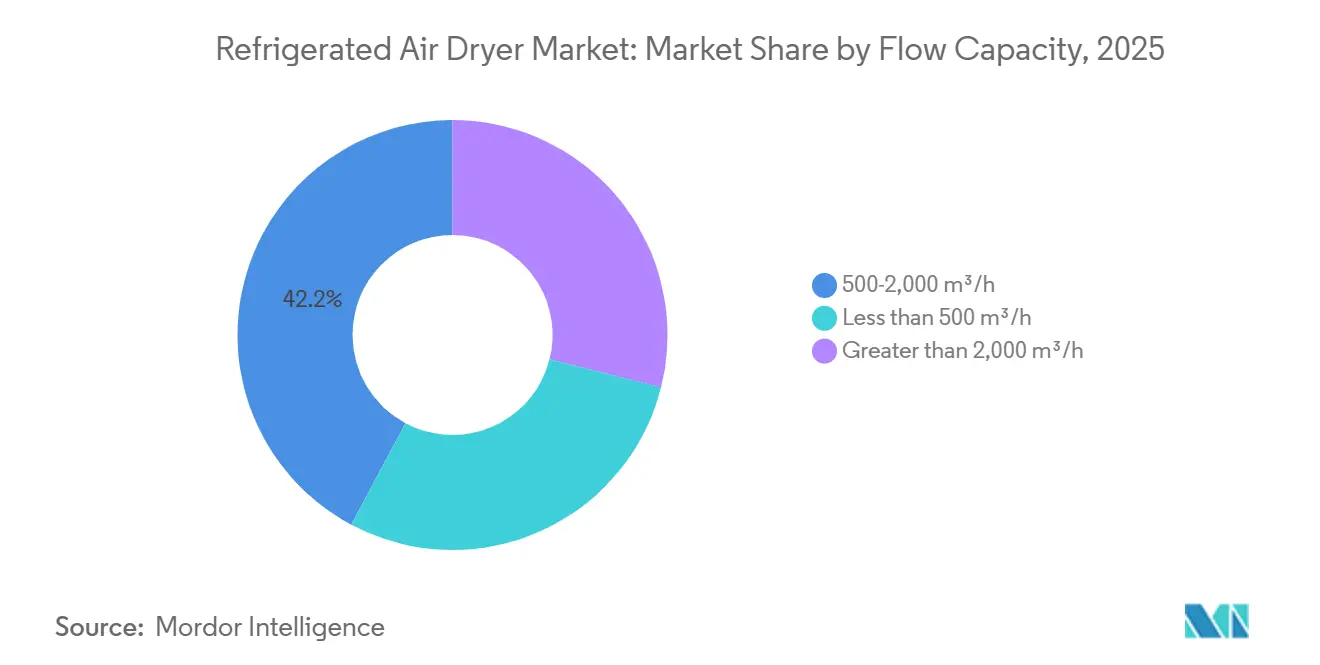

- By flow capacity, the 500-2,000 m³/h class captured 42.21% of the refrigerated air dryer market share in 2025, and greater than 2,000 m³/h are projected to grow at a 6.21% CAGR during the forecast period (2026-2031).

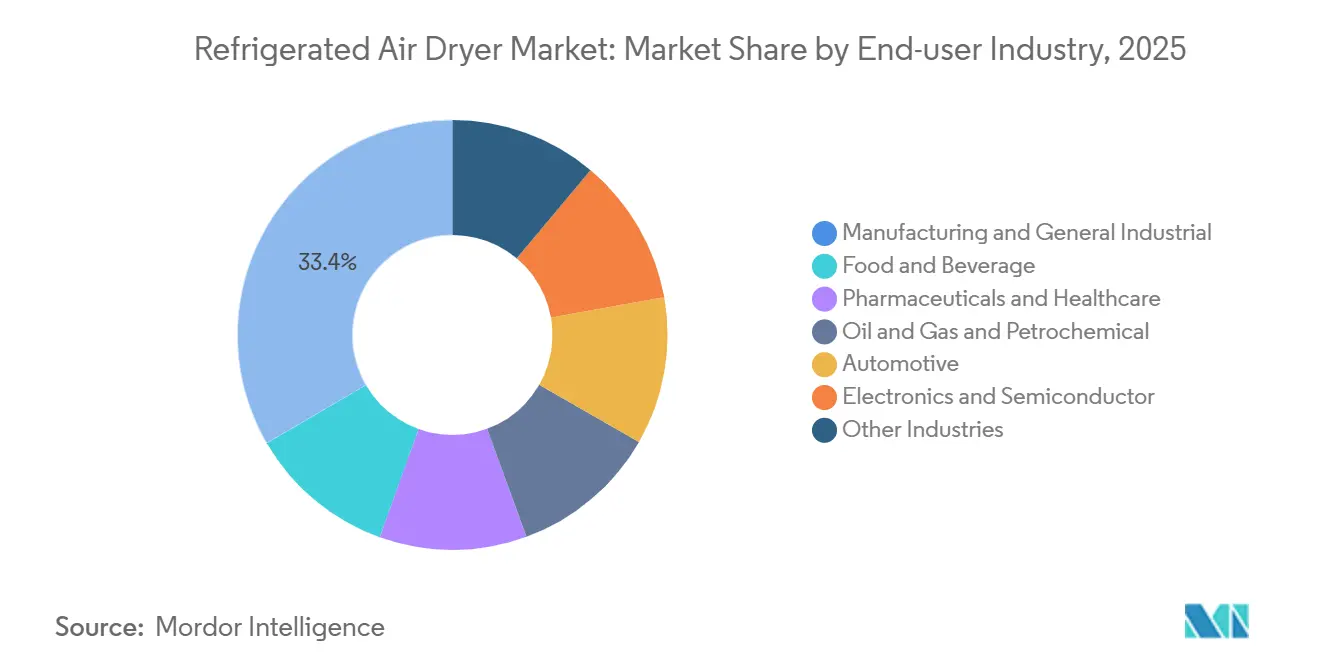

- By end-user industry, manufacturing and general industrial applications represented 33.41% of the refrigerated air dryer market size in 2025, whereas electronics and semiconductor facilities are expanding at a 6.38% CAGR during the forecast period (2026-2031).

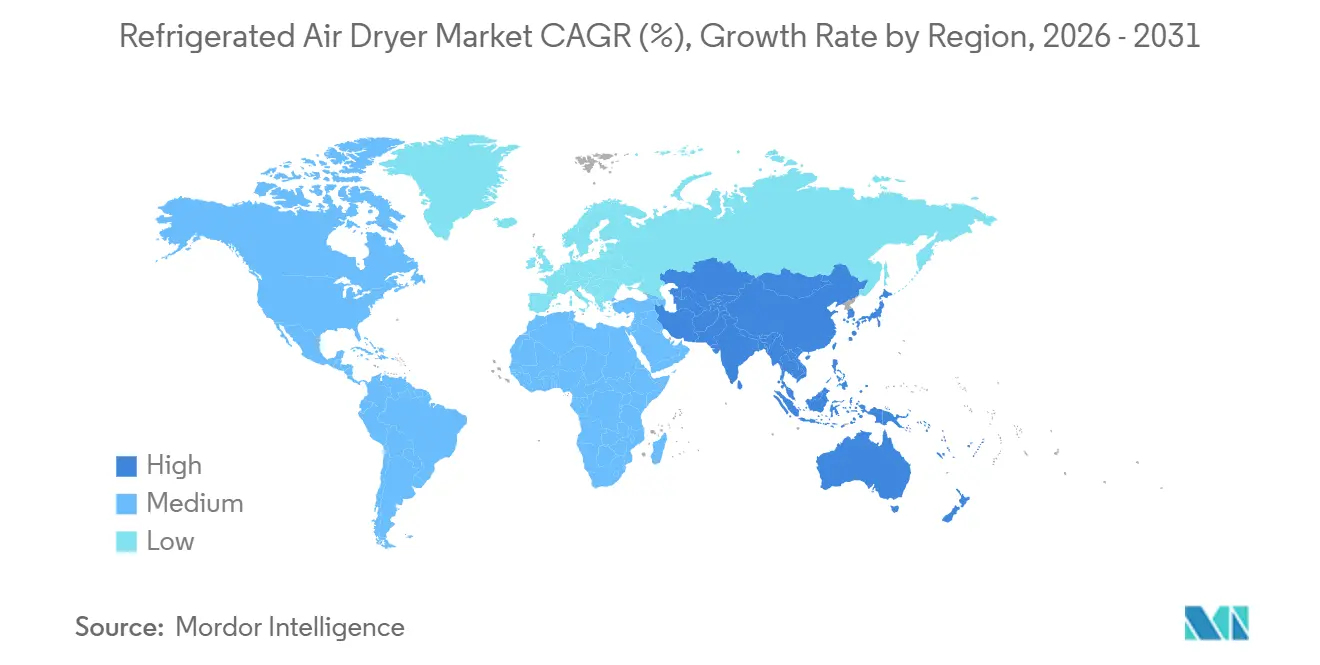

- By geography, Asia-Pacific accounted for 36.11% share of the refrigerated air dryer market size in 2025, and are expanding at 6.63% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Refrigerated Air Dryer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent ISO 8573 compliance in regulated industries | +1.00% | Global, with concentration in North America, Europe, and APAC pharmaceutical/food hubs (Hyderabad, Ahmedabad, Jiangsu) | Medium term (2-4 years) |

| Expansion of global discrete-manufacturing capacity post-2025 | +1.30% | APAC core (China, India, Vietnam, Thailand), spill-over to Mexico, Eastern Europe (Poland, Czech Republic) | Medium term (2-4 years) |

| Energy-efficiency incentives and carbon-credit schemes for VSD dryers | +1.20% | North America (California, Ontario), EU (Germany, Netherlands, Denmark), South Korea | Short term (≤ 2 years) |

| Growth of hybrid desiccant-refrigerated dryers for low-dew-point LNG fueling | +0.50% | North America (Permian Basin, Bakken), Middle East (Qatar, UAE), ASEAN CNG corridors (Thailand, Indonesia) | Long term (≥ 4 years) |

| Surge in containerised micro-breweries and craft food plants needing compact units | +0.40% | North America (U.S. craft beer regions), Europe (UK, Germany, Belgium), APAC urban centers (Shanghai, Seoul, Tokyo) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent ISO 8573 Compliance in Regulated Industries

Regulators now view compressed air as a critical utility with the same validation rigor as process water. ISO 8573-1 Class 2 requires a -40°C pressure-dew-point ceiling, forcing retirement of older cycling dryers that drift during off-load periods. Pharmaceutical aseptic lines and brewery carbonation systems are leading adopters of non-cycling and VSD models because batch losses linked to transient moisture exceed the replacement cost of advanced dryers. Annual third-party testing, costing USD 5,000-15,000 per system, and HACCP alignment in the European Union add to the compliance bill, yet most plants accept the trade-off because audit failures trigger costlier shutdowns[1]U.S. Food and Drug Administration, “Current Good Manufacturing Practice for Compressed Air,” fda.gov.

Expansion of Global Discrete-Manufacturing Capacity Post-2025

Fixed-asset investment in China’s discrete-manufacturing sector rose 8.3% in 2025, while India commissioned 14 new component plants aimed at “China Plus One” supply chains. ASEAN attracted USD 22 billion of electronics FDI in 2024-2025, and each new facility specified refrigerated dryers as part of Class 1 cleanroom builds. North America’s semiconductor renaissance under the CHIPS and Science Act added 11 announced fabs that will each consume up to 20,000 m³/h of conditioned compressed air by 2028. Long order lead times, 24-32 weeks for large custom units, are prompting buyers to commit capital 18 months before plant start-up[2]U.S. Department of Commerce, “CHIPS and Science Act Semiconductor Grants,” commerce.gov.

Energy-Efficiency Incentives and Carbon-Credit Schemes for VSD Dryers

Variable-speed compressors trim 15-25% of energy use versus fixed-speed units. Utilities in Ontario and California reimburse up to 50% of the VSD premium once kWh cuts are proven, and the EU Emissions Trading System allows manufacturers to monetize carbon allowances banked from energy savings worth EUR 80-100 per metric-ton CO₂. Germany and South Korea crossed the USD 0.15 /kWh threshold in 2025, shrinking VSD paybacks below 18 months, so buyers increasingly treat the technology as standard rather than optional.

Growth of Hybrid Desiccant-Refrigerated Dryers for Low-Dew-Point LNG Fueling

LNG and CNG fueling stations need -70°C dew points to prevent hydrate blockages. Hybrid trains combine a refrigerated stage that removes bulk moisture to +3°C with a desiccant polisher that achieves the final low point while using just 3-5% purge gas. U.S. shale basins added 127 new CNG sites in 2024-2025, Qatar is scaling LNG bunkering for marine fuel, and ASEAN’s CNG corridors are mandating hybrid dryers to comply with fuel-quality codes. Although still a 4% unit-share niche in 2025, the segment is advancing at 8-10% a year.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Large upfront CAPEX for industrial-grade units | -0.8% | Global, with acute sensitivity in price-conscious ASEAN and Latin America markets | Short term (≤ 2 years) |

| HFC phasedown (Kigali Amendment) raising refrigerant-compliance cost | -0.9% | Global, with steepest impact in North America and Europe (Annex I countries) | Medium term (2-4 years) |

| Volatility in stainless-steel prices impacting BOM costs | -0.5% | Global, with supply-chain concentration in China, India, and Indonesia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Large Upfront CAPEX for Industrial-Grade Units

Installed prices of USD 40,000-120,000 for 1,000 m³/h and above deter cash-constrained plants in emerging economies, even though moisture-related downtime can cost multiples of that over five years. Equipment-as-a-service contracts in North America let customers pay per cubic meter of dry air, but adoption outside mature markets is hamstrung by weak leasing infrastructure. Long fabrication lead times further strain working capital because buyers must post letters of credit months in advance.

HFC Phasedown Under Kigali Amendment Raises Refrigerant-Compliance Cost

The Kigali Amendment cuts HFC production 70% by 2029 in Annex I countries, pushing R-134a prices from USD 8/kg in 2023 to USD 14/kg in 2025. New dryers now ship with R-1234ze or R-513A, which cost 30-40% more per kilogram and often require redesigns that add USD 3,000-8,000 to a 1,000 m³/h platform. Early adopters shoulder higher capex but avoid future service bottlenecks as reclaimed HFC availability declines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dryer Type: Non-Cycling Units Lead, VSD Technologies Accelerate

Non-cycling models retained 38.12% refrigerated air dryer market share in 2025 on the back of simple maintenance and 20-30% lower purchase prices. They run compressors continuously, which wastes 10-15% energy when demand dips. Variable-speed (VSD) refrigerated dryers, growing at 5.92% CAGR for the forecast period (2026-2031), fine-tune motor speed to real-time load, harvesting 15-25% electricity savings that offset higher purchase prices in high-tariff regions. Cycling designs are losing momentum because start-stop spikes jeopardize ISO 8573 Class 2 compliance in pharmaceutical lines. Hybrid desiccant-refrigerated units sit at 4% of shipments yet clock 8-10% annual growth in LNG and CNG fueling, where -70°C dew points are mandatory. Atlas Copco’s 2025 expansion in New York will add capacity for large VSD centrifugal trains, signaling confidence that installations above 500 m³/h will increasingly default to variable speed. The overall shift suggests a future where intelligence and speed modulation become baseline features even in mid-size systems.

VSD adoption changes aftermarket dynamics. Because variable-speed drives limit mechanical stress, expected overhaul intervals stretch from seven to nine years, lowering parts revenue per installed base. OEMs compensate by bundling cloud monitoring that sells as recurring software. Non-cycling units stay relevant under 300 m³/h where energy savings cannot justify the drive premium, especially in markets with subsidized electricity. As utility tariffs rise, however, even small workshops may migrate, compressing the price gap and eroding non-cycling leadership.

By Refrigerant Type: HFC Incumbency Gives Way to HFO and Natural Choices

HFC-Based (R-134a and R-404A) powered 47.55% of 2025 shipments, reflecting historical safety and service familiarity. The Kigali phase-down shifts momentum to low-GWP HFOs and natural/hydrocarbon (R-290 and CO₂), expected to expand at 6.11% CAGR during the forecast period (2026-2031). R-290 uptake is restrained by A3 flammability limits that cap charge sizes at 150g, whereas CO₂ systems incur heavy-wall and high-pressure penalties that confine use to cold climates. HFOs such as R-513A offer a middle road but still carry a 30-40% price adder over R-134a. Europe banned R-404A in new dryers and slashed R-134a quotas, creating a bifurcated global aftermarket that inflates service costs for late adopters. Multirefrigerant platforms help customers hedge but add 8-12% to list prices and complicate inventory. The installed base will remain mixed through 2031, with retrofit and service markets mirroring local regulatory clocks.

Service technicians need new certifications to handle flammable or high-pressure media, tightening labor availability, and raising maintenance fees by 15-20% in regions where skilled refrigeration labor is scarce. Plants that switch early lock in predictable compliance costs yet must trust OEMs (Original Equipment Manufacturers) to secure long-term HFO and parts supply in a fluid regulatory landscape. Conversely, operators who delay upgrades risk sticker shock as virgin HFC allowances shrink and reclaimed stocks thin out.

By Cooling Method: Air-Cooled Dominance Endures as Water-Cooled Gains Ground

Air-cooled configurations supplied 64.22% of 2025 shipments because they install without cooling towers and sidestep rising industrial-water tariffs in arid regions. Water-cooled units, though gaining at 5.94% CAGR for the forecast period (2026-2031), still face barriers where permits limit abstraction or operators cannot justify the capital for closed-loop chillers. Their 8-12% energy-efficiency edge becomes decisive in data centers and tropical climates where 35°C ambient temperatures push air-cooled condensers beyond design limits. Hybrid air-water systems hold a niche portion of sales but appeal to sites with large seasonal temperature swings. Regulatory nudges are indirect: the EU Water Framework Directive now factors water consumption into operating permits, subtly favoring air-cooled or closed-loop solutions even in efficiency-minded Europe.

Offshore platforms and maritime applications tend to use water-cooled systems because seawater is plentiful, and air-cooled fins corrode rapidly in salt spray. The trade-off is higher materials cost for titanium or cupronickel exchangers. In the Middle East, the doubling of municipal-water fees since 2024 locked in air-cooled dominance, whereas Singapore’s data-center cluster opts for water-cooled packages tied into district chilled-water loops that repay the capex differential in under three years via lower electricity use.

By Flow Capacity: Mid-Range Rules, Large-Capacity Surges

The 500-2,000 m³/h band delivered 42.21% of the refrigerated air dryer market size in 2025 because it aligns with the airflow needs of mid-sized automotive, food, and metalworking plants. Above-2,000 m³/h machines, benefiting from petrochemical, LNG, and semiconductor megaprojects, are growing 6.21% a year to 2031. Each new 300 mm wafer fab under construction in the United States will require 30-40 such dryers, front-loading demand through 2028. Below-500 m³/h equipment faces commoditization from low-cost Chinese suppliers that undercut Western OEMs by up to 50%, pushing incumbents to exit low-end tiers.

Large-capacity orders are custom-engineered, priced at premiums of 25-35%, and typically bundled with multi-year service to guarantee uptime in critical gas and chemical processes. Mid-range replacements cycle faster as ISO audits shorten acceptable asset ages from 12 to nine years. Small-flow packages still appeal to point-of-use labs and clinics but rarely include the digital connectivity that drives aftermarket revenue, leaving them as margin-thin staples for regional assemblers.

By End-user Industry: Manufacturing Anchors Demand, Electronics Accelerates

Manufacturing and general industrial accounted for 33.41% of 2025 revenue, reaffirming compressed air’s role as a universal utility for pneumatic tools, painting, and material handling. Electronics and semiconductor fabrication, climbing at 6.38% CAGR during the forecast period (2026-2031), will be the swing sector through 2031 because every sub-5 nm node fab consumes unprecedented volumes of ISO Class 1 air. Food and beverage plants remain a stable second-tier buyer group as GMP updates codify compressed-air quality as a controlled parameter. Pharmaceutical biologics expansion sustains steady demand for -40°C dew-point dryers with redundant sensors.

Oil, gas, and petrochemical users require massive, continuously operating dryers aboard offshore platforms and in LNG trains. Automotive lines moving to lithium-ion battery assembly, retrofit older dryers to tighter humidity control. Regionally, Asia-Pacific will dominate electronics uptake, North America will lead in large-capacity custom builds linked to fabs, and Europe will focus on energy-efficient upgrades in mature plants.

Geography Analysis

Asia-Pacific held 36.11% of 2025 revenue and is set to notch a 6.63% CAGR through 2031 on the back of China’s 8.3% jump in discrete-manufacturing investment and India’s GMP-driven pharmaceutical retrofits. Eighteen Chinese semiconductor fabs broke ground in 2024-2025 under the “Made in China 2025” banner, each demanding 10,000-20,000 m³/h of ultra-dry air. India’s Tamil Nadu and Gujarat added 14 new automotive-component plants aligned to global OEM near-shoring. ASEAN’s USD 22 billion electronics FDI wave is equipping greenfield lines with advanced refrigerated dryers, while South Korea’s power-price spike shortened VSD paybacks below 18 months, accelerating replacement of cycling units. Supply-side frictions remain: ELGi postponed a Kinathukadavu capacity expansion to 2027-2028 because of regulatory delays, showing infrastructure still lags demand.

In North America, CHIPS Act fabs in Arizona, Texas, and Ohio will collectively order more than 350 large-capacity dryers by 2028. Inflation Reduction Act credits cover up to 30% of VSD premiums, boosting adoption across the general industry. The United States opened 127 new CNG fueling stations during 2024-2025; every station installs a hybrid dryer for -70°C dew points. Canada’s utility rebates drove a year-on-year rise in dryer-upgrade applications in 2025, while Mexico’s near-shoring wave added nine automotive-component plants that replicate parent-company air-quality specs.

In Europe, growth is tempered by a mature base but re-energized by the F-Gas Regulation that bans R-404A and restricts R-134a, forcing a refrigerant rethink that inflates equipment cost 30-40%. Germany, the largest regional buyer, now exceeds 60% VSD penetration in new 500-2,000 m³/h orders because tariffs passed USD 0.15/kWh. Southern Europe leans toward air-cooled units as drought-related water tariffs doubled after 2024. Russia, under sanctions, reverse-engineers Western designs for domestic oil and gas projects but remains isolated from global OEM (original equipment manufacturer) supply chains.

South America and the Middle East and Africa share the least market share. Brazil’s beverage-bottling boom added seven plants in 2024-2025, each mandating ISO Class 2 air for direct product contact. Saudi Aramco’s Jafurah scheme is installing multiple 3,000 m³/h dryers certified to API 618 for sour-gas duty. South African mines postpone upgrades because rolling blackouts force capex into diesel generators, while Nigeria’s currency volatility leaves the market to uncertified imports that underperform in ISO audits.

Competitive Landscape

The Refrigerated Air Dryer market is moderately fragmented. Regional challengers undercut on price. India’s ELGi and China’s Risheng discount small-capacity units 40-50% below incumbents, prompting Western OEMs to abandon low-end tiers and redeploy engineering toward high-capacity, high-regulation niches. Refrigerant compliance becomes a competitive lever; suppliers marketing multirefrigerant machines win bids from buyers worried about Kigali schedules. The trade-off is higher complexity and inventory cost.

Refrigerated Air Dryer Industry Leaders

Atlas Copco AB

Ingersoll Rand

SPX FLOW, Inc.

KAESER KOMPRESSOREN

Sullair

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: ELGi Compressors Europe, a subsidiary of ELGi Equipments Limited, unveiled its latest offering: the AR N Series Direct Expansion Refrigerated Compressed Air Dryers.

- August 2024: Ingersoll Rand has acquired Hi-line Industries, a UK-based company specializing in energy-efficient compressed-air purification equipment. This acquisition is expected to strengthen Ingersoll Rand's position in the refrigerated air dryer market by enhancing its product portfolio and energy-efficient solutions.

Global Refrigerated Air Dryer Market Report Scope

A refrigerated air dryer is an industrial device that removes moisture from compressed air by cooling it to temperatures. By cooling the air, it forces water vapor to condense into liquid, which is then drained away, providing dry, clean air suitable for general manufacturing and pneumatic tools.

The refrigerated air dryer market is segmented by dryer type, refrigerant type, cooling method, flow capacity, end-user industry, and geography. By dryer type, the market is segmented into cycling refrigerated dryers, non-cycling refrigerated dryers, variable-speed (VSD) refrigerated dryers, and hybrid desiccant-refrigerated dryers. By refrigerant type, the market is segmented into HFC-based (R-134a and R-404A), HFO-based (R-1234ze and R-513A), and natural/hydrocarbon (R-290 and CO₂). By cooling method, the market is segmented into air-cooled and water-cooled. By flow capacity, the market is segmented into less than 500 m³/h, 500-2,000 m³/h, and greater than 2,000 m³/h. By end-user industry, the market is segmented into manufacturing and general industrial, food and beverage, pharmaceuticals and healthcare, oil and gas and petrochemical, automotive, electronics and semiconductor, and other industries. The report also covers the market size and forecasts for refrigerated air dryer in 19 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Cycling Refrigerated Dryers |

| Non-Cycling Refrigerated Dryers |

| Variable-Speed (VSD) Refrigerated Dryers |

| Hybrid Desiccant-Refrigerated Dryers |

| HFC-Based (R-134a and R-404A) |

| HFO-Based (R-1234ze and R-513A) |

| Natural/Hydrocarbon (R-290 and CO₂) |

| Air-Cooled |

| Water-Cooled |

| Less than 500 m³/h |

| 500-2,000 m³/h |

| Greater than 2,000 m³/h |

| Manufacturing and General Industrial |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Oil and Gas and Petrochemical |

| Automotive |

| Electronics and Semiconductor |

| Other Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Dryer Type | Cycling Refrigerated Dryers | |

| Non-Cycling Refrigerated Dryers | ||

| Variable-Speed (VSD) Refrigerated Dryers | ||

| Hybrid Desiccant-Refrigerated Dryers | ||

| By Refrigerant Type | HFC-Based (R-134a and R-404A) | |

| HFO-Based (R-1234ze and R-513A) | ||

| Natural/Hydrocarbon (R-290 and CO₂) | ||

| By Cooling Method | Air-Cooled | |

| Water-Cooled | ||

| By Flow Capacity | Less than 500 m³/h | |

| 500-2,000 m³/h | ||

| Greater than 2,000 m³/h | ||

| By End-user Industry | Manufacturing and General Industrial | |

| Food and Beverage | ||

| Pharmaceuticals and Healthcare | ||

| Oil and Gas and Petrochemical | ||

| Automotive | ||

| Electronics and Semiconductor | ||

| Other Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the refrigerated air dryer market in 2026 and where is it heading?

The market stands at USD 2.39 billion in 2026 and is projected to reach USD 3.15 billion by 2031, growing at a 5.71% CAGR

Which dryer type is gaining the fastest traction?

Variable-speed-drive refrigerated dryers are expanding 5.92% annually during the forecast period (2026-2031) to electricity-cost savings and utility-rebate programs.

What is driving Asia-Pacific growth?

Expanding semiconductor, automotive, and pharmaceutical capacity in China, India, and ASEAN countries is propelling a 6.63% regional CAGR through 2031.

How will the Kigali Amendment affect equipment choices?

HFC supply cuts are pushing operators toward costlier but compliant HFO or natural-refrigerant dryers, increasing upfront prices yet insulating owners from future restrictions.

Page last updated on: