Phoenix Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

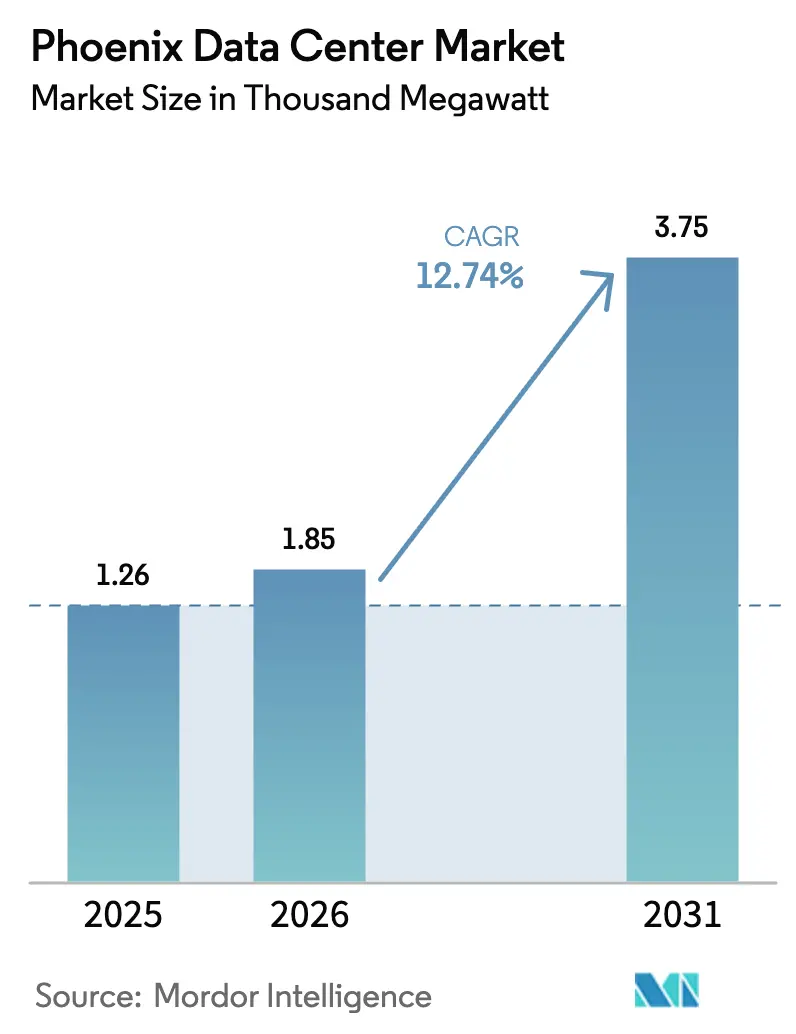

| Base Year Market Size (2025) | 1.26 Thousand megawatt |

| Market Volume (2026) | 1.85 Thousand megawatt |

| Market Volume (2031) | 3.75 Thousand megawatt |

| Growth Rate (2026 - 2031) | 12.74% CAGR |

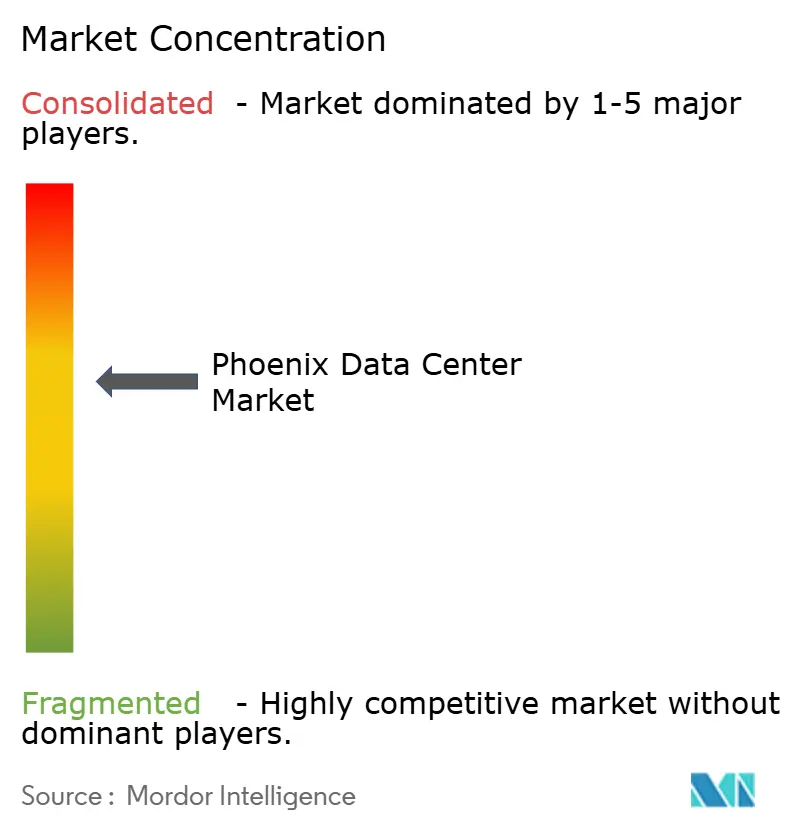

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Phoenix Data Center Market Analysis by Mordor Intelligence

Phoenix data center market size in 2026 is estimated at 1.85gigawatt, growing from 2025 value of 1.25 gigawatt with 2031 projections showing 3.75 gigawatt, growing at 12.74% CAGR over 2026-2031. Growth stems from the convergence of hyperscale artificial intelligence (AI) workloads, a rapidly expanding semiconductor base, and cost-competitive renewable energy. Power-dense AI clusters, on-site microgrids, and a ten-year sales-tax waiver on IT equipment encourage rapid facility roll-outs. Operators also benefit from average electricity prices that sit 20% below California rates and a low-risk climate that avoids earthquakes and hurricanes. As a result, the Phoenix data center market continues to attract flagship deployments from Microsoft, Google, Amazon, and Meta while simultaneously drawing enterprise relocations out of constrained coastal hubs.

Key Report Takeaways

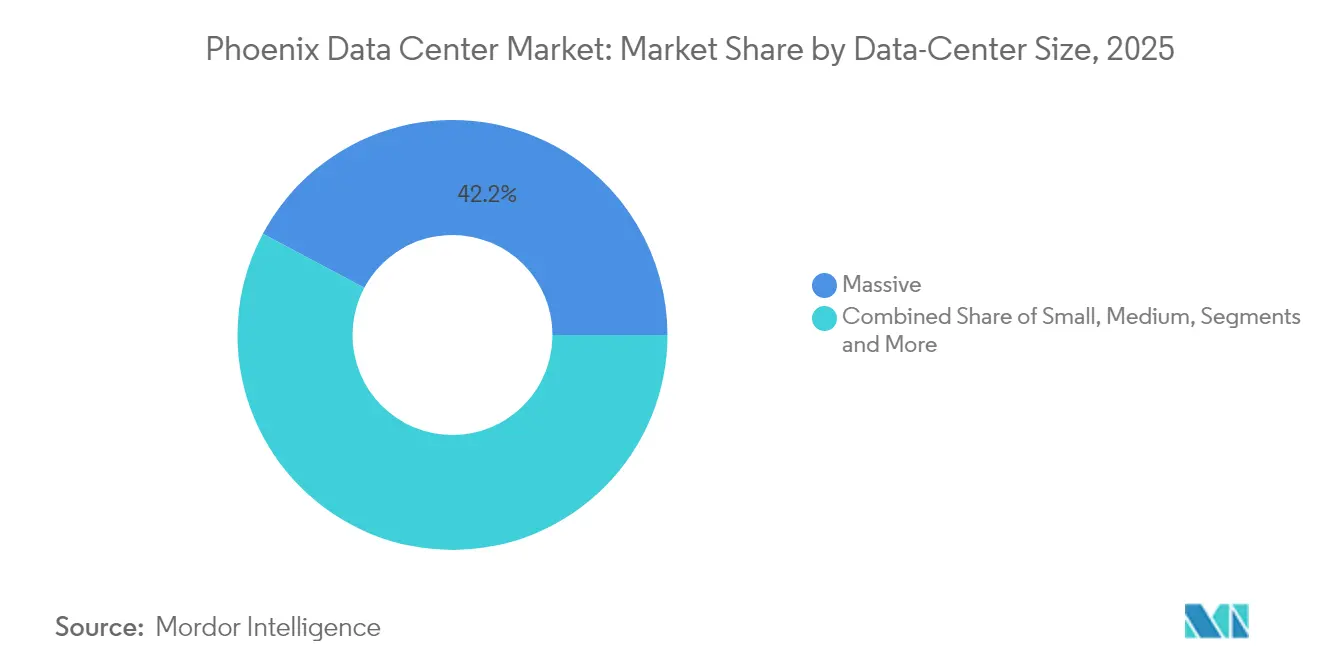

- By data-center size, large facilities commanded 42.19% of Phoenix data center market share in 2025 and are expanding at a 15.86% CAGR through 2031.

- By tier, Tier 4 infrastructure is set to grow at 16.74%—the fastest rate—while Tier 3 retained 76.22% share of Phoenix data center market size in 2025.

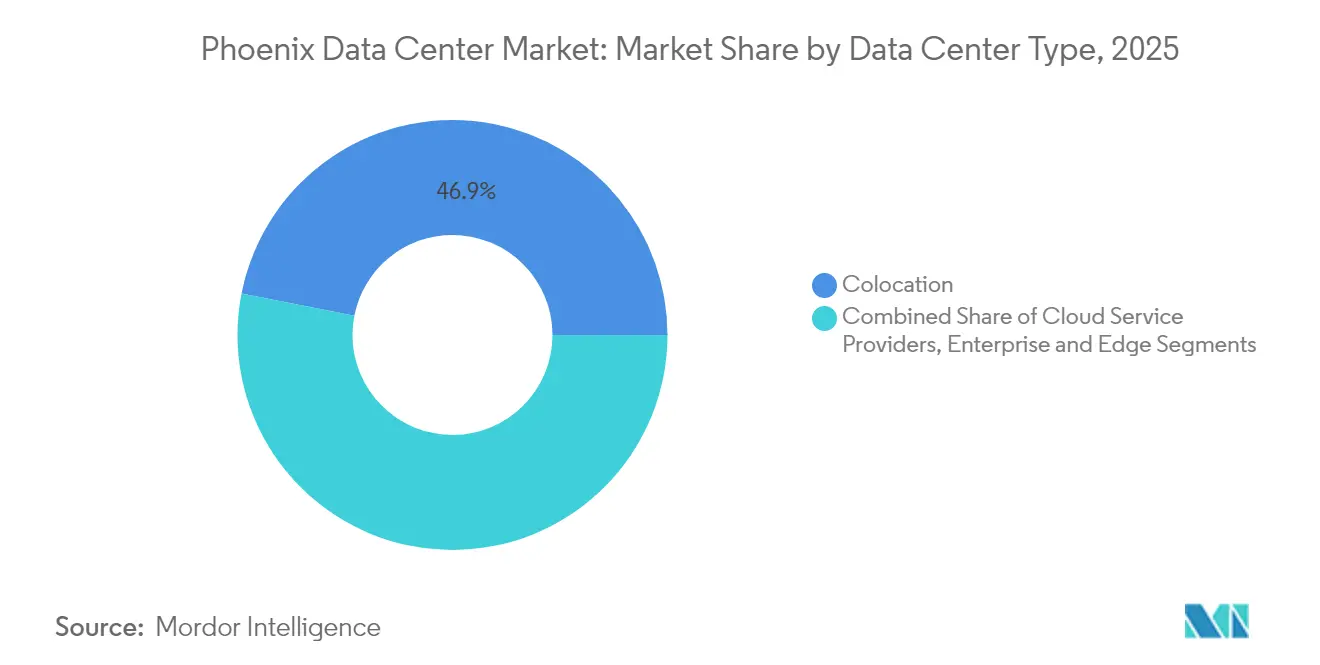

- By data-center type, colocation held 46.91% share in 2025, yet cloud service providers are advancing at an 17.82% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Phoenix Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging hyperscale and AI-driven demand | 4.2% | Global, concentrated in Phoenix metro | Short term (≤ 2 years) |

| Competitive power prices and renewable PPAs | 3.1% | Arizona statewide, spillover to Southwest | Medium term (2-4 years) |

| Ten-year sales-tax waiver on IT equipment | 2.3% | Arizona statewide | Long term (≥ 4 years) |

| Semiconductor fabs' edge-compute spill-over | 1.8% | Phoenix metro, Chandler corridor | Medium term (2-4 years) |

| Migration from CA seismic and water-restricted sites | 1.1% | California to Arizona corridor | Short term (≤ 2 years) |

| On-site microgrid deployment for rapid energization | 0.7% | Phoenix metro, utility-constrained areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging hyperscale and AI-driven demand

AI training clusters require up to 1,000 MW per campus—tenfold traditional deployments—prompting rapid land and power acquisitions across greater Phoenix. Microsoft’s Goodyear estate is engineered for high water-usage evaporative cooling, while Blackstone’s USD 25 billion outlay covers more than 60 football fields of floor area.[1]Data Center Dynamics Editorial Team, “Microsoft is building two huge data centers in Arizona,” datacenterdynamics.com Local semiconductor output by TSMC from 2025 shortens supply chains for GPUs, reinforcing a loop in which chips feed local AI workloads and spur even more capacity additions.

Competitive power prices and renewable PPAs

Arizona’s average electricity tariff is 20% below California and is falling further through innovative power-purchase agreements (PPAs) that bypass utility bottlenecks.[2]Kye Larkin, “Data centers reshape Phoenix’s economy,” azbigmedia.com Salt River Project (SRP) supports Google’s Mesa campus with a 260 MW solar-plus-storage farm, while Meta’s 200 MW Brittlebush Solar Park delivers dedicated green power. The American Clean Power Association values completed and committed clean-energy investments across the state at USD 13 billion.

Ten-year sales-tax waiver on IT equipment

Arizona expanded its Computer Data Center Program in 2024 to grant 10-year sales-tax exemptions on purchases above USD 50 million, saving hyperscalers millions over the life of each campus.[3]Dave Smith, “Arizona’s new data-center deal sweetens tax breaks,” datacenterknowledge.com The incentive applies to both colocation customers and owner-operated builds, widening its reach throughout the Phoenix data center market.

Semiconductor fabs’ edge-compute spill-over

TSMC’s three-fab, USD 165 billion project is bringing more than 62,000 jobs and large-scale edge computing needs for real-time analytics and defect detection. Intel’s legacy Chandler campus and AMD’s design wins further densify the local chip supply chain, locking in steady data-center demand for at least the next decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Utility power-queue bottlenecks | -2.8% | Phoenix metro, APS and SRP service areas | Short term (≤ 2 years) |

| Water-consumption scrutiny in desert climate | -1.9% | Arizona statewide, municipal oversight areas | Medium term (2-4 years) |

| Municipal push-back over heat-island rezoning | -1.3% | Phoenix city limits, suburban municipalities | Long term (≥ 4 years) |

| Transformer supply-chain delays for liquid-cooling | -0.9% | Global, acute in high-growth markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Utility power-queue bottlenecks

APS is already evaluating interconnection requests that exceed 13 GW against an existing grid that served just 7 GW in 2024, stretching approval cycles to as long as three years. To sidestep the queue, Aligned Data Centers adopted a 63 MW diesel microgrid capable of grid-island operation, while Vantage paired with VoltaGrid to secure 1 GW of on-site generation capacity.

Water-consumption scrutiny in a desert climate

Microsoft’s Goodyear campus drew headlines for projected withdrawals of tens of millions of gallons annually. Roughly 66% of all U.S. data-center projects underway since 2022 sit in areas of “high” or “extremely high” water stress. Response strategies include Edged Energy’s Mesa site, which eliminates evaporative cooling and claims annual savings of 94 million gallons edgedenergy.com, and Microsoft’s pledge to achieve zero-water data centers by 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Large Facilities Drive AI Transformation

Large campuses accounted for 42.19% of Phoenix data center market share in 2025 and captured the highest growth trajectory at 15.86% CAGR to 2031. The Phoenix data center market size for large builds is therefore set to rise well above 2.2 GW by the end of the decade. Operators deploy massive footprints to deliver contiguous power and efficient liquid-cooling loops that suit AI racks drawing 40 kW or more per cabinet. QTS is progressing on a 750 MW campus over 400 acres in the West Valley, while Tract is master-planning a USD 14 billion, 1,000-acre estate comprising 30 buildings.

Second-tier demand persists for sub-50 MW halls serving regional enterprises, yet hyperscale roadmaps dominate expansions. Mega campuses typically add dedicated substations, solar arrays, and gas-fired microgrids, as seen in Vantage-VoltaGrid’s 1 GW program. Edge-scale rooms closer to TSMC fabs complement the wider footprint by hosting low-latency analytics and robotics control.

By Tier Type: Tier 4 Facilities Accelerate for AI Workloads

Tier 3 remained the workhorse at a 76.22% slice of Phoenix data center market size in 2025, but Tier 4 is on track for a 16.74% CAGR through 2031 digitalrealty.com. Up-time guarantees jump from 99.982% (Tier 3) to 99.995% (Tier 4), a differential that becomes pivotal when AI training clusters can cost millions if interrupted mid-cycle. Digital Realty’s roadmap includes multiple Tier 4-ready halls in Mesa, while Aligned integrates Delta³ cooling to hit both Tier 4 resilience and energy-efficiency benchmarks.

Legacy facilities are investing in electrical redundancies and new chillers to reclassify halls from Tier 3 into Tier 4, attracting premium rates from CSP tenants. Meanwhile, Tier 1 and Tier 2 builds persist for lab workloads and dev-test sandboxes where downtime is less critical.

By Data Center Type: Cloud Service Providers Lead Growth

Colocation maintained 46.91% share of Phoenix data center market size in 2025, but CSPs exhibit the quickest expansion at 17.82% CAGR. Microsoft secured nearly 300 acres in El Mirage, Google filed to double its Mesa campus footprint, and Amazon continues to scout land along Interstate-10. Hyperscalers prefer Phoenix for multi-AZ availability zones that back up California regions without crossing multiple time zones.

Retail colocation remains vital for enterprises migrating legacy hardware, government agencies centralizing workloads, and fintechs requiring audited facilities. However, wholesale colocation is migrating toward “hyperscale-as-a-service,” where providers build entire halls to a single tenant’s specification. Edge and modular deployments have begun serving semiconductor fabs and public-sector IoT nodes, ensuring data locality and sovereignty.

Geography Analysis

Phoenix ranks as the second-largest data-center cluster in the United States, anchored by low seismic risk, dry climate, and a backbone of more than 40 carriers. The Phoenix data center market benefits from 5,500 MW of installed clean-energy capacity with 8,700 MW more in the queue—ample headroom for 400 MW-plus campuses while hitting renewable commitments.

Expansion is no longer limited to Maricopa County. Tucson’s USD 1.2 billion Project Blue will add 8-10 halls over 290 acres, complementing Phoenix while tapping a different labor pool. Across the state line, Google’s Henderson, Nevada build illustrates a Southwest multi-state strategy whereby operators arbitrage solar resources and transmission capacity datacenterknowledge.com.

California’s strained grid and water restrictions have already triggered a migration wave; Santa Clara alone hosts more than 50 facilities consuming 60% of city power, a trend nudging operators toward Arizona’s friendlier permitting environment. Fiber and power interconnections across the Desert Southwest tie Phoenix, Las Vegas, and Southern California into a resilient “sun belt” corridor for cloud growth.

Competitive Landscape

The Phoenix data center market features a core of incumbents—Digital Realty, Vantage, CyrusOne, QTS, Iron Mountain—supplemented by agile entrants leveraging liquid cooling and modular construction. Digital Realty booked record quarterly signings in Q4 2024, translating worldwide scale into regional momentum. Vantage secured USD 9.2 billion in fresh equity and paired with VoltaGrid to guarantee 1 GW of dispatchable on-site power, a differentiator amid grid bottlenecks.

Iron Mountain reported 20% year-over-year data-center revenue growth in Q1 2025—proof that established storage brands can effectively cross-sell cloud-adjacent infrastructure. Disruptors such as Edged Energy target AI-ready, water-free designs, while the Evoque-Cyxtera merger into Centersquare aggregates 320 MW across 50 locations, adding national reach to new Phoenix builds.

Competitive differentiation now hinges on three levers: renewable-rich PPAs that lower total-cost-of-ownership, innovative liquid-cooling systems that shrink land and water footprints, and microgrid architectures that bypass multiyear interconnection queues. Whitespace persists in semiconductor edge hubs, government cloud zones, and AI inference clusters where low-latency proximity to end users matters.

Phoenix Data Center Industry Leaders

Digital Realty Trust, Inc.

CyrusOne

Vantage Data Centers

Aligned Data Centers

EdgeCore Digital Infrastructure

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vantage Data Centers and McCarthy Building Companies topped out Phase II of their Goodyear campus, advancing a multi-building Phoenix expansion

- May 2025: QTS purchased 200 acres in Avondale, adding to prior 400-acre land banking for future hyperscale builds

- April 2025: Aligned Data Centers broke ground on a Phoenix facility featuring Delta³ cooling to serve AI demand

- April 2025: TSMC finished its second Arizona fab ahead of schedule, accelerating edge compute requirements

Phoenix Data Center Market Report Scope

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services and store and manage the data connected with those applications and services.

The Phoenix Data Center Market is segmented by DC size (small, medium, large, massive, mega), tier type (tier 1&2, tier 3, tier 4), absorption (utilized [colocation type [retail, wholesale, hyperscale], end user [cloud & IT, telecom, media & entertainment, government, BFSI, manufacturing, e-commerce]), and non-utilized). The market sizes and forecasts are provided in terms of value (MW) for all the above segments.

| Small |

| Medium |

| Large |

| Hyperscale |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Cloud Service Providers (CSPs) | |||

| Enterprise, Modular and Edge | |||

| Colocation | Non-Utilized | ||

| Utilized | Colocation Type | Retail | |

| Wholesale | |||

| End User | Cloud and IT | ||

| Telecom | |||

| Media and Entertainment | |||

| Government | |||

| BFSI | |||

| Manufacturing | |||

| E-Commerce | |||

| Other End User | |||

| By Data Center Size | Small | |||

| Medium | ||||

| Large | ||||

| Hyperscale | ||||

| By Tier Type | Tier 1 and 2 | |||

| Tier 3 | ||||

| Tier 4 | ||||

| By Data Center Type | Cloud Service Providers (CSPs) | |||

| Enterprise, Modular and Edge | ||||

| Colocation | Non-Utilized | |||

| Utilized | Colocation Type | Retail | ||

| Wholesale | ||||

| End User | Cloud and IT | |||

| Telecom | ||||

| Media and Entertainment | ||||

| Government | ||||

| BFSI | ||||

| Manufacturing | ||||

| E-Commerce | ||||

| Other End User | ||||

Key Questions Answered in the Report

What is the current size of the Phoenix data center market?

The market hosts 2.71 GW of deployed capacity as of 2026, second only to Northern Virginia.

How fast is the Phoenix data center market expected to grow?

Capacity is forecast to reach 4.93 GW by 2031, translating into a 12.74% CAGR over the 2026-2031 forecast period.

Why are hyperscale operators choosing Phoenix over California?

Arizona offers electricity prices 20% lower than California, ten-year sales-tax exemptions, and a lower risk profile for natural disasters.

Which segment is expanding the quickest within the Phoenix data center market?

Tier 4 facilities register the highest growth rate at 16.74% through 2031 as AI workloads demand maximum uptime.

How are operators addressing water use in a desert environment?

Providers are adopting waterless or refrigerant-based cooling, on-site microgrids for energy efficiency, and corporate pledges toward zero-water operations by 2026.

What role does the semiconductor industry play in Phoenix’s data-center boom?

TSMC’s USD 165 billion fab complex and Intel’s upgrades generate edge computing demand that directly feeds new data-center builds across the metro area.

Page last updated on: