Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

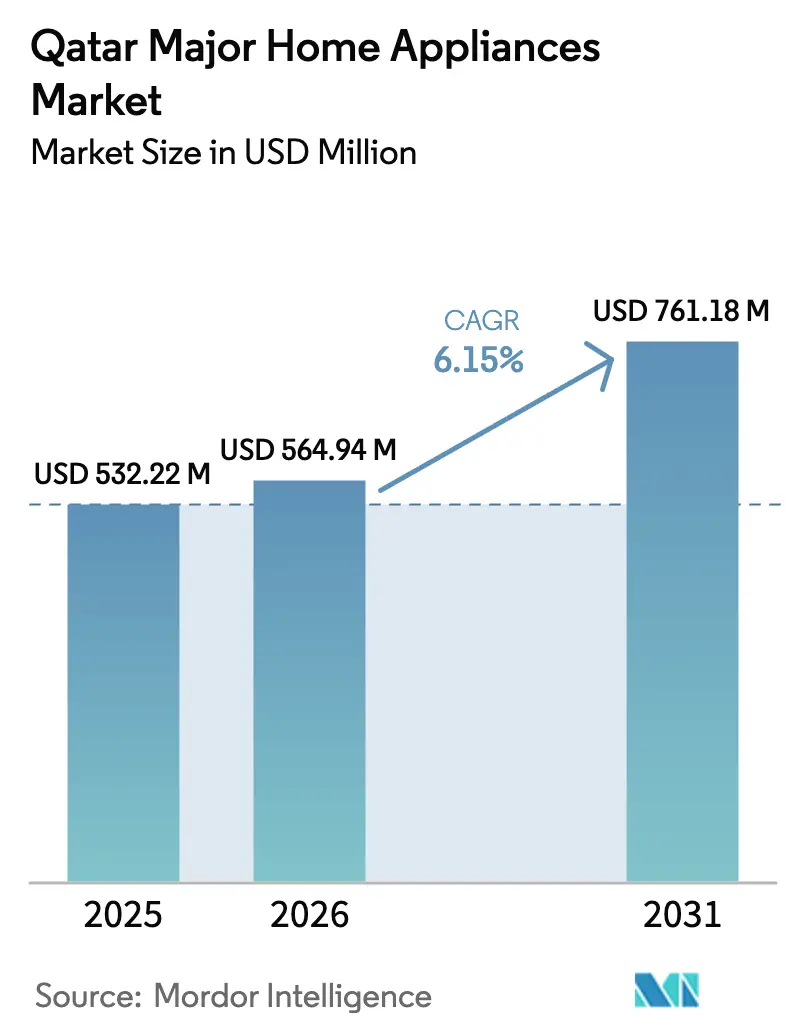

| Base Year Market Size (2025) | USD 532.22 Million |

| Market Size (2026) | USD 564.94 Million |

| Market Size (2031) | USD 761.18 Million |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Major Home Appliances Market Analysis by Mordor Intelligence

The Qatar Major Home Appliances market size was valued at USD 532.22 million in 2025 and estimated to grow from USD 564.94 million in 2026 to reach USD 761.18 million by 2031, at a CAGR of 6.15% during the forecast period (2026-2031). The current expansion of the Qatar Major Home Appliances market reflects a post-FIFA World Cup economy that continues to leverage immigration-driven household formation, government housing loans, and accelerating digital retail growth. Air conditioners retain primacy within the Qatar Major Home Appliances market because extreme heat pushes cooling devices from discretionary to essential status. Dishwashers are gaining ground as Western lifestyle habits diffuse through the expatriate workforce, while energy-efficiency subsidies under Qatar National Vision 2030 redirect consumer attention from upfront price to lifetime operating cost. E-commerce now builds on 5G rollout, high mobile penetration, and one-hour delivery pilots to rewrite brand visibility rules across the Qatar Major Home Appliances market, even as multi-brand stores remain critical for large-ticket items that require in-store demonstration and post-sale servicing.

Key Report Takeaways

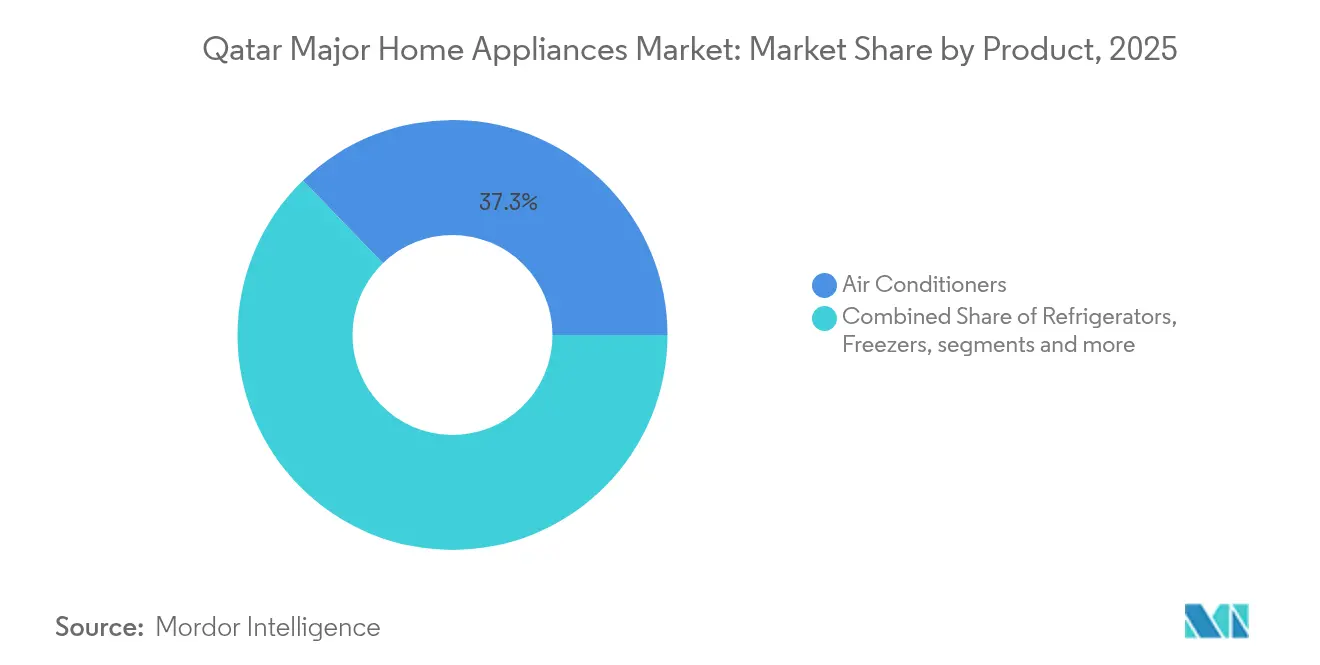

- By product category, air conditioners led with 37.25% revenue share in 2025, while dishwashers are projected to expand at a 6.85% CAGR through 2031.

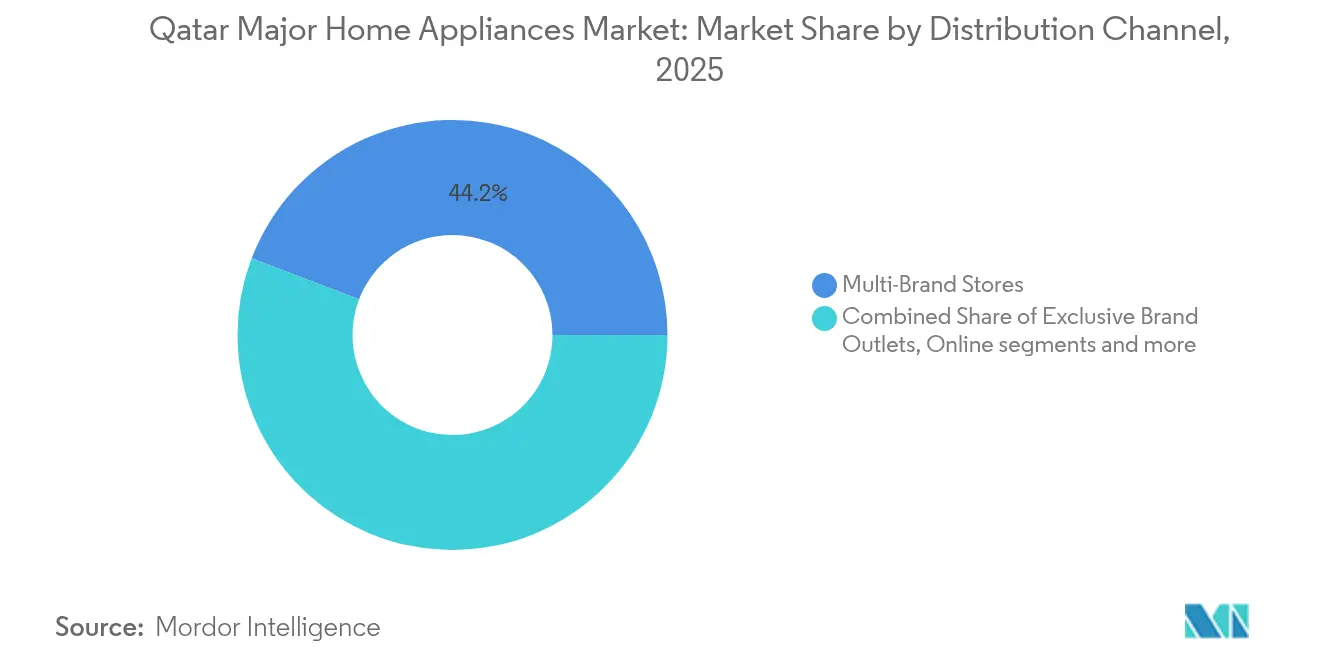

- By distribution channel, multi-brand stores held 44.20% of the Qatar Major Home Appliances market share in 2025, whereas online channels are advancing at a 7.45% CAGR to 2031.

- By geography, Doha accounted for 59.30% share of the Qatar Major Home Appliances market size in 2025, and Al Wakrah is projected to expand at a 7.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Major Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income & expatriate population growth | +1.8% | National, concentrated in Doha and Al Rayyan | Medium term (2-4 years) |

| Government housing initiatives & infrastructure development | +1.2% | National, early gains in Al Wakrah, Umm Salal | Long term (≥ 4 years) |

| High penetration of smart home technology | +0.9% | Urban centers, mainly Doha and Al Rayyan | Short term (≤ 2 years) |

| FIFA World Cup legacy boosts rental turnover | +0.7% | National, peak in Doha | Short term (≤ 2 years) |

| Energy-efficiency subsidies (QNV 2030) | +0.6% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income & Expat Population Growth

Qatar’s expatriates constitute roughly three-quarters of residents, and their combined purchasing power underpins frequent appliance replacement. Rental agreements for furnished units commonly run 24–36 months, a term that accelerates demand for mid-range refrigerators and dishwashers. Employers competing for skilled talent offer housing allowances that push buyers toward premium brands touting quieter compressors and lower electricity use. Whirlpool supplied more than 50,000 units to local project developers, signaling a vibrant business-to-business pipeline. Wage growth tied to the Third National Development Strategy keeps household budgets resilient even as headline inflation cooled to 1% in 2024[1]International Monetary Fund, “Qatar—Staff Concluding Statement of the 2024 Article IV Mission,” imf.org.

Government Housing Initiatives & Infrastructure Development

Interest-free loans and free land plots for Qatari nationals stimulate construction in suburban municipalities, creating entire housing clusters that require full appliance suites. The extension of 23,400 electricity substations by 2026 removes grid bottlenecks and permits higher-capacity cooling systems across the Qatar major home appliances market[2]Qatar General Electricity & Water Corporation, “Annual Transmission & Distribution Report 2025,” kahramaa.gov.qa. Developers phase procurement near handover, producing concentrated order cycles that favor suppliers able to guarantee short-lead deliveries. Sustainable-building codes mandate inverter compressors, R32 refrigerants, and water-saving washing machines, elevating specification over price comparisons. Ongoing petrochemical and port projects in Ras Laffan and Mesaieed draw contractor camps that also generate residential appliance demand for workers.

High Penetration of Smart Home Technology

Qatar’s National Digital Agenda earmarks USD 11 billion for ICT contribution to non-hydrocarbon GDP, spurring 5G coverage that now blankets major municipalities. Samsung integrates SmartThings hubs into premium AC models, enabling mobile scheduling and predictive maintenance alerts, while LG embeds AI agents into refrigerators that monitor door-open frequency. Expatriates accustomed to connected living in Europe and North America accelerate adoption curves in the Qatar major home appliances market. Energy-use dashboards allow users to visualize cost savings, an attribute that dovetails with power-tariff reforms planned for 2027. Retailers position Wi-Fi-ready models as the default rather than an upgrade, shifting price sensitivities toward software support and over-the-air update longevity.

FIFA World Cup Legacy Boosting Rental Turnover

Stadium-adjacent districts converted to mixed-use zones now host serviced apartments that refresh interiors every leasing season. Property managers favor durable yet mid-priced appliances capable of rapid swap-outs when occupancy switches. Hospitality venues built for the tournament purchased commercial-grade laundry and refrigeration units that still fall within the statistical scope of the Qatar major home appliances market, blurring category boundaries. Tourism arrivals have remained above pre-event levels, elongating this turnover impulse beyond the typical mega-event halo. Landlords cite sustainability expectations established during the World Cup bid, prioritizing high Energy Star-style ratings when selecting replacement stock.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Disruptions & Import Dependency | -1.4% | National, affecting all distribution channels | Short term (≤ 2 years) |

| Rising Inflation & Currency Fluctuation | -0.8% | National, with a higher impact on imported premium brands | Short term (≤ 2 years) |

| Influx of Low-Cost Asian Brands Compressing Margins | -0.6% | National, concentrated in multi-brand stores and online channels | Medium term (2-4 years) |

| Water-Scarcity Regulations Limiting Appliance Specs | -0.4% | National, with stricter enforcement in water-stressed municipalities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Disruptions & Import Dependency

Nearly all large appliances arrive through Hamad Port, exposing retailers to freight-rate spikes and customs documentation backlogs. The new 12-digit GCC tariff code temporarily slowed clearance in early 2025, forcing safety-stock expansions that tie up working capital. Certificate-of-origin notarization adds an administrative burden for smaller importers, widening scale advantages for regional distributors. Qatar’s 5% external duty is modest yet still compounds when currency fluctuations elevate supplier quotations[3]U.S. Department of Commerce, “Doing Business in Qatar 2025,” trade.gov. Although China lifted appliance export quotas in 2024, Red Sea shipping route tensions raise insurance premiums that pass through to shelf prices.

Influx of Low-Cost Asian Brands Compressing Margins

TCL, Hisense, and Haier push aggressively into the Qatar Major Home Appliances market by bundling warranties and financing dealer showrooms. Their chassis-level cost advantages allow refrigerator prices below European incumbents, pressuring profit pools across multi-brand retail. Online marketplaces further sharpen comparisons, letting shoppers sort dishwashers by lowest price within seconds. Premium names respond with feature escalation—door-in-door storage, UV-sterilization cycles, and voice control—to justify differentials. Retailers welcome higher footfall yet concede narrower per-unit margins as incentives shift toward volume rebates rather than headline percentages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cooling Dominance Amid Kitchen Evolution

Air conditioners commanded 37.25% revenue in 2025, anchoring the Qatar major home appliances market around climate-driven necessity. The segment draws strength from household energy statistics showing cooling appliances account for half of electricity usage in GCC homes ScienceDirect. Refrigerators maintain steady upgrades as buyers prefer larger capacities compatible with bulk grocery habits adopted during the pandemic. Dishwashers grew fastest and benefit from BSH’s strong regional advertising around hygienic wash temperatures, reflecting lifestyle convergence among expatriates. Washing machines incorporate water-efficiency features that align with forthcoming grey-water recycling regulations.

The Qatar major home appliances market size for dishwashers is forecast to climb at 6.85% CAGR, supported by rising dual-income households that trade time savings for utility costs. Ovens, particularly convection-microwave hybrids, gain traction in apartments where kitchen footprints are constrained. LG’s antimicrobial evaporator coatings resonate with hospitality buyers seeking health certifications for post-stay sanitation audits. Specialty cooking devices, including smart air fryers, sit within the “Others” category yet foreshadow adjacent expansion into countertop appliances. Across every sub-category, energy labels and IoT readiness shape brand consideration more than color or handle style, signaling maturity in consumer evaluation criteria.

By Distribution Channel: Digital Transformation Accelerates

Multi-brand stores held a 44.20% share of the Qatar major home appliances market in 2025 because consumers still rely on hands-on comparison for bulky items. Retailers cluster along Salwa Road in Doha, where one-stop appliance districts simplify weekend shopping itineraries. Floor staff use augmented-reality tablets to superimpose refrigerator door swings onto apartment floor plans, bridging online research with physical inspection. Exclusive brand outlets target the premium tier with experiential showrooms; Bosch and Siemens operate design centers featuring live cooking demos that reinforce aspirational positioning.

The Qatar major home appliances market size for online channels is projected to advance at 7.45% CAGR to 2031, driven by fintech-enabled installment plans and real-time inventory visibility. Marketplace platforms partner with logistics providers, offering doorstep installation within 48 hours across all municipalities. Price transparency is reshaping promotion cycles: brands now synchronize flash sales with pay-day calendars common to expatriate salaried workers. “Click-and-collect” models leverage existing storefronts, reducing last-mile costs while preserving service touchpoints. Independent installers register on digital ecosystems to capture after-sale revenue, illustrating how e-commerce growth permeates broader value-chain economics.

Geography Analysis

Doha retained 59.30% share of the Qatar Major Home Appliances market size in 2025, as its skyline of high-rise apartments compresses thousands of households into a narrow radius. Vertical living favors stackable washer-dryer combos and built-in dishwashers. Retail density allows same-day delivery for breakdown replacements, reinforcing purchase confidence. Al Rayyan follows as a complementary hub where larger homes translate into multi-unit cooling systems and side-by-side refrigerators. Umm Salal’s emergent housing for government staff sustains demand for mid-priced models that balance feature depth with affordability.

Al Wakrah leads in growth at 7.08% CAGR, catalyzed by coastal master plans that integrate marinas, schools, and healthcare facilities. Family-sized villas in the municipality typically feature dual kitchens—one indoor, one outdoor—doubling appliance count per property.

Al Khor’s industrial zone erects dormitories for petrochemical workers, generating bulk purchases of durable washing machines with simplified user interfaces. Northern districts such as Al Daayen invest in road connectivity first, but retail feasibility studies already earmark plots for future appliance megastores. This geographic diffusion ensures that Qatar's major home appliances market evolves from a Doha-centric profile into a multi-nodal landscape.

Competitive Landscape

The Qatar major home appliances market features more than 20 active international brands, producing a moderate concentration scenario with vigorous feature competition but limited pricing power. European incumbents, chiefly BSH and Whirlpool, protect premium margins via advanced inverter compressors, hygienic steam cycles, and extensive after-sales service contracts. Samsung and LG pivot on connectivity, bundling appliances with smart-home hubs and cloud-based diagnostics that appeal to tech-savvy expatriates. Chinese players such as TCL, Haier, and Hisense enter through aggressive distributor incentives, lowering retail prices, and squeezing gross margins across the board.

Strategic moves in 2024-2025 illustrate dual playbooks. LG broke ground on a USD 600 million India plant intended to backfill Middle East shipments and mitigate freight risk, KED Global. Arçelik acquired Whirlpool’s MENA operations to gain scale and region-specific product knowledge, signaling consolidation intent. Arçelik Retailers align with whichever supplier offers the fastest replenishment: shortages in split-AC outdoor units during summer 2024 prompted some dealers to reorder container loads directly from Shenzhen factories. Smart-appliance ecosystems form a second competitive axis; Samsung’s SmartThings counts 360 million users, while LG’s Home 8 voice assistant allows refrigerator firmware updates over 5 G. Value-tier challengers copy premium functions within months, eroding differentiation and shortening product refresh intervals.

White-space opportunities persist in project sales. Government affordable-housing schemes create volume bids where the total cost of ownership overrides badge prestige. As efficiency mandates tighten, compressor suppliers become critical bottlenecks, and vertically integrated brands hold an edge. Overall, rivalry centers on who can synchronize global manufacturing, local compliance, and omnichannel engagement faster than peers.

Qatar Major Home Appliances Industry Leaders

Whirlpool Corporation

LG Electronics Inc.

Samsung Electronics Co. Ltd

Haier Smart Home Co. Ltd.

BSH Home Appliances

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: LG Electronics broke ground on a USD 600 million appliance plant in Sri City, India, designed to supply 1.5 million air conditioners annually to Middle East export markets.

- February 2025: Lulu Retail opened 21 GCC stores, including outlets in Qatar, and disclosed 70% e-commerce revenue growth for electrical categories.

- October 2024: Rheem launched Dubai production of commercial AC units using locally sourced components and zero-waste processes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Qatar major home appliances market as sales of new refrigerators, freezers, washing machines, dishwashers, air conditioners, ovens (including microwave and combi units), and comparable large domestic machines supplied to residential end-users across Doha, Al Rayyan, Al Wakrah, Umm Salal, Al Khor, and adjoining municipalities.

Scope exclusion: small countertop appliances such as kettles, mixers, and personal grooming devices are outside this study.

Segmentation Overview

- By Product

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Ovens (Incl. Combi & Microwave)

- Air Conditioners

- Other Major Appliances

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- Doha

- Al Rayyan

- Al Wakrah

- Umm Salal

- Al Khor

- Others (Al Daayen, Al Shahaniya, Al Shamal)

Detailed Research Methodology and Data Validation

Primary Research

To tighten assumptions, Mordor analysts interviewed importers, large electronics retailers, and HVAC installers across Doha and Al Wakrah, alongside brief surveys with facility managers in hospitality and new residential projects. These conversations verified channel mark-ups, typical replacement cycles, and the planned uptake of inverter air conditioners and washer-dryer combos.

Desk Research

Our analysts gathered baseline statistics from high-credibility, non-paywalled portals such as Qatar Planning and Statistics Authority, Qatar Customs, Gulf Co-operation Council tariff data, and the International Energy Agency, complemented by trade association releases from APPLiA and regional retail federations. Company filings, retailer presentations, and energy-label registration logs informed product mix and price points. Subscription databases like D&B Hoovers and Dow Jones Factiva supplied company revenue splits and shipment references. This list is illustrative; many additional public and paid touchpoints were consulted for cross-checks and clarifications.

Market-Sizing & Forecasting

A top-down construct starts with import-adjusted supply and estimated in-country assembly, which are then matched to household stock renewal and first-time purchase pools. Select bottom-up checks, sampled average selling price multiplied by reported unit volumes at leading chains, help us refine totals. Key variables include annual housing completions, resident expatriate growth, average room air-conditioner penetration, appliance energy-efficiency premiums, and e-commerce share. Multivariate regression models project each driver forward, while scenario stress tests, guided by expert views, account for policy shifts in energy subsidies. Gaps in bottom-up observations are bridged through weighted interpolation using nearest year data.

Data Validation & Update Cycle

We compare provisional numbers with external import values, manufacturer shipment trends, and consumer-price indices. Variances trigger iterative analyst reviews before sign-off. Reports update every twelve months, with mid-cycle refreshes if currency volatility or regulatory action materially reshapes demand. An analyst performs a final pass just before client release to assure the latest view.

Why Our Major Home Appliances Market In Qatar Size & Share Analysis Baseline Commands Reliability

Published market estimates often diverge because providers pick differing product baskets, pricing references, and refresh cadences.

Key gap drivers include: some studies merge small and major appliances; others apply unverified import-to-retail mark-ups or assume uniform growth across cooling and laundry categories, while Mordor anchors value to product-level supply flows and differentiated price trajectories. Frequent annual refreshes further curb vintage data risks that inflate or deflate totals elsewhere.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 532.22 M (2025) | Mordor Intelligence | |

| USD 892 M (2024) | Regional Consultancy A | Includes small appliances and uses single national ASP without channel splits |

| USD 232 M (2024) | Trade Journal B | Relies solely on import value, excludes distributor and retail mark-ups |

These comparisons show that when scope and price realism differ, headline values swing widely; Mordor's disciplined variable selection and dual validation steps yield a balanced, transparent baseline clients can trace and repeat confidently.

Key Questions Answered in the Report

What is the current value of the Qatar Major Home Appliances market?

The market is valued at USD 564.94 million in 2026.

How fast is the Qatar Major Home Appliances market expected to grow?

It is projected to post a 6.15% CAGR and reach USD 761.18 million by 2031.

Which product dominates the Qatar Major Home Appliances market?

Air conditioners lead with a 37.25% revenue share in 2025.

Which distribution channel is gaining momentum?

Online channels are growing at a 7.45% CAGR as e-commerce infrastructure and digital payments improve.

Which municipality shows the fastest growth?

Al Wakrah records the highest geographic CAGR of 7.08% through 2031 due to post-World Cup suburban development.

What policy is driving energy-efficient appliance demand?

Rebates under Qatar National Vision 2030 energy-efficiency programs incentivize consumers to select high-performance models.

Page last updated on: