Nickel-Cadmium Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

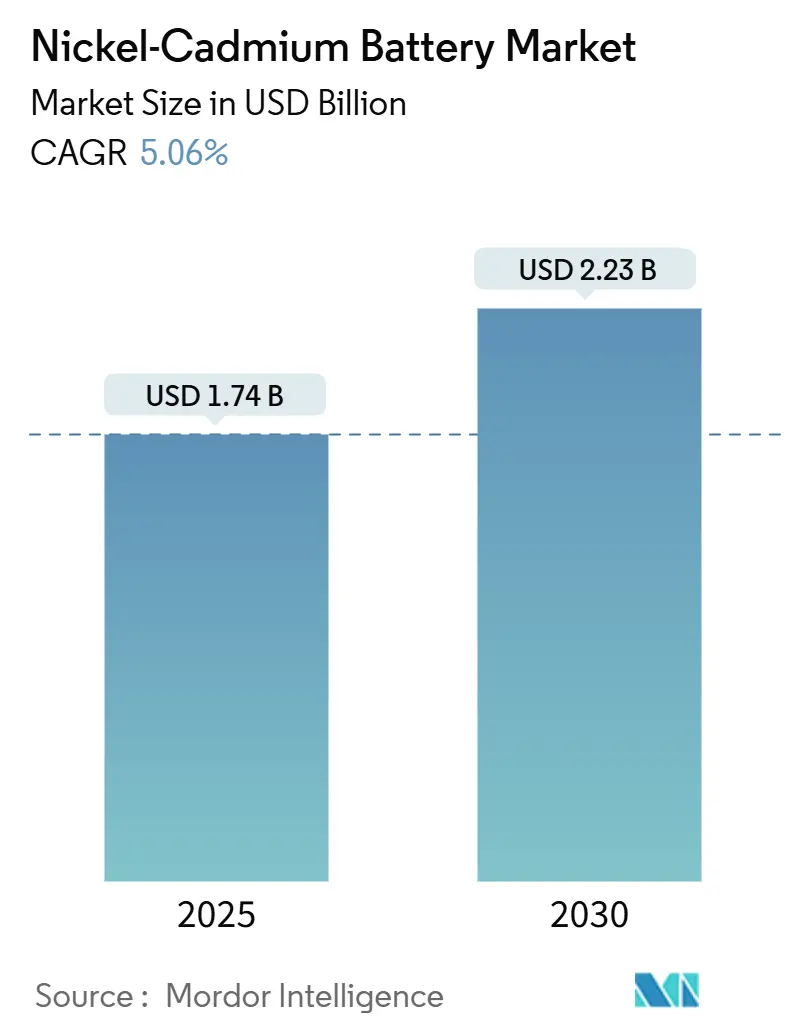

| Market Size (2025) | USD 1.74 Billion |

| Market Size (2030) | USD 2.23 Billion |

| Growth Rate (2025 - 2030) | 5.06% CAGR |

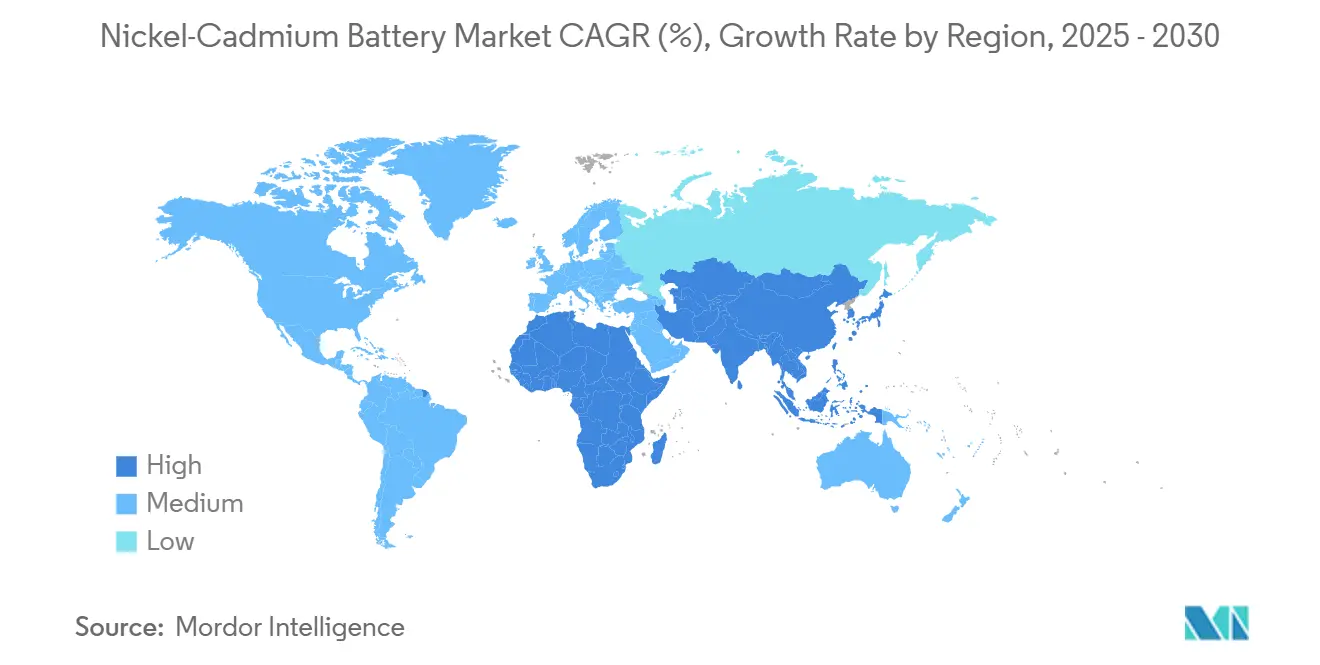

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

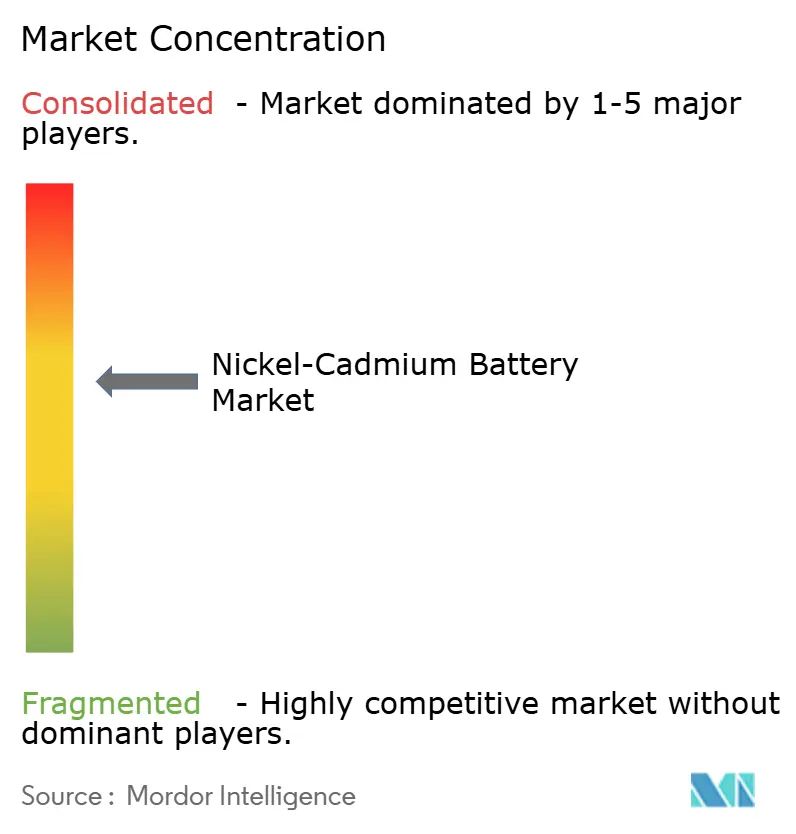

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nickel-Cadmium Battery Market Analysis by Mordor Intelligence

The Nickel-Cadmium Battery Market size is estimated at USD 1.74 billion in 2025, and is expected to reach USD 2.23 billion by 2030, at a CAGR of 5.06% during the forecast period (2025-2030).

Robust demand from industrial standby power, aviation starters, and defense electronics sustains growth even as environmental regulations tighten. Reliability in harsh operating conditions, proven 20-year service lives, and immunity to deep discharge continue to outweigh cost concerns for mission-critical users. Recycling mandates now redefine competitive dynamics, as producers with established take-back networks face a lower compliance risk. At the same time, lithium-ion price erosion limits addressable volumes in consumer products but has yet to displace nickel-cadmium in extreme-temperature or safety-certified systems.

Key Report Takeaways

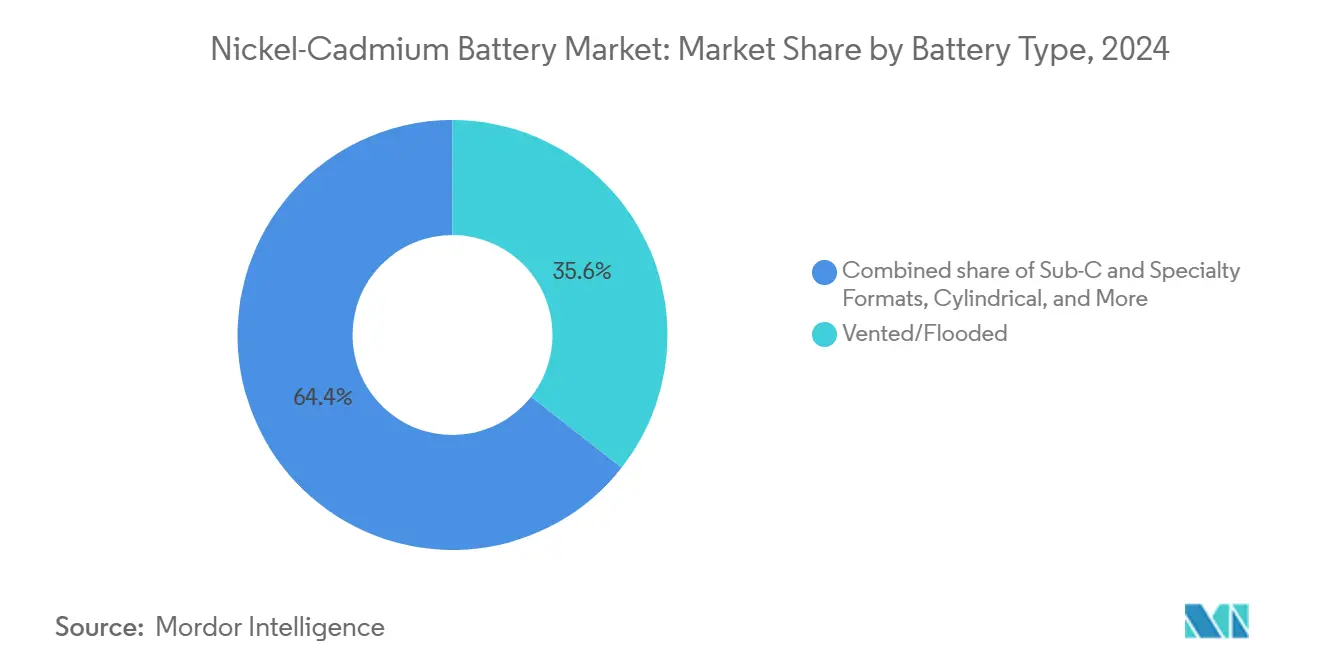

- By battery type, vented/flooded configurations led the nickel-cadmium battery market with 35.6% of the market share in 2024. Sub-C and other specialty formats are projected to grow at the fastest 5.9% CAGR between 2025 and 2030.

- By capacity, the above-10 Ah class accounted for a 47.5% share of the nickel-cadmium battery market size in 2024.

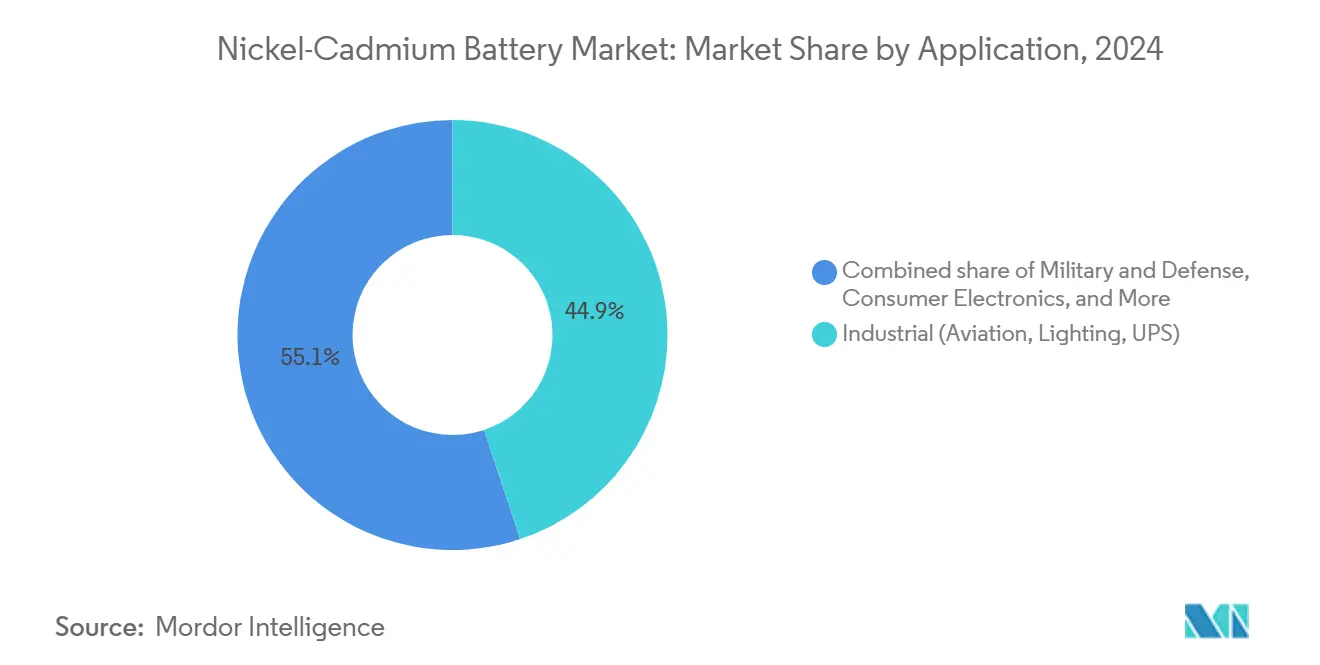

- By application, military and defense devices are expected to expand at a 6.1% CAGR to 2030, while industrial installations retained a 44.9% share in 2024.

- By geography, Asia-Pacific dominated with a 40.2% revenue share in 2024 and is anticipated to advance at a 5.8% CAGR through 2030.

Global Nickel-Cadmium Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial demand for mission-critical backup power | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Superior low-temperature performance | +0.8% | APAC core, spill-over to Nordic regions | Long term (≥ 4 years) |

| Mandatory use in safety-critical certified systems | +0.9% | Global, strongest in North America & Europe | Long term (≥ 4 years) |

| Retrofit of off-grid telecom towers in Sub-Saharan Africa | +0.6% | Sub-Saharan Africa, with expansion to rural Asia | Medium term (2-4 years) |

| Hydrogen-aviation starter batteries niche | +0.3% | North America & Europe | Long term (≥ 4 years) |

| EU closed-loop recycling economics | +0.4% | European Union | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industrial Demand for Mission-Critical Backup Power

Large processing plants, offshore rigs, and metro rail networks place uptime above initial cost, driving steady purchases of nickel-cadmium strings for uninterruptible power equipment. Field data from EverExceed units show service lives exceeding 20 years with only routine topping-up, thereby lowering lifecycle expenses compared to sealed lead-acid varieties. Resistance to electrical abuse allows safe high-rate discharges needed for turbine cranking and emergency lighting. Global IEC and CE certification frameworks reinforce procurement decisions, as compliance documentation facilitates insurance audits. New refinery projects in the Middle East and pipeline expansions in North America incorporate battery rooms that utilize nickel-cadmium batteries to prevent thermal runaway. As brownfield industrial sites modernize switchgear, retrofit orders sustain baseline demand.

Superior Low-Temperature Performance

Nickel-cadmium chemistry retains nearly full capacity at −20 °C, whereas lithium-ion loses 30-40% under identical loads, according to controlled chamber tests published by EverExceed. Arctic telecommunications shelters and high-altitude radar outposts exploit this attribute to minimize oversizing. Cold-weather performance also supports rail signaling across the Nordic network, where batteries remain exposed on trackside cabinets. Utility crews report fewer replacement cycles during polar winters, which helps trim maintenance budgets. The performance edge underpins emerging polar-route commercial aviation, where auxiliary power batteries must meet both low-temperature and rapid-charging requirements. Long-term infrastructure investments in Canada and northern Russia thus reinforce organic volume growth for the nickel-cadmium battery market.

Mandatory Use in Safety-Critical Certified Systems

Federal Aviation Administration rule 14 CFR 25.1353 and related civil-aircraft test protocols continue to list nickel-cadmium as an accepted baseline technology for main- and auxiliary-power batteries.[1]Federal Aviation Administration, “14 CFR Part 25.1353 Electrical Equipment,” faa.gov Certification pathways for alternative chemistries require multi-year flight validation, giving existing suppliers a durable installed-base advantage. Military handheld radios, sonar buoys, and arming devices also rely on rugged nickel-cadmium packs that are cleared under MIL-STD-810. Failure tolerance thresholds below 1 in 10 million events incentivize retaining a chemistry with decades of logged reliability. Naval contracts typically mandate the use of off-the-shelf parts with traceable production lots, further shielding the nickel-cadmium battery market from rapid substitution.

Retrofit of Off-Grid Telecom Towers in Sub-Saharan Africa

Mobile operators are investing in hybrid energy solutions to reduce their reliance on diesel. MTN allocated USD 101.3 million in 2024 to batteries, gensets, and solar arrays across South Africa’s load-shedding zones. Rural towers often face ambient temperatures above 45 °C and sporadic maintenance visits, which favor nickel-cadmium cells that can tolerate high heat and deep discharge without advanced management electronics. Grants from the World Bank’s Digital Infrastructure Program extend similar tower retrofits to Kenya and Nigeria. As smartphone usage increases, network uptime metrics are directly tied to service revenues, locking in demand for reliable storage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening cadmium regulations & disposal costs | -1.1% | Global, strongest in Europe & North America | Short term (≤ 2 years) |

| Competition from Li-ion & NiMH price drops | -0.9% | Global, with concentration in consumer segments | Medium term (2-4 years) |

| Nickel hydroxide cake export quotas (Indonesia) | -0.7% | Global, with strongest impact on Asia-Pacific | Medium term (2-4 years) |

| Subsidy schemes favour Li-ion for grid storage | -0.5% | North America & Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Cadmium Regulations and Disposal Costs

Regulation 2023/1542 obliges producers selling into the EU to finance collection points, apply cadmium hazard labels, and file audited supply-chain reports, all of which raise operating costs.[2]European Parliament and Council, “Regulation (EU) 2023/1542 on Batteries,” europa.eu U.S. states such as California and Washington pursue parallel extended producer laws that add return logistics overhead. Small assemblers without captive recycling partners face double-digit percentage cost inflation, prompting them to exit marginal product lines. Consumer-grade cordless phones, toys, and shavers disappear fastest because retail buyers switch to cadmium-free batteries to pre-empt disposal fees. Industrial fleet owners cannot avoid compliance either, but their larger budgets enable amortization across long-life assets, reducing the overall impact on the nickel-cadmium battery market to manageable levels.

Competition from Lithium-Ion and NiMH Price Drops

Benchmark spot quotations for lithium-ion prismatic packs declined another 18% year-over-year in 2024, owing to smelter expansions in Qinghai and CATL yield gains. Nickel-metal hydride enjoys a stable supply of rare earths and avoids toxic-metal labeling, attracting tool and toy makers. Huizhou Shenzhou Super Power, a contract manufacturer for cordless phone batteries, shifted 60% of its 2023 output to NiMH formats, thereby slashing nickel-cadmium demand in that segment. Industrial customers that accept modest temperature limits also experiment with low-cobalt lithium-ion to achieve weight savings. Consequently, price-sensitive orders migrate away from nickel-cadmium, compressing overall sales even as premium niches expand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Vented Systems Sustain Industrial Dominance

Vented or flooded blocks captured 35.6% of the nickel-cadmium battery market share in 2024, driven by transformer-substation backup and offshore drilling starter applications. Their open construction permits gas recombination and rapid electrolyte inspection, yielding service lives over 20 years. The nickel-cadmium battery market size associated with Sub-C and other specialty formats is projected to grow at a 5.9% CAGR by 2030, driven by the need for compact cells in aviation start-stop units and handheld medical tools that require validation under aerospace norms. Sealed, maintenance-free styles are often preferred in rail lighting where ventilation is limited, whereas prismatic blocks remain common in telecom huts. Cylindrical variants continue their gradual retreat in household gadgets as retail chains delist cadmium-bearing products.

Product managers for vented strings now bundle electrolyte-monitoring IoT sensors that feed predictive-maintenance dashboards, locking in service contracts. Specialty-format suppliers collaborate with airframe OEMs to co-design form factors for hydrogen auxiliary-power units. Meanwhile, regulatory audits prompt sealed-cell makers to publish gas-generation rates to satisfy workplace safety officers. Across categories, differentiation shifts from pure electrochemistry to packaging, certification, and digital diagnostics, which carry higher margins than commodity cells.

By Capacity Range: High-Ah Blocks Anchor Revenue

The above-10 Ah band generated 47.5% of the nickel-cadmium battery market size in 2024 and is projected to grow at a 5.5% CAGR to 2030, as large UPS rooms and crane-starter banks require robust discharge currents. These large blocks also reduce rack count, thereby cutting cabling losses for petrochemical plants that operate in 50 °C ambient temperatures. Intermediate 3–10 Ah packs retain a steady share in portable calibration tools and hospital infusion pumps. Below-3 Ah cells sit under pricing pressure from pouch-cell lithium-ion, especially in electronic toys. Upsizing trends within industrial design portfolios, such as consolidating three 100 Ah strings into one 300 Ah string, further tilt revenue toward the upper capacity tier.

Manufacturing lines for high-Ah cells are increasingly integrating robotic welding to meet the traceability requirements set by aerospace buyers. Some producers trial foam-nickel electrodes to squeeze extra energy density without sacrificing safety. The market segment also witnesses a flurry of service-retrofit contracts, where aging 1980s-era lead-acid racks are swapped for high-Ah nickel-cadmium blocks to extend runtime while maintaining legacy charger cabinets.

By Application: Defense Outpaces but Industrial Core Holds Ground

Defense electronics, unmanned systems, and ordnance support equipment will post a 6.1% CAGR through 2030 as modernization budgets climb in the United States, India, and Japan. Procurement documents continue to cite nickel-cadmium for hot-and-cold temperature survivability, electromagnetic-pulse resistance, and logistics familiarity. Industrial plants, airports, and data centers stayed the largest slice at 44.9% in 2024, ordering multi-ton battery rooms for switchgear and runway lighting. Consumer electronics slide further because retailers prefer cadmium-free labels to avoid eco-fees. Medical instruments remain a steady, albeit small, niche market thanks to regulatory inertia surrounding established power packs in infusion pumps. Power tools remain a vital component in professional construction, where cold-weather drilling requires high surge current without voltage sag.

The defense lead accelerates as armed forces deploy autonomous surface vessels and high-mobility radar trailers that emphasize immediate start capability after months in storage. Industrial owners, meanwhile, redesign safety-critical circuits to exploit nickel-cadmium’s flat discharge curve, letting engineers specify a smaller capacity for the same minimum voltage floor. Across both segments, life-cycle economics rather than upfront price defines buyer decisions, preserving margins for certified suppliers.

Geography Analysis

Asia-Pacific generated 40.2% of 2024 revenue for the nickel-cadmium battery market, with Indonesia alone refining roughly half of the world’s mined nickel after the government’s 2024 export ban redirected ore to domestic smelters.[3] Center for Strategic and International Studies, “Indonesia’s Nickel Industrial Policy,” csis.org Chinese conglomerates have committed more than USD 30 billion to high-pressure acid-leach plants, lowering metal costs for regional cell makers. The nickel-cadmium battery market size for the region is projected to rise at a 5.8% CAGR through 2030 as rail build-outs in India and off-grid telecom towers in Indonesia demand high-temperature-tolerant storage. Yet environmental NGOs continue to scrutinize coal-fired smelters, raising the prospect of carbon-border taxes on exports to Europe.

Europe faces the strictest compliance regime after Regulation 2023/1542 took effect in August 2025, mandating 80% recycling efficiency and full producer responsibility.[4]European Parliament and Council, “Regulation (EU) 2023/1542 on Batteries,” europa.eu Nordic utilities continue to specify nickel-cadmium for sub-zero grid assets, supporting moderate demand even as Southern European telecoms transition to lithium-ion. Germany’s Fraunhofer IKTS pilots alkaline-electrolyte recycling techniques that recover cadmium hydroxide at 92% yield, offering a future cost offset. Eastern European rolling-stock refurbishments also help maintain volumes, because rail-safety standards in that region continue to mirror legacy Western norms.

North America leverages defense budgets and industrial upgrades. The U.S. Navy issued Small Business Innovation Research (SBIR) grants in May 2025 to investigate sodium-ion chemistries; however, near-term platforms will still procure nickel-cadmium batteries, given the certification timeline. FAA rules keep the chemistry entrenched in commercial aircraft, and refinery outages after the 2024 hurricane season spurred new backup-power installs along the Gulf Coast. Canada’s telecom providers deploy vented strings in Arctic microwave-relay huts where −40 °C winter nights challenge lithium-ion pre-heaters. Latin America and the Middle East & Africa contribute smaller volumes; however, tower-build programs financed by the World Bank in Kenya and Nigeria accelerate the adoption of high-Ah vented blocks.

Competitive Landscape

Industry concentration remains moderate. The five largest producers together hold an estimated 55–60% revenue share, a level that supports both price discipline and healthy niche competition. Certification catalogs, particularly EN 62133 and FAA technical standard orders, create high entry barriers. Long-run cell contracts often pair with 15-year service agreements. Established players bundle recycling credits to blunt the cost impact of Regulation 2023/1542, locking in European utilities. Smaller Asian assemblers are pivoting to private-label units for telecom operators, attracted by agile procurement cycles and a lower compliance burden.

Technology differentiation is shifting toward electrode sintering quality, electrolyte purity, and real-time diagnostics, rather than basic chemistry. One leading supplier released a cloud-linked electrolyte-level sensor that cuts manual inspections by 80% and reports directly to SCADA dashboards. Another invested in ISO 14001-certified closed-loop cadmium recovery, marketing a carbon-neutral battery to data-center clients. Joint development programs with airframe prime contractors secure sole-source status for starter batteries on next-generation turboprops. Despite rising lithium-ion volumes, nickel-cadmium maintains a safe-harbor reputation among risk-averse engineers.

Cost pressures, however, spur incremental consolidation. A mid-tier European vendor exited the sub-C hobbyist segment in 2024 and sold tooling to an Indonesian consortium. Chinese cell makers capitalize on local nickel supply to undercut Western pricing by 8–10%; yet, longer shipping times, export-license constraints, and customer aversion to certifications performed outside EASA oversight keep Western incumbents competitive in aviation and defense.

Nickel-Cadmium Battery Industry Leaders

Saft (Total Energies)

Panasonic Energy

GS Yuasa Corporation

Alcad

EnerSys (Hawker)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The EU Battery Regulation 2023/1542's producer-responsibility clauses entered into force, obliging manufacturers to fund nationwide collection networks and material-recovery audits in all member states.

- December 2024: The journal Advanced Materials published a retrospective on early pacemaker batteries, noting the pioneering role of nickel-cadmium systems before lithium-iodine systems became the standard.

- September 2024: GODSON Technology released test data showing that nickel-cadmium cells retained 90% of their capacity after 500 cycles at −30 °C, bolstering performance claims for extreme-temperature projects.

- July 2024: Indonesia inaugurated its first domestic battery-cell plant, a partnership between LG Energy and Hyundai, which links local nickel ore to downstream manufacturing.

Global Nickel-Cadmium Battery Market Report Scope

| Cylindrical |

| Prismatic |

| Sub-C and Specialty Formats |

| Sealed (Maintenance-Free) |

| Vented/Flooded |

| Below 3 Ah |

| 3 to 10 Ah |

| Above 10 Ah |

| Consumer Electronics |

| Industrial (Aviation, Lighting, UPS) |

| Military and Defense |

| Medical Devices |

| Power Tools and Engineering Equipment |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Battery Type | Cylindrical | |

| Prismatic | ||

| Sub-C and Specialty Formats | ||

| Sealed (Maintenance-Free) | ||

| Vented/Flooded | ||

| By Capacity Range | Below 3 Ah | |

| 3 to 10 Ah | ||

| Above 10 Ah | ||

| By Application | Consumer Electronics | |

| Industrial (Aviation, Lighting, UPS) | ||

| Military and Defense | ||

| Medical Devices | ||

| Power Tools and Engineering Equipment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is global demand for nickel-cadmium batteries growing?

Global revenue is advancing at a 5.06% CAGR between 2025 and 2030 as industrial and defense buyers prioritize durability.

Which battery type leads shipments?

Vented or flooded designs hold the largest share at 35.6% because they support high-temperature industrial backup duties.

Why do defense programs still specify nickel-cadmium packs?

Proven reliability under extreme heat and cold, long certification histories and electromagnetic-pulse resilience keep the chemistry in military contracts.

What does EU Regulation 2023/1542 mean for producers?

From 2025 all suppliers must achieve 80% recycling efficiency and fund end-of-life collection, increasing compliance costs but also favoring integrated recyclers.

Where is the strongest regional growth expected?

Asia-Pacific is projected to rise at 5.8% CAGR thanks to Indonesia's nickel supply chain and large-scale infrastructure electrification.

Page last updated on: