Americas Polypropylene (PP) Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

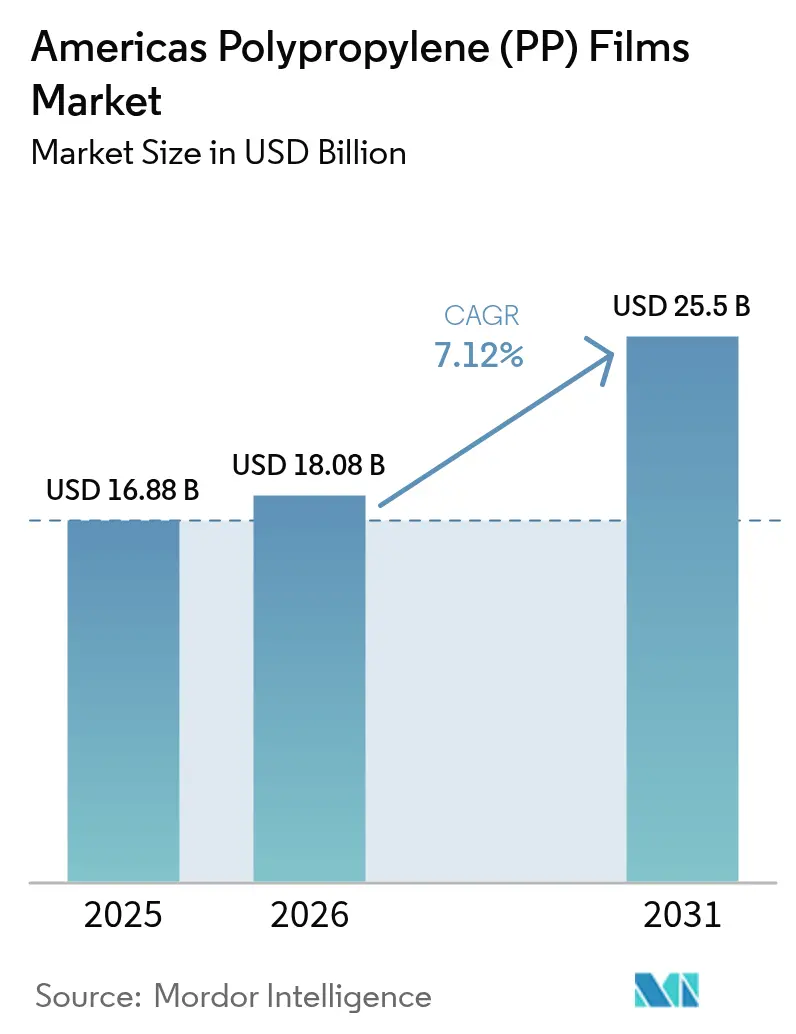

| Base Year Market Size (2025) | USD 16.88 Billion |

| Market Size (2026) | USD 18.08 Billion |

| Market Size (2031) | USD 25.5 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | South America |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Americas Polypropylene (PP) Films Market Analysis by Mordor Intelligence

The Americas polypropylene films market size is expected to grow from USD 16.88 billion in 2025 to USD 18.08 billion in 2026 and is forecast to reach USD 25.5 billion by 2031 at 7.12% CAGR over 2026-2031. This growth stems from a decisive shift toward mono-material flexible packaging that protects products, preserves recycling compatibility, and meets increasingly stringent state sustainability requirements. Demand also rises as North American meal-kit and grocery e-commerce channels adopt high-barrier pouches that weigh less than rigid formats, cutting last-mile freight costs. Film producers are investing in silicon-oxide and aluminum-oxide barrier coatings that match the performance of polyethylene terephthalate at a lower resin expense, while pharmaceutical blister-pack converters are replacing polyvinyl chloride to meet phthalate-free mandates. Competitive intensity is elevated because integrated petrochemical firms are now backward-integrating into film production, narrowing margins for traditional converters and reinforcing the need for product differentiation through coatings, downgauging, and recycled-content certifications.

Key Report Takeaways

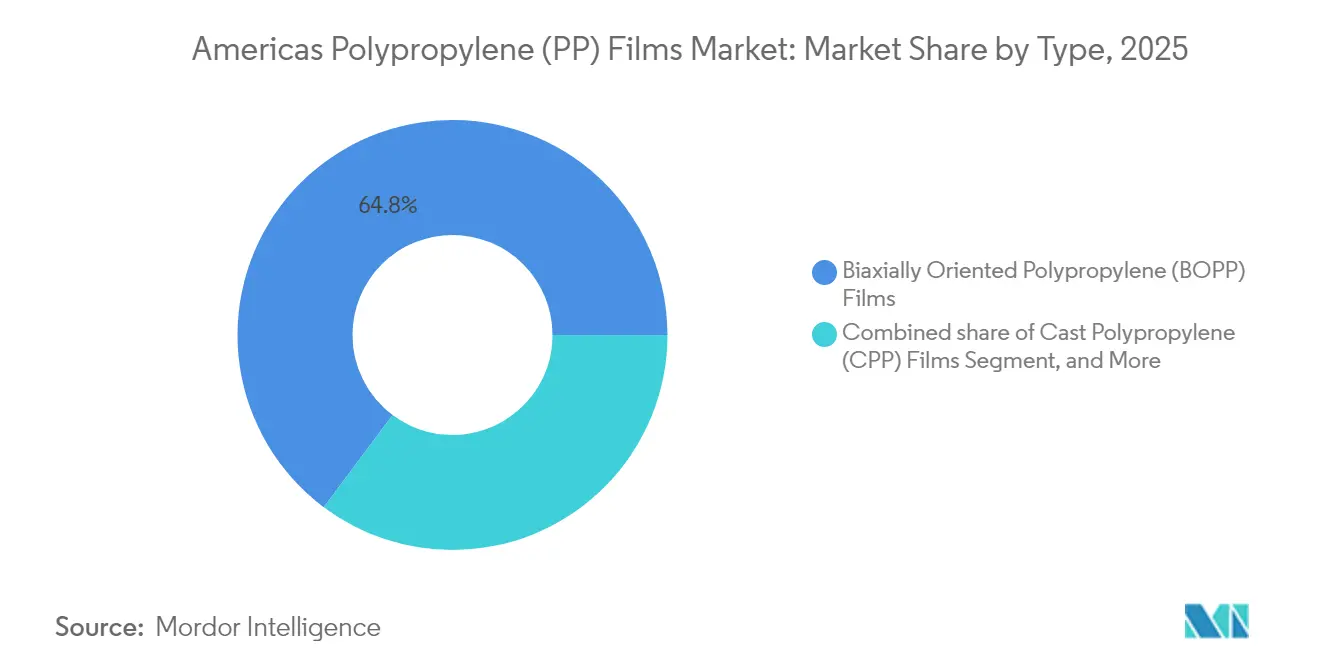

- By type, biaxially oriented polypropylene commanded 64.78% of volume in 2025, while cast polypropylene is expanding at an 8.18% CAGR through 2031.

- By thickness, the 20-40 micron range held 52.05% share in 2025; films below 20 microns are advancing at a 9.05% CAGR.

- By application, packaging accounted for a 67.65% slice in 2025, whereas laminated structures are forecast to grow at an 8.32% CAGR.

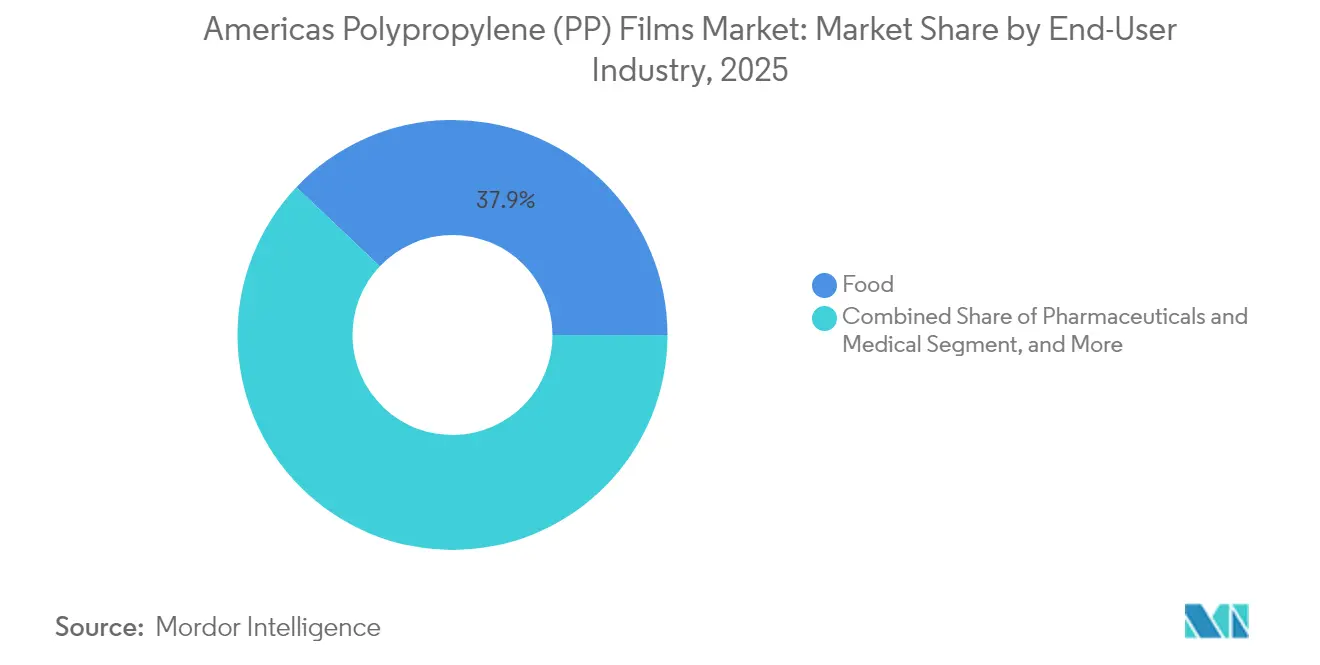

- By end-user, food consumption represented 37.94% of demand in 2025; pharmaceuticals and medical uses are rising at an 7.95% CAGR.

- By geography, North America captured 77.88% regional share in 2025; South America is projected to post an 8.01% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Americas Polypropylene (PP) Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift Toward Mono-Material Flexible Packaging Solutions | +1.8% | North America, with early adoption in Brazil and Argentina | Medium term (2-4 years) |

| Expansion of E-commerce Fresh Food Delivery Networks | +1.5% | North America urban corridors, expanding to São Paulo and Mexico City | Short term (≤ 2 years) |

| Increased Demand for High-Barrier Films in Sustainable Packaging | +1.4% | Global, with regulatory acceleration in California and Northeast U.S. | Medium term (2-4 years) |

| Replacement of PVC and PET with Polypropylene Films in Pharmaceutical Blister Packs | +1.2% | North America and Brazil pharmaceutical hubs | Long term (≥ 4 years) |

| Investment in Advanced Biaxially Oriented Lines by Latin American Converters | +0.9% | Brazil, Argentina, Chile, with spillover to Andean markets | Long term (≥ 4 years) |

| Rising Adoption of Recyclable Transparent Wraps by Quick-Service Restaurants | +0.7% | North America, concentrated in U.S. metropolitan statistical areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Mono-Material Flexible Packaging Solutions

Brand owners are collapsing multilayer laminates into single-polymer formats to meet design-for-recycling targets and avoid extended producer responsibility fees. Coveris and Borealis commercialized a mono-polypropylene pet-food pouch in 2024 that eliminates polyethylene tie layers and still passes drop-test protocols. [1]Coveris, “Launch of Mono-Material Pet-Food Pouches,” coveris.com Borouge and Siegwerk have released a compatible ink-adhesive system that delivers peel strengths of above 2 N per 15 mm while preserving the purity of the recycling stream. Fraunhofer research shows that laminates retain 85% of their tensile strength after three mechanical cycles, compared to 60% for polyethylene terephthalate blends. California regulations, effective in 2024, require 25% post-consumer content in single-use packaging by 2032, accelerating the adoption of these mono-structures. Together, these advances make the Americas polypropylene films market a preferred platform for closed-loop packaging programs.

Expansion of E-commerce Fresh Food Delivery Networks

Meal-kit and online grocery services are scaling cold-chain hubs that favor lightweight, puncture-resistant pouches. Metallized cast polypropylene delivers moisture barriers below 1 g m⁻² day⁻¹, crucial for condensation control in refrigerated cross-docks.[2]MDPI Coatings Journal, “Barrier Coating Advances on BOPP Films,” mdpi.com Flexible packs reduce shipping weight by 40% and cube utilization by 25%, trimming courier costs in dense cities. UFlex brought an 18,000 tpa line online in Mexico in H2 FY 2025 to supply U.S. fulfillment centers with rapid-turnaround custom prints. Reclosable zippers and fitment spouts laminated onto mono-material webs add consumer convenience without compromising recyclability. As subscription grocery penetration climbs, that functionality propels incremental square-meter demand in the Americas polypropylene films market.

Increased Demand for High-Barrier Films in Sustainable Packaging

Silicon-oxide and aluminum-oxide vapor deposition on biaxially oriented polypropylene reduces oxygen transmission by 65-fold, extending the shelf life of coffee and dried fruit by up to nine months. Aluminum-oxide coatings push OTR below 0.5 cc m⁻² day⁻¹, meeting stringent pharmaceutical blister specs. Fraunhofer’s ORMOCER hybrids add scratch resistance without impeding melt reprocessing, addressing converter concerns about line scuffing. California’s Circular Economy Act imposes a USD 0.25 per kg penalty on non-recyclable packs, making coated polypropylene more cost-effective than polyethylene terephthalate or polyvinyl chloride. These material gains safeguard the Americas polypropylene films market as brand owners balance barrier, weight, and recyclability objectives.

Replacement of PVC and PET with Polypropylene Films in Pharmaceutical Blister Packs

Amcor’s 2024 mono-polypropylene blister meets U.S. Pharmacopeia Class VI and outperforms polyvinyl chloride on moisture ingress, an advantage for hygroscopic drugs. TekniPlex’s dead-fold formulation yields crisp creases for push-through dispensing without delamination. SÜDPACK eliminated aluminum lidding by integrating a peelable sealant, cutting pack weight 30% and enabling stream-pure recycling. Health Canada guidance issued in 2024 on extractables testing tilts procurement toward inert polypropylene webs. These breakthroughs underpin a long-run CAGR lift for the Americas polypropylene films market as drug makers roll out phthalate-free unit doses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Propylene Feedstock Prices Linked to Shale Gas Dynamics | -1.3% | North America, with spillover to Latin American import-dependent markets | Short term (≤ 2 years) |

| Stringent Single-Use Plastic Regulations in Major U.S. States | -0.9% | California, Colorado, Maine, with adoption pending in New York and Washington | Medium term (2-4 years) |

| Supply Chain Disruptions from Regional Plant Outages | -0.6% | U.S. Gulf Coast, with cascading effects across North America | Short term (≤ 2 years) |

| Competition from Emerging Bio-Based and Biodegradable Film Alternatives | -0.5% | North America and Brazil, concentrated in food-service and agricultural applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Propylene Feedstock Prices Linked to Shale Gas Dynamics

Henry Hub spot prices fell to USD 2.27 per MMBtu in 2024 but spiked 15% during unplanned Gulf Coast outages, sending propylene references higher and squeezing converters locked into fixed-price film contracts. [3]U.S. Energy Information Administration, “Natural Gas and Propylene Price Dynamics 2024,” eia.gov INEOS declared force majeure in early 2024 after a compressor failure, while Winter Storm Enzo temporarily idled steam crackers in January 2025. Latin American extruders reliant on U.S. chemical exports paid import premiums that compressed spreads. Because resin accounts for 55-65% of finished-film cost, volatility discourages capital-intensive barrier-coating upgrades and can slow the Americas polypropylene films market in the short term.

Stringent Single-Use Plastic Regulations in Major U.S. States

California’s SB 54 rules, implemented in 2024, impose recycling-rate thresholds and escalating post-consumer content mandates, with fees up to USD 0.50 kg⁻¹ for non-recyclable packs. Colorado and Maine adopted similar extended-producer-responsibility laws, while New York and Washington draft comparable bills. Quick-service restaurants must redesign wrappers or absorb higher stewardship costs, cutting film order volumes until compliant designs are validated. Prohibitions on per- and polyfluoroalkyl substances further complicate coating chemistries. These overlapping state rules tighten margins for small converters and temper the Americas polypropylene films market growth outlook during the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: BOPP Strength Sustains, CPP Accelerates in Pharma

Biaxially oriented grades retained 64.78% of 2025 volume, anchoring the Americas polypropylene films market with strong tensile strength and high gloss that suit snack, label, and tape applications. Producers stretch molten sheet in both machine and transverse directions, boosting modulus above 3 GPa and enabling 15 micron downgauging without puncture compromise. Converters overlay silicon-oxide to meet sub-1 cc m⁻² day⁻¹ oxygen targets for roasted coffee, displacing polyethylene terephthalate structures. Cast polypropylene is projected to grow at an 8.18% CAGR as pharmaceutical blister lines transition from polyvinyl chloride to comply with extractables rules and as aseptic pouches demand stronger seal integrity. Brazilian converters ordered wide-cast lines in 2024 to serve Mercosur drug makers, underscoring CPP’s rising strategic weight in the Americas polypropylene films market.

Rapid output additions in Mexico, Argentina, and the United States ease historic CPP shortfalls, yet BOPP remains the scale workhorse for labels, overwraps, and transparent snacks. Vitopel’s metallized BOPP capacity jump in 2024 lowered lead times for moisture-sensitive coffee bags, while North American converters qualified 30% recycled-content BOPP to meet brand sustainability targets. Niche oriented grades, such as capacitor films and holographic overlays, enjoy premium margins thanks to tight thickness tolerance and dielectric purity, but they combined represent less than 2% of Americas polypropylene films market share.

By Thickness: Sub-20 Micron Films Lead Downgauging Drive

Films under 20 microns post a 9.05% CAGR because high-stiffness biaxial orientation enables brand owners to reduce resin mass while maintaining puncture resistance. Barrier-coated 12-micron webs deliver the same oxygen protection as 40-micron uncoated films, unlocking 40% material savings. The 20-40 micron slot held 52.05% share in 2025, favored for pharmaceutical blister thermoforming, heavy-duty industrial wraps, and form-fill-seal pouches that need caliper for seal integrity. Many blister lines are calibrated for 25-micron webs, and retrofitting for thinner gauges requires new heater plates and cooling racks that converters often defer.

Above 40 microns, polypropylene competes with oriented polyethylene for stiff freezer bags and with polyethylene terephthalate for transparent retort lids. Growth here is muted, yet the Americas polypropylene films market size for thick gauges holds steady because construction wraps and synthetic paper labels value tear and moisture resistance over weight. The anticipated migration of coffee and snack packs to 15-micron coated webs will continue to put pressure on mid-gauge output, prompting producers to invest in ultra-thin tenter frames and high-output winding systems.

By End-User Industry: Food Dominates While Pharmaceuticals Gain Momentum

Food processors absorbed 37.94% of 2025 demand, relying on gloss finish, printability, and moisture barrier for snacks, bakery wraps, and produce bags. Shelf-life extension tactics, such as nitrogen flushing, pair well with low-oxygen-transmission biaxially oriented films. Yet growth moderates as paper-based laminates attract dry cereal and powdered beverage applications looking for perceived eco-friendliness over oxygen performance. Pharmaceuticals and medical packaging are projected to register an 7.95% CAGR, driven by mono-material blister innovations that meet Health Canada and U.S. FDA guidelines on extractables while enhancing senior-friendly push-through strength. Drug makers adopt unit-dose formats for antibiotics and antihistamines, amplifying square-meter use even when pill count stays flat.

Beverage label converters seek shrink-sleeve and in-mold formats that conform to the curves of aluminum cans and polyethylene terephthalate bottles, while ensuring sortability at material recovery facilities. Industrial tapes, stretch wraps, and release liners exhibit stable but cyclical demand tied to construction starts and light-vehicle production. Personal-care sachets face regulatory risk in coastal U.S. states exploring single-use bans, yet multi-use refill pouches often employ high-barrier cast polypropylene, preserving some offset demand inside the Americas polypropylene films industry.

By Application: Packaging Holds Pole Position, Laminations Surge

Packaging represented 67.65% of 2025 consumption, encompassing form-fill-seal snack webs, stand-up pouches, and produce wraps. Downgauging to 15-micron coated films and the rise of reclosable formats sustain volume despite resin savings. Laminations are expected to rise at an 8.32% CAGR because converters overlay silicon oxide or aluminum oxide on polypropylene, replacing polyethylene terephthalate in retort pouches and aseptic drink cartons while preserving a mono-material status. Label and tape markets tap polypropylene’s print clarity and dielectric properties for consumer goods, logistics tracking, and electrical insulation.

Specialty graphics, holographic gift wraps, and book-cover overlays account for modest but high-margin niches, fetching prices three to five times the rates of commodity film. Capacitor dielectrics, synthetic paper, and agricultural mulch use thicker, highly oriented films tailored for electrical strength or ultraviolet resistance. The Americas polypropylene films market size in laminated structures is poised for above-trend expansion as barrier-coating adoption deepens and as converters reply to extended producer responsibility mandates by shifting away from multi-polymer stacks.

Geography Analysis

North America secured 77.88% of 2025 revenue, buoyed by dense food-processing clusters, a robust pharmaceutical pipeline, and widespread e-commerce fulfillment networks. Integrated feedstock supply from Gulf Coast crackers into Midwestern and Southeastern film extrusion hubs stabilizes logistics and enables lean inventories. California’s 2024 stewardship-fee framework accelerates mono-material redesigns, prompting converters to qualify recyclable coatings ahead of 2030 content thresholds. Canada’s dairy and bakery sectors sustain steady demand, while Mexico’s near-shoring boom channels automotive and medical packaging orders to polypropylene film plants certified under Good Manufacturing Practice standards.

South America yields an 8.01% CAGR between 2026 and 2031, outperforming the region, as Brazil and Argentina add biaxially oriented and cast lines. Vitopel’s 2024 metallizer startup raised output 40%, winning snack-food and coffee-roaster contracts that need shiny oxygen barriers. Argentina’s blister-pack market moves toward mono-polypropylene to harmonize with Mercosur rules favoring phthalate-free materials. Chile, although smaller, increases seafood-pouch uptake, leveraging polypropylene’s low temperature crack resistance for frozen salmon exports.

Mexico’s role as a duty-free platform under the United States-Mexico-Canada Agreement intensifies, with multinational consumer-goods firms relocating packaging operations from Asia to cut lead times and tariff exposure. Rest-of-South-America markets such as Colombia and Peru show moderate uptake tied to urban retail expansion but face currency-driven resin-cost swings because they import U.S. propylene. Overall, growing intra-Americas trade and fresh foreign direct investment maintain a diversified demand base for the Americas polypropylene films market.

Competitive Landscape

Integrated propylene suppliers, such as Braskem and INEOS, exploit feedstock leverage to price aggressively during oversupply cycles, challenging stand-alone film extruders. Taghleef Industries coordinates global asset loads to cover regional outages, while Jindal Films Americas channels corporate research resources into dielectric and holographic grades that carry premium margins. Inteplast Group’s 2024 ISCC PLUS certification across three U.S. plants allows mass-balance crediting of bio-attributed feedstocks, meeting brand sustainability pledges and differentiating bids.

Niche converters focus on ultra-thin gauges below 12 microns or complex barrier laminations where expertise and capital barriers shelter margins. Private-equity activity intensifies, as Industrial Opportunity Partners acquired specialty converter Transcendia in May 2024, funding expansion into capacitor film and holography segments. Latin American players add wide tenter frames and metallizers to capture value in snack and coffee exports, while North American plants integrate plasma treater upgrades to improve ink adhesion on recycled-content substrates. With regulatory pressure favoring mono-material designs, coating and metallization capabilities become decisive competitive weapons in the Americas polypropylene films industry.

Americas Polypropylene (PP) Films Industry Leaders

Altopro S.A. de C.V.

Oben Holding Group S.A.

Taghleef Industries LLC

Toray Plastics (America), Inc.

Inteplast Group Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: UFlex commissioned an 18,000 tpa cast polypropylene line in Mexico to serve pharmaceutical and food customers requiring rapid, Good-Manufacturing-Practice-approved supply.

- January 2025: Winter Storm Enzo forced shutdowns of multiple Gulf Coast propylene units, delaying film deliveries to packaging converters by up to three weeks and spiking monomer contracts in the first quarter.

- October 2024: Vitopel installed a Bobst Expert K5 metallizer, boosting metallized BOPP capacity by 40% for snack-food and coffee customers in Brazil and Argentina.

- September 2024: Inteplast Group earned ISCC PLUS certification at its South Carolina, Texas, and Tennessee plants, enabling mass-balance allocation of bio-attributed feedstocks.

Americas Polypropylene (PP) Films Market Report Scope

The report on the America PP film market studies BOPP, CPP films, and others used for packaging products that withstand extreme temperatures, gases, and moisture. Furthermore, these packages also help with other properties, such as extending the shelf life and ultimately maintaining the product's quality and image.

The Americas Polypropylene Films Market Report is Segmented by Type (BOPP, CPP, SPP, Other Types), Thickness (Below 20 Microns, 20-40 Microns, Above 40 Microns), End-User Industry (Food, Beverage, Pharmaceuticals and Medical, Industrial, Personal Care and Cosmetics, Other End-User Industries), Application (Packaging, Labelling and Tapes, Laminations, Graphics and Overlays, Other Applications), and Geography (North America, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Biaxially Oriented Polypropylene (BOPP) Films |

| Cast Polypropylene (CPP) Films |

| Shrink Polypropylene (SPP) Films |

| Other Types |

| Below 20 Microns |

| 20 - 40 Microns |

| Above 40 Microns |

| Food |

| Beverage |

| Pharmaceuticals and Medical |

| Industrial |

| Personal Care and Cosmetics |

| Other End-User Industries |

| Packaging |

| Labelling and Tapes |

| Laminations |

| Graphics and Overlays |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America |

| By Type | Biaxially Oriented Polypropylene (BOPP) Films | |

| Cast Polypropylene (CPP) Films | ||

| Shrink Polypropylene (SPP) Films | ||

| Other Types | ||

| By Thickness | Below 20 Microns | |

| 20 - 40 Microns | ||

| Above 40 Microns | ||

| By End-User Industry | Food | |

| Beverage | ||

| Pharmaceuticals and Medical | ||

| Industrial | ||

| Personal Care and Cosmetics | ||

| Other End-User Industries | ||

| By Application | Packaging | |

| Labelling and Tapes | ||

| Laminations | ||

| Graphics and Overlays | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is polypropylene film demand in the Americas in 2026?

The Americas polypropylene films market size is USD 18.08 billion in 2026 and is forecast to grow at a 7.12% CAGR over 2026-2031.

Which film type leads regional consumption?

Biaxially oriented polypropylene accounts for 64.78% of 2025 volume because its high stiffness and clarity suit snacks, labels, and tapes.

What segment delivers the fastest growth to 2031?

Cast polypropylene films expand at an 8.18% CAGR through 2031, propelled by pharmaceutical blister-pack substitution of PVC and polyethylene terephthalate.

Why are thin-gauge films gaining share?

Sub-20 micron webs cut resin weight by up to 40% while barrier coatings maintain shelf life, enabling logistics savings for e-commerce fresh food shipments.

How will U.S. state regulations influence demand?

California, Colorado, and Maine stewardship fees, active from 2024, accelerate adoption of recyclable mono-material packs but raise compliance costs for non-conforming films, moderating short-term growth.

Which region in the Americas is growing fastest?

South America is expected to post an 8.01% CAGR through 2031 as Brazil and Argentina add new biaxially oriented and cast lines to serve food and pharmaceutical exporters.

Page last updated on: