Overhead Catenary System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 35.14 Billion |

| Market Size (2030) | USD 58.81 Billion |

| Growth Rate (2025 - 2030) | 10.85% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Overhead Catenary System Market Analysis by Mordor Intelligence

The overhead catenary system market size reached USD 35.14 billion in 2025 and is projected to climb to USD 58.81 billion by 2030, representing a robust 10.85% CAGR. This expansion stems from synchronized government decarbonization mandates, rapid rail-network modernization, and shifting freight corridors toward electric traction. Record public-sector capital outlays, such as the USD 2.4 billion United States rail-infrastructure program Consolidated Rail Infrastructure and Safety Improvements (CRISI), and USD 1.1 billion set aside for grade-crossing elimination, have multiplied tender pipelines and eased near-term funding risks. Asia-Pacific remains the largest regional demand center on the back of China’s high-speed rail surge and India’s ongoing network electrification, while the Middle East and Africa are accelerating the fastest thanks to multi-billion-dollar greenfield projects across Egypt, Morocco, and the GCC. Component makers are racing to introduce lightweight composite structures and smart IoT monitoring to curtail life-cycle costs, and suppliers are localizing production, exemplified by Siemens’ New York facility, to reduce logistics exposure and comply with domestic-content rules.

Key Report Takeaways

- By application, rail transport commanded 59.14% of the overhead catenary system market share in 2024; light rail transit is projected to advance at a 12.15% CAGR through 2030.

- By component, catenary wires led with 43.06% of the overhead catenary system market share in 2024; insulators are poised for the fastest 11.62% CAGR on growing demand for smart monitoring.

- By technology, single-wire systems captured 49.33% of the overhead catenary system market share in 2024, while rigid catenary systems are forecast to expand at a 12.56% CAGR through 2030.

- By end-use, public transportation captured 64.18% of the overhead catenary system market share in 2024 and is forecast to expand at a 10.97% CAGR through 2030.

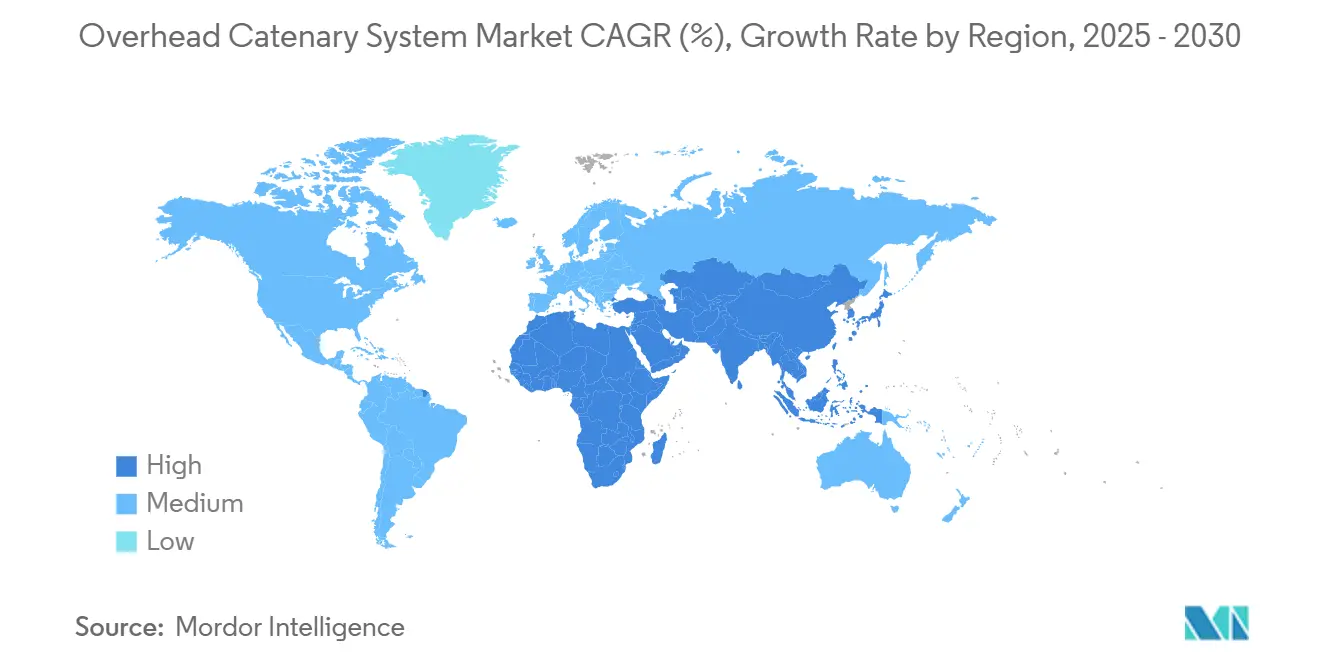

- By geography, Asia-Pacific held 47.25% of the overhead catenary system market share in 2024, and the Middle East & Africa region is set to post the highest 11.14% CAGR to 2030.

Global Overhead Catenary System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban and High-Speed Electrification | +3.2% | Global; APAC and Europe lead | Medium term (2-4 years) |

| Government Decarbonization Mandates | +2.8% | Global; strongest in EU and North America | Long term (≥ 4 years) |

| Lower Lifecycle Cost | +1.9% | Global; especially emerging markets | Medium term (2-4 years) |

| Modernization of Aging Infrastructure | +1.7% | North America and Europe | Long term (≥ 4 years) |

| Smart IoT Catenary Monitoring | +0.8% | Developed markets, expanding globally | Short term (≤ 2 years) |

| Lightweight Composite Components | +0.6% | Global; early APAC adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification of Urban and High-Speed Rail

National and regional rail agencies are committing unprecedented sums to electrification. Germany’s Euregiobahn program is converting 47 km of regional lines to the 15 kV 16.7 Hz standard. In the United Kingdom, a city-region transport fund extends tramways and metro links through 2031. Australia earmarked AUD 78.8 million (~USD 51.9 million) for the Sydney-Newcastle high-speed rail business case, cementing electrification as the backbone of intercity mobility [1]“High-Speed Rail Authority Budget 2025,” Commonwealth of Australia, infrastructure.gov.au. Even resource-rich corridors are transitioning: Queensland is evaluating electrification options for the Mount Isa line to support its critical minerals economy. These deployments illustrate how passenger and freight segments alike now view catenary systems as a non-negotiable prerequisite for future capacity upgrades.

Government Decarbonization Mandates

Mandatory climate-action roadmaps are embedding overhead catenary system market adoption into national regulations. The Biden-Harris administration has already committed significant investment toward grade-crossing elimination and passenger-rail enhancements that favor electric traction [2]“Biden-Harris Administration Announces Rail Infrastructure Investments,” U.S. Department of Transportation, transportation.gov. In Europe, Bavaria and Baden-Württemberg jointly approved EUR 450 million (~USD 530.5 million) to electrify the 72.5 km Ulm–Aalen line, underscoring multistate alignment on net-zero transport. China’s 2060 carbon-neutral pledge sustains large-scale projects such as the Nanning–Pingxiang “Four Electrics” installation across 213.88 km of new high-speed track. Supplier selection criteria now often include ISO 14001 certification, driving manufacturers like Dalekovod OSO to maintain externally audited environmental-management systems.

Lower Lifecycle Cost vs. Diesel Traction

Electric networks deliver superior economics over a 30-year horizon. Caltrain’s public electrification model projects lower per-mile operating costs than diesel while supporting higher headways. Britain’s commitment to finish Midland Main Line electrification between Kettering and Wigston and to upgrade West Coast Main Line power supplies demonstrates how long-run maintenance and fuel-price stability outweigh higher up-front capex [3]“City Region Sustainable Transport Settlements 2025-32,” Department for Transport (UK), gov.uk. Similar payback logic underpins Inland Rail’s future-proofing for electric conversion as Australian freight volumes expand. Public-health co-benefits, chiefly urban air-quality improvements, reinforce the financial case for rapid switchover.

Modernization of Aging Rail Infrastructure

Mature networks are embedding catenary upgrades into track-renewal cycles. BNSF Railway’s 2025 capital plan includes replacing 2.5 million ties and 410 miles of rail, creating ideal windows to install power and signaling concurrently. New Zealand has allocated significant capital to overhaul Wellington’s Johnsonville, Kāpiti, and Hutt Valley lines, positioning electrification as a standard element of asset-life extension. The United Kingdom East Coast Main Line digital-signaling upgrade targets a one-third delay reduction and anticipates 4,800 supply-chain roles, illustrating how modernization fosters reliability and employment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Electrification Costs | –2.1% | Global; strongest in emerging markets | Short term (≤ 2 years) |

| Legacy Asset Integration Complexity | –1.4% | North America and Europe | Medium term (2-4 years) |

| Competition From New Trains | –0.9% | Europe and Japan | Long term (≥ 4 years) |

| Copper Price Volatility | –0.8% | Global supply chain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex for Electrification

Capital intensity remains the chief hurdle, especially in cost-sensitive regions. Queensland’s Direct Sunshine Coast Stage 1 dual-track line is priced accordingly for 19 km. Germany’s Ulm–Aalen program reaches significant investment per kilometer, even inside a developed corridor. Such sticker prices often trigger funding pauses, evidenced by the U.K. temporarily suspending Midland Main Line Phase 3. Public-private partnerships can fill gaps, but add due diligence complexity and extend tender timelines.

Integration Complexity with Legacy Assets

Electromagnetic interference and clearance limits complicate retrofits. Transportation Research Board studies show signaling systems must be shielded or replaced when traction power is introduced. Bridge structures in North America often require costly track-lowering or catenary-profile adjustments to retain freight clearance. AC/DC interface zones demand custom changeover stations and rigorous operating rules, stretching project schedules and requiring specialist engineering teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Rail Transport Leads Urban Mobility Transformation

Rail transport accounted for 59.14% of the overhead catenary system market share in 2024, reflecting its status as the backbone of intercity connectivity. Its share is anchored by China’s ongoing high-speed corridor rollouts and North America’s freight-line modernization. Simultaneously, the segment benefits from obligatory net-zero requirements that force freight carriers to prepare for electric traction upgrades even before installation dates are finalized. Light rail transit, although smaller today, is expanding at a 12.15% CAGR through 2030 as metropolitan areas invest in pollution-free commuting solutions.

City-region transport deals such as the United Kingdom’s GBP 15.6 billion (~USD 21 billion) program and Germany’s Euregiobahn illustrate how tram and metro extensions dovetail with broader sustainability goals. Tramway networks in Eastern Europe and Asia maintain cautious but steady adoption, leveraging legacy trolleybus skills for workforce cross-training. Urban planners also see trolleybus systems as low-cost electrification bridges where rail alignments face right-of-way constraints. Accordingly, diversified application demand stabilizes the overhead catenary system market, mitigating exposure to any single project class.

By Component: Wire Technologies Drive Innovation

Catenary wires represented the largest slice of 43.06% in the overall overhead catenary system market share in 2024, thanks to inevitable conductor replacements during each electrification rollout. Alloy R&D is now centered on reducing resistive losses without exacerbating copper dependence, and several European programs are piloting aluminum-magnesium-silicon blends that promise a significant weight reduction. Insulators, the fastest-growing component at an 11.62% CAGR, capitalize on embedded sensor packages that relay real-time leakage currents and ambient-temperature data to maintenance crews.

Support structures stand at the frontier of composite innovation: CFRP and GFRP masts lower handling weight, while factory-precast anchor blocks accelerate on-site assembly. Connector devices incorporate digital junction boxes that relay load currents into central asset-management dashboards. Suppliers are consequently aligning production systems with ISO 50001 energy-management mandates, reinforcing the sustainability narrative that rolling-stock operators and public funders demand.

By Technology: Rigid Systems Gain High-Speed Traction

Single-wire configurations maintained 49.33% of the overhead catenary system market share in 2024, largely because their capital costs remain lowest for conventional passenger and urban lines. Yet high-speed corridors above 250 km/h are pivoting to rigid catenary systems, which are forecast to grow at an annual 12.56% through 2030. Brightline West’s Las Vegas–Southern California project, supported by Siemens’ New York plant, explicitly specifies rigid technology to ensure aerodynamic stability at 300 km/h.

Double-wire solutions continue to serve heavy-axle freight routes where current draw exceeds single-wire capacity, but line speeds remain below rigid thresholds. Sectional catenary designs find favor in dense metros that must isolate maintenance zones without disrupting peak-hour headways. As computational fluid-dynamics models refine pantograph-interaction parameters, procurement teams base awards on total life-cycle cost rather than capital outlay, raising the technology bar across tenders.

By End-Use: Public Transportation Dominates Sustainable Mobility

Public operators absorbed 64.18% of the overhead catenary system market size in 2024 and are expected to grow at a 10.97% CAGR to 2030. Australia’s Suburban Rail Loop, powered entirely by renewable electricity, exemplifies how regional authorities anchor climate policy in mass-transit electrification. Europe’s TransPennine Route Upgrade and East West Rail to Cambridge likewise integrate catenary deployment alongside signaling and digital-control modernization.

Freight carriers are the second-largest customer set, hedging fuel-price swings and increasingly facing carbon surcharges at intermodal ports. Mining and construction niches rely on short-haul catenary layouts in tunnels and site perimeters, where diesel exhaust poses health hazards and ventilation costs. Collectively, these diversified end-uses reinforce the continual demand cycle that underpins the overhead catenary system industry’s revenue stability.

Geography Analysis

Asia-Pacific remained the epicenter of demand, holding 47.25% of the overhead catenary system market share in 2024 on the strength of China’s Nanning–Pingxiang installation and India’s Mumbai–Ahmedabad high-speed corridor awards. Japan continues to pioneer aerodynamic pantograph research, while South Korea integrates real-time catenary analytics into its metro networks.

The Middle East and Africa are on course for an 11.14% CAGR, buoyed by Egypt’s national electrification and Morocco’s rail-modernization blueprint. Gulf Cooperation Council states are synchronizing cross-border alignments that will eventually link Oman’s Duqm Port to European markets, a step expected to elevate regional tender volumes sharply after 2026.

Europe posted steady additions through secondary-line upgrades, Germany’s Euregiobahn and the Ulm–Aalen Brenzbahn being illustrative. North America accelerated as Brightline West secured a USD 3 billion federal grant, while Siemens localized production to satisfy Buy-America clauses. South America runs a mixed trajectory: Brazil’s São Paulo Urban Train Company and Argentina’s Belgrano Cargas logistics corridor are electrification bright spots, but macro-fiscal pressures still temper broader rollouts.

Competitive Landscape

The overhead catenary system market demonstrates moderate concentration. Siemens, Alstom, and CRRC account for a significant global revenue, leveraging multi-continent factories and proprietary monitoring suites. Siemens’s plant builds rigid catenary assemblies for domestic high-speed contracts, trimming lead times and aligning with Buy-America stipulations. Alstom’s French capacity upgrade adds rolling-stock shells and ROCS assembly lines to support Avelia Horizon demand.

Hitachi Energy is investing USD 155 million to scale transformer and switchgear output in North America, positioning itself for full-system “power-to-wire” packages. CRRC leverages massive domestic production economies and targets turnkey exports to Africa and Latin America, bundling financing with equipment to offset developing-market capex hurdles. Smaller specialists like Schunk Transit Systems and Wabtec carve out high-margin niches in real-time monitoring and pantograph packages, respectively.

Supply-chain resilience dominates board-level agendas. OEMs are dual sourcing copper and qualifying aluminum alloys, while composite-mast pioneers sign exclusive licensing deals to protect intellectual property. Certifications, ISO 9001, 14001, and 50001 have transitioned from differentiators to tender prerequisites, effectively filtering out unaccredited entrants. The pivot toward digital-service revenues, including data analytics subscriptions, is expected to reshape profit pools over the next five years.

Overhead Catenary System Industry Leaders

CRRC Corporation Limited

Alstom SA

Siemens AG

ABB Ltd.

Nexans SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Alstom signed with RESA Yapi Elektromekanik A.S. to supply ROCS for Türkiye’s 153 km Halkali–Kapikule corridor, part of the TEN-T backbone.

- November 2024: Mitsubishi Heavy Industries secured a contract to upgrade the overhead catenary system at Taiwan High-Speed Rail’s Zuoying depot.

- October 2024: IRCON commissioned India’s first ROCS rated for 180 km/h on the Delhi–Meerut RRTS twin-tunnel segment.

- April 2024: TSO Canada began an eight-year contract to design, supply, and maintain overhead line equipment for Toronto’s 15.6 km Ontario Line subway.

Global Overhead Catenary System Market Report Scope

| Rail Transport |

| Light Rail Transit |

| Tramways |

| Trolleybus System |

| Supports |

| Catenary Wires |

| Insulators |

| Connector Devices |

| Single Wire System |

| Double Wire System |

| Sectional Catenary System |

| Rigid Catenary System |

| Public Transportation |

| Freight Transport |

| Construction |

| Mining |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Rail Transport | |

| Light Rail Transit | ||

| Tramways | ||

| Trolleybus System | ||

| By Component | Supports | |

| Catenary Wires | ||

| Insulators | ||

| Connector Devices | ||

| By Technology | Single Wire System | |

| Double Wire System | ||

| Sectional Catenary System | ||

| Rigid Catenary System | ||

| By End-Use | Public Transportation | |

| Freight Transport | ||

| Construction | ||

| Mining | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the overhead catenary system market by 2030?

The market is forecast to reach USD 58.81 billion by 2030, growing at a 10.85% CAGR.

Which region leads demand for overhead catenary systems?

Asia-Pacific commanded 47.25% of 2024 revenue, buoyed by large-scale electrification projects in China and India.

Which technology segment is expanding fastest?

Rigid catenary systems are expected to grow at a 12.56% annual rate through 2030 due to high-speed rail adoption.

Which application is the main revenue driver?

Rail transport remains dominant, accounting for 59.14% of 2024 global revenue, while light rail is the fastest-growing segment.

Page last updated on: