North America Casino Gambling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

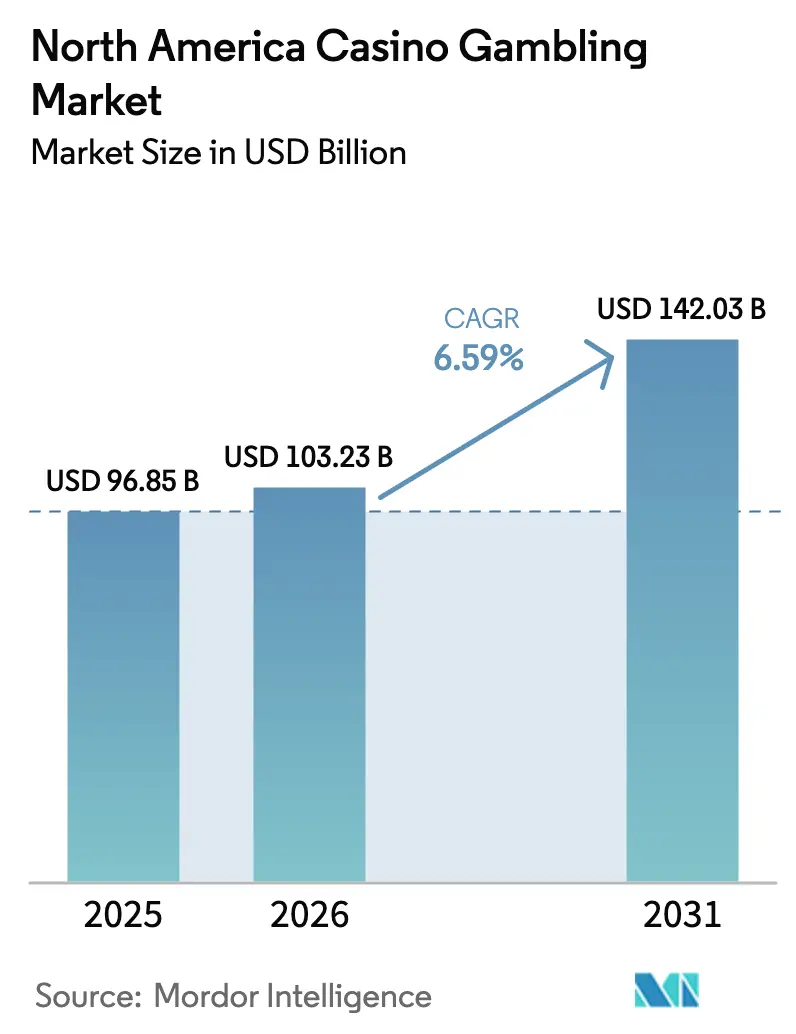

| Base Year Market Size (2025) | USD 96.85 Billion |

| Market Size (2026) | USD 103.23 Billion |

| Market Size (2031) | USD 142.03 Billion |

| Growth Rate (2026 - 2031) | 6.59% CAGR |

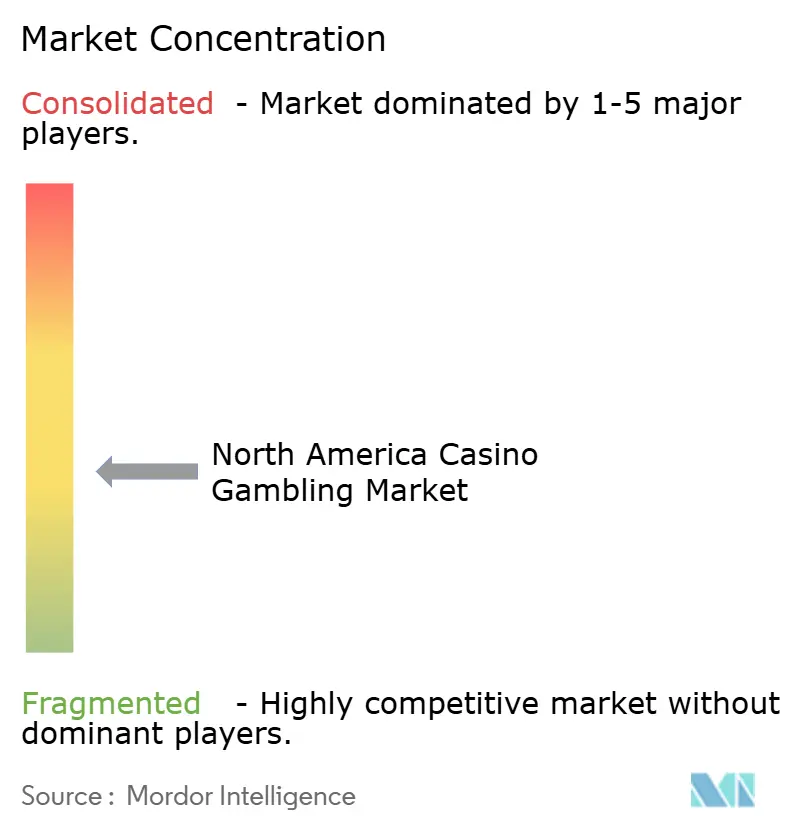

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Casino Gambling Market Analysis by Mordor Intelligence

The North America casino gambling market size was valued at USD 96.85 billion in 2025 and estimated to grow from USD 103.23 billion in 2026 to reach USD 142.03 billion by 2031, at a CAGR of 6.59% during the forecast period (2026-2031). Demand is supported by the steady legalization of sports betting, rising tourism volumes, and the rapid rollout of cash-free payment ecosystems that streamline gaming-floor transactions. Record tribal-gaming revenues, coupled with multibillion-dollar resort expansions, have insulated the North America casino gambling market from near-term macro headwinds. Operators are also deploying AI-based slot-yield optimisation and omnichannel loyalty programs that raise time-on-device and cross-property visitation. Leisure-travel metrics now exceed 2019 benchmarks in Las Vegas and Atlantic City, underscoring a durable consumer appetite for integrated entertainment experiences.

Key Report Takeaways

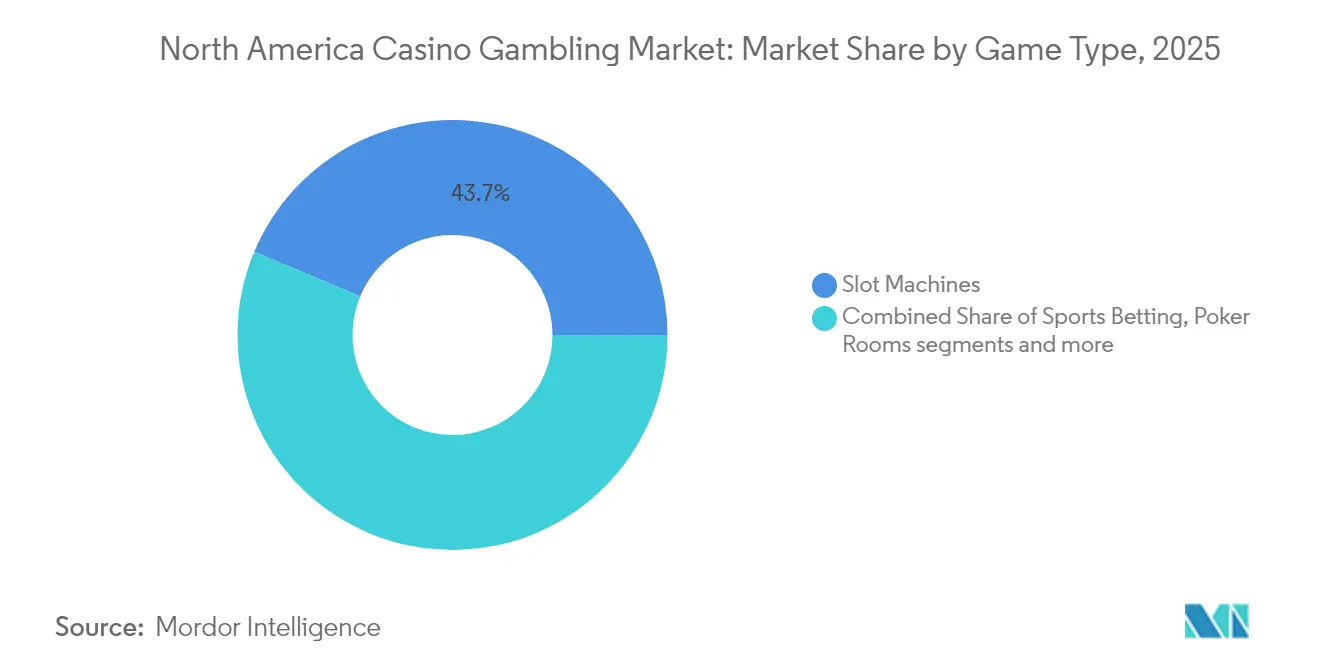

- By game type, slot machines secured 43.68% of the North America casino gambling market share in 2025, while sports betting is forecast to post the fastest 7.26% CAGR through 2031

- By platform, land-based venues commanded 61.02% of the North America casino gambling market in 2025; online casino operations are expanding at an 8.21% CAGR to 2031.

- By geography, the United States captured 77.65% revenue share of the North America casino gambling market in 2025, whereas Canada is projected to advance at a 7.63% CAGR, the fastest national growth rate to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple regions, with North america forming one of the important contributors. Mordor Intelligence's global casino gambling market size report represents that cumulative total.

North America Casino Gambling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continued legalization of sports betting | +1.2% | United States; spillover to Canada | Medium term (2-4 years) |

| Post-pandemic rebound in tourism & leisure spending | +0.8% | Las Vegas, Atlantic City | Short term (≤ 2 years) |

| Cashless payment & digital-wallet roll-out | +0.6% | Early-adopter U.S. states and Canadian provinces | Medium term (2-4 years) |

| Expansion of regulated online casino states | +1.1% | United States and Canada | Long term (≥ 4 years) |

| AI-driven slot-floor yield optimisation | +0.4% | Integrated resorts worldwide | Long term (≥ 4 years) |

| Tribal–commercial joint ventures in under-served regions | +0.3% | Rural U.S. markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Continued Legalization of Sports Betting

Thirty-eight U.S. states plus Washington D.C. now regulate sports wagering, generating USD 10.92 billion in operator revenue during 2023 [1]National Conference of State Legislatures, “Sports Betting Revenue by State,” ncsl.org . Tax rates span a wide spectrum from Nevada’s 6.75% to New York’s 51%, forcing operators to calibrate market-entry strategies against razor-thin margins in high-levy states. Mobile channels dominate penetration because app-based geolocation removes proximity barriers that once limited on-property sportsbooks. Ongoing federal proposals such as the SAFE Bet Act would impose national affordability checks, potentially harmonising consumer-protection rules across state lines. Cross-sell synergies between sportsbooks and casino floors lift customer-lifetime value, especially around major sporting events when handle spikes attract incremental visitation.

Post-Pandemic Rebound in Tourism & Leisure Spending

Las Vegas attracted 40.8 million visitors in 2023 and generated USD 51.5 billion in total out-of-wallet spend, surpassing pre-COVID highs [2]Hospitality Net, “Las Vegas Visitor Statistics 2024,” hospitalitynet.org . Convention traffic represents a high-value segment, as business travelers contribute substantial per-trip spending. This segment stabilizes weekday occupancy levels, effectively complementing the demand surges observed during weekend leisure periods. International arrivals have normalised, with Canadian and Mexican tourists comprising more than half of foreign visitation, though currency movements still influence win volumes. Operators are investing in entertainment residencies and headline sporting events such as Formula 1 to diversify demand drivers beyond core gaming. While economists warn of cyclical slow-downs, well-capitalised resorts are positioned to capture share from smaller competitors during any spending pullback.

Cashless Payment & Digital-Wallet Roll-Out on Gaming Floors

Integrated mobile wallets are now live across large U.S. casino networks through partnerships such as Everi’s CashClub Wallet and Crane Payment Innovations’ BetBridge technology. Digital-first transactions shorten queue times, heighten spend visibility, and reduce cage-cash handling costs that once suppressed operating margins. Tribal operators have exploited sovereign flexibility to pilot cryptocurrency acceptance, with Choctaw Casinos enabling on-device crypto liquidity that draws tech-savvy clientele. Regulators are drafting updated standards that marry know-your-customer procedures with frictionless onboarding to mitigate anti-money-laundering risks. Early usage data shows higher average daily theoretical win per guest when wagers originate from digital wallets rather than physical bills.

Expansion of Regulated Online Casino (iGaming) States

Ontario’s competitive iGaming framework has produced more than USD 7 billion in gross receipts since its April 2022 launch and delivered USD 1.4 billion in tax revenue to the province [3]Gaming News Canada, “Ontario iGaming Revenue Update,” gamingnewscanada.ca . Alberta’s iGaming Alberta Act was passed in 2025, setting the stage for second-mover market liberalisation when operations go live in 2026. Six U.S. states filed iGaming bills in January 2025, collectively covering close to 50 million residents and underscoring bipartisan appetite for digital revenue streams. Caesars Entertainment recently pooled WSOP Online liquidity across Pennsylvania, Nevada, New Jersey, and Michigan, proving that multi-state compacts can overcome early liquidity challenges. Early evidence from Ontario suggests digital casinos complement, rather than cannibalise, land-based visitation, alleviating political resistance in prospective states.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty & slow legislative cycles | -0.7% | Patchwork U.S. jurisdictions | Medium term (2-4 years) |

| Rising labour & energy costs at integrated resorts | -0.9% | High-wage U.S. markets | Short term (≤ 2 years) |

| Macroeconomic pressure on discretionary spending | -0.5% | Global | Short term (≤ 2 years) |

| Escalating cyber-insurance premiums | -0.3% | Large-scale operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainty & Slow Legislative Cycles

Quebec has opted to preserve Loto-Québec's monopoly, prioritizing centralized control over potential tax revenue gains that could arise from a competitive market structure. The protracted renegotiation of tribal-state compacts in certain reservations has delayed critical advancements, including slot-floor modernization and the rollout of sports betting operations. At the federal level, ongoing deliberations on the SAFE Bet Act have introduced a dual compliance framework, requiring operators to address both state-level licensing requirements and anticipated national regulations. These regulatory uncertainties have extended the time required for return on investment, thereby discouraging smaller regional companies from committing to significant capital expenditures. As a result, policy-related challenges continue to hinder growth opportunities and investment momentum within the affected markets.

Rising Labour & Energy Costs at Integrated Resorts

MGM Resorts granted a cumulative 32% wage hike to Culinary Workers Union members in 2024, pushing labour expense ratios to multi-year highs. Although revenue on the Las Vegas Strip grew by 6.8%, net income amounted to USD 820 million, reflecting margin compression driven by inflationary pressures [4]Casinos.com, “Las Vegas Strip Results 2024,” casinos.com . Tight labour markets elevate overtime pay, while mandated resort-fee transparency could cap upside on average daily rates. At the same time, electricity and natural-gas charges remain volatile as mega-resorts run 24-hour HVAC, lighting, and high-density server rooms for digital-gaming infrastructure. Operators are deploying renewable-energy power-purchase agreements and automation technologies, but payback periods extend beyond common REIT lease terms, complicating financing structures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Game Type: Sports Betting Drives Digital Transformation

Slot machines retained 43.68% of 2025 revenue, leveraging high-frequency spin mechanics that generate stable win yields and justify premium floor allocation. Their dependable cash flows anchor the North America casino gambling market size within large destination properties, allowing management to underwrite marquee entertainment attractions that pull incremental visitation. Sports betting, however, is projected to grow at a 7.26% CAGR, turning mobile apps into year-round acquisition funnels that feed higher-margin on-premise gaming during event weekends. Table games such as blackjack and roulette continue to deliver elevated theoretical hold per seat, yet their labour requirements and staffing shortages compress floor productivity in peak periods. Electronic table variants mitigate this constraint by utilising digital dealers and touch-screen interfaces, thereby slashing operating expense per open position.Live poker, once a flagship amenity, now cedes casual traffic to online rooms but remains indispensable for televised tournaments that elevate brand stature and non-gaming spend. Specialty games like keno and bingo appeal to older demographics that value social settings, ensuring steady contribution even as properties pivot toward younger, tech-oriented audiences. AI-driven slot analytics fine-tune pay-tables and theme rotations in real time, which lifts expected-value metrics across diverse patron cohorts without breaching regulatory hold ceilings. Branded content—illustrated by Aristocrat’s Dallas Cowboys licensing deal—refreshes player engagement cycles and extends dwell times, supporting incremental coin-in targets. Sportsbook integration raises cross-product wallet share by rewarding bettors with slot credits, deepening stickiness across multiple verticals and fortifying the North America casino gambling market against single-segment volatility.

By Platform/Channel: Online Casino Acceleration Challenges Land-Based Dominance

Land-based facilities amassed 61.02% of 2025 revenue, an outcome driven by integrated-resort ecosystems that bundle gaming, lodging, conventions, and live entertainment into a single, high-spend itinerary. Their extensive footprints support luxury hotel towers, Michelin-star restaurants, and headline residencies that transform properties into all-inclusive mini-cities—attributes that digital competitors cannot replicate. Loyalty programs such as Caesars Rewards and MGM Rewards stitch multiple properties together, granting comp redemption across rooms, shows, and dining to maximise share-of-wallet per trip. Tribal casinos bring regional diversity, often operating in rural corridors where they serve as primary job creators and cultural anchors. Card-room operations concentrated in California add further granularity by focusing almost exclusively on player-banked table games, allowing lower-overhead entries into municipal markets with strict slot bans.Online casinos are forecast to grow at an 8.21% CAGR as legislative tailwinds, improved geolocation, and seamless payment solutions shrink friction points that once hindered sign-ups. Operators like Fanatics introduce exclusive in-house titles and cross-vertical loyalty coins, thus extending brand stickiness beyond sports merchandise and sportsbook ecosystems. Mobile optimisation now emphasises low-latency streaming of live-dealer tables, replicating an on-floor experience that appeals to urban professionals who lack time for multi-day resort visits. Social-casino formats serve as inexpensive acquisition channels by monetising through micro-transactions that habit-train casual gamers for eventual real-money migration, thereby feeding the wider North America casino gambling market funnel.

Geography Analysis

The United States dominated with 77.65% of 2025 revenue, reflecting a mature regulatory landscape that spans 44 casino-permissive states plus Puerto Rico. Revenue distribution is heterogeneous: the West leads tribal-gaming inflows, the Northeast concentrates high-yield commercial venues, the South represents the fastest-legalising cluster, and the Midwest maintains middle-aged properties that still post respectable occupancy metrics. Las Vegas Strip properties pulled USD 31.5 billion in aggregate revenue during 2024, yet surging wage and utility costs dragged net income down to USD 820 million, underscoring the delicate balance between headline growth and margin retention. Upcoming sportsbook rollouts in Missouri and several iGaming bills under consideration across Maryland, Virginia, and Indiana indicate fresh demand pipelines that extend beyond traditional coastal centres.

Canada represents the most exciting growth frontier, with a projected 7.63% CAGR through 2031 that could see its share of the North America casino gambling market size widen materially. Ontario’s open-licence iGaming ecosystem already hosts more than 70 approved operators, creating robust tax flows alongside a thriving supplier base of studios and fintech providers. Alberta is set to follow in 2026, and lobbying groups in British Columbia and Manitoba advocate for competitive models that mirror Ontario’s success. Yet policy fragmentation persists: Quebec has doubled down on a single-operator monopoly, citing problem-gaming risk in its refusal to open the market. Cross-border travel remains a key driver of on-property spend, as favourable exchange rates for Canadian visitors enhance average win per trip in U.S. destinations.Mexico adds optionality to the long-range outlook. A 2024 tribunal ruling voided a longstanding federal slot ban, opening a legal pathway for Vegas-style casino floors pending secondary regulation. Grupo Caliente extended its Playtech supply pact in anticipation of expanded game portfolios, signalling operator optimism despite continued legislative unpredictability. Industry advocates aim to harmonise state-issued permits with federal oversight to curtail grey-market proliferation that currently siphons taxable income. U.S.-based chains track these developments closely, as brand recognition among cross-border tourists could accelerate site ramp-up once clarity emerges. Therefore, Mexico’s contribution to the wider North America casino gambling market may accelerate in the latter half of the forecast window, adding another diversification vector for multinational operators.

Coverage of the casino gambling market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Asia and Europe.

Competitive Landscape

The North America casino gambling market shows moderate concentration; the five largest operators accounted for almost half of 2024 revenue, leaving significant share for regional specialists and digital-first entrants. Bally’s agreed to merge with Standard General for USD 4.6 billion, expanding its footprint to 19 facilities across 11 states and unlocking operational synergies in marketing spend and technology platforms. IGT’s USD 6.2 billion combination with Everi unites game-content portfolios with fintech payment systems, positioning the merged firm to supply turnkey omnichannel solutions. MGM Resorts and Playtech launched proprietary live-dealer studios in Las Vegas, exporting the Strip brand into regulated European markets and enhancing non-U.S. revenue streams. Caesars’ multi-state WSOP Online pool cements a first-mover advantage in regulated poker liquidity, amplifying network effects that smaller rivals struggle to replicate.

Tribal operators wield unique flexibility through sovereign status, allowing quicker adoption of crypto payments, esports wagering, and skill-based gaming prototypes. Choctaw’s crypto-liquidity pilot exemplifies how such sovereignty can leapfrog regulatory bottlenecks and attract younger, tech-native demographics. Diversification is advancing as tribes pursue federal contracting; USD 1.2 billion in subcontract awards during 2024 offset gaming-cycle volatility and funded new resort amenities that keep properties competitive. Meanwhile, sports media and e-commerce brands such as Fanatics leverage vast customer datasets to disrupt traditional player-acquisition funnels, subsidising promotions with cross-vertical profit pools.

White-space opportunities persist in rural corridors where casinos can double as regional convention centres and entertainment hubs, catalysing job creation and local tax receipts. Technology adoption has become the gating factor for sustainable share capture; AI-powered player analytics, integrated cashless wallets, and seamless omnichannel loyalty schemes are now baseline requirements rather than optional innovations. Operators that delay digital transformation risk falling below the experiential standards set by tech-forward rivals, potentially ceding slices of the North America casino gambling market to agile newcomers.

North America Casino Gambling Industry Leaders

MGM Resorts International

Caesars Entertainment Inc.

Las Vegas Sands Corp.

Wynn Resorts Ltd.

Penn Entertainment Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Caesars Entertainment completed a USD 160 million redesign of Harveys Lake Tahoe, reopening as Caesars Republic Lake Tahoe with upgraded casino floors and a Gordon Ramsay HELL’S KITCHEN restaurant.

- April 2025: Caesars Entertainment expanded WSOP Online to pool liquidity across four jurisdictions, achieving the first multi-state poker network in the United States.

- May 2025: Fanatics Casino launched across Michigan, New Jersey, Pennsylvania, and West Virginia with exclusive games and a USD 2 million FanCash promotion.

- November 2024: Turning Stone Resort Casino unveiled a USD 370 million expansion featuring a new conference centre, hotel tower, and outdoor venues that will generate USD 616 million in economic impact.

North America Casino Gambling Market Report Scope

A casino is a facility for certain types of gambling. Casinos are often built near or combined with hotels, resorts, restaurants, retail shops, cruise ships, and other tourist attractions. This report aims to provide a detailed analysis of the North American casino gambling market. It focuses on the market dynamics, emerging trends in the segments and regional markets, and insights into the various product and application types. Also, it analyzes the key players and the competitive landscape.

The North American casino gambling market is segmented by type (live casino, baccarat, blackjack, poker, slots, and other casino games) and by geography (USA, Canada, and the rest of North America).

The report offers market size and values in USD during the forecast period for the above segments.

| Slot Machines | |

| Table Games | Blackjack |

| Roulette | |

| Baccarat | |

| Craps | |

| Sports Betting | |

| Poker Rooms | |

| Electronic Gaming Tables | |

| Other Specialty Games (Keno, Bingo) |

| Land-based Casino Gaming | Commercial Casinos |

| Tribal Casinos | |

| Card Rooms | |

| Online Casino (Social, Mobile etc) |

| United States | Northeast |

| Midwest | |

| South | |

| West | |

| Canada | Ontario |

| British Columbia | |

| Alberta | |

| Quebec | |

| Rest of Canada | |

| Mexico | Baja California |

| Mexico City & State of Mexico | |

| Nuevo León (Monterrey) | |

| Rest of Mexico |

| By Game Type | Slot Machines | |

| Table Games | Blackjack | |

| Roulette | ||

| Baccarat | ||

| Craps | ||

| Sports Betting | ||

| Poker Rooms | ||

| Electronic Gaming Tables | ||

| Other Specialty Games (Keno, Bingo) | ||

| By Platform / Channel | Land-based Casino Gaming | Commercial Casinos |

| Tribal Casinos | ||

| Card Rooms | ||

| Online Casino (Social, Mobile etc) | ||

| By Geography | United States | Northeast |

| Midwest | ||

| South | ||

| West | ||

| Canada | Ontario | |

| British Columbia | ||

| Alberta | ||

| Quebec | ||

| Rest of Canada | ||

| Mexico | Baja California | |

| Mexico City & State of Mexico | ||

| Nuevo León (Monterrey) | ||

| Rest of Mexico | ||

Key Questions Answered in the Report

What is the projected growth rate for the North American casino gambling market?

The market is forecast to grow at a 6.59% CAGR, rising from USD 103.23 billion in 2026 to USD 142.03 billion by 2031.

Which segment contributes the largest share of revenue?

Slot machines contributed 43.68% of 2025 revenue, making them the largest segment in the North America casino gambling market.

How fast is sports betting expanding in North America?

Sports betting is expected to register a 7.26% CAGR to 2031, the highest among all game types.

Why is Canada considered the fastest-growing country?

Provincial iGaming liberalisation, spearheaded by Ontario and soon Alberta, positions Canada for a 7.63% CAGR through 2031.

What technologies are reshaping player experience?

Cashless digital wallets, AI-driven slot analytics, and omnichannel loyalty programs are redefining engagement and operational efficiency across both land-based and online platforms.

How concentrated is the competitive landscape?

The five largest operators hold approximately half of industry revenue, indicating a moderately concentrated market that still offers expansion potential for mid-tier players.

Page last updated on: