Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

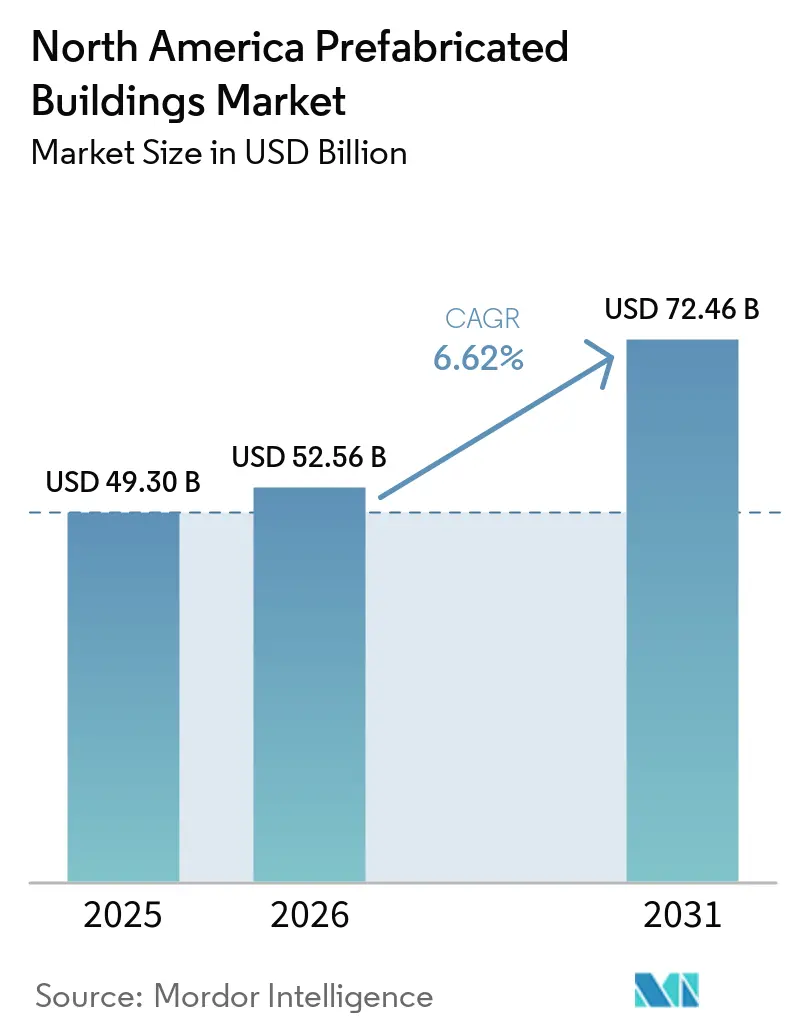

| Base Year Market Size (2025) | USD 49.30 Billion |

| Market Size (2026) | USD 52.56 Billion |

| Market Size (2031) | USD 72.46 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Prefabricated Buildings Market Analysis by Mordor Intelligence

The North America Prefabricated Buildings Market size was valued at USD 49.3 billion in 2025 and estimated to grow from USD 52.56 billion in 2026 to reach USD 72.46 billion by 2031, at a CAGR of 6.62% during the forecast period (2026-2031).The growth trajectory is propelled by persistent labor shortages, accelerating project timelines, and supportive federal programs that reduce financing friction for factory-built housing. Net-zero energy codes under IECC-2024, tax-equity incentives tied to affordable housing, and rapid expansion of e-commerce warehousing together elevate demand for precision-manufactured components[1]U.S. Department of Energy, “Energy Savings Analysis: 2024 IECC for Residential Buildings,” energycodes.gov .

Timber innovations, rising steel and aluminum tariffs that favor domestic sourcing, and breakthroughs in interstate code harmonization further reinforce the structural case for the North America prefabricated buildings market. Supply-chain localization around border regions, especially the United States–Mexico corridor, deepens cross-border integration that benefits factory throughput and logistics efficiencies, while the adoption of 3-D printing and plug-and-play electrical systems widens the technology moat for early movers[2]U.S. Department of Housing and Urban Development, “HUD Showcases 3-D Printing as an Innovative Solution for Affordable Housing Supply,” hud.gov.

Key Report Takeaways

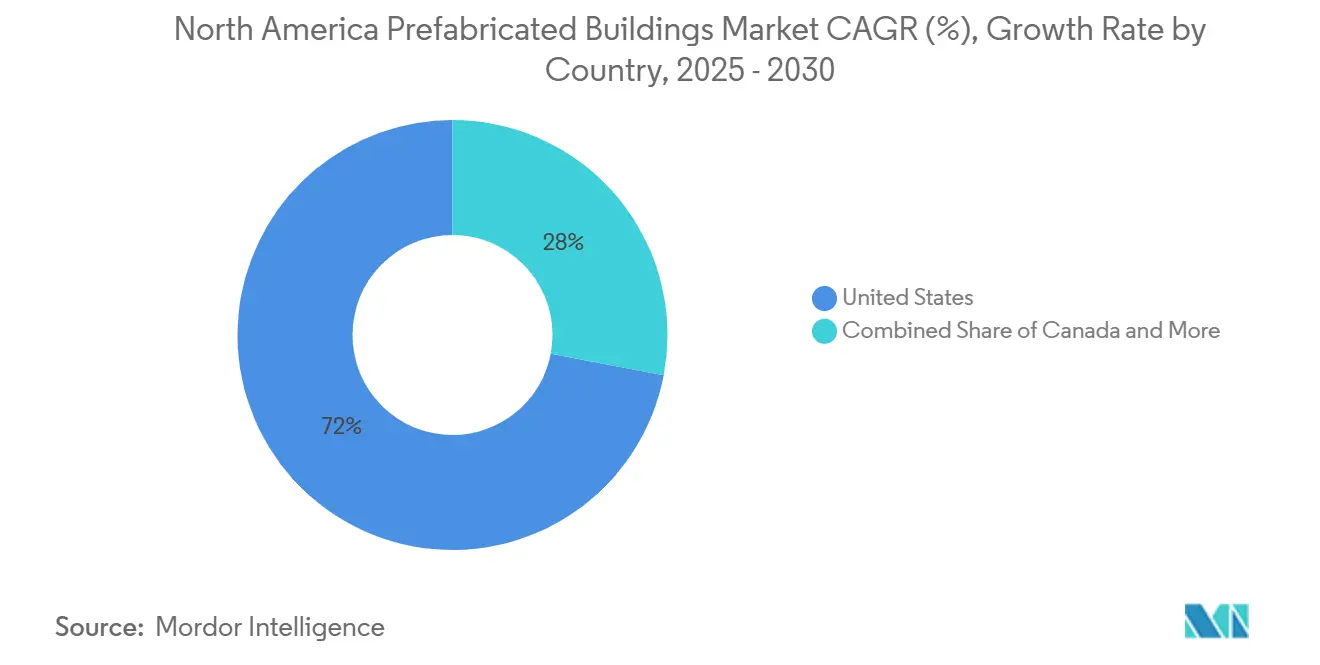

- By geography, the United States commanded 71.35% of the North America prefabricated buildings market share in 2025, while Mexico is forecast to advance at a 7.62% CAGR through 2031.

- By material, concrete led with 35.42% share of the North America prefabricated buildings market size in 2025; timber is set to climb at a 7.41% CAGR to 2031.

- By application, residential construction accounted for 50.35% of the North America prefabricated buildings market size in 2025, whereas the commercial segment is progressing at a 7.12% CAGR through 2031.

- By product type, modular buildings held a 38.28% slice of the North America prefabricated buildings market size in 2025; panelized and componentized systems are expanding at a 7.33% CAGR over the same horizon.

- Clayton Homes, Cavco Industries, and Skyline Champion together delivered 55% of manufactured-home shipments in 2024, underscoring the current balance of market power.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Prefabricated Buildings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tribal and rural modular-housing push | +1.2% | U.S. tribal lands, rural states | Medium term (2-4 years) |

| E-commerce warehouse boom | +1.5% | U.S. industrial corridors, Canadian logistics hubs | Short term (≤ 2 years) |

| Skilled-labor shortages | +1.8% | Urban construction centers across North America | Long term (≥ 4 years) |

| Net-zero energy codes | +1.0% | U.S. code-adopting states, Canadian provinces | Medium term (2-4 years) |

| Tax-equity financing for factory-built housing | +0.8% | U.S. low-income housing markets | Short term (≤ 2 years) |

| Coastal climate-resilience programs | +0.7% | Gulf Coast and Atlantic seaboard | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal Housing Policy Catalyzes Tribal and Rural Development

Updated Section 184 and Section 502 programs are widening access to capital by lowering guarantee fees and lengthening pilot waivers, directly improving affordability for buyers in low-density regions[3]U.S. Department of Housing and Urban Development, “Section 184 Indian Home Loan Guarantee Program,” hud.gov. Award allocations under the USD 225 million PRICE initiative earmark community-level upgrades that bundle infrastructure with manufactured-home installations, ensuring demand continuity for the North America prefabricated buildings market. As tribal authorities channel the funds into mixed-use developments, manufacturers capture incremental volume while lenders secure federal backstops, reducing credit-risk premiums. The multiplier effect extends to skilled-labor retention, because stable factory employment inside reservations helps stem outward migration of younger cohorts. In turn, companies achieve higher plant utilization rates, cushioning cyclical swings in broader housing starts.

E-commerce Infrastructure Drives Pre-Engineered Building Demand

Fulfillment-center footprints continue to swell as online retail penetration rises. With site selection gravitating toward last-mile nodes and cross-dock hubs, developers favor long-span steel frames, insulated roof panels, and plug-and-play MEP modules to guarantee 18-month delivery targets. Prefabrication compresses critical-path scheduling, enabling tenants to capture holiday-season turnover earlier than conventional builds, strengthening the value proposition inside the North America prefabricated buildings market. Industrial landlords also cite ESG scorecard requirements that reward low-waste assembly and repeatable envelope details. Despite growing plant backlogs, manufacturers mitigate bottlenecks by adopting takt-time production and by staging auxiliary lines in Mexico’s border states, trimming over-the-road miles for outbound shipments into the U.S. Sun Belt logistics belt.

Labor Market Disruption Accelerates Off-Site Construction Adoption

With construction unemployment hovering below 4% in 2025, general contractors scramble to fill specialty-trade openings, inflating wage bills and prolonging schedules. Factory settings automate repetitive tasks, reducing head-count dependence by up to 30% on equivalent gross floor area projects. The resulting visibility into cost and lead times attracts institutional investors funding data centers, hospitals, and mixed-income housing. ABB and Wieland Electric’s prefabricated electrical raceways demonstrate tangible productivity gains, cutting onsite installation time 70% and solidifying the competitive edge for firms investing in digital fabrication[4]ABB Group, “ABB and Wieland Electric Partner to Redefine Efficiency in Modular Construction,” new.abb.com . As baby-boomer retirements accelerate, younger workers gravitate toward climate-controlled, robotics-enabled facilities, reinforcing secular labor shifts that underpin the North America prefabricated buildings market.

Building Code Evolution Favors Low-Carbon Prefabricated Solutions

IECC-2024 mandates an average 9.8% energy-performance improvement in commercial projects compared with prior baselines. Factory-built assemblies reliably achieve air-sealing tolerances and continuous insulation targets, helping developers secure utility rebates and green-bond financing. Life-cycle studies show prefabricated methods cut embodied carbon by nearly 86 kg per m² while reducing annual energy loads 7.5%. States such as Virginia have streamlined plan-review procedures by referencing ICC/MBI Off-Site Construction Standards, shaving weeks off permit cycles. Faster approvals translate into earlier revenue recognition for project stakeholders, reinforcing a regulatory feedback loop that advantages participants in the North America prefabricated buildings market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Over-dimensional logistics costs | -1.3% | Long-haul routes with bridge or tunnel limits | Short term (≤ 2 years) |

| Fragmented state and municipal permitting | -0.9% | Multi-state projects | Medium term (2-4 years) |

| Limited factory throughput for giga-scale builds | -0.8% | High-growth tech corridors | Short term (≤ 2 years) |

| Consumer perceptions of resale discount | -0.6% | Suburban single-family markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Transportation Economics Challenge Volumetric Module Scalability

Permitting, escort vehicles, and structural clearances push transport costs beyond 15% of total installed value for single-lift volumetric units exceeding standard trailer dimensions. The cost curve steepens after 500 miles, prompting manufacturers to cluster plants within megaregions such as Texas’s Triangle and the Great Lakes. MMY US’s Louisville facility illustrates the strategy, adding 73 jobs and positioning annual output of 500 units within one-day drive times to Midwest metros. Panelized systems—shipped flat within legal load envelopes—circumvent the constraint, explaining their superior 7.62% CAGR inside the North America prefabricated buildings market.

Regulatory Fragmentation Impedes Standardization and Interstate Commerce

The United States alone counts more than 20,000 authorities having jurisdiction over building codes, saddling manufacturers with duplicative certification pathways. Professional licensure reciprocity gaps force architects and structural engineers to maintain multi-state credentials, inflating soft costs and diluting economies of scale. Early adopters of ICC/MBI standards reduce administrative drag, yet voluntary uptake yields an uneven operating map that disadvantages smaller plants seeking cross-border expansion. Larger enterprises absorb the overhead, consolidating share and widening the competitive moat across the North America prefabricated buildings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Timber Innovation Drives Sustainable Construction

Concrete retained 35.42% of the North America prefabricated buildings market size in 2025 due to fire-rating and load-bearing benchmarks crucial for warehouses and data centers. Yet timber is charting a 7.41% CAGR to 2031 on the back of cross-laminated panels and glue-laminated beams that satisfy seismic codes in mid-rise applications. British Columbia, Quebec, and Oregon now sanction mass-timber towers above 12 stories, accelerating order pipelines for engineered-wood suppliers. Forward-looking developers cite 15% lighter foundations and 30% faster enclosure timelines as decisive advantages, driving incremental wins against concrete.

Timber’s ascendance also dovetails with embodied-carbon disclosure mandates in public-procurement tenders, giving low-carbon materials a scoring edge. University pilot projects such as Toronto’s Academic Wood Tower validate durability and acoustical performance at scale, shrinking insurer hesitation. Meanwhile metal demand remains steady for roof trusses and long-span girders that dominate e-commerce warehouses. Hybrid composite panels integrating glass curtain walls and steel cores address hurricane-zone resilience without compromising factory throughput, serving niche coastal installations within the North America prefabricated buildings market.

By Application: Commercial Acceleration Outpaces Residential Growth

Residential builds commanded 50.35% of the North America prefabricated buildings market size in 2025, fueled by financing support and housing-supply deficits. Manufactured homes provide cost-per-square-foot advantages of 35-40% compared with site-built options, anchoring baseline volume. Clayton Homes alone delivered 51,000 units in 2024 while certifying 95% of output to Zero Energy Ready thresholds.

Commercial projects, however, are advancing at a 7.12% CAGR through 2031 as standardized room modules gain favor in hospitality, health care, and education. Hospitals leverage infection-controlled production environments to minimise onsite disruption when adding ICU wings. Universities deploy dormitory blocks during summer breaks to absorb enrollment spikes. Data centers and logistics hubs adopt off-site MEP racks that slash commissioning hours, reflecting a sophistication level that redefines the opportunity mix for the North America prefabricated buildings market.

By Product Type: Panelized Systems Gain Market Share

Modular buildings held 38.28% North America prefabricated buildings market share in 2025, representing turnkey volumetric units craned into place. Panelized and componentized assemblies, though, are growing at 7.33% CAGR as architects and developers seek design flexibility without surrendering factory efficiency. Wall and floor panels arrive with pre-fitted insulation, vapor barriers, and conduit chases, reducing job-site waste and RFIs.

Digital-twin coordination between BIM files and CNC routers allows shop-floor teams to fabricate complex geometries that once required onsite carpentry. Electrical raceway cassettes by ABB exemplify how componentization unlocks 70% onsite time savings. Hybrid kits that fuse volumetric wet-rooms with flat-pack wall assemblies occupy a middle ground, proving attractive for multi-family podium projects intent on accelerating critical-path trades. The model diversification broadens the client base while feeding continuous pipeline visibility for stakeholders in the North America prefabricated buildings market.

Geography Analysis

The United States controlled 71.35% of the North America prefabricated buildings market in 2025, fortified by USD 600 million in HUD research partnerships that underwrite factory innovation and by Section 184 guarantees that lower origination fees for tribal borrowers. Virginia’s early adoption of ICC/MBI standards provides a replicable template that can shorten permitting timelines across other states, potentially removing up to 2% of project cost embedded in change-order administration. At the same time, 15-25% steel tariff escalations in 2025 steer developers toward localized supply chains that privilege domestic module production over imported kits, indirectly expanding utilization rates in U.S. plants.

Canada ranks second, leveraging a forest-product surplus and federal funding under the Rapid Housing Initiative to scale net-zero modular prototypes. The government’s CAD 600 million (USD 450 million) allocation for advanced housing technology extends competitive grants to consortiums that pair universities with manufacturers, reinforcing research-to-commercial pipelines. Mass timber approvals rising in British Columbia underpin forecasts for the timber segment, positioning Canada as a low-carbon materials export hub within the North America prefabricated buildings market.

Mexico, though presently smaller in absolute value, is the fastest-growing territory at 7.62% CAGR to 2031. Near-shoring inflows in automotive and electronics spark industrial-park construction that favors pre-engineered framing systems. Cavco Industries capitalizes on favorable wage differentials by operating assembly lines near Monterrey that backfill orders into U.S. Sun Belt states under USMCA provisions. Sovereign emphasis on renewable-energy manufacturing clusters stimulates worker-housing demand that modular plants can satisfy within 16-week cycles, de-risking delivery schedules amid volatile commodity pricing.

Competitive Landscape

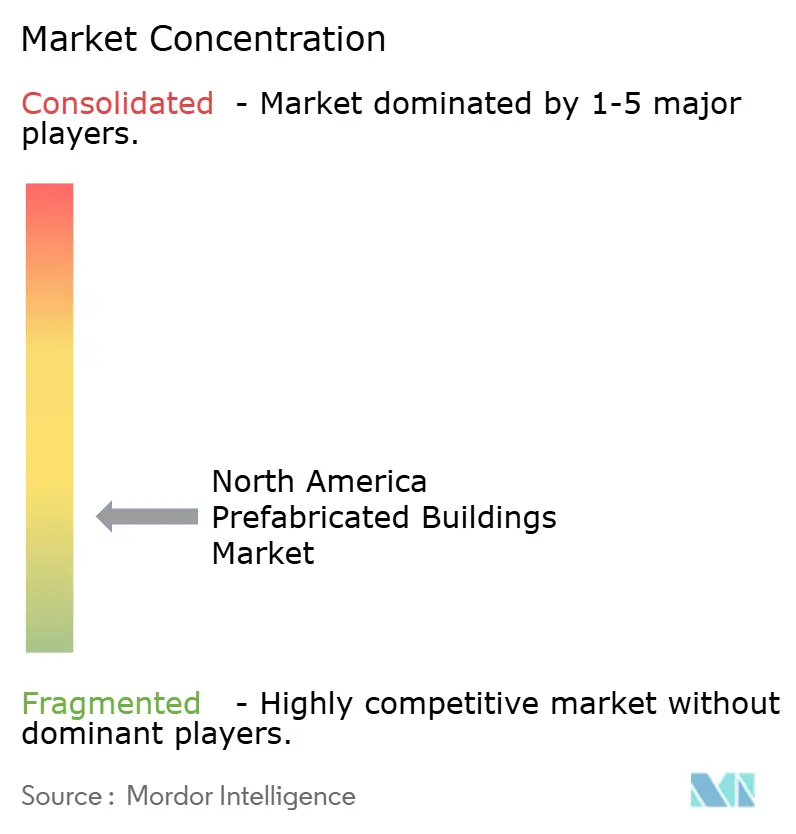

The North American prefabricated buildings market is moderately fragmented, with regional specialists fiercely contesting commercial niches. Backed by Berkshire Hathaway's robust balance sheet, Clayton Homes channels its USD 12.4 billion revenue into vertically integrated sectors like lumber, distribution, and retail lending. This strategy bolsters its defenses against rising commodity costs. Meanwhile, Cavco and Skyline Champion tap into their multistate plant networks, efficiently servicing orders within a 500-mile radius, and expanding their footprint in the retirement communities of the Sun Belt.

Between 2024 and 2025, the pace of consolidation quickened. ATCO Structures took over NRB Modular Solutions, boosting its capacity in Eastern Canada and streamlining the procurement of cold-formed steel frames. Vantem's acquisition of Arris Manufacturing is a strategic move, with ambitions to elevate its annual multifamily module production to 2,000 units by 2026. On the tech front, companies like Mighty Buildings are pioneering the use of 3-D-printed wall shells, significantly reducing labor hours, though they operate on a smaller scale. In a bid to stay ahead, established contractors are launching corporate-venturing arms, scouting for innovations in robotics and AI scheduling tools. These tools promise to harmonize factory operations with timely site deliveries. Collectively, these developments are amplifying the pace of innovation and intensifying competition in the North American prefabricated buildings arena.

North America Prefabricated Buildings Industry Leaders

Clayton Homes

Skyline Champion Corporation

Cavco Industries

BluHomes

Plant Prefab

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Boldt Group unveiled Bildt, a Wisconsin-based plant capable of shifting up to 90% of project labor off-site while targeting 30% cost reductions. The plant’s 90% off-site workflow showcases how healthcare and EV-charging clients can shave months off project schedules, reinforcing demand for high-precision panels that lift the overall North America prefabricated buildings market.

- January 2025: Vantem completed the acquisition of Arris Manufacturing, expanding capacity to 2,000 multifamily modules annually by 2026. Vantem completed acquisition of Arris Manufacturing to expand modular construction capabilities through its new Vantem Clio facility in South Carolina, targeting production of 700-800 multifamily units in the first year and up to 2,000 annually by 2026

- January 2025: ABB and Wieland Electric introduced prefabricated raceway systems that lower onsite electrical installation time 70%. ABB and Wieland Electric announced partnership to redefine modular construction efficiency through advanced prefabricated electrical installation systems, reducing on-site electrical installation time by up to 70% and costs by approximately 30%

- September 2024: ATCO Structures completed acquisition of NRB Modular Solutions, consolidating market position in the North American prefabricated buildings sector and expanding geographic coverage. Consolidation should boost purchasing leverage on raw materials, enabling price stability even as steel tariffs rise, thereby supporting steady margins for large-scale modular providers.

North America Prefabricated Buildings Market Report Scope

Prefabricated buildings (also known as prefabs) are building structures manufactured offsite and transported to the on-site assembly location. This report covers market insights, such as market dynamics, drivers, restraints, opportunities, technological innovations, their impact, Porter's five forces analysis, and the impact of geopolitics and pandemic on the market. The report also provides company profiles to understand the competitive landscape in the market.

The North American prefabricated buildings market is segmented by application (residential, commercial, and industrial) and geography (United States, Canada, and Mexico). The report offers the North America Prefabricated Buildings Market sizes and forecasts in terms of revenue (USD) for all the above segments.

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By Country

| US |

| Canada |

| Mexico |

| By Material Type | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By Country | US |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected value of the North America prefabricated buildings market by 2031?

The market is expected to reach USD 72.46 billion by 2031, growing at a 6.62% CAGR from 2026 to 2031.

Which material is growing fastest in prefabricated construction across North America?

Timber, especially mass-timber and cross-laminated products, is advancing at a 7.41% CAGR through 2031.

Why are panelized systems gaining share over traditional volumetric modules?

They ship within standard truck dimensions, cut logistics costs, and let developers retain design flexibility while capturing factory efficiency.

Which country shows the highest growth rate within North America?

Mexico is forecast to expand at a 7.62% CAGR as near-shoring boosts demand for industrial and worker-housing modules.

How do new energy codes affect prefabricated building adoption?

IECC-2024 and ASHRAE-90.1-2022 raise efficiency thresholds that factory-built envelopes meet more easily, giving prefabrication a regulatory advantage.

What logistical constraint most limits volumetric module adoption?

Over-dimensional transport fees and route-permit complexities can exceed 15% of project cost when shipping beyond 500 miles.

Page last updated on: