Market Overview

| Study Period | 2021 - 2031 |

|---|---|

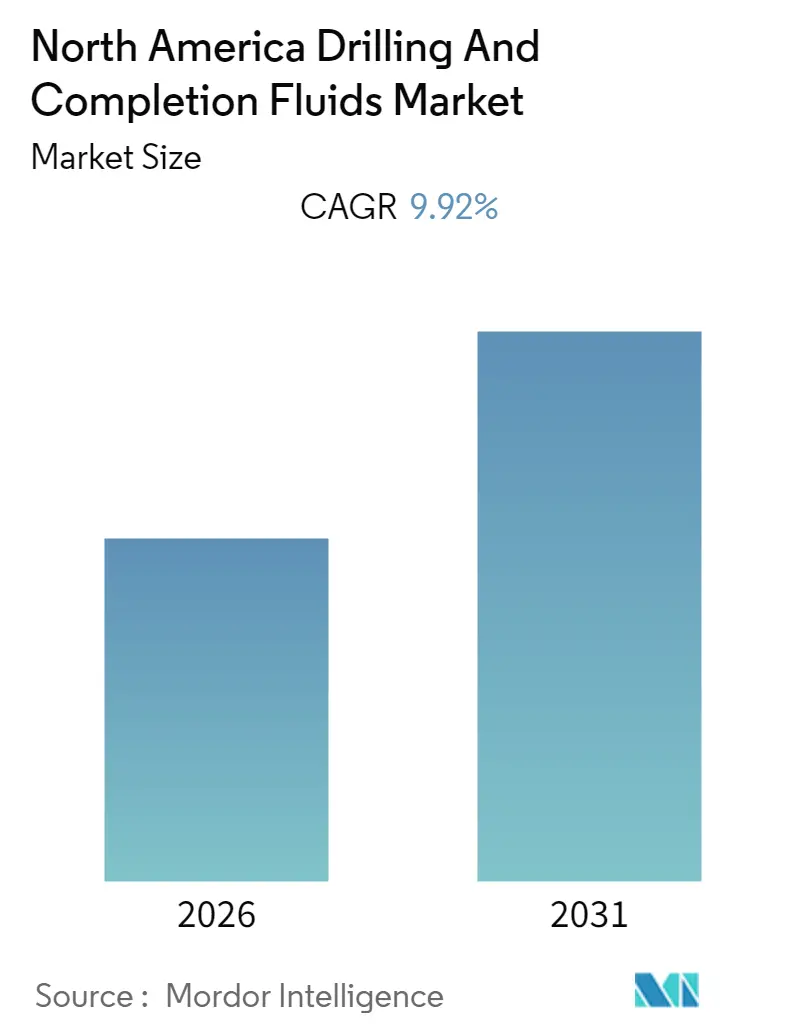

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Growth Rate | 9.92% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Drilling And Completion Fluids Market Analysis by Mordor Intelligence

The North America Drilling and Completion Fluids Market size is expected to register a CAGR of 9.92% during the forecast period (2026-2031).

- The onshore segment accounted for the largest share in the market in 2018, owing to the onshore oil & gas activities in the United States and Canada.

- A close proximity to extensive infrastructure coupled with promising results from the deployment of new technology puts Austin Basin in a comparatively stronger position and hence is expected to provide an ample opportunity for the drilling and completion fluids market in the near future.

- The United States is expected to dominate the market over the forecast period owing to its robust drilling activities in the unconventional plays.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Drilling And Completion Fluids Market Trends and Insights

Onshore Segment to Dominate the Market

- Onshore segment accounted for more than half of the market share in 2018 and is expected to continue its dominance in the coming years. As of December 2018, the average onshore active rig count from the United States and Canada totalled 1,202 units, representing an increase of 13.3% over the previous year's value.

- As of 2018, the United States is leading the onshore oil and gas activity, followed by Canada, with its robust drilling in the shale reserves, resulting in a surge in the North American oil and gas production. The major reason behind the surge is the declining operational cost in the country's basin, which has made marginal projects economical in the low oil price regime.

- As the upstream activities continue to increase in North America, the demand for oil field services is also increasing. This, in turn, is expected to help the services companies to progress in this market over the forecast period.

- The onshore activity in North America had picked up so much in 2017 that the oilfield services sector is struggling to keep up with the demand. Moreover, the onshore sector has benefited more from the rise in crude oil price, when compared to offshore in North America.

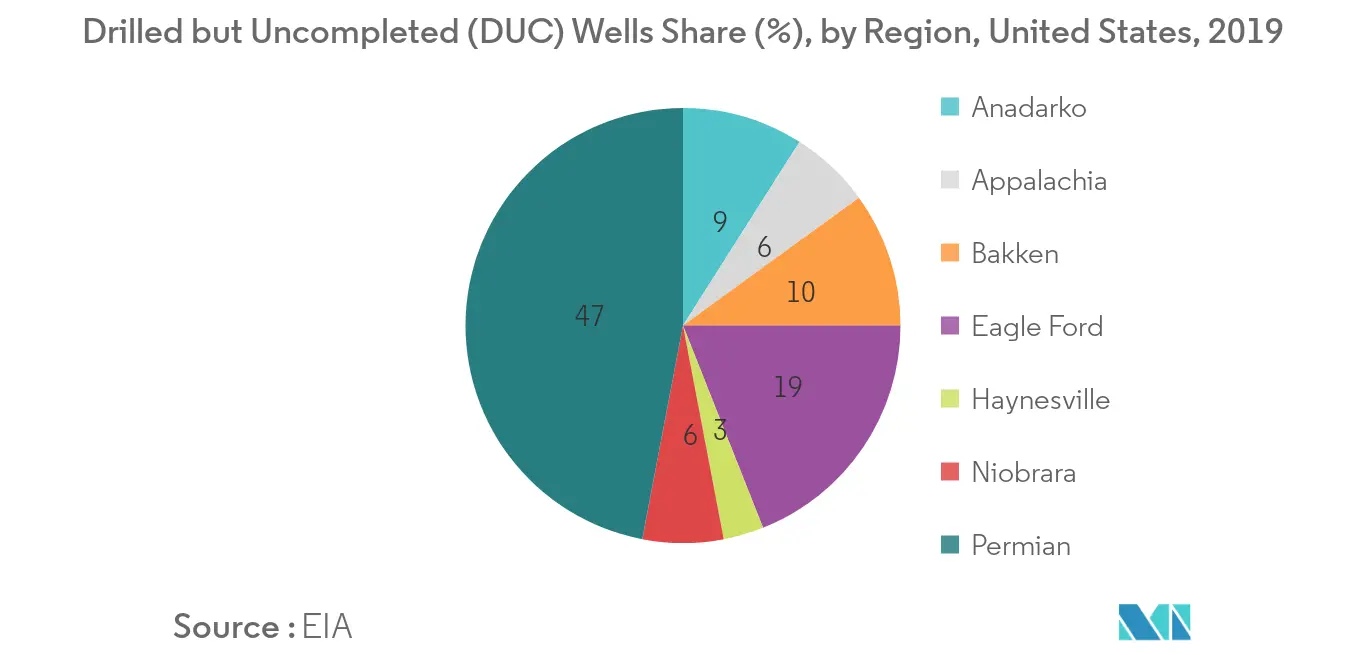

- Adding to this, there is a large number of uncompleted wells across the region. These wells are expected to be completed in the coming years, creating an ample opportunity for completion fluid providers.

The United States to Dominate the Market

- The United States is one of the largest drilling and completion fluids markets across the world, due to many wells being drilled every year. In the global rig count, the United States accounted for almost half of the onshore global average rig count for the period of January to September 2019.

- During the past decade (since 2008), the upstream oil and gas activity has shifted toward the shell reserves. During 2018, tight oil (which predominantly includes crude oil from shale reserves) and dry gas from shale reserves accounted for 59% and 69% respectively, of the total crude oil and dry natural gas production in the country.

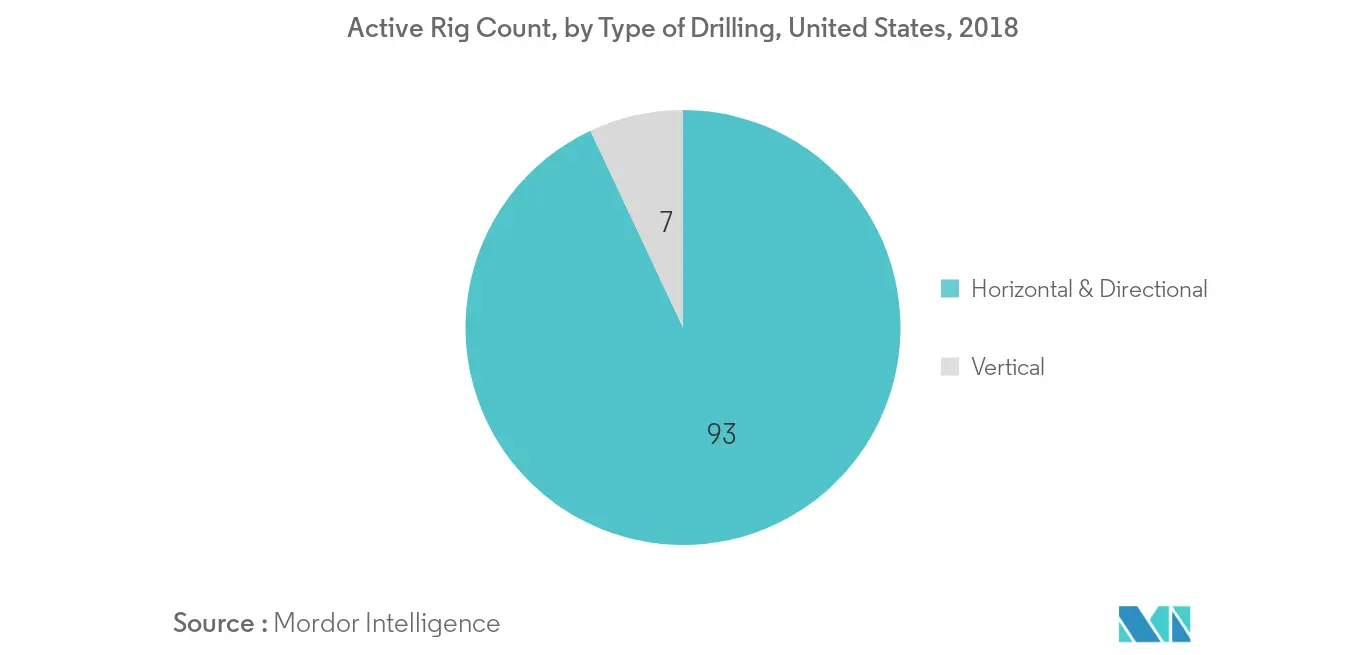

- Shale oil and gas production requires a much larger number of wells per acre than conventional oil fields, in turn, the requirement for a large number of wells per area and increasing share of the horizontal wells are expected to drive the demand for the completion and drilling fluid in the country.

- In 2004, horizontal wells accounted for about 15% and 14% of the country's crude oil production and natural gas production in the country. However, the share of horizontal wells in crude oil and natural gas production has increased to 96% and 97%, respectively, by the end of 2018. Hence, with increasing lateral length, the completion and drilling fluids market is being promulgated in the United States.

Competitive Landscape

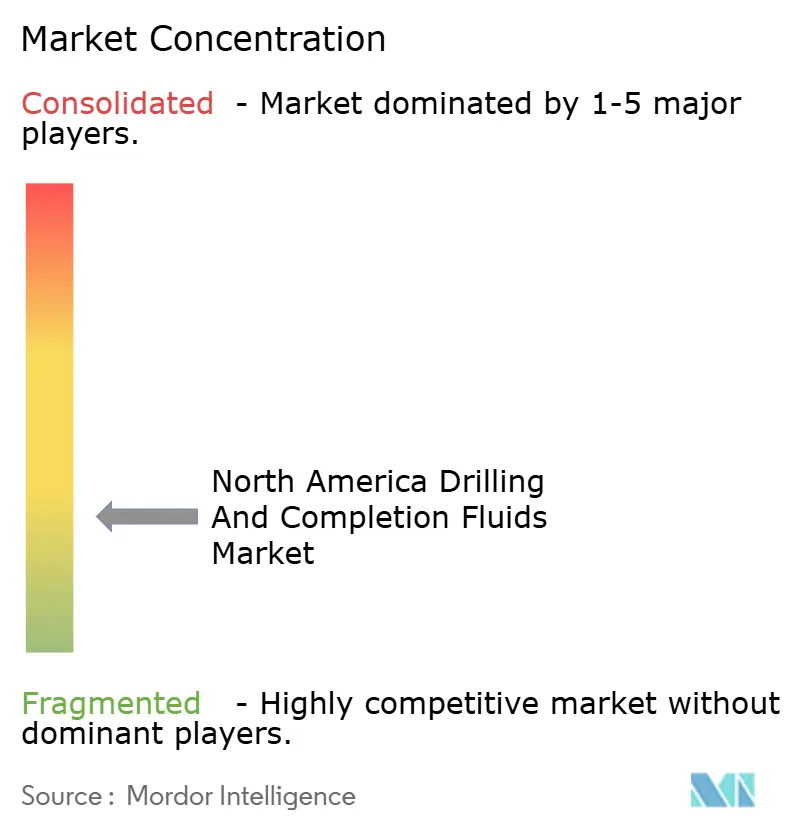

The North America drilling and completion fluids market is fragmented. Some of the key players are Schlumberger Limited, Baker Hughes Co., Halliburton Company, and National-Oilwell Varco Inc. and CES Energy Solutions Corp.

North America Drilling And Completion Fluids Industry Leaders

Schlumberger Limited

Baker Hughes - A GE Company

Halliburton Company

National-Oilwell Varco Inc.

CES Energy Solutions Corp

- *Disclaimer: Major Players sorted in no particular order

North America Drilling And Completion Fluids Market Report Scope

The North America drilling and completion fluids market report include:

Fluid Type

| Water-Based |

| Oil-Based |

| Others |

Location

| Onshore |

| Offshore |

Geography

| United States |

| Canada |

| Rest of North America |

| Fluid Type | Water-Based |

| Oil-Based | |

| Others | |

| Location | Onshore |

| Offshore | |

| Geography | United States |

| Canada | |

| Rest of North America |

Key Questions Answered in the Report

What is the current North America Drilling and Completion Fluids Market size?

The North America Drilling and Completion Fluids Market is projected to register a CAGR of 9.92% during the forecast period (2026-2031)

Who are the key players in North America Drilling and Completion Fluids Market?

Schlumberger Limited, Baker Hughes - A GE Company, Halliburton Company, National-Oilwell Varco Inc. and CES Energy Solutions Corp are the major companies operating in the North America Drilling and Completion Fluids Market.

What years does this North America Drilling and Completion Fluids Market cover?

The report covers the North America Drilling and Completion Fluids Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the North America Drilling and Completion Fluids Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: