PEF (Polyethylene Furanoate) In Bottles And Films Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

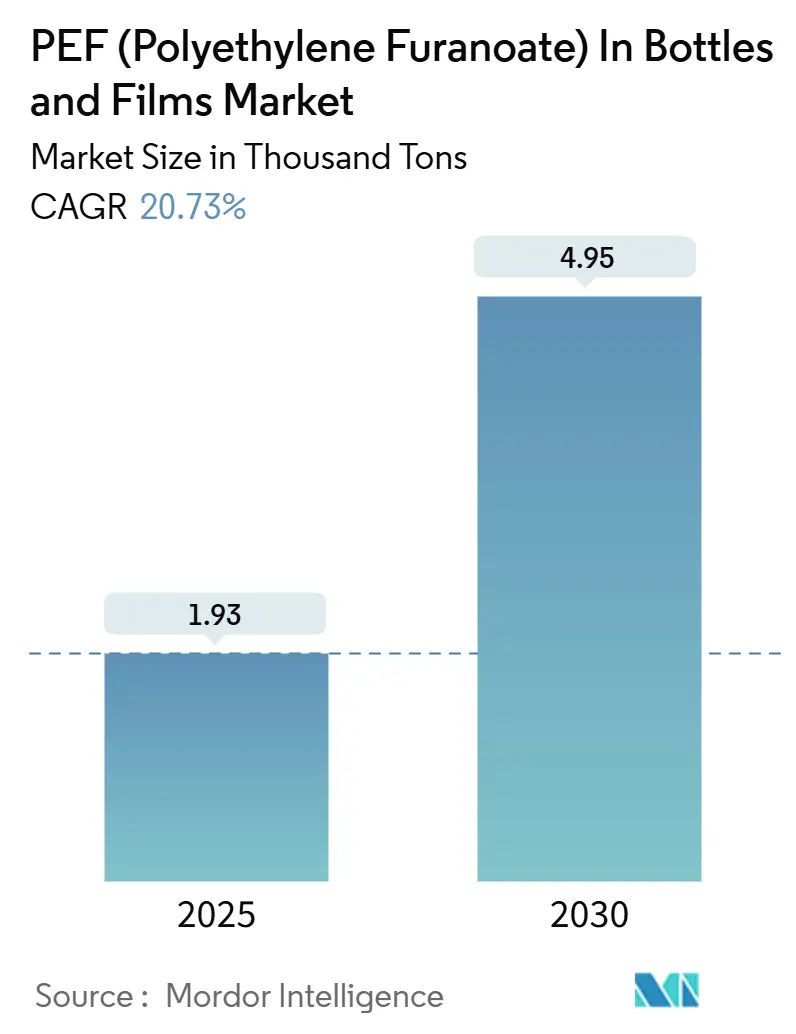

| Market Volume (2025) | 1.93 Thousand tons |

| Market Volume (2030) | 4.95 Thousand tons |

| Growth Rate (2025 - 2030) | 20.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PEF (Polyethylene Furanoate) In Bottles And Films Market Analysis by Mordor Intelligence

The PEF (Polyethylene Furanoate) in Bottles and Films Market size is estimated at 1.93 Thousand tons in 2025, and is expected to reach 4.95 Thousand tons by 2030, at a CAGR of 20.73% during the forecast period (2025-2030). The market size outlook is anchored in tightening regulations on single-use plastics, premium pricing for low-carbon packaging, and demonstrable improvements in product shelf-life. Brand owners are accelerating offtake agreements to secure early supplies of the bio-based polymer, while converters upgrade their processing lines that already handle PET to minimize capital outlays. Rapid capacity additions in Europe and Japan improve supply visibility, and the first U.S. food-contact approval unlocks access to high-value applications in North America. Competitive differentiation now hinges on intellectual property coverage, feedstock supply contracts for fructose-derived FDCA, and the ability to certify recyclability within existing PET streams.

Key Report Takeaways

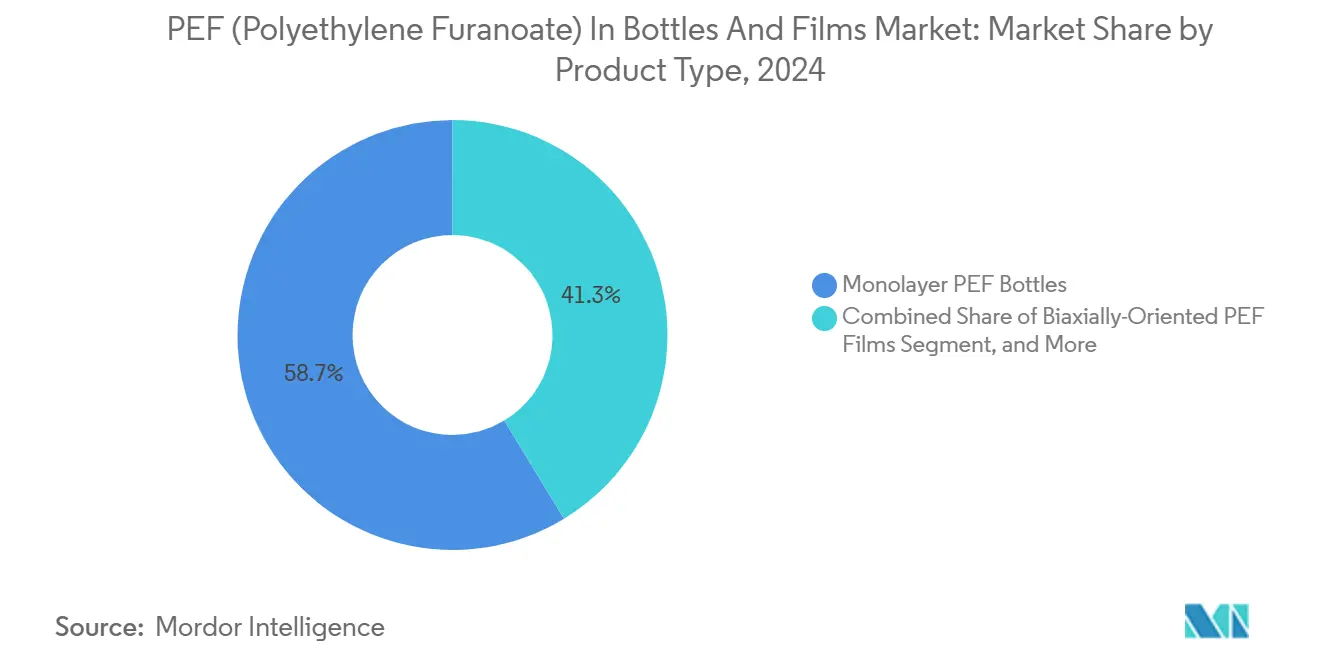

- By product type, monolayer bottles captured 58.68% of the PEF (Polyethylene Furanoate) in Bottles and Films market share in 2024.

- By application, PEF (Polyethylene Furanoate) in bottles and films market size for films is projected to grow at 21.93% CAGR between 2025–2030.

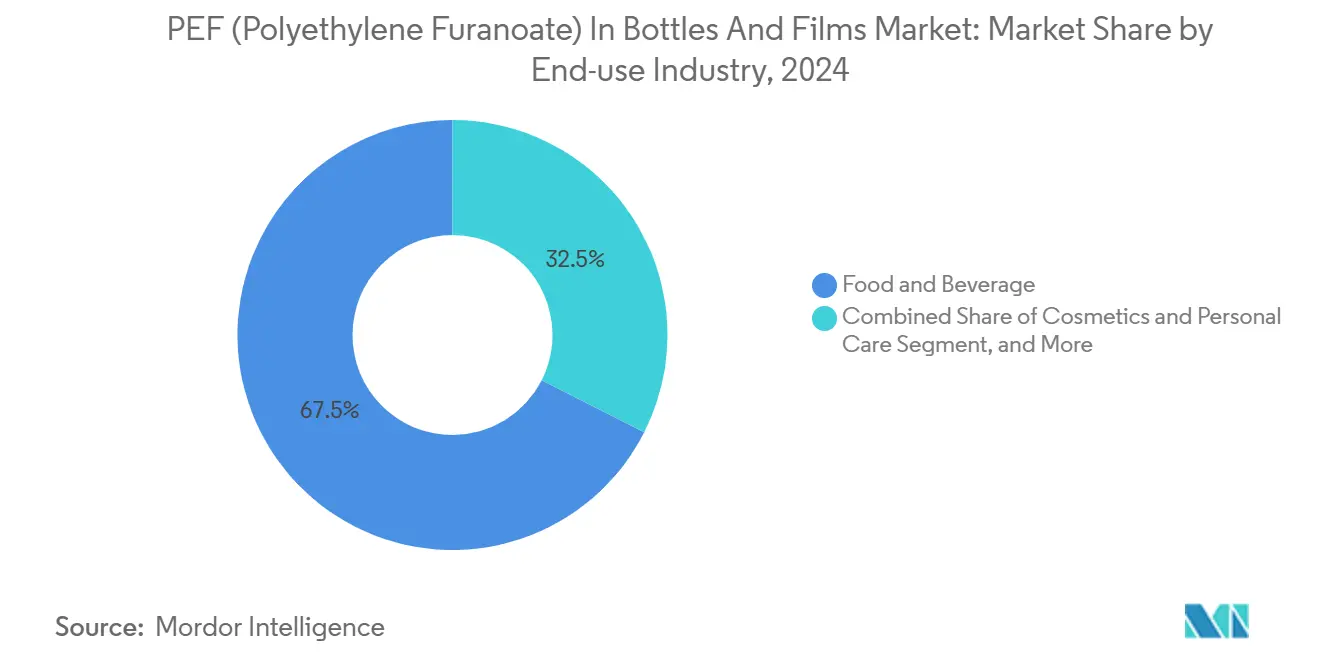

- By end-use industry, food and beverage captured 67.54% of the PEF (Polyethylene Furanoate) in bottles and films market share in 2024.

- By geography, PEF (Polyethylene Furanoate) in bottles and films market size for Asia-Pacific is projected to grow at 23.47% CAGR between 2025–2030.

Global PEF (Polyethylene Furanoate) In Bottles And Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for sustainable packaging among beverage brands | +4.2% | Global, led by Europe and North America | Medium term (2-4 years) |

| EU single-use plastics directives favoring bio-based polymers | +3.8% | Europe, spill-over to United Kingdom and European Free Trade Association | Short term (≤ 2 years) |

| Superior gas-barrier properties extending shelf-life | +3.1% | Global, notable in Asia-Pacific food markets | Long term (≥ 4 years) |

| Investments in FDCA and PEF capacity expansions | +2.9% | Europe and North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Carbon-accounting premiums in FMCG supply contracts | +2.4% | Global, led by multinational FMCG companies | Long term (≥ 4 years) |

| Compatibility with existing PET recycling streams | +1.9% | Global, infrastructure-dependent regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for sustainable packaging among beverage brands

Carlsberg and AmBev disclosed conditional supply agreements that reserve volumes from the first commercial FDCA plant, signaling intent to move beyond pilot deployments. Early adopters secure marketing differentiation and gain preferred access to line time at contract fillers that are retooling for biopolymer processing. Shelf-life gains lower write-off costs for premium beverages, creating a direct economic incentive that complements reputational benefits. As life-cycle assessment datasets mature, procurement teams can quantify a carbon-footprint reduction that supports higher shelf prices in premium categories. De facto standards set by multinational brands then ripple across private-label producers that share the same bottling infrastructure.

EU single-use plastics directives favoring bio-based polymers

The EU Packaging and Packaging Waste Regulation, enacted in December 2024, bans specific single-use formats and imposes minimum recycled-content thresholds that conventional PET will struggle to meet. Because PEF qualifies as bio-based and is recyclable in existing PET streams, converters can meet upcoming mandates without the need to install entirely new recovery systems. Member states are granted latitude to mandate compostable solutions for additional product groups, expanding PEF’s accessible addressable market in food service disposables. Regulatory certainty through 2030 enables long-term supply contracts, which underpin the bankability of new FDCA plants. Down-gauging enabled by PEF’s barrier performance aligns with the Regulation’s weight-reduction targets, providing another compliance lever for brand owners.

Superior gas-barrier properties extending shelf-life

Oxygen-transmission testing shows that PEF is close to 10 times more effective than PET in blocking oxygen ingress, and independent studies report up to 16 times better carbon-dioxide retention. These technical advantages enable longer distribution windows and allow exporters to reach distant markets without requiring cold-chain upgrades. Fresh-produce trials in Dutch retail chains confirm that salads stored in PEF trays maintain their quality for several extra days compared to identical PET formats. The same barrier profile supports lightweighting because thinner walls provide the same protection, resulting in further material savings and lower transport emissions.

Investments in FDCA and PEF capacity expansions

Avantium’s Delfzijl facility became operational in October 2024, with an annual capacity of 5,000 metric tons, establishing a reference plant that demonstrates process economics and quality consistency at scale. Technology-licensing packages accelerate replication, enabling regional producers to mitigate risk by adopting a proven design. Japanese chemical majors invested in start-ups commercializing biomass-based FDCA, thereby broadening the geographic supply base. As plants scale towards the 100 kiloton threshold, optimizing catalyst performance and heat-integration strategies is expected to close a significant portion of the current cost gap with PET. Announced projects already in the basic engineering stage suggest that effective supply could triple by 2028, thereby mitigating near-term allocation risks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost versus PET | -3.7% | Global, especially price-sensitive economies | Medium term (2-4 years) |

| Limited commercial-scale capacity | -2.8% | Global, supply-constrained regions | Short term (≤ 2 years) |

| Feedstock supply constraints (fructose/FDCA) | -2.1% | Regions dependent on imported feedstocks | Long term (≥ 4 years) |

| Regulatory approval gaps in emerging markets | -1.6% | Asia-Pacific, South America, MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production cost versus PET

Current FDCA synthesis routes rely on catalytic oxidation and energy-intensive purification stages that elevate variable costs above those of fossil-derived terephthalic acid. Even after accounting for capital depreciation, modeled cash costs still exceed PET benchmarks by a substantial margin, limiting penetration into commodity applications. Electricity-assisted pathways under investigation show meaningful energy savings, but commercial demonstration is pending.[1]Source: Lin Chen et al., “Integrated electrochemical and chemical system for ampere-level production of terephthalic acid alternatives and hydrogen,” Nature Communications, nature.com Until economies of scale and process intensification mature, converters must rely on carbon-footprint premiums or marketing differentiation to justify higher resin costs. Down-gauging and shelf-life benefits offset pricing in certain segments; however, cost pressure remains material in bulk packaging, where specifications are less demanding.

Limited commercial-scale capacity

With only one operational plant and a handful of pilot units worldwide, aggregate PEF output is insufficient to serve large-volume launches. The early production has already been reserved under multi-year offtake agreements, delaying material availability for prospective entrants. Engineering lead times of three to five years slow the pace at which new capacity can come online, and investors remain cautious of overbuilding before mass-market prices converge with those of PET. Any supply disruption at the inaugural facility would therefore ripple across the value chain, hindering brand-owner rollouts and eroding confidence among converters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Monolayer Bottles Lead Early Adoption

Monolayer PEF bottles represented 58.68% of the PEF (Polyethylene Furanoate) in Bottles and Films market share in 2024. Adoption is facilitated by the ability to run the polymer on existing single-stage injection-stretch blow molding equipment with minor parameter adjustments. Commercial bottlers allocate limited campaign runs to PEF while maintaining PET throughput, allowing for progressive scaling. The monolayer format captures value in carbonated soft drinks and premium waters where the resin’s carbon dioxide barrier supports longer shelf life at room temperature.

Biaxially-oriented PEF films post a 25.45% CAGR, the highest among product types. Thin-gauge film trials show material reductions of up to 30% versus multilayer PET due to PEF’s intrinsic barrier strength. Converters focus on snack and fresh-produce pouches where oxidation or moisture ingress impairs quality. Multilayer bottles, cast films, and niche variants occupy smaller shares but underpin technical development, particularly for hot-fill beverages and retort applications that require enhanced thermal stability. As cost curves improve, multilayer bottle formats might migrate to full PEF structures, consolidating demand.

By Application: Bottles Dominate but Films Accelerate

Bottles controlled 68.84% of the PEF (Polyethylene Furanoate) market size in bottles and films in 2024. Big-brand commitments, most visibly in beer and sports drinks, converted early pilot work into pre-commercial runs. Retailers highlight bio-based logos on labels, enabling price premiums and higher shelf rotations. Regulations mandating tethered caps and recyclable mono-materials further favor bottle applications that integrate seamlessly into established deposit systems.

Films, growing at 21.93% CAGR, unlock higher value density per kilogram of polymer because performance benefits accrue across large surface areas. Trials in modified-atmosphere salads report waste reductions that translate directly into retailer margin gains. Pharmaceutical blister-foil laminate suppliers are evaluating PEF films for use with moisture-sensitive tablets, aiming to replace aluminum foils and thereby open a pathway to carbon reduction in healthcare packaging. Successful validation in a single high-margin drug category could cascade into broader adoption across over-the-counter products.

By End-use Industry: Food and Beverage Account for Bulk Demand

The food and beverage arena accounted for 67.54% of the PEF (Polyethylene Furanoate) in Bottles and Films market size in 2024, as sustainability commitments intersect with shelf-life economics. Premium juice makers champion PEF for oxygen-sensitive formulations, gaining marketing leverage through transparent biocircular messaging. Meal-kit companies are adopting PEF liners to reduce spoilage during last-mile distribution, aligning with their waste-reduction goals.

Pharmaceutical demand, projected to expand at a 22.16% CAGR, is driven by a regulatory push for improved drug stability amid rising ambient-temperature supply chains. Early stability studies conducted under International Council for Harmonization protocols demonstrate significant moisture barrier improvements in PEF blister systems, thereby reducing the need for secondary desiccants. Cosmetics brands experiment with PEF jars for water-free formulations where oxidative rancidity is a concern, though volume contributions remain modest. Household-care packaging lags due to thinner margins and comparatively low barrier requirements.

Geography Analysis

European momentum stems from the balance between regulatory certainty and local monomer supply. Brand owners secure allocations from the single FDCA plant, mitigating logistics risks and benefiting from tight supplier-retailer collaboration on eco-labels. Several national governments add fees to plastic packaging with less than 30% recycled content, indirectly boosting demand for PEF, whose lifecycle can begin with entirely renewable feedstocks. Retailer-led pilots in Germany, France, and the Netherlands validate consumer acceptance without price erosion, reinforcing the commercial case. Collaboration platforms, such as the European PET Bottle Platform, have already green-listed PEF as compatible with existing recycling streams, thereby smoothing downstream adoption.

Asia-Pacific’s acceleration pivots on capacity investments and regulatory green lights. Japanese chemical companies integrate FDCA units within existing aromatics complexes, leveraging shared utilities and logistics. The Ministry of the Environment signals support for advanced biopolymers, including PEF, within its Plastic Resource Circulation Strategy, providing a supportive policy anchor. Australia and New Zealand are considering labeling schemes that recognize bio-based content, which would further encourage the import of PEF bottles for wine and specialty beverages.[2]Source: Argus Media Staff, “Japan's MGC to fund U.S. biomass-based plastic start-up,” Argus Media, argusmedia.com China focuses on industrial pilots contiguous to its sugarcane and corn-starch supply chains, although final deployment timelines hinge on licensing agreements with Western IP holders.

North America’s market transition was unlocked by FDA food-contact approval, allowing converters to launch products without the cost of individual no-objection letters. Multistate beverage deposit frameworks look favorably upon PEF co-recycling because near-infrared sorters can distinguish it from PET. Early interest emerges from plant-based milk brands that require oxygen protection and wish to highlight bio-based packaging. Canada’s Extended Producer Responsibility expansions could further prioritize high-barrier bio-polymers if eco-modulated fees gain traction. Large retailers monitor shelf-life data from European pilots to inform local supplier specifications.

Competitive Landscape

The PEF (Polyethylene Furanoate) in Bottles and Films market features a high concentration, dominated by technology originators and their licensees. Avantium holds broad patents covering oxidation catalysts and polymerization conditions, enabling it to charge royalties and to screen licensees on ESG criteria. Commercial relationships are cemented through multi-year offtake agreements that secure offtake for over 95% of initial capacity, blocking latecomers from accessing resin until new plants materialize. Established PET producers tend to pursue joint ventures rather than in-house process development, reflecting a risk-averse approach in capital-intensive commodity sectors.

Strategic moves favor vertical integration of feedstock supply. Some licensors partner with fructose producers to secure high-purity inputs necessary for FDCA yields, while others investigate agricultural-residue pathways to diversify risk. Intellectual property litigation risk remains moderate but could increase as alternative catalytic routes reach commercial scale. Process innovation is a crucial axis of competition; the electrochemical oxidation of furfural establishes a position as a lower-energy route that bypasses noble-metal catalysts. If demonstrated at scale, it could erode the cost premium that currently protects pioneer plants.

Packaging converters compete on application development rather than resin production. Firms with proprietary molding technologies can optimize cycle times and wall thickness, providing an edge in cost per filled unit. Pharmaceutical blister suppliers race to be first with package inserts citing PEF stability data, anticipating regulatory differentiation.[3]Source: Kolon Industries Press Release via KunststoffWeb, “Stora Enso: Kolon Industries steigt in PEF-Entwicklung ein,” kunststoffweb.de Equipment vendors supply screw-design retrofits and melt-filter systems specialized for PEF, offering turnkey packages that minimize changeover time from PET.

PEF (Polyethylene Furanoate) In Bottles And Films Industry Leaders

Avantium N.V.

Toyobo Co., Ltd.

Toray Industries, Inc.

Sulzer Ltd.

Mitsui Chemicals, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Stora Enso partnered with Kolon Industries to expand PEF into electronics films and tire cord fibers, marking a diversification beyond packaging.

- April 2025: Avantium has obtained FDA Food Contact Notification approval, covering all food grades except infant formula and high-alcohol beverages, clearing a critical barrier in North America.

- March 2025: Mitsubishi Gas Chemical invested in U.S. start-up ReSource Chemical to pursue woody-biomass FDCA, including plans for a pilot plant.

- November 2024: Avantium and Kirin began exploring PEF applications across the Japanese beverage giant’s product portfolio.

Global PEF (Polyethylene Furanoate) In Bottles And Films Market Report Scope

| Monolayer PEF Bottles |

| Multilayer PEF Bottles |

| Biaxially-Oriented PEF Films |

| Cast PEF Films |

| Other Product Types |

| Bottles |

| Films |

| Food and Beverage |

| Cosmetics and Personal Care |

| Pharmaceuticals |

| Household and Cleaning |

| Other End-use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Monolayer PEF Bottles | ||

| Multilayer PEF Bottles | |||

| Biaxially-Oriented PEF Films | |||

| Cast PEF Films | |||

| Other Product Types | |||

| By Application | Bottles | ||

| Films | |||

| By End-use Industry | Food and Beverage | ||

| Cosmetics and Personal Care | |||

| Pharmaceuticals | |||

| Household and Cleaning | |||

| Other End-use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What volumes define commercial viability for PEF packaging?

With 5,000 metric-ton annual output now online and nearly fully allocated, analysts view a 50,000 metric-ton regional capacity cluster as the threshold for broad market entry, which current project pipelines aim to reach by 2028.

How does PEF improve beverage shelf-life versus PET?

Tests show that oxygen transmission rates are roughly one-tenth those of PET, and carbon-dioxide retention is up to 16 times higher, supporting longer ambient storage for carbonated drinks and oxygen-sensitive juices.

When will PEF resin prices reach parity with conventional PET?

Producers expect that scale-up to multi-tens-of-kiloton plants and incremental process improvements will narrow the cost gap, but parity is unlikely before the end of this decade.

Can PEF be recycled in existing PET streams?

Independent sorting trials in Europe have confirmed that PEF can be detected and either co-recycled or separately recovered without degrading PET flake quality, thereby enabling infrastructure compatibility from day one.

Which end-use sector shows the fastest growth for PEF?

Pharmaceutical barrier packaging is projected to advance at a 22.16% CAGR, driven by humidity-sensitive formulations and stricter stability requirements in ambient logistics.

What regulatory milestone unlocked North American demand?

The U.S. Food and Drug Administration issued a Food Contact Notification for PEF in April 2025, clearing the polymer for virtually all food packaging applications except infant formula and high-alcohol beverages.

Page last updated on: