Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

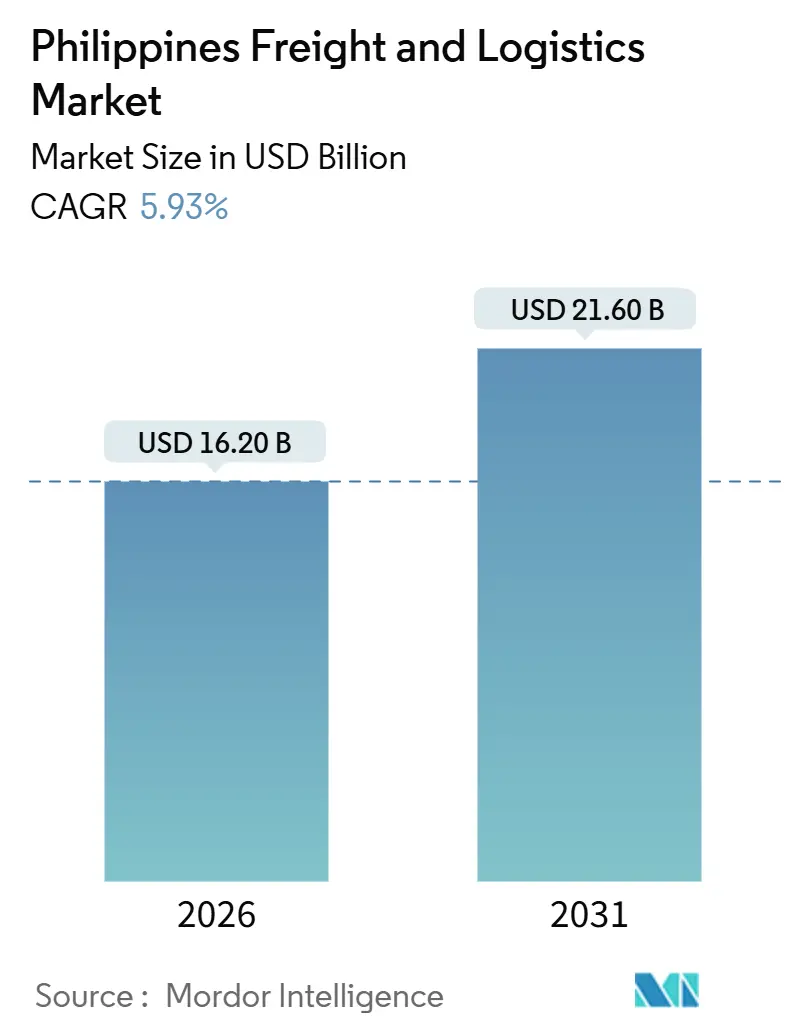

| Market Size (2026) | USD 16.20 Billion |

| Market Size (2031) | USD 21.60 Billion |

| Growth Rate (2026 - 2031) | 5.93% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Freight And Logistics Market Analysis by Mordor Intelligence

The Philippines freight and logistics market size is estimated at USD 16.20 billion in 2026, and is expected to reach USD 21.60 billion by 2031, at a CAGR of 5.93% during the forecast period (2026-2031). E-commerce adoption, flagship infrastructure spending, and resurgent export manufacturing are expanding shipment volumes across every transport mode, while digital platforms compress fulfillment lead times and lower search costs for shippers. Temperature-controlled capacity is moving up the investment queue as food and pharmaceutical flows require tighter environmental controls. Global integrators are scaling air-cargo hubs in Clark to capture high-value cargo, even as domestic truckers and coastal shippers leverage the Build Better More corridors to unlock underserved provincial lanes. At the same time, chronic Metro Manila congestion, high inter-island freight rates, and recurring typhoon disruptions shave cost competitiveness and push operators toward alternative gateways and risk-mitigation technologies.

Key Report Takeaways

- By logistics function, courier, express, and parcel services posted the fastest 6.82% CAGR between 2026-2031, while freight transport retained a 63.27% Philippines freight and logistics market share in 2025.

- By freight transport mode, road freight handled 67.45% of 2025 revenue, but air freight advanced at a leading 7.55% CAGR between 2026-2031, narrowing the gap with sea lanes.

- By CEP destination, domestic parcels held 64.98% of revenue in 2025; international parcels accelerated at 7.07% CAGR and will outpace domestic growth between 2026-2031.

- By warehousing temperature control, temperature-controlled capacity captured 8.41% of 2025 space and is set to grow at a 6.69% CAGR between 2026-2031, outstripping ambient facilities.

- By freight forwarding mode, sea and inland waterways controlled 58.20% of 2025 values, but air forwarding rose at a 6.76% CAGR between 2026-2031 on the strength of electronics and pharma traffic.

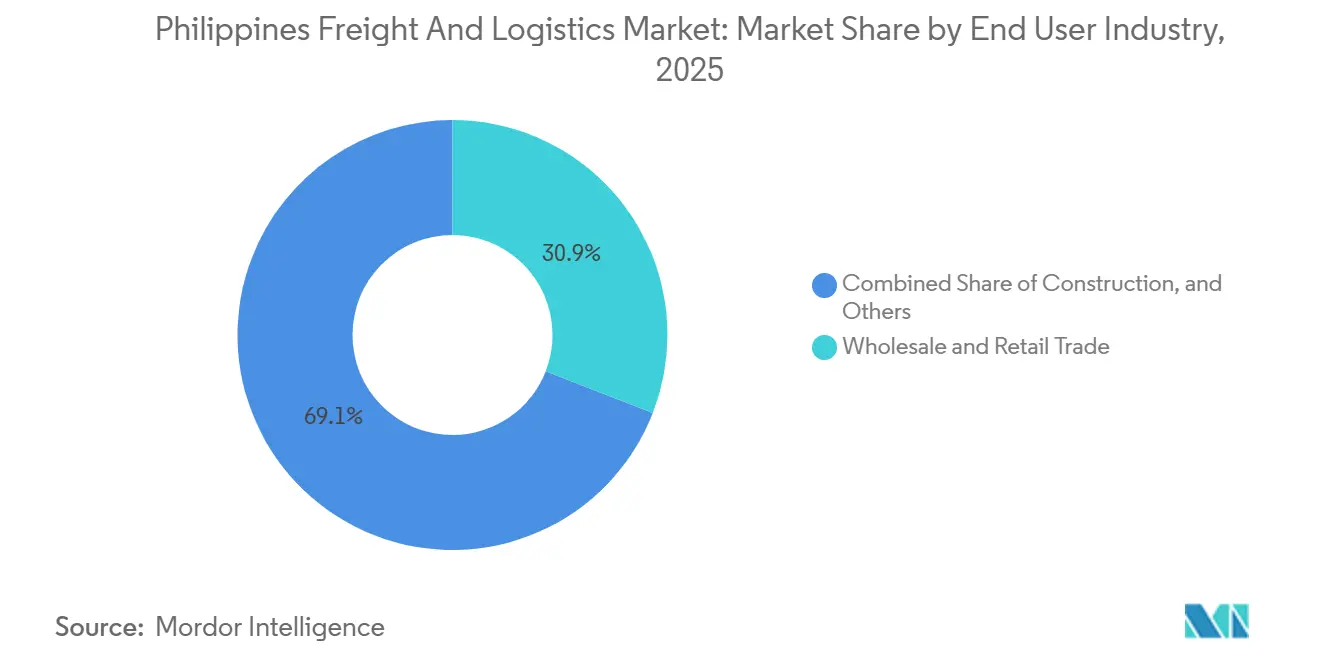

- By end-user industry, wholesale and retail trade led with 30.91% of the Philippines freight and logistics market size in 2025, expanding at a sector-high 6.52% CAGR between 2026-2031, as modern trade penetrated Visayas and Mindanao.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Freight And Logistics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in B2C e-commerce parcel volumes | +1.2% | National, with concentration in Metro Manila, Calabarzon, Central Luzon | Short term (≤ 2 years) |

| Build Better More infrastructure pipeline | +1.4% | National, prioritizing Luzon connectivity, Mindanao road networks | Long term (≥ 4 years) |

| Manufacturing re-shoring within ASEAN | +0.9% | Calabarzon, Central Luzon, Cebu | Medium term (2-4 years) |

| Growth in temperature-controlled food and pharma flows | +1.1% | National, early gains in Metro Manila, Cebu, Davao | Medium term (2-4 years) |

| Expansion of digital freight-matching platforms | +0.6% | National, urban adoption in Metro Manila, Cebu | Short term (≤ 2 years) |

| Nickel-ore exports for EV battery supply chains | +0.8% | Mindanao (Surigao, Palawan), reverse logistics to mining zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Surge in B2C E-Commerce Parcel Volumes

E-commerce gross merchandise value climbed to USD 21 billion in 2025 as 73% of adult Filipinos shopped online, generating a step-change in last-mile activity. Ninja Van’s 2025 tie-up with Universal Robina embeds scan-to-print fulfillment inside fast-moving consumer-goods channels, cutting South Luzon order cycles to under 24 hours. Domestic CEP held 64.98% of 2025 parcels, yet cross-border flows are expanding faster because Clark and Manila gateways now clear most ASEAN parcels within a single day under the National Single Window. Integrated operators that combine warehouse management, sortation, and delivery on a unified software stack capture price premiums and higher asset turns. Pure-play couriers without warehousing depth face commoditization as shippers demand bundled solutions[1]“E-Commerce and Retail Trade Statistics,” Department of Trade and Industry, dti.gov.ph .

Build Better More Infrastructure Pipeline

The PHP 8.3 trillion (USD 143.23 billion) Build Better More program has locked in infrastructure spending near 6% of GDP, with 83% of its 194 flagship projects targeting roads, bridges, ports, and airports. The New Manila International Airport, due in 2028, will handle up to 5 million tons of freight a year, creating a multimodal node that rivals Bangkok and Ho Chi Minh City. Subic Bay’s berth expansion and the Mindanao Railway ring will divert cargo away from Metro Manila choke points, reducing long-haul domestic ton-kilometer costs by up to 18%. These corridors improve equipment utilization for trucking fleets and unlock backhaul opportunities for domestic forwarders, while coastal shippers must lower tariffs to remain competitive[2]“Build Better More Infrastructure Program,” Department of Budget and Management, dbm.gov.ph.

Growth in Temperature-Controlled Food and Pharma Flows

The Department of Agriculture placed PHP 3 billion (USD 51.77 billion) in 2024 for 99 provincial cold stores aimed at trimming post-harvest waste by one-third. Maersk’s Optimus Distribution Center opened in late 2024 with 76,000 pallet positions and LEED credentials, signaling multinational demand for sustainable temperature-controlled warehousing. Frabelle’s Navotas blast-freezing hub and Royale Cold Storage’s 2025 Bulacan mega-site expand provincial capacity, while ASEAN pharma harmonization lets a single Philippine hub distribute vaccines to 10 member states. Cold-chain capacity is slated to grow 6.69% to 2031, outpacing ambient space and raising service expectations across seafood, meat, and biologics lanes.

Nickel-Ore Exports for EV Battery Supply Chains

With 23.3 million wet metric tons shipped in 2024, the Philippines ranked second in global nickel-ore output, earning USD 1.2 billion in export receipts. Every outbound ton triggers up to 2.2 tons of inbound machinery and reagent freight into Surigao and Palawan mine sites, lifting Mindanao’s freight volumes above historical norms. As producers shift to high-pressure acid leach processing, chemical-grade temperature control becomes mandatory, blending bulk commodities with cold-chain requirements. Forwarders packaging ore exports, reagent imports, and equipment reverse-logistics under long-term contracts will lock in predictable revenue, while pure vessel brokers absorb rate volatility.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic road congestion in Metro Manila | -0.7% | Metro Manila, Calabarzon spillover | Short term (≤ 2 years) |

| High domestic shipping costs across islands | -0.5% | Visayas, Mindanao, island provinces | Medium term (2-4 years) |

| Typhoon-induced supply-chain disruptions | -0.6% | Bicol, Eastern Visayas, Northern Luzon | Short term (≤ 2 years) |

| Limited uptake of cargo insurance among SMEs | -0.3% | National, acute in provincial routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Road Congestion in Metro Manila

Peak-hour speeds of 12–15 kilometers per hour in 2024 impose PHP 3.5 billion (USD 60.39 million) in daily economic losses, with cold-chain breaches costing pharma distributors up to PHP 200,000 (USD 3,451) per incident. Operators are repositioning hubs to Clark and Laguna, lowering land costs by as much as 60% and raising average speeds to 60 kilometers per hour. Cabotage relaxation aims to divert 15% of inter-regional freight to coastal shipping, yet domestic shipowner resistance has delayed full roll-out. Until the Metro Manila Subway becomes operational post-2028, the congestion premium on urban deliveries will persist[3]“Traffic and Congestion Statistics,” Metropolitan Manila Development Authority, mmda.gov.ph .

Typhoon-Induced Supply-Chain Disruptions

Typhoon Kristine in October 2024 caused USD 126.5 million in crop losses and halted 2GO sailings for three days, stranding 18,000 tons of perishables. With 20 cyclones on average each year, cargo insurance uptake below 15% leaves SMEs self-insured and vulnerable. Although larger carriers deploy weather-routing analytics that cut storm delays by 18%, 600-plus small vessel operators lack the capital for such tools. The absence of a national catastrophe pool shifts risk to retailers and farmers, eroding thin margins and prolonging recovery times[4]“Typhoon Kristine Damage Assessment,” National Disaster Risk Reduction and Management Council, ndrrmc.gov.ph.

Segment Analysis

By End-User Industry: Retail Leads, Mining Surges

Wholesale and Retail Trade generated 30.91% of 2025 demand and grew at a 6.52% CAGR (2026-2031), lifted by modern grocery chains spreading into Visayas and Mindanao. Manufacturing follows, buoyed by a PMI above 53 since 2024 and USD 42 billion in electronics exports.

Oil, gas, and mining carry outsize logistics intensity, particularly nickel-ore lanes that require inbound reagents and spare parts. Construction demand remains stable, keyed to USD-indexed steel and cement inflows for 194 flagship projects. Agriculture freight will climb as cold-chain coverage lowers spoilage on high-value perishables.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Logistics Function: CEP Gains Momentum

Courier, Express, and Parcel activity is expected to rise at 6.82% CAGR between 2026-2031, while Freight Transport still commanded a 63.27% Philippines freight and logistics market share in 2025. The Philippines freight and logistics market size for CEP will climb as integrated sortation-fulfillment models truncate delivery windows and bundle value-added services. Partnerships like Ninja Restock demonstrate that embedding logistics inside consumer-goods distribution compresses the delivery curve and raises parcel density. Non-temperature-controlled warehousing still hosts 91.59% of inventory, yet cold-chain nodes capture outsized capital because food spoilage and pharma compliance impose hard cost ceilings on service lapses. Digital freight platforms are steering customs brokerage and freight insurance toward single-click transactions, lowering administrative overheads and giving SMEs direct access to multicarrier networks.

Temperature-controlled warehousing capacity, while representing a modest 8.41% share, is expanding at 6.69% as the Department of Agriculture backs 99 new cold rooms and private investors add pallet positions in Navotas, Bulacan, and Cebu. The Philippines freight and logistics market size devoted to cold chain is therefore widening its share faster than ambient space, supported by pharmaceutical supply chains aligned under ASEAN regulations. Freight Forwarding volumes reflect the archipelago’s reliance on sea channels, but the fastest lane growth now flows through air as electronics and biologics shippers buy speed to protect value.

By CEP Destination: Cross-Border Parcels Accelerate

Domestic parcels held 64.98% of 2025 values, but international traffic is scaling faster at 7.07% CAGR between 2026-2031 as regional e-commerce sellers leverage four-hour flight radii to reach 60% of ASEAN consumers. The National Single Window condenses 14 clearances into a one-day digital process, trimming border dwell time and raising shipment visibility. Ninja Van’s Cabuyao automation center sorts half a million parcels daily, embedding customs clearance workflows to sustain same-day handoffs to airlines. For domestic flows, organized retail’s expansion in Visayas and Mindanao pushes CEP operators into provinces historically overlooked, creating greenfield capacity for high-growth lanes.

Mindanao’s growth trajectory exceeds the national average due to reverse-logistics loops tied to nickel-ore exports. Every ore ton exported requires inbound equipment and reagents, elevating parcel movements in mining districts. The Philippines freight and logistics industry, therefore, finds new revenue streams at the intersection of minerals and e-commerce, rewarding carriers that mesh bulk, parcel, and spare-parts flows on a unified network.

By Warehousing Temperature Control: Cold Chain Scales

Non-temperature-controlled facilities still host 91.59% of revenue in 2025, but the cold-chain segment is growing at 6.69% CAGR (2026-2031), nearly matching the overall 5.93% market CAGR (2026-2031) as retailers and manufacturers tighten quality requirements. The Philippines freight and logistics market size for temperature-controlled warehousing will climb in step with government and private investments.

Department of Agriculture funding lowered entry barriers for provincial stores, while private projects in Bulacan and Cebu added thousands of sub-zero pallet slots. ASEAN pharma harmonization lets a single compliant hub reach 10 economies, creating economies of scale and justifying premium rents. Ambient warehouses remain vital for fast-moving consumer goods, but cross-docking and micro-fulfillment layouts are emerging as e-commerce players chase two-day nationwide delivery.

By Freight Transport Mode: Air Narrows the Gap

Road freight still lifted 67.45% of 2025 revenue, yet air values are compounding at 7.55% CAGR (2026-2031), propelled by USD 42 billion in electronics exports and strict time-temperature profiles on biologics. FedEx’s 34,000-square-meter Clark ramp and UPS’s incoming facility will sharpen air-cargo service reliability, allowing shippers to bypass Manila’s saturation. Sea and inland waterways, at 25% of tonnage, remain critical for bulk and inter-island trades, although high tariff structures tied to limited vessel competition drag on modal shift. Pending cabotage reforms promise 10–15% rate relief if fully executed. Rail still accounts for under 1% of freight, but the Mindanao Railway’s 2028 debut will provide a land bridge across commodity corridors, introducing competition to coastal routes.

In the short term, road remains the backbone of the Philippines freight and logistics market, but the Build Better More highway grid is reshaping route economics, handing cost advantages to carriers able to stage inventory outside Metro Manila. The Philippines freight and logistics market share of air cargo is set to creep upward as customs digitalization trims dwell times, improving aircraft utilization and lowering per-kilo costs for shippers of semiconductors, perishables, and relief goods.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Freight Forwarding Mode: Air Chases Sea

Sea forwarding retains a 58.20% revenue share in 2025, but air forwarding, advancing at 6.76% CAGR (2026-2031), edges closer as shippers of electronics and pharma pay four-fold rate premiums to guarantee 48-hour transit. FedEx and UPS expansions in Clark anchor capacity, while 2GO’s ship re-fleet raises roll-on/roll-off capacity 35%, tightening domestic competition. Pending foreign-flagged vessel access promises to shave coastal rates, yet union and owner lobbying has delayed rollout.

Rail and multimodal chains gain traction once the Mindanao line opens, delivering a land alternative that erodes the sea’s dominance on specific corridors. For now, the Philippines freight and logistics market relies on sea for heavy and bulk cargo, but air and multimodal solutions will skim higher-margin traffic.

Geography Analysis

Metro Manila and Calabarzon processed 70% of 2025 container traffic, but congestion-induced logistics costs plus limited developable land push operators to Clark, Laguna, and Subic. Clark’s tax-free zone and 24/7 runway attract air-cargo specialists, while Subic’s deepwater berths capture shippers willing to truck 120 kilometers to skip Manila port queues. The Build Better More corridors allocate the majority of road capex to Luzon, yet Mindanao wins share through the railway and strategic mining exports. Visayas leverages Cebu’s port-airport complex, and new cold stores in Consolacion help pharma distributors reach central islands with two-day service.

Inter-island shipping costs remain 30-40% above ASEAN norms due to limited foreign vessel competition, but targeted cabotage relaxation could trim tariffs by 15% if fully enacted. Temperature-controlled warehousing outside Metro Manila and Cebu sits below 12% of national capacity, yet 99 new cold rooms will redistribute space across Central Luzon, Ilocos, and Cagayan Valley. The New Manila International Airport will give shippers a multimodal platform with five-million-ton capability, slashing relay times and rebalancing traffic away from the port.

Mindanao’s freight flows will outpace the national rate as nickel exports and agro-industrial investments deepen, creating premium volume for trucking and air cargo. Typhoon corridors across Bicol and Eastern Visayas inject volatility into routing plans, sending carriers to secondary ports in dry months and driving investment in weather analytics.

Competitive Landscape

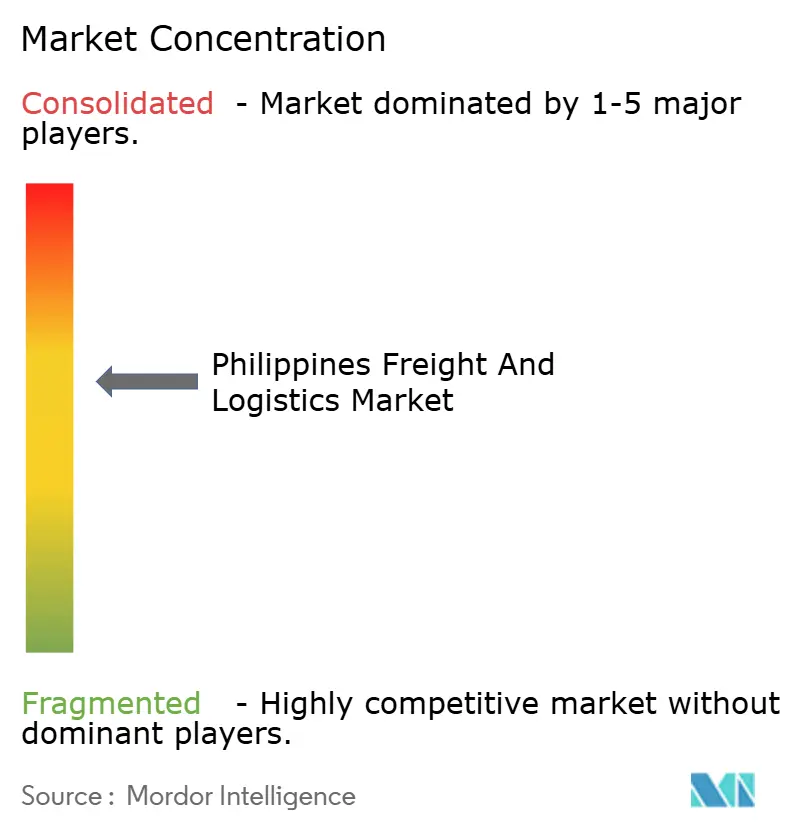

The top five operators capture roughly 35–40% of 2025 revenues, making the Philippines freight and logistics market moderately fragmented. FedEx doubled its Clark footprint to 34,000 square meters, and UPS will open a new hub in late 2026 as part of a USD 250 million Asia-Pacific investment. Maersk’s PHP 4.8 billion (USD 82.83 million) Optimus Center in Calamba targets pharma and electronics, integrating WMS tech that cuts pick errors 35%.

Ayala Corporation’s PHP 1.5 billion (USD 25.88 billion) exit from Air21 highlights last-mile density challenges beyond Metro Manila. Ninja Van’s B2B pivot with Universal Robina embeds fulfillment in FMCG distribution, squeezing traditional wholesalers.

Digital startups such as Locad raised USD 9 million in late 2024, scaling six fulfillment nodes that promise one-to-two-day nationwide delivery. White-space opportunities concentrate in Visayas and Mindanao cold chain, where capacity shortages run 25–30%. Compliance demands under ISO 9001 and new cabotage rules will accelerate consolidation among undercapitalized mid-tier forwarders.

Philippines Freight And Logistics Industry Leaders

SM Investments Corp. (including 2GO Group)

LBC Express Holdings, Inc.

DHL Group

Royal Cargo

DSV A/S (including DB Schenker)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Ayala Corporation sold its 60% Air21 stake for PHP 1.5 billion (USD 25.88 million) after provincial parcel density proved uneconomic.

- October 2025: Royale Cold Storage began a USD 130 million Bulacan facility spanning 1.5 hectares and targeting Metro Manila and Central Luzon pharma and food flows.

- April 2025: DSV A/S finalized the EUR 14.3 billion (USD 15.78 billion) takeover of DB Schenker, creating the world’s largest freight forwarder and broadening service scope in the archipelago.

- January 2025: Ninja Van partnered with Universal Robina on Ninja Restock, delivering South Luzon orders within 24 hours.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Philippines freight and logistics market as gross revenue earned from moving and handling goods within, into, and out of the country through road, sea and inland waterway, air, and rail freight transport, freight forwarding, courier-express-parcel, warehousing, and related third-party value-added services. We value flows at contractual prices before VAT and after customary trade discounts.

Scope Exclusions: Passenger transport, purely captive in-house logistics, and standalone warehouse real-estate rents are outside this study.

Segmentation Overview

- By End-User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining, and Quarrying

- Wholesale and Retail Trade

- Others

- By Logistics Function

- Courier, Express, and Parcel (CEP)

- By Destination Type

- Domestic

- International

- By Destination Type

- Freight Forwarding

- By Mode of Transport

- Air

- Sea and Inland Waterways

- Others

- By Mode of Transport

- Freight Transport

- By Mode of Transport

- Air

- Pipelines

- Rail

- Road

- Sea and Inland Waterways

- By Mode of Transport

- Warehousing and Storage

- By Temperature Control

- Non-Temperature-Controlled

- Temperature-Controlled

- By Temperature Control

- Other Services

- Courier, Express, and Parcel (CEP)

Detailed Research Methodology and Data Validation

Primary Research

Interviews with freight forwarders, 3PL managers, airline cargo chiefs, e-commerce retailers, and regulators across Luzon, Visayas, and Mindanao refine modal shares, rate corridors, and short-term demand signals that desktop sources alone cannot reveal.

Desk Research

We start by downloading official time-series from the Philippine Statistics Authority, Bureau of Customs, Department of Transportation traffic counts, and Philippine Ports Authority tonnage logs. We then enrich them with World Bank Logistics Performance Index scores and papers from the Supply Chain Management Association of the Philippines. Congressional budget briefs and port operator notices clarify capacity pipelines and tariff revisions. Proprietary sweeps through D&B Hoovers and Dow Jones Factiva let our team cross-check carrier revenues and deal news. These examples show depth, while many other references support verification.

A second pass tracks e-commerce parcel volumes, diesel price trends, warehouse vacancy, and peso-dollar movements so demand drivers and cost modifiers entering the model rest on verified public indicators.

Market-Sizing & Forecasting

Our analysts launch a top-down build that reconstructs 2024 freight expenditure from supply-use tables, port and road ton-kilometer data, and average tariff surveys. Selective bottom-up checks, supplier roll-ups, and sampled average selling price multiplied by volume fine-tune informal and cross-border flows. Core variables such as GDP growth, infrastructure outlays, parcel counts, diesel index, and cold-chain capacity drive a multivariate regression projecting values through 2030. Gaps in evidence are bridged with three-year moving averages from comparable ASEAN corridors.

Data Validation & Update Cycle

Outputs face variance tests against alternate trade, tax, and carrier capacity series. Deviations above three percentage points trigger analyst review and call-backs. Reports refresh every twelve months, and interim updates follow major policy shifts or industry deals.

Why Mordor's Philippines Freight and Logistics Baseline Stand Firm and Reliable

Published estimates often differ because firms adopt varying service boundaries, exchange-rate cut-offs, and refresh speeds. We flag those gaps up front so users are not blindsided later.

Key gap drivers include whether supply-chain management fees are counted, how informal micro-couriers are treated, the multiplier applied to booming e-commerce, and the currency date used.

According to Mordor Intelligence, our consistent scope, mid-year peso-to-USD conversion, and disciplined annual update cadence give planners a dependable anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.26 bn (2025) | Mordor Intelligence | |

| USD 18.03 bn (2024) | Regional Consultancy A | Counts supply-chain fees and higher e-commerce multiplier |

| USD 19.70 bn (2024) | Global Consultancy B | Uses fixed logistics-to-GDP ratio, ignores informal flows |

| USD 19.16 bn (2023) | Trade Journal C | Adds passenger baggage handling and pre-pandemic FX |

Taken together, our disciplined scope selection and yearly refresh deliver a transparent, repeatable baseline that decision-makers can trust while still leaving room for dialogue when unique planning assumptions are required.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the 2026 value of the Philippines freight and logistics market?

The Philippines freight and logistics market size is USD 16.20 billion in 2026.

How fast will the sector grow through 2031?

The market is forecast to post a 5.93% CAGR (2026-2031), reaching USD 21.60 billion by 2031.

Which logistics function shows the highest growth?

Courier, Express, and Parcel services lead with a 6.82% CAGR between 2026-2031.

Why are cold-chain facilities attracting investment?

Government grants and rising food and pharma flows are pushing temperature-controlled warehousing to a 6.69% CAGR (2026-2031).

How will cabotage reform affect inter-island shipping costs?

Full implementation could lower domestic sea freight tariffs by 10–15% by expanding foreign vessel access.

Which region is emerging as an air-cargo hub?

Clark Freeport is hosting expanded FedEx and UPS facilities, positioning Central Luzon as the country’s primary international air-cargo gateway.