Nasogastric Tube Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

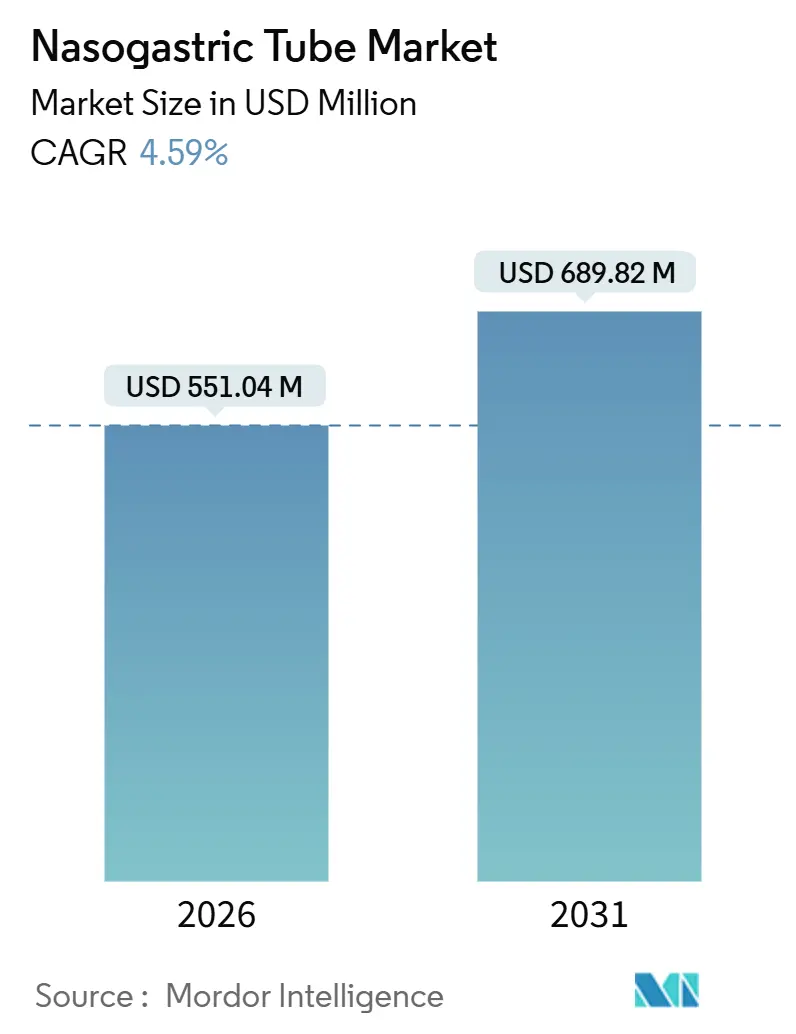

| Market Size (2026) | USD 551.04 Million |

| Market Size (2031) | USD 689.82 Million |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

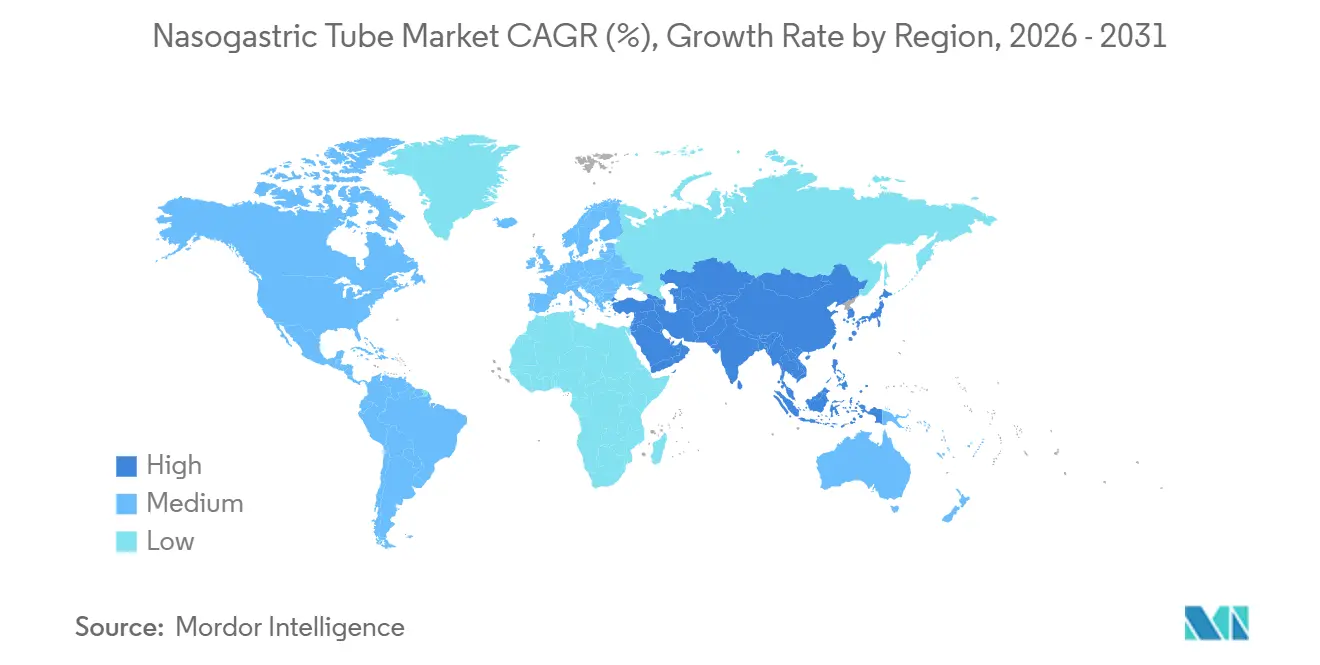

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nasogastric Tube Market Analysis by Mordor Intelligence

The Nasogastric Tube Market size is estimated at USD 551.04 million in 2026, and is expected to reach USD 689.82 million by 2031, at a CAGR of 4.59% during the forecast period (2026-2031).

Rising demand for decentralized care, tighter biocompatibility standards, and the integration of artificial intelligence (AI) confirmation tools are reshaping procurement priorities. Hospitals still account for the bulk of placements, yet payers in the United States and several OECD nations have enlarged reimbursement for home-based enteral therapy, encouraging early discharge and lowering readmission costs. Material-science advances, such as silicone formulations with lower extractables, are enhancing patient tolerance, while electromagnetic-tipped tubes are gaining momentum as malpractice insurers push for verifiable placement. Asia-Pacific is the fastest-growing region as China and India localize production and accelerate regulatory approvals, signaling a long-term shift in volume toward emerging economies.

Key Report Takeaways

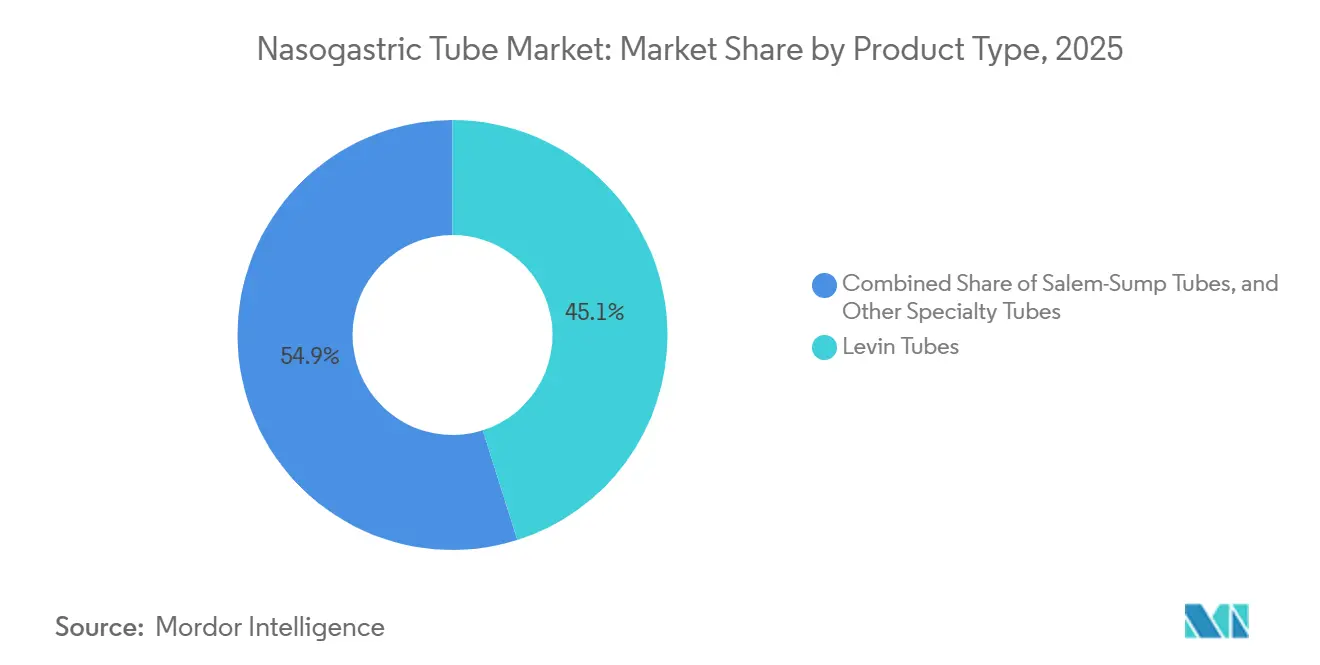

- By product type, Levin tubes led the nasogastric tube market with 45.11% market share in 2025, and specialty tubes are projected to expand at a 6.48% CAGR through 2031.

- By material, polyurethane accounted for 37.87% of the nasogastric tube market in 2025, while silicone is advancing at a 7.12% CAGR through 2031.

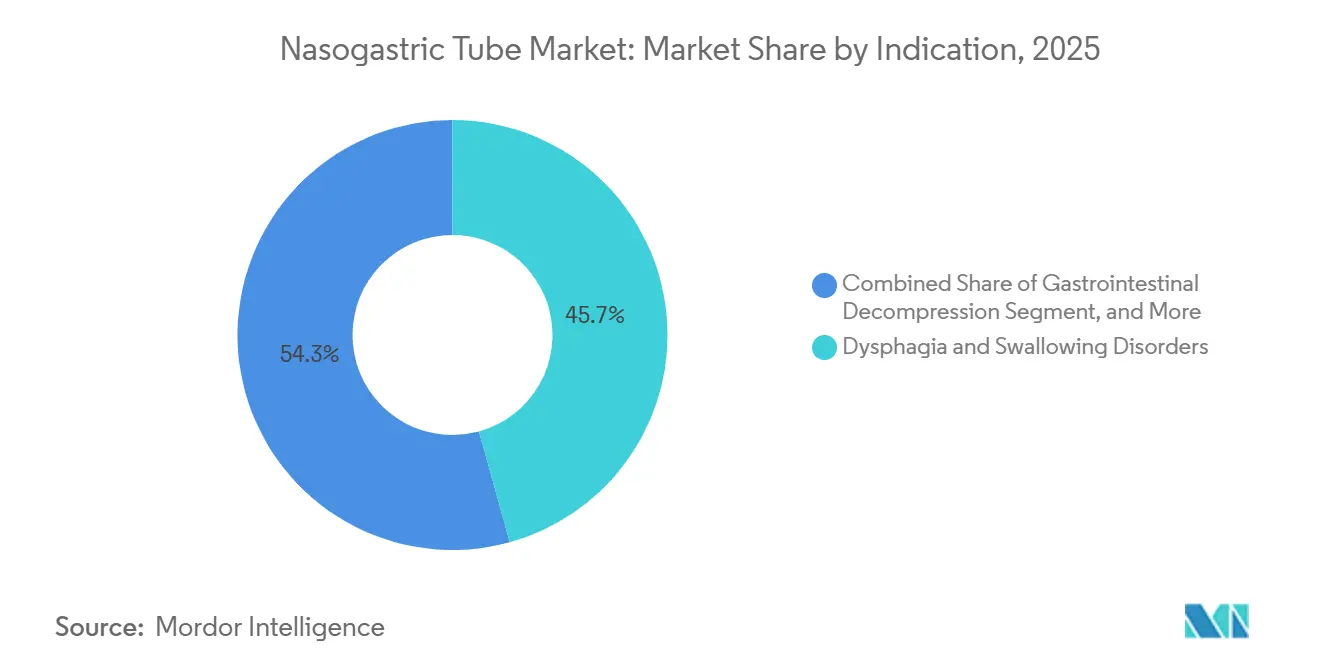

- By indication, dysphagia and swallowing disorders captured 45.72% of the 2025 volume, whereas drug and nutrient administration is growing at an 8.87% CAGR through 203.

- By end user, hospitals accounted for 61.13% of 2025 demand, while home healthcare is registering a 7.39% CAGR through 2031.

- By geography, North America accounted for 35.03% of 2025 revenue, whereas Asia-Pacific is expected to expand at a 9.39% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nasogastric Tube Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Gastrointestinal Disorders Requiring Enteral Access | +1.2% | Global, with concentration in North America and Europe due to aging demographics | Medium term (2-4 years) |

| Growing Geriatric Population & Dysphagia Prevalence | +1.5% | Global, peak impact in Asia-Pacific (China, Japan) and Europe | Long term (≥4 years) |

| Increasing Critical-Care Admissions Globally | +0.8% | North America, Europe, urban centers in APAC | Short term (≤2 years) |

| Preference for Enteral Over Parenteral Nutrition | +0.6% | Global, led by North America and Europe clinical guidelines | Medium term (2-4 years) |

| AI-Enabled Bedside Placement Confirmation Devices | +0.5% | North America, Western Europe, early adoption in Japan | Short term (≤2 years) |

| Bariatric Pre-Op Decompression Demand in Outpatient Centers | +0.3% | North America, Middle East (medical tourism hubs), select APAC markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Gastrointestinal Disorders Requiring Enteral Access

Inflammatory bowel disease diagnoses climbed 6.3% year-on-year in the United States in 2025, boosting short-term nasogastric decompression demand.[1]Centers for Disease Control and Prevention, “IBD 2025 Surveillance Report,” cdc.gov Bariatric surgery volumes reached 1.2 million procedures in 2024, each involving perioperative gastric drainage, and updated 2025 guidelines mandate prophylactic tube placement across 3,800 accredited North American centers. Outpatient surgical programs intensify consumable turnover by discharging patients within 24 hours. UnitedHealthcare expanded coverage in 2025 to include gastroparesis, adding 180,000 beneficiaries eligible for enteral access each year.[2]UnitedHealthcare, “2025 Medical Policy Update,” uhc.com These converging factors raise baseline procedure counts and reinforce recurring device revenue.

Growing Geriatric Population and Dysphagia Prevalence

Global citizens aged ≥ 65 will reach 1.6 billion by 2030, with dysphagia affecting up to 22% of that cohort. Japan subsidized home enteral nutrition in 2024, cutting patient co-pays and lifting tube placements by 14.2% in 12 months. Stroke incidence in the Asia-Pacific region climbed 3.8% in 2024, expanding acute demand in rehabilitation units. Neurological diseases extend feeding duration; ALS prevalence rose 5.1% in 2024, lengthening nasogastric dependence to more than four years. Long-term care facilities, therefore, train nursing staff in bedside insertion, lowering hospital transfers and per-patient costs by USD 2,400.

Increasing Critical-Care Admissions Globally

ICU bed utilization across OECD countries moved from 71% in 2020 to 78% in 2025, elevating early enteral nutrition to a standard of care. The Society of Critical Care Medicine links 48-hour feeding to shorter ventilator time and better outcomes. India alone added 14,000 ICU beds in 2024, each stocked with single-use polyurethane tubes. European survey data confirm that 89% of ICUs prefer nasogastric access over post-pyloric alternatives. Such infrastructure build-outs lay the foundation for annual device consumption.

AI-Enabled Bedside Placement Confirmation Devices

The FDA urged adoption of objective confirmation in 2024 after litigation payouts topped USD 300 million. Cortex Medical’s deep-learning X-ray algorithm, commercialized through Avanos in January 2025, flags malposition with 97.3% sensitivity and trims time-to-feeding by 3.2 hours. CMS assigned a new CPT code reimbursing USD 42 per AI verification, removing cost barriers for hospitals performing 15 or more placements weekly. Early adopters cut tube-related adverse events by 64%, thereby reducing malpractice premiums.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Complications Hindering Growth | -0.9% | Global, acute impact in North America and Europe due to litigation and quality reporting | Short term (≤2 years) |

| Shift Toward PEG & Other Alternate Feeding Routes | -0.7% | North America, Europe, urban centers in APAC | Medium term (2-4 years) |

| Supply-Chain Volatility in Polyurethane & Silicone Resins | -0.4% | Global, peak disruption in Asia-Pacific manufacturing hubs | Short term (≤2 years) |

| Environmental Regulations on Single-Use Plastics | -0.2% | Europe, select North American states, emerging in APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Complications Hindering Adoption

Aspiration pneumonia occurs in 3.2% of placements and extends the length of stay by 4.7 days, adding USD 8,200 per episode.[3]American Journal of Gastroenterology, “Complications of Nasogastric Feeding,” ajg.org Tube dislodgement within 72 hours reaches 14% in ICU settings, consuming nursing hours and delaying calorie goals. Sentinel-event data log 47 unintended bronchial intubations in 2025, up 12% from 2023, elevating malpractice premiums 9% for non-compliant facilities. Patient discomfort drives early removal in 38% of home-care cases, risking readmissions. Collectively, these events temper the growth of procedures until mitigation technologies mature.

Shift Toward PEG and Other Alternate Feeding Routes

ESPEN’s 2025 guidelines elevate percutaneous endoscopic gastrostomy (PEG) to first-line status beyond 30 days of feeding, citing 41% fewer infections and 23% lower 90-day mortality compared with prolonged nasogastric feeding. Medicare raised PEG placement fees 8.2% for 2025, signaling payer preference for durable solutions. A JAMA Surgery cohort of 2,800 stroke patients corroborated lower mortality with early PEG transition. Jejunostomy placements in post-gastrectomy settings grew 14% in 2024, further fragmenting long-term enteral options. These shifts could erode 8–12% of chronic nasogastric demand by 2029.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialty Tubes Gain Amid Safety Mandates

Levin tubes captured 45.11% of the 2025 volume, underscoring their dominance in acute decompression and cost-sensitive markets. The nasogastric tube market size for Levin designs remains resilient as sub-USD 5 pricing aligns with high-turnover wards. Specialty tubes, electromagnetic-tipped, pH-sensing, and dual-lumen, are projected to post a 6.48% CAGR, buoyed by hospital policies that now mandate objective confirmation in non-emergent placements. The FDA safety communication issued in 2024 accelerated adoption; 38% of U.S. hospitals require electromagnetic guidance, creating predictable demand for higher-margin devices.

Enhanced features justify the premium pricing of USD 18–25 per unit. Medtronic’s Kangaroo ePump integrates a wireless pH sensor that alerts staff to dislodgement and helps early adopters cut adverse events by 52%. Dual-lumen Salem-sump tubes are used in bariatric and upper-GI surgery, supported by 2025 ASMBS guidelines that standardize their use. In neonatal ICUs, electromagnetic guidance reduces perforation risk to 0.1%, outweighing the cost premium. Collectively, technology embeds defensible margins into a historically commoditized segment.

By Material: Silicone Advances on Biocompatibility Standards

Polyurethane retained 37.87% of 2025 demand and dominates short-term decompression due to favorable cost-performance ratios. However, ISO 10993 revisions tightened extractable thresholds, propelling silicone to a 7.12% CAGR through 2031. The nasogastric tube market share for silicone expands as long-duration placements shift procurement toward inert materials. Clinical trials show that silicone reduces nasal ulcers by 47% and discomfort scores by 31% by week 3, findings that informed the U.K. National Health Service’s 2025 directive specifying silicone for insertions lasting more than 10 days.

PVC is exiting European public hospitals after 2026 due to Single-Use Plastics levies, boosting silicone volumes despite a 40% price premium. Chinese resin capacity additions by 2027 are expected to trim silicone costs by 12–15%, narrowing the gap with polyurethane. Polyurethane remains entrenched in emergency departments, where 24–48-hour residence times render biocompatibility upgrades less compelling.

By Indication: Drug Delivery Surges Amid Oncology Protocols

Dysphagia led 2025 volumes at 45.72%, driven by stroke and neurodegenerative diseases. Yet drug and nutrient administration is tracking an 8.87% CAGR, fueled by oncology protocols that bypass oral mucositis. The American Society of Clinical Oncology recommends enteral feeding during chemoradiation for head-and-neck cancer, expanding the nasogastric tube market in oncology.

Prophylactic tube placement reduced treatment interruptions by 29% and elevated 6-month progression-free survival by 11 points in a 2024 Lancet Oncology study. Enhanced recovery after surgery (ERAS) limits decompression to 24 hours, curbing dwell times but increasing annual throughput as surgical volume rises. Poison-control-driven lavage is declining, but remains a residual niche.

By End-User: Home Healthcare Ascends on Reimbursement Reforms

Hospitals generated 61.13% of 2025 revenue, reflecting centralized critical care. The nasogastric tube market size in home settings, however, is advancing at a 7.39% CAGR as CMS removed prior authorization and added USD 1.2 billion in annual claims for chronic dysphagia. Private insurers reimbursing at 85% of inpatient rates further accelerate transitions.

Virtual nursing programs from Fresenius Kabi cut unplanned visits by 31%, demonstrating scalable support models. Long-term care facilities maintain a mid-teen share, but PEG adoption tempers volume growth. Ambulatory surgical centers, buoyed by rising bariatric activity, widen institutional diversity.

Geography Analysis

North America held 35.03% of 2025 revenue. The United States, with 5,800 acute-care hospitals, benefits from AI confirmation reimbursement and expanded home-therapy coverage, trends expected to add 180,000 placements by 2028. Canada earmarked USD 310 million in 2024 for enteral programs aimed at cutting readmissions by 25%. Mexico’s bariatric procedures reached 78,000 in 2024 and are climbing 9.1% annually, supported by medical tourism flows.

Asia-Pacific registers the fastest CAGR of 9.39%. China approved 47 new devices in 2025, and India commissioned 12 manufacturing clusters under its Production-Linked Incentive scheme. Japan’s subsidies reduced co-pays, driving a 14.2% rise in home placements. Australia shortened AI device review cycles to 9 months, improving innovation velocity.

Europe faces cost pressure from polymer levies and PVC bans effective in 2026, steering demand toward silicone. GCC countries add ICU beds under Vision 2030, while the UAE mandates electromagnetic verification in public hospitals. Brazil procured 1.8 million tubes in 2024, but currency volatility hampers upgrades.

Competitive Landscape

The five leading vendors, Avanos Medical, Fresenius Kabi, Medtronic, B. Braun, and Cardinal Health, collectively held significant global revenue, confirming moderate concentration. Premium suppliers embed AI, electromagnetic tracking, and pH sensors into tubes priced at USD 18–25, while Asian manufacturers target cost leadership below USD 5. Avanos’ 2025 integration of Cortex Medical’s X-ray algorithm reduced adverse events by 64% and cut time-to-feeding by 3.2 hours, showcasing technology as a market differentiator.

Patent filings rose to 23 in 2024, covering wireless sensors and biodegradable coatings. Fresenius Kabi’s virtual nursing platform elevated caregiver confidence 42 points, underscoring service as a retention lever. Chinese and Indian challengers secure public tenders with ISO 13485 certification at 40–50% discounts, pressuring mid-tier Western firms. Regulatory compliance expenses climb under EU MDR and FDA post-market surveillance, tilting the advantage toward incumbents with mature quality systems.

Nasogastric Tube Industry Leaders

Becton, Dickinson and Company

Baxter International Inc.

Fresenius Kabi AG

Medtronic

Cardinal Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ICP DAS-BMP announced participation in WHX Dubai 2026 to showcase medical-grade TPU for enteral devices.

- January 2026: ENvue Medical launched a program using vibration technology from NanoVibronix to reduce discomfort from indwelling tubes.

- July 2024: Dale Medical Products released UltraGrip, a securement device for nasogastric tubes, available worldwide from mid-July 2024.

Global Nasogastric Tube Market Report Scope

The Nasogastric Tube Market refers to the global industry involved in the manufacturing, distribution, and sale of nasogastric (NG) tubesthin, flexible medical devices inserted through the nose, nasopharynx, and esophagus into the stomach. These tubes are primarily used for enteral nutrition (delivery of food/nutrients), medication administration, gastric decompression (removal of air/liquids), or diagnostic purposes in patients unable to eat orally due to conditions such as chronic diseases, malnutrition, surgery, or critical illness.

The nasogastric tube market report is segmented by product type into Levin tubes, Salem-sump tubes, other specialty tubes, technology into polyvinyl chloride, polyurethane, silicone, indication into dysphagia & swallowing disorders, and more, end user into hospitals, long-term care facilities, and more, and geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are in Value (USD).

| Levin Tubes |

| Salem-Sump Tubes |

| Other Specialty Tubes |

| Polyvinyl Chloride |

| Polyurethane |

| Silicone |

| Dysphagia & Swallowing Disorders |

| Gastrointestinal Decompression |

| Drug & Nutrient Administration |

| Others |

| Hospitals |

| Long-term Care Facilities |

| Ambulatory Surgical Centers |

| Home Healthcare Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Levin Tubes | |

| Salem-Sump Tubes | ||

| Other Specialty Tubes | ||

| By Material | Polyvinyl Chloride | |

| Polyurethane | ||

| Silicone | ||

| By Indication | Dysphagia & Swallowing Disorders | |

| Gastrointestinal Decompression | ||

| Drug & Nutrient Administration | ||

| Others | ||

| By End-user | Hospitals | |

| Long-term Care Facilities | ||

| Ambulatory Surgical Centers | ||

| Home Healthcare Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the medical shoe covers market expected to grow through 2031?

The market is projected to advance at a 4.28% CAGR, moving from USD 642.98 million in 2026 to USD 792.83 million by 2031.

Which region presents the strongest growth opportunity?

Asia-Pacific is forecast to expand at a 7.86% CAGR, driven by new hospital construction in China, India, and Southeast Asia.

Why are reusable shoe covers gaining interest?

Facilities processing high volumes can cut per-use cost to USD 0.06 after 75 laundry cycles, aligning with sustainability targets without sacrificing barrier performance.

What material trend should suppliers monitor closely?

Nylon variants are outpacing other materials with a 5.43% CAGR, as they resist tearing and work smoothly with automated dispensers.

How are digital procurement platforms reshaping purchasing behavior?

E-commerce portals from Medline and Cardinal Health reduce unit costs by up to 12% through volume aggregation and automated reordering, accelerating adoption among mid-sized hospital networks.

Page last updated on: