Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

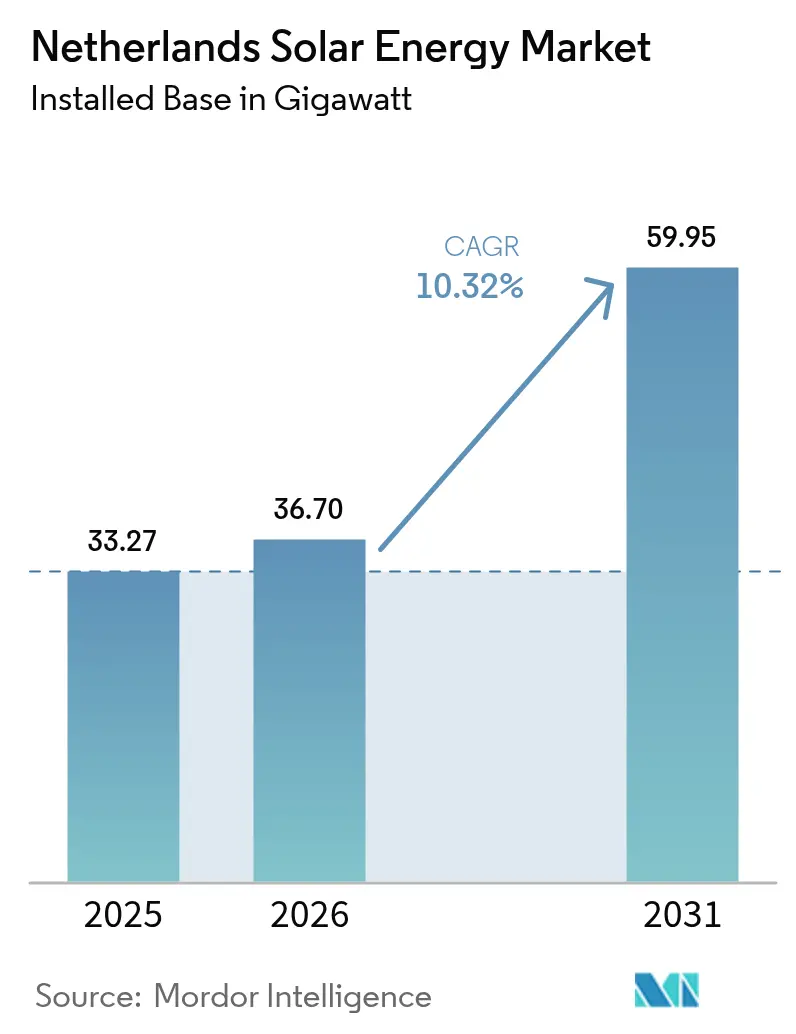

| Base Year Market Size (2025) | 33.27 gigawatt |

| Market Volume (2026) | 36.7 gigawatt |

| Market Volume (2031) | 59.95 gigawatt |

| Growth Rate (2026 - 2031) | 10.32% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Solar Energy Market Analysis by Mordor Intelligence

The Netherlands Solar Energy Market size in 2026 is estimated at 36.7 gigawatt, growing from 2025 value of 33.27 gigawatt with 2031 projections showing 59.95 gigawatt, growing at 10.32% CAGR over 2026-2031.

Market Analysis

Strong policy mandates, a sustained decline in the levelized cost of electricity, and a pre-deadline rush ahead of the 2027 net-metering phase-out are reinforcing growth momentum. Corporate power-purchase agreements (PPAs) from data-center and retail giants are broadening demand beyond the residential segment, while agrivoltaic incentives are unlocking dual-use land opportunities. At the same time, developers are investing in hybrid solar-plus-storage designs to navigate curtailment risk and secure premium evening-hour revenues. Grid upgrades announced by TenneT, coupled with the EU Fit-for-55 framework, position the Netherlands' solar energy market as a resilient growth story through 2030.

Key Report Takeaways

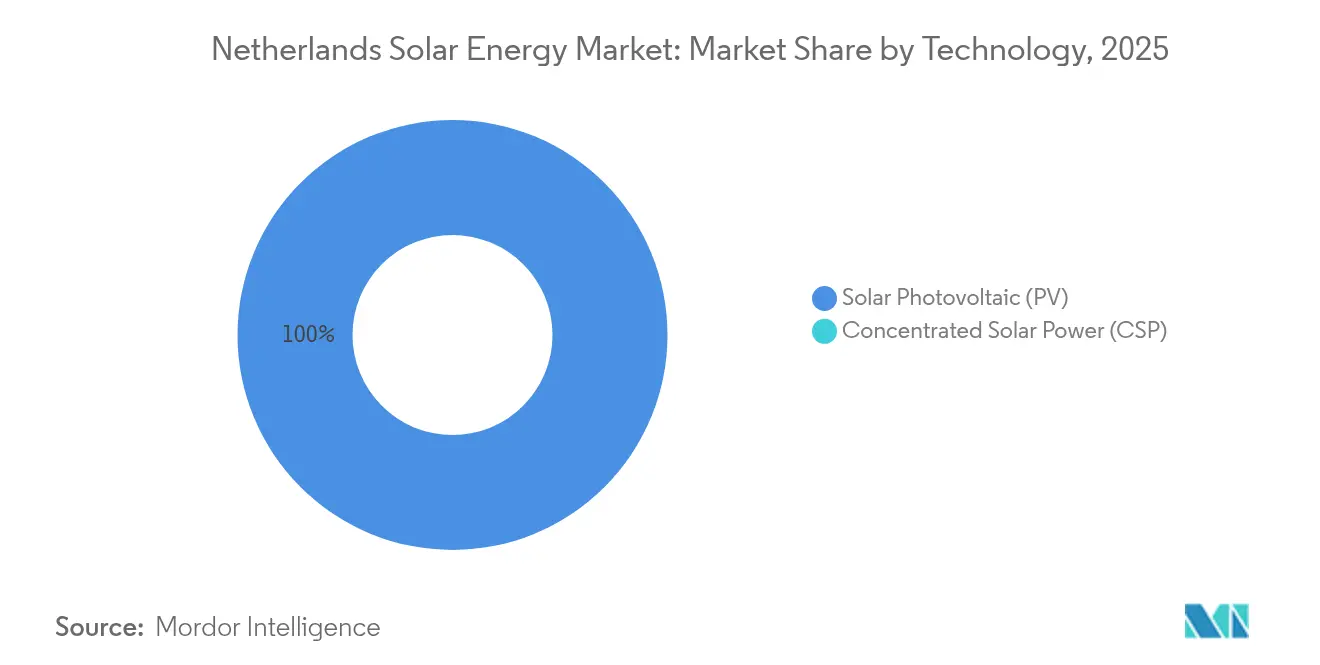

- By technology, photovoltaic systems held 100.00% of the Netherlands' solar energy market share in 2025.

- By grid type, on-grid assets commanded 98.62% of the Netherlands solar energy market size in 2025, while off-grid installations are advancing at a 15.21% CAGR toward 2031.

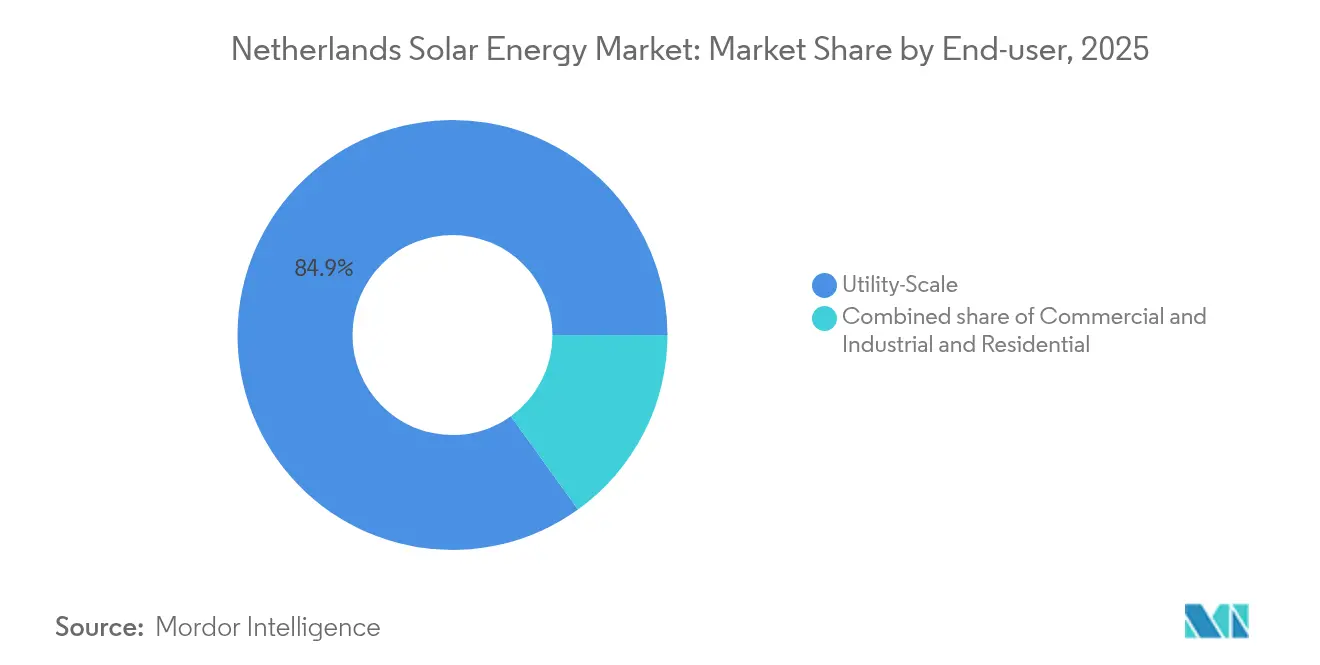

- By end-user, commercial and industrial projects grew 13.78% year over year in 2025 and are set to outpace utility-scale additions through 2031.

- By geography, Noord-Brabant and Limburg together accounted for 34.78% of installed capacity in 2025, whereas grid-constrained zones are forecast to register the highest curtailment-mitigation investments through 2028.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Fit-for-55 targets accelerate PV roll-out | +2.80% | National, aligned with EU mandates | Long term (≥ 4 years) |

| Phase-out of net-metering after 2025 spurs pre-cut-off rush | +1.90% | National, residential & small C&I | Short term (≤ 2 years) |

| Corporate PPAs from data-center & retail giants | +2.30% | Amsterdam & Rotterdam corridors | Medium term (2-4 years) |

| Declining LCoE below EUR 0.04/kWh | +1.70% | Utility-scale clusters nationwide | Medium term (2-4 years) |

| Agri-PV subsidies for livestock shading | +0.90% | Gelderland & Noord-Brabant | Long term (≥ 4 years) |

| Curtailment-insurance products | +0.60% | Noord-Brabant, Limburg & Zeeland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Fit-for-55 Targets Accelerate PV Roll-Out

The EU requirement to source 39% of final energy from renewables by 2030 translates into roughly 70 TWh of additional clean electricity for the Netherlands.[1]European Commission, “Fit-for-55 Package,” ec.europa.eu Utility-scale solar currently offers the lowest delivered power cost, with 2024 projects achieving EUR 0.03–0.04 per kWh amid a 35% slide in module prices. The SDE++ program set aside EUR 11.5 billion in 2024 to close the wholesale-versus-renewable cost gap, yet auction volumes missed the 5 GW target by 18% because grid connections, not capital, remain the bottleneck.[2]Netherlands Enterprise Agency, “SDE++ 2024 Allocation,” rvo.nl Developers are therefore pairing photovoltaics with one- to two-hour batteries, allowing stored midday output to meet evening peaks and satisfy guarantees of origin demanded under Renewable Energy Directive II.

Phase-Out of Net-Metering After 2025 Spurs Pre-Cut-Off Rush

Retail prosumers can currently offset electricity imports at retail rates; however, the scheme ends on January 1, 2027, when exports will earn only the wholesale price minus grid fees. The change extends residential payback from seven to roughly eleven years, prompting a wave of orders through 2025. Installers report full calendars into Q3 2025, while household battery-attachment rates reached 22% in 2024, nearly triple the 2023 level. Demand beyond 2027 is uncertain, implying that corporate and utility buyers, not homeowners, will dominate the Netherlands solar energy market thereafter.

Corporate PPAs from Data-Center and Retail Giants

Microsoft and Google signed 200 MW and 100 MW PPAs, respectively, with Eneco in 2024, locking fixed prices for 10-15 years. These contracts bypass retail networks and secure finance at interest rates up to 150 basis points below SDE++ projects. Connection queues in Noord-Holland now exceed 36 months, prompting behind-the-meter solar adjacent to data centers. This PPA wave mitigates merchant risk and cements corporate procurement as a durable pillar of the Netherlands' solar energy market.

Declining LCoE Below EUR 0.04/kWh

All-in costs for 2024 utility sites dropped to EUR 0.03–0.04 per kWh, putting solar ahead of gas peakers on price. Bifacial panels, now 40% of new builds, add 10-15% output, and agrivoltaic ground treatments further boost rear irradiance. Yet curtailment lifts effective costs by up to EUR 0.012 per kWh in grid-choked provinces, making one- to two-hour batteries a standard design feature.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe grid congestion in Noord-Brabant & Limburg | −1.8% | Southern provinces | Medium term (2-4 years) |

| Land-use opposition in Natura 2000 areas | −1.2% | Protected ecological zones | Long term (≥ 4 years) |

| Rising module waste-management costs | −0.7% | Nationwide | Long term (≥ 4 years) |

| Volatility in SDE++ clearing prices | −0.9% | Utility & large C&I | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Severe Grid Congestion in Noord-Brabant and Limburg

TenneT classifies both provinces as critical congestion zones, with a connection backlog topping 8 GW, three times the upgrade pipeline through 2027. Curtailment trims effective capacity factors to below 10%, forcing developers to install batteries that add EUR 0.15–0.20 per watt in capex. A proposed congestion-management scheme that would pay curtailed generators 90% of day-ahead prices remains under regulatory review, leaving near-term revenue uncertainty.

Land-Use Opposition in Natura 2000 Areas

Roughly 15% of Dutch territory falls under Natura 2000 protection, where environmental impact assessments can delay projects 18-24 months. Local objections have derailed several 50 MW-plus sites, pushing developers toward costly agrivoltaic or floating solutions. Even with streamlined priority-zone designations, only 30% of protected areas are fast-track eligible.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Monopoly Drives Innovation

Photovoltaics owned 100.00% of the Netherlands' solar energy market share in 2025, and the segment is forecast to post a 10.32% CAGR through 2031. Concentrated solar power remains absent due to sub-optimal direct normal irradiance of 1,000–1,100 kWh/m². Bifacial modules captured 40% of 2024 utility builds, and tandem perovskite-silicon prototypes reached 29% efficiency in domestic pilot lines run by the Solliance consortium.

Advances in tandem cells may shorten residential payback to under nine years once commercial releases start in 2026. Agrivoltaic roll-outs, supported by a EUR 200 million SDE++ envelope, use elevated racking that maintains farm output while tapping solar revenues, reinforcing land-use compatibility and sustaining the Netherlands solar energy market.

By Grid Type: Off-Grid Surge Targets Resilience

On-grid systems comprised 98.62% of installed capacity in 2025, yet off-grid arrays are forecast to expand at a 15.21% CAGR by 2031. Hyperscale data centers adopt islandable solar-plus-diesel-plus-battery clusters to mitigate outages costing EUR 10,000–15,000 per minute. Hybrid configurations cut daytime diesel burn and ensure uptime while bypassing congested interconnection queues. Grid-tied assets remain dominant, but rising curtailment risk is motivating designs that can island during congestion, store excess energy, then re-export once constraints ease, blurring the on-versus off-grid dichotomy in the Netherlands solar energy market.

By End-User: C&I Outpaces Utility Growth

Utility-scale farms held 84.92% of the Netherlands' solar energy market size in 2025. However, commercial and industrial installations are tracking a 13.78% CAGR to 2031 as corporate PPAs unlock sub-4% financing. Warehouses around Rotterdam and Amsterdam host 1–1.5 MW rooftop systems that offset up to 40% of load. Solar-as-a-service contracts eliminate upfront capex, accelerating uptake. Residential momentum is slowing; 2.6 million homes already feature PV, and net-metering sunset discourages new adopters beyond 2026. Utility builds still anchor volume additions, but C&I flexibility, rooftop availability, and tariff hedging prospects are shifting growth weight toward corporate buyers in the Netherlands solar energy market.

Geography Analysis

The Netherlands' solar energy market exhibits stark regional contrasts. Noord-Brabant and Limburg supplied 34.78% of capacity in 2025, lifted by marginally higher irradiance and lower land prices, yet both provinces face substation curtailment exceeding 15% of output. A EUR 4 billion TenneT expansion aims to add 3 GW of capacity by 2028, potentially clearing an 8 GW connection queue. In the interim, developers pivot to Noord-Holland and Zuid-Holland, where behind-the-meter PPAs with data centers bypass grid queues and stabilize revenues.

Gelderland and Overijssel, constrained by Natura 2000 overlap, are emerging hotspots for agrivoltaic projects that blend livestock grazing with power generation. Coastal Zeeland and Friesland exploit hybrid solar-wind synergies, sharing grid links and smoothing seasonal intermittency. Groningen and Drenthe cut permitting for agrivoltaics to 12 months, catalyzing northern cluster growth. Whether the Netherlands' solar energy market consolidates into high-capacity southern hubs post-upgrade or remains distributed hinges on grid build-out timelines and land-use compromises.

Regulatory Landscape

The Dutch solar framework combines national energy law, subsidy schemes, and network regulation. The Energiewet entered into force in 2026, with implementing rules under the Energiebesluit effective January 1, 2026, updating market and system governance for electricity generation and grid operation. For large-scale renewable electricity, SDE++ remains the core support instrument in 2026. The government has also published design choices to transition toward two-way Contracts for Difference (CfDs) for new projects from 2027, linking support to wholesale-price outcomes and addressing periods of negative prices.

For small-scale solar, the net-metering scheme (salderingsregeling) is scheduled to end on January 1, 2027, shifting household economics toward self-consumption and storage. On grid access and tariffs, the Netherlands Authority for Consumers and Markets (ACM) is advancing measures to improve efficient grid use, including work on producer feed-in tariffs for large-scale generators and standardized approaches for supplier model contracts that calculate feed-in costs per kWh for residential solar owners from 2026. These rules intersect with congestion in provinces such as Noord-Brabant and Limburg, where connection queues and curtailment risks are increasingly shaping project design and siting decisions.

Competitive Landscape

The top five developers, Vattenfall, Eneco, GroenLeven, BayWa r.e., and Shell Renewables, control roughly 45% of utility pipelines, indicating moderate concentration. Vertically integrated utilities leverage EPC and trading desks to capture value chain margins, while Chinese module makers vie for cost and product innovation. Residential and C&I installation remains fragmented among 200-plus contractors, though roll-ups by solar-as-a-service platforms are accelerating.

Competitive edges now rest on three pillars: securing long-dated corporate PPAs, mastering agrivoltaic engineering to navigate land constraints, and integrating storage to monetize price spreads. SMA Solar and GoodWe are embedding grid-forming inverters that qualify solar plants for voltage support and black-start services. Floating solar, curtailment insurance, and virtual power plants represent emerging niches. EU WEEE compliance is also differentiating suppliers like First Solar that run take-back schemes.

Netherlands Solar Energy Industry Leaders

Solarfields Nederland BV

DMEGC Solar Energy

Vattenfall AB

Orsted A/S

AB SOLAR TOTAL.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The planned shift from SDE++ to a CfD-based support model creates space for developers, utilities, and financiers to structure projects around price volatility and settlement mechanics. In April 2026, the government (via RVO) set out design choices for CfDs for renewable electricity, targeting a first bidding procedure in autumn 2027 and directly addressing negative-price exposure that has weakened merchant and SDE++ business cases. This transition supports opportunities in utility-scale and large C&I portfolios pairing solar with storage, using curtailment-aware dispatch, and relying on corporate offtake structures to reduce dependence on retail export remuneration.

Distributed and community-led solar also has a dedicated funding channel through the Cooperative Energy Generation (SCE) scheme, planned to open from March 2 to October 1, 2026, with a budget of EUR 78 million. This reinforces an opportunity set for energy cooperatives, municipalities, and aggregators working on standardized rooftop and near-load projects. On the demand side, Statistics Netherlands (CBS) reported solar generation reaching 93 PJ in 2025 (up 19% from 2024), supporting continued system-level relevance as the market moves away from mass net-metering-driven residential additions toward self-consumption and grid-supportive designs. In parallel, the Roadmap Circular Solar Power Systems launched on November 5, 2025, pushing circular design and high-value recycling. As module waste-management costs become more material to total project economics, it creates openings for take-back services, refurbishment, and compliant end-of-life processing.

Recent Industry Developments

- July 2026: The Netherlands Authority for Consumers and Markets (ACM) implemented new rules for grid access that prioritize essential facilities such as care and education over households and businesses. The update shows congestion management moving from ad hoc measures toward formal prioritization, affecting connection timelines and increasing the value of behind-the-meter solar and storage in constrained areas.

- June 2026: DMEGC Solar signed a strategic cooperation agreement with PHOTOMATE at Intersolar Europe 2026 to distribute INFINITY RT 3.0 PV modules across Europe, including the Netherlands. The deal broadens availability of newer module lines through established distribution channels, which can influence EPC sourcing strategies and replacement cycles for Dutch rooftop and C&I installers.

- August 2024: TenneT announced a EUR 4 billion grid expansion package to add 3 GW of substation capacity in Limburg and Noord-Brabant. The program targets two of the most constrained provinces for solar interconnection and supports the market shift toward hybrid solar-plus-storage designs as grid reinforcement work progresses over a multi-year timeline.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers solar power capacity in the Netherlands, counted as installed and grid-connected solar energy systems across residential, commercial, industrial, and utility settings, and tracked in gigawatts so the sizing stays tied to physical deployment.

Scope exclusions: We do not count unrelated power generation sources, and we do not treat electricity price or power trading as part of the solar energy market size.

Segmentation Overview

- By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- By Grid Type

- On-Grid

- Off-Grid

- By End-User

- Utility-Scale

- Commercial and Industrial (C&I)

- Residential

- By Component (Qualitative Analysis)

- Solar Modules/Panels

- Inverters (String, Central, Micro)

- Mounting and Tracking Systems

- Balance-of-System and Electricals

- Energy Storage and Hybrid Integration

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a fact base on how much solar is installed, how fast it is being added, and what the policy and grid constraints look like for the Netherlands. For this, we lean on public sources such as Statistics Netherlands (CBS), IEA PVPS, Eurostat energy statistics, European Commission energy and climate documents, and Dutch transmission and grid operator publications where available.

We also use company annual reports, investor presentations, tender announcements, and reputable press coverage to understand project pipelines and typical equipment price movements for solar builds. For cross-checks, a paid subscription used for company financials and another used for patent activity help us confirm supplier exposure and technology direction, without relying on any one dataset to set totals. These examples are not exhaustive, and many other public and paid references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions are used to stress-test what the desk data suggests, especially around how much of the pipeline is actually buildable under grid limits and permitting timelines in the Netherlands. We spoke with a mix of developers, EPC and installer groups, equipment participants, utilities, and commercial buyers so that pricing and commissioning assumptions could be corrected where needed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | |

| Mid tier: 48% | Functional/Unit leaders: 34% | |

| Smaller Players: 15% | Managers: 51% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where national installed capacity, yearly additions, and connection trends are reconstructed from official energy statistics and grid disclosures, and then mapped into the report scope. Once that core is set, the totals are corroborated using selective bottom-up checks such as sampled project commissioning lists, disclosed tender awards, and a simple ASP x volume sense check for major system types, which helps us spot undercounts or double counting.

A few practical inputs used in the model include annual capacity additions (GW), grid connection and curtailment signals, rooftop versus utility build mix, permitting and interconnection lead times, and typical system pricing by installation type (module and inverter price direction is treated as an input, not a fixed constant). Where data is missing for a sub-segment, the gap is handled through penetration-style assumptions linked to observable build activity, followed by rechecks with interview feedback.

Forecasts are developed using scenario analysis, because policy updates, net-metering changes, and grid availability can shift the short-term path even if long-term targets remain stable in the Netherlands. Final forecast paths are then aligned to expert views on near-term execution constraints and expected price normalization over the forecast window.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, so the capacity story, installation activity, and price logic do not contradict each other in the Netherlands solar market. Large variances trigger a deeper look at the underlying drivers, after which assumptions are adjusted and reviewed again before sign-off.

Each report is refreshed annually, and interim updates are made when a material policy, grid, or pricing event changes the demand picture. Before delivery, the model is re-run with the latest available datapoints, and re-contacts are done when new information creates a meaningful swing in the results.

Mordor Intelligence's Netherlands Solar Energy Market Sizing Compared With Other Published Estimates

Different publishers often land on different solar market values because they do not always measure the same thing, and the timing of price and currency inputs can shift the number even when the installed base is similar. In this market, the gaps usually come from whether sizing is done in capacity units or in USD, and whether forecasts assume rapid price declines or a steadier ASP path.

In our build, the estimate is updated on an annual refresh cycle with a consistent currency timing rule and an ASP logic that is rechecked through recent installation activity and grid-connection reality, which helps keep the sizing stable across updates, and that discipline is applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 36.70 B (2026) | |

| Global Consultancy A | USD 3.50 B (2026) | This figure is presented as a solar power value number without clear disclosure on whether it counts only yearly installations, only equipment revenue, or a narrower end-user mix, which can compress the total versus an installed-capacity anchored view. |

| Industry Research Group B | USD 40.60 B (2024) | The number is reported in gigawatts in its own write-up, and it appears to mix a capacity metric with a value label, so direct comparisons can drift due to unit treatment and different base-year timing. |

Overall, the spread is mainly explained by unit choice, base-year timing, and how pricing is handled, rather than a disagreement that solar is growing in the Netherlands. By tying the model to installed capacity signals and then checking pricing and execution constraints, the resulting market size stays easier to reproduce and audit year to year.

Key Questions Answered in the Report

How large is the Netherlands solar energy market in 2026?

Installed capacity totals 36.7 GW, and the Netherlands solar energy market is on track for 59.95 GW by 2031.

What CAGR is forecast for Dutch solar from 2026 to 2031?

The market is expected to register a 10.32% CAGR during the period.

Will the net-metering phase-out halt residential solar growth in the Netherlands?

Orders are surging until 2026, but residential demand is likely to slow post-2027, shifting growth to corporate and utility projects.

Which segment is growing fastest in Dutch solar?

Commercial and industrial installations lead with a forecast 13.78% CAGR through 2031 due to widespread corporate PPAs.

Where are grid constraints most severe for Dutch solar developers?

Noord-Brabant and Limburg provinces face the highest curtailment rates and connection backlogs.

What technology trend will shape Dutch solar competitiveness beyond 2026?

Hybrid solar-plus-storage systems that capture price spreads and mitigate curtailment are becoming the new investment benchmark.

Page last updated on: