Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

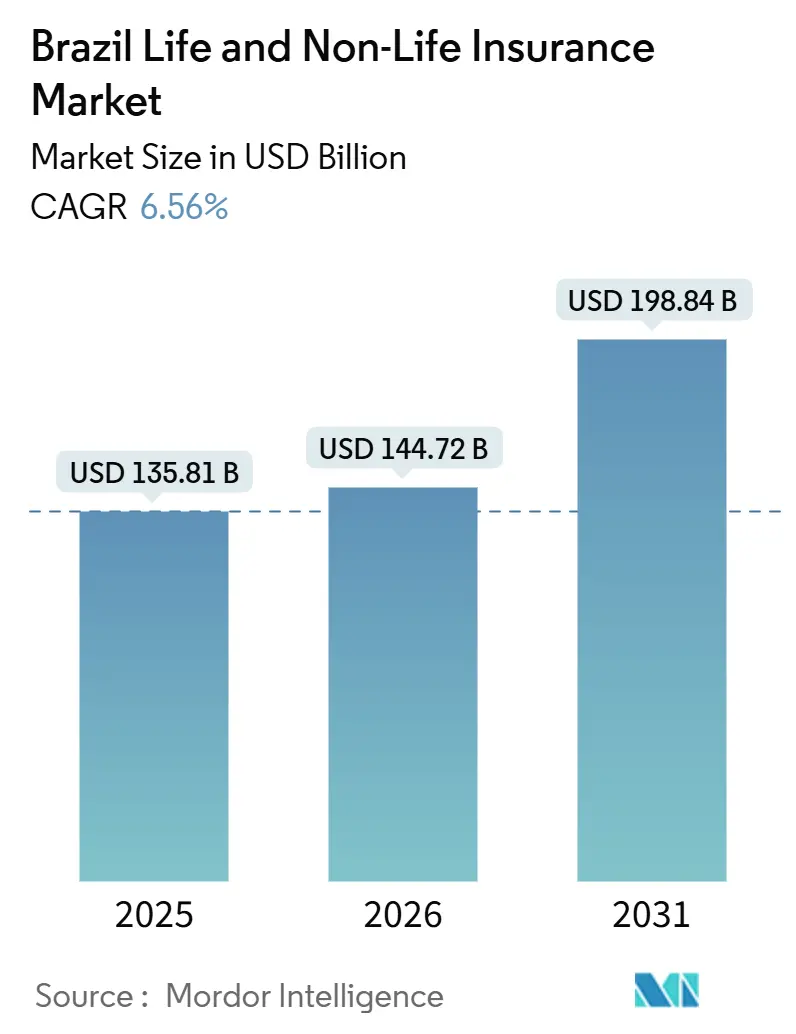

| Base Year Market Size (2025) | USD 135.81 Billion |

| Market Size (2026) | USD 144.72 Billion |

| Market Size (2031) | USD 198.84 Billion |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

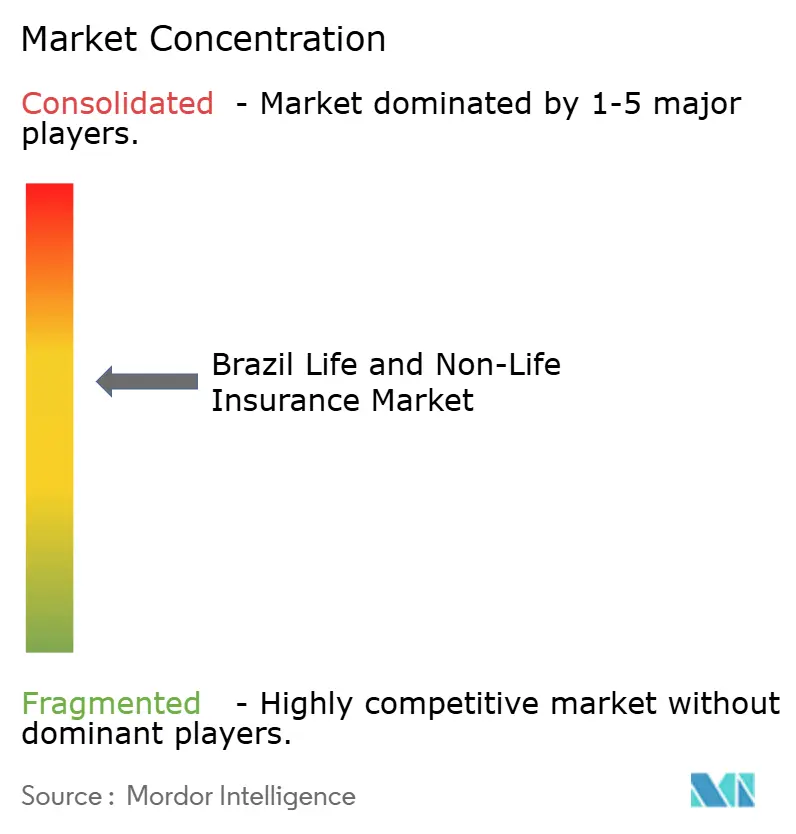

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Life And Non-Life Insurance Market Analysis by Mordor Intelligence

The Brazil Life And Non-Life Insurance Market size is expected to grow from USD 135.81 billion in 2025 to USD 144.72 billion in 2026 and is forecast to reach USD 198.84 billion by 2031 at 6.56% CAGR over 2026-2031.

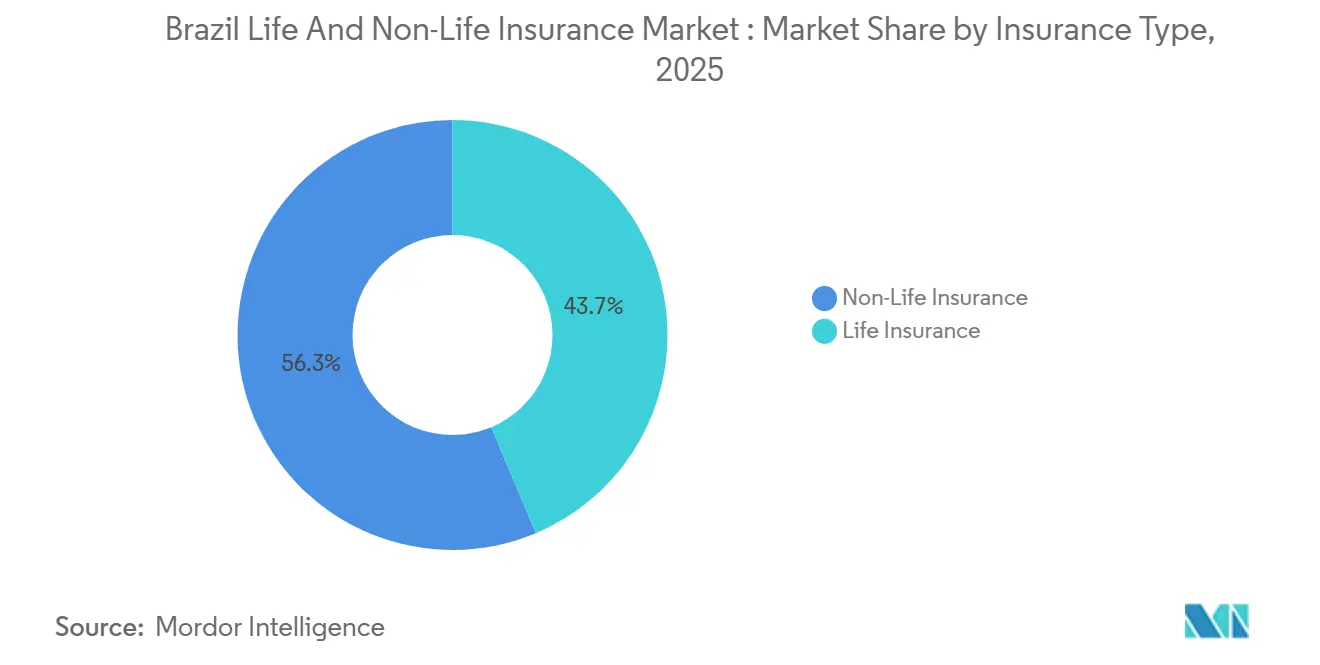

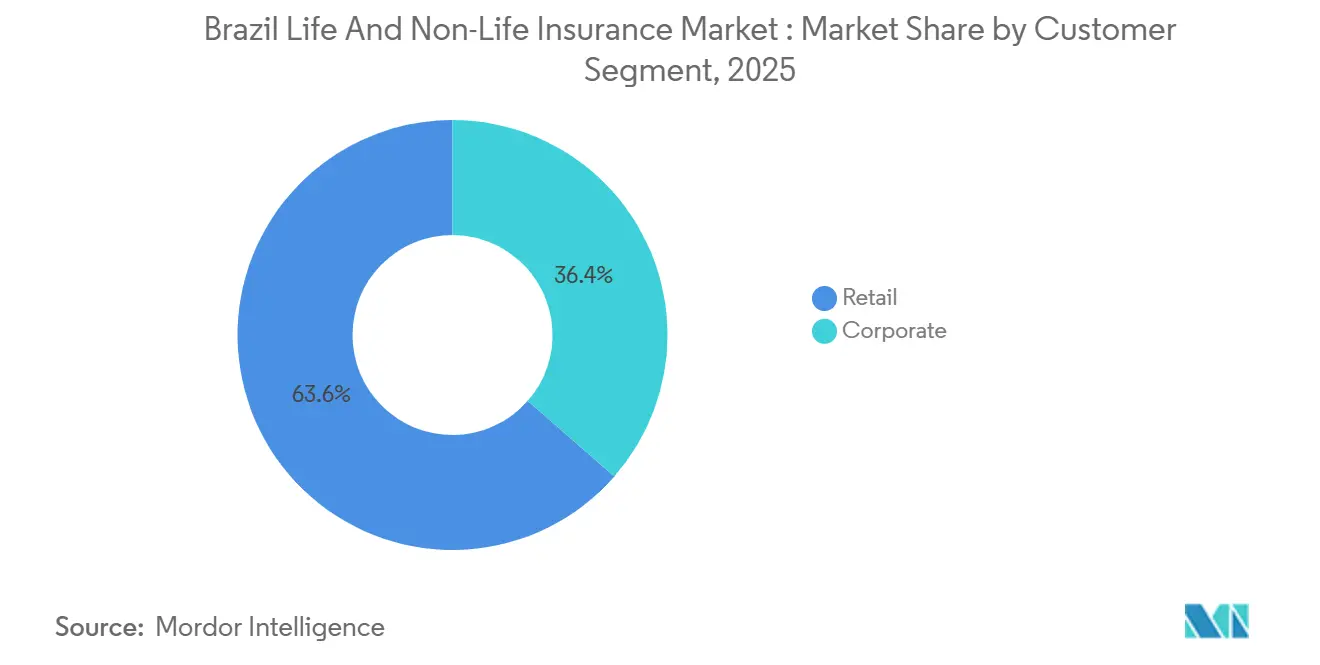

The Brazil life and non-life insurance market is supported by structural demand, regulatory modernization, and digital distribution scale. Non-life lines controlled 56.34% of 2025 premiums, while life coverage is expected to expand faster at 6.91% through 2031, reflecting rising awareness of mortality and critical-illness risk across aging households and formal workers in urban corridors. Bancassurance anchors distribution, with banks responsible for 41.23% of 2025 flows, while direct digital channels are expected to post a 7.84% CAGR as open-insurance APIs and Pix reduce onboarding friction and premium-collection hurdles. Retail customers held 63.56% of the 2025 value, but corporate buyers are projected to grow at 7.42% annually, helped by emerging environmental-liability mandates and group-benefits expansion. Regionally, the Southeast led with 41.24% of 2025 premiums, and the North shows the fastest forecast CAGR at 6.83% as micro-ticket products reach underserved municipalities.

Key Report Takeaways

- By insurance type, non-life lines led with 56.34% market share in 2025, while life insurance is forecasted to expand at a 6.91% CAGR through 2031.

- By customer segment, retail held 63.56% of the 2025 value, and corporate buyers are projected to grow at a 7.42% CAGR through 2031.

- By distribution channel, banks controlled 41.23% of 2025 flows, while direct digital channels are projected to record a 7.84% CAGR through 2031.

- By geography, the Southeast corridor accounted for 41.24% of 2025 premiums, and the North is expected to post the fastest CAGR at 6.83% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Life And Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising middle-class income & financial literacy | +1.2% | Southeast, South early; spreading to Northeast urban hubs | Medium term (2-4 years) |

| Growth in private-health expenditure & employer plans | +1.8% | Southeast, South; spillover to Brasília | Short term (≤ 2 years) |

| Expansion of digital distribution & bancassurance | +1.5% | National, strongest in Southeast metros; accelerating in North and Center-West via fintech platforms | Short term (≤ 2 years) |

| Open-insurance API framework accelerates personalization | +0.9% | National, with early gains in Southeast and South, North lagging | Medium term (2-4 years) |

| Climate-driven catastrophe awareness boosts property & rural demand | +1.3% | South flood zones, Northeast drought belt, Center-West crop pilots | Short term (≤ 2 years) |

| Tax-expenditure reform pushes demand for annuity wrappers | +0.9% | National; concentrated among high-net-worth segments in Southeast financial centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rising Middle-Class Income & Financial Literacy

Brazil’s middle class, defined as households earning between USD 361 and USD 1,445 monthly, now covers a broad population base, but life insurance ownership remains near 18%, signaling a wide protection gap for basic term and critical-illness products. Life-insurance premiums grew 8.4% year-on-year in the first half of 2025 to USD 6.82 billion, with individual life advancing 13.2%, aided by CNseg-led awareness drives and financial education under ENEF[1]CNseg, “Seguros de Pessoas crescem 8,4% no primeiro semestre de 2025,” CNseg, cnseg.org.br. Penetration is higher in the Southeast and South than in the North, mirroring income levels and formal employment, with residential and life coverage lagging in lower-income municipalities. Digital orchestration matters, as WhatsApp-enrollment journeys and Pix-based recurring contributions lowered onboarding friction for classes C and D and shifted acquisition economics for pension-linked products. Near-term growth aligns with the Central Bank’s macro backdrop in 2025, when services posted sequential strength even as the broader economy stabilized, supporting household willingness to persist with basic risk covers.

Growth in Private-Health Expenditure & Employer Plans

Private health-plan beneficiaries reached 53.23 million as of September 2025, up 2.1% year-on-year, and group plans represented nearly three-quarters of medical-assistance contracts, confirming the employer channel’s central role. ANS authorized premium adjustments for 2025 in specified bands while reporting sector profitability at a multi-year high for the first nine months, driven by a lower claims ratio that stabilized below recent peaks. Larger operators captured a majority of sector earnings due to scale in network contracting and administrative efficiency, which favors carriers with integrated provider relationships. The aging population and growing chronic-disease burden sustain demand for supplemental health coverage even when pricing is controlled at the regulatory level. Banks continue to cross-sell health-related covers alongside life and pension products, using payroll relationships and digital journeys to lift attachment to protection bundles.

Expansion of Digital Distribution & Bancassurance

Digital channels are growing faster than legacy outlets as insurers compress quote-to-bind cycles and add embedded offers into broader consumer journeys. Bradesco Seguros reported multi-channel progress in 2024 and 2025, supported by a portfolio of digital tools and investment in analytical maturity, while Brasilprev’s WhatsApp-based enrollment added speed and reduced cost-to-serve for lower-ticket contributions. The Pix instant-payment network simplified premium collection and enabled smaller-ticket products to reach profitability at scale, which is relevant for accident, device protection, and micro-life. Bancassurance remains the dominant route for pensions, mortgage life, and credit-linked protection, with investor materials from leading bank-owned groups confirming high penetration in bank-originated contributions and premiums across those lines. Open Finance, formally completed in 2024, broadened data-sharing and interoperability across financial products and created a pathway for open insurance to expand personalization in underwriting and servicing[2]Banco Central do Brasil, “Open Finance,” Banco Central do Brasil, bcb.gov.br.

Open-Insurance API Framework Accelerates Personalization

SUSEP’s open-insurance architecture has moved from design to scale after Open Finance completion, enabling policy and claims data sharing once a customer consents and elevating competition on price and service. Interoperable APIs standardize formats and allow customers to port data between providers within defined time windows, improving the transparency of coverages and premium schedules. Digital-focused carriers are deploying AI-driven underwriting models that ingest shared data to tailor quotes to granular risk profiles and link cover to contextual triggers such as vehicle telematics or spend patterns. Bank-owned groups also activated data-sharing capabilities in life and pensions, using the same infrastructure to widen cross-selling inside their large retail and payroll bases. Broker roles are evolving toward data orchestration, where intermediaries consolidate consented information from multiple sources and simplify comparison at bind.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High premium-tax/IOF burden limits penetration | -1.4% | National; acute for high-ticket VGBL contributions | Short term (≤ 2 years) |

| Macro volatility & high rates hurt affordability/lapse | -1.1% | National; steeper in the Northeast and North | Short term (≤ 2 years) |

| ANS co-pay caps & unlimited-therapy rules squeeze margins | -0.8% | Southeast and South concentration, nationwide compliance | Medium term (2-4 years) |

| Consumer-protection litigation inflates liability losses | -0.6% | Southeast judicial districts with national spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Premium-Tax/IOF Burden Limits Penetration

The tax wedge on insurance-linked savings reduces the appeal of higher-ticket contributions and weakens incentives to rebalance toward pension wrappers during rate normalizations. VGBL revenue trends in 2025 showed contraction alongside higher redemptions, reflecting alternative returns available in fixed-income instruments and the tax burden on incremental contributions above defined thresholds. Property-casualty pricing also faces state and municipal levies that vary by product and jurisdiction, fragmenting quotes across regions and complicating price comparison for commercial buyers. Sectoral tax receipts remain material for public finance, which limits the likelihood of near-term relief even as industry associations argue for measures to reduce the cost of protection for mid-income households. The combined effect holds back mass-market adoption in auto and residential lines, where penetration trails advanced-economy benchmarks by wide margins.

Macro Volatility & High Rates Hurt Affordability/Lapse

The Selic rate remained elevated through 2025, and real yields stayed positive after inflation, creating a high hurdle for long-duration savings products and reducing affordability for lower-income buyers. Redemptions increased as households prioritized liquidity and debt service or pursued fixed-income returns, while lapses in individual life rose above historical ranges during the mid-2025 stress period. Exchange-rate dynamics also increased the cost of reinsurance for contracts denominated in hard currency and compressed margins in specialized lines. Inflation pressure diminished purchasing power for households with lower disposable income, and confidence indicators signaled cautious consumption during the year. When the economy stabilized toward the end of 2025, sector performance showed mixed quarter-on-quarter results, suggesting that affordability remains a constraint for new issuance and persistency.

Segment Analysis

By Insurance Type: Life Gains Share as Aging and Middle-Class Growth Converge

Non-life coverage accounted for 56.34% of the market in 2025, while life products are projected to grow at 6.91% through 2031. This reflects shifting demographics and increased financial awareness. Mandatory and credit-linked covers sustain property-casualty activities, while mortality and critical illness needs drive individual and group life insurance growth at payroll and credit initiation points. The Brazil insurance market leaned toward non-life in 2025, but life insurance is expected to outperform, driven by rising adoption among mid-income customers in Southeastern cities. Open-insurance data sharing and improved digital processes are enhancing quoting and onboarding for both segments. The 2024 flood season highlighted under-insurance issues and boosted demand for property coverage.

By September 2025, health plans, a key non-life segment, covered 53.23 million beneficiaries, maintaining stable penetration despite regulatory caps. Motor insurance volumes moderated as vehicle prices stabilized, with telematics adoption reducing loss frequency. Property insurance gained traction through mortgage flows and mandated coverage for financed units, though catastrophe losses led to repricing in flood-prone areas. Liability coverage is expanding as climate policies advance, increasing demand for specialized covers. Broader product adoption is expected as insurers integrate coverage with digital commerce, mobility, and utility payments, supported by rising micro-ticket attachments.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Customer Segment: Corporate Buyers Accelerate as ESG Mandates Bite

Retail customers accounted for 63.56% of the value in 2025, remaining the primary drivers of bancassurance and direct digital models. Corporate buyers are projected to grow at 7.42% annually through 2031, driven by group benefits and specialized liability demand. Employer-sponsored health plans dominate medical-assistance beneficiaries, highlighting HR-led procurement and multi-year retention in group arrangements. Corporate insurance spans surety, D&O, liability, and rural sectors, supported by infrastructure activities and supply chain needs in industrial and agribusiness regions. Rising ESG-linked exposures and carbon-compliance policies are increasing demand for pollution-legal liability within industrial clusters. Retail micro-insurance is scaling through simplified underwriting and embedded offers, reaching underserved households.

Corporate buyers leverage larger risk pools and negotiate for discounts to reduce commission loads and improve retention during benefit renewals. In 2024, bank-owned insurers utilized agribusiness and SME relationships to cross-sell group life and rural covers, enhancing pricing accuracy through centralized data. SMEs remain under-insured in business-interruption and key-person coverage, but digital underwriting platforms and accounting-software partnerships are reducing costs and cycle times. Retail persistency is higher for auto and residential products than standalone life, while group benefits show superior renewal rates. The Brazilian life and non-life insurance sectors are refining segment pricing using open-finance and open-insurance data sharing, improving persistency, and reducing lapses during the forecast period.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Direct Digital Scales While Bancassurance Holds Commanding Lead

Banks held 41.23% of distribution flows by value in 2025, with bancassurance dominating life insurance, pensions, credit life, and mortgage-related protections. Flagship institutions leveraged branch networks, payroll systems, and mobile apps for cross-selling while excelling in asset administration and pension contributions. Direct sales are expected to grow at a 7.84% CAGR through 2031, driven by API connectivity that streamlines quote-to-bind processes and enhances mobile conversions. Digital channels gained traction in 2025, with Pix integration improving onboarding and straight-through processing. Embedded offers at checkout in travel, electronics, and mobility continue to attract first-time policyholders and price-sensitive segments in Brazil's life and non-life insurance market.

Broker networks are consolidating to sustain scale in benefits and property & casualty advisory amid rising commission pressures in direct and embedded channels. Global fintech entrants like Acrisure have expanded specialty capabilities and aligned with local brokerages to address complex enterprise risks. Bank-owned groups maintain leadership in pension contributions and mortgage-linked covers, while digital platforms grow in micro-ticket auto, residential, and accident insurance. Investments in underwriting and claims automation are enhancing both models, with digital journeys improving conversions at lower costs. Brazil's insurance market is expected to retain its dual structure, with bancassurance driving large-ticket flows and direct and embedded channels expanding first-time purchases and upselling opportunities.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Southeast captured 41.24% of premiums in 2025, driven by affluent households, a strong bancassurance network, and early adoption of open-insurance tools. São Paulo and Rio de Janeiro lead in life and property insurance penetration, while Minas Gerais excels in group-health coverage due to industrial employers. Despite its dominance, the Southeast's forecast CAGR is moderate compared to frontier regions. Micro-products have the potential to reach uninsured middle-income households in residential and accident lines. Regulatory clarity fosters cross-selling within bank ecosystems, where customers with multiple relationships show higher persistency and lower lapse rates. The Brazil life and non-life insurance market is expected to maintain deep penetration in Southeast metros due to income alignment, distribution capacity, and product diversity.

In 2024, the South faced severe-weather events, highlighting under-insurance in property lines and the need for climate resilience[3]CNseg, “THE ROLE OF INSURANCE IN CLIMATE TRANSITION,” CNseg, casadoseguro.org.br. Repricing occurred in flood-prone areas, and parametric crop cover pilots advanced with reinsurer and insurtech support to address drought and rainfall volatility. The region’s culture of private risk transfer and cooperative networks sustains residential coverage above the national average. Public discussions on catastrophe funding and private risk transfer are intensifying, while climate-related product innovations expand beyond traditional indemnity models. The Brazil life and non-life insurance market is likely to see increased adoption of parametric solutions in Southern agricultural corridors, where payout speed and transparency are valued.

The North is forecasted to grow at the fastest CAGR of 6.83% through 2031, supported by digital access that bypasses limited branch infrastructure and enables micro-ticket life and accident insurance. Smartphone use in urban centers facilitates WhatsApp and app-based distribution, with Pix streamlining premium collection and renewals. Health-plan coverage, though below the national average, is growing faster than the country’s mean due to expanding formal employment in select industries. Financial literacy initiatives aim to close awareness gaps in households reliant on informal risk pooling. Simplified products and embedded journeys support first-time purchases at lower premiums, driving growth in Brazil's life and non-life insurance market in frontier regions.

Competitive Landscape

The Brazil life and non-life insurance market remains moderately concentrated, with the top five groups accounting for 34.5% of non-VGBL premiums as of September 2025. Digital entrants and regional specialists continue to gain market share. Bancassurance leaders leverage distribution advantages to support life, pension, and credit-linked products while expanding provider relationships in health to influence cost-of-care. Bradesco Seguros and other bank-affiliated groups benefit from scale in beneficiaries, assets, and distribution networks, alongside investments in analytics and modernization of core platforms. Reinsurers and engineering-focused carriers are increasing their presence in property-casualty, signaling interest in direct underwriting as regulatory conditions improve. Portfolios are shifting toward embedded and micro-ticket offerings, supported by investments in traditional distribution channels.

Strategic initiatives highlight convergence between underwriting and care delivery, as well as distribution and risk-capital capabilities. Bradesco expanded hospital partnerships to achieve network efficiencies in major metropolitan areas, aligning cost and outcome incentives. International players and global fintechs strengthen their presence through licensing and rebranding, such as FM Global’s direct-insurer license and Acrisure’s integration of brokerages under a unified brand. AI-enabled underwriting and pricing accelerate rate reviews and shorten development cycles, with platform modernizations supporting data-driven underwriting and faster claims processing. Carriers combining distribution scale with operational efficiency are rewarded.

Growth opportunities exist in residential, auto, SME protection, and climate-linked agricultural risks, where coverage rates remain low. Parametric insurance pilots for drought and rainfall risks scale with reinsurer participation, enabling rapid payouts post-event. ESG governance is embedded in regulatory expectations, with insurers formalizing frameworks and disclosures. ANS publishes quality and complaint indices, influencing public perception and incentivizing service improvements. The market is expanding its product mix toward data-rich risk pools and improving accessibility through simplified onboarding and embedded insurance offerings, with non-VGBL premiums reaching 164.826 billion Reais by September 2025.

Brazil Life And Non-Life Insurance Industry Leaders

BrasilSeg (Banco do Brasil & MAPFRE)

Bradesco Seguros

SulAmérica

Porto Seguro

Caixa Seguridade

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: FM Global’s Brazilian subsidiary, FM Seguros S.A., obtained a direct-insurer license from SUSEP, ending its reinsurance-only model and preparing to write property-casualty coverage for large multinationals from 2026.

- August 2025: Acrisure launched its brand in Brazil by rebranding the acquired entity It’sSeg, consolidating 880 employees across 16 offices to serve 1,500 corporate clients and adding facultative reinsurance capabilities.

- July 2025: MAG Seguros launched Favela Seguros in partnership with NGO CUFA, piloting life coverage distribution tailored for residents in Brazil’s favelas and creating community sales roles supported by a digital platform.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Brazil's life and non-life insurance market as the aggregate gross written premiums generated by resident carriers across all individual and group life, pension, property, motor, health, liability, marine, and agricultural lines. These values are captured in USD at the statutory level and exclude inward reinsurance and unit-linked investment funds.

Scope exclusion: premiums ceded to reinsurers and capital-market ILS structures fall outside this sizing.

Segmentation Overview

- By Insurance Type (Value)

- Life Insurance

- Non-Life Insurance

- Motor Insurance

- Health Insurance

- Property Insurance

- Liability Insurance

- Other Insurance

- By Customer Segment (Value)

- Retail

- Corporate

- By Distribution Channel (Value)

- Brokers

- Agents

- Banks

- Direct Sales

- Other Channels

- By Region (Value)

- North

- Northeast

- Southeast

- South

- Center-West

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct structured interviews with underwriting executives, bancassurance heads, independent brokers, and SUSEP officials across Sao Paulo, Rio de Janeiro, Recife, and Porto Alegre. These dialogues validate premium flows, average selling prices, lapse behavior, and digital-channel uptakes that public data leave opaque.

Desk Research

We begin by mapping the market landscape through high-credibility, open sources such as SUSEP's monthly premium bulletins, the Brazilian Central Bank's financial stability notes, IBGE household-income surveys, ANS health-coverage dashboards, and World Bank macro data. Annual reports filed by leading insurers and rating-agency solvency reviews enrich carrier-level insight, while paid databases, D&B Hoovers for company financials and Dow Jones Factiva for news flow, help triangulate growth signals. This multi-angle scan clarifies premiums, channel splits, and regulatory inflection points before any modeling occurs.

Trade associations like CNseg, plus patent and regulatory filings, supplement trend spotting on telematics, bancassurance APIs, and climate-risk products. The sources cited above are illustrative; many additional publications were consulted for data checks and context building.

Market-Sizing & Forecasting

The core model applies a top-down build that lifts SUSEP line-of-business premiums, adjusts for exchange moves, and re-casts them into constant 2024 dollars; selective bottom-up carrier roll-ups and channel checks then fine-tune totals. Key variables like GDP per capita, vehicle fleet expansion, bancassurance share, claims ratio inflation, and PIX transaction volumes drive both historical calibration and projections. Forecasts employ multivariate regression blended with scenario analysis around interest-rate and catastrophe-loss bands, with gaps in micro-segments filled by sample ASP × policy-count proxies.

Data Validation & Update Cycle

Outputs pass a two-stage analyst review that screens variance against independent macro indicators and prior year loss experience; anomalies trigger re-contacts. Reports refresh annually, while material events such as major floods prompt an interim update before client delivery.

Why Mordor's Brazil Life And Non-Life Insurance Baseline Stands Firm

Published estimates often differ; scope choices, currency treatments, and refresh cadences rarely match perfectly.

Key gap drivers here include: some publishers model only retained risk, others merge reinsurance or exclude private pension premiums; a few freeze assumptions on bancassurance ASP drift, whereas Mordor updates them quarterly; refresh timing also varies, with fast-moving FX swings widening USD gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 135.81 B (2025) | Mordor Intelligence | - |

| USD 134.0 B (2024) | Global Consultancy A | Does not adjust for 2025 pension contribution spike; life-annuity pool blended with investment funds |

| USD 67.91 B (2024) | Industry Analytics B | Captures only direct life and motor lines, excludes group health and agricultural covers |

Taken together, the comparison shows that Mordor's disciplined scope selection, quarterly variable refresh, and dual-pass validation yield a balanced, transparent baseline investors can trust for planning and benchmarking decisions.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and 2031 outlook for the Brazil life and non-life insurance market?

The Brazil life and non-life insurance market size is USD 144.72 billion in 2026 and is projected to reach USD 198.84 billion by 2031 at a 6.56% CAGR.

Which segment is growing faster within Brazil’s life and non-life coverage?

Life coverage is forecast to grow at 6.91% through 2031, outpacing non-life, which reflects aging demographics and better financial literacy campaigns.

How significant is bancassurance in Brazil’s distribution mix in 2025?

Banks controlled 41.23% of 2025 distribution flows, and they remain the dominant route for life, pensions, credit life, and mortgage-related products.

Which customer segment presents the strongest growth outlook to 2031?

Corporate buyers are projected to grow at 7.42% annually due to employer-sponsored benefits and rising demand for liability and ESG-linked coverage.

Which region leads by share, and which is the fastest-growing area?

The Southeast led with 41.24% of 2025 premiums, while the North is expected to post the fastest CAGR at 6.83% through 2031.

What role does Open Finance play in the Brazil life and non-life insurance market?

Open Finance and open-insurance APIs enable data sharing and personalization, improving quote-to-bind speed and supporting embedded and direct digital sales.