Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

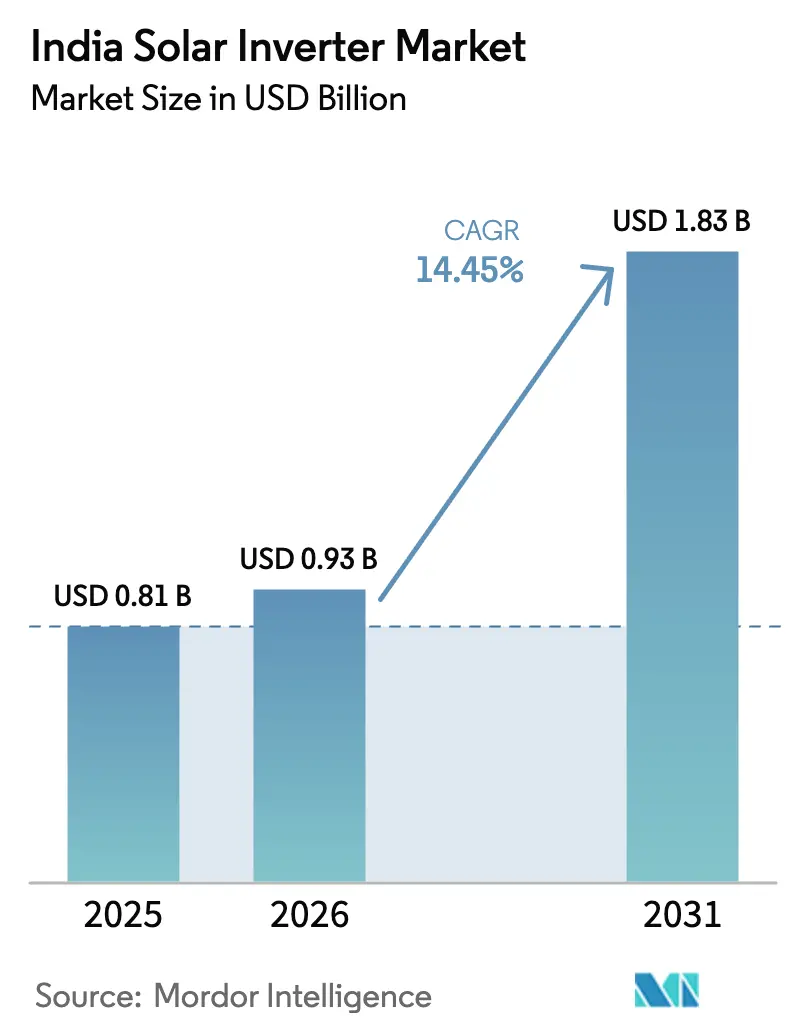

| Base Year Market Size (2025) | USD 0.81 Billion |

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 14.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Solar Inverter Market Analysis by Mordor Intelligence

The India Solar Inverter Market size is expected to increase from USD 0.81 billion in 2025 to USD 0.93 billion in 2026 and reach USD 1.83 billion by 2031, growing at a CAGR of 14.45% over 2026-2031.

Rapid policy support, falling photovoltaic (PV) module prices, and aggressive state-level renewable purchase obligations are expanding project pipelines across utility-scale parks and distributed rooftop systems, lifting demand for high-efficiency conversion equipment. Central inverters are benefiting from the gigawatt-scale solar parks under construction in Rajasthan and Gujarat, while string inverters dominate commercial rooftops that prefer modular expansion and easier maintenance. Three-phase architectures command two-thirds of shipments because most plants tie into medium-voltage feeders that require balanced loads and reactive-power support. Meanwhile, off-grid solutions linked to irrigation pumps and village microgrids are expanding faster than the on-grid segment as PM-KUSUM incentives lower upfront costs for farmers in states with unreliable distribution networks.

Key Report Takeaways

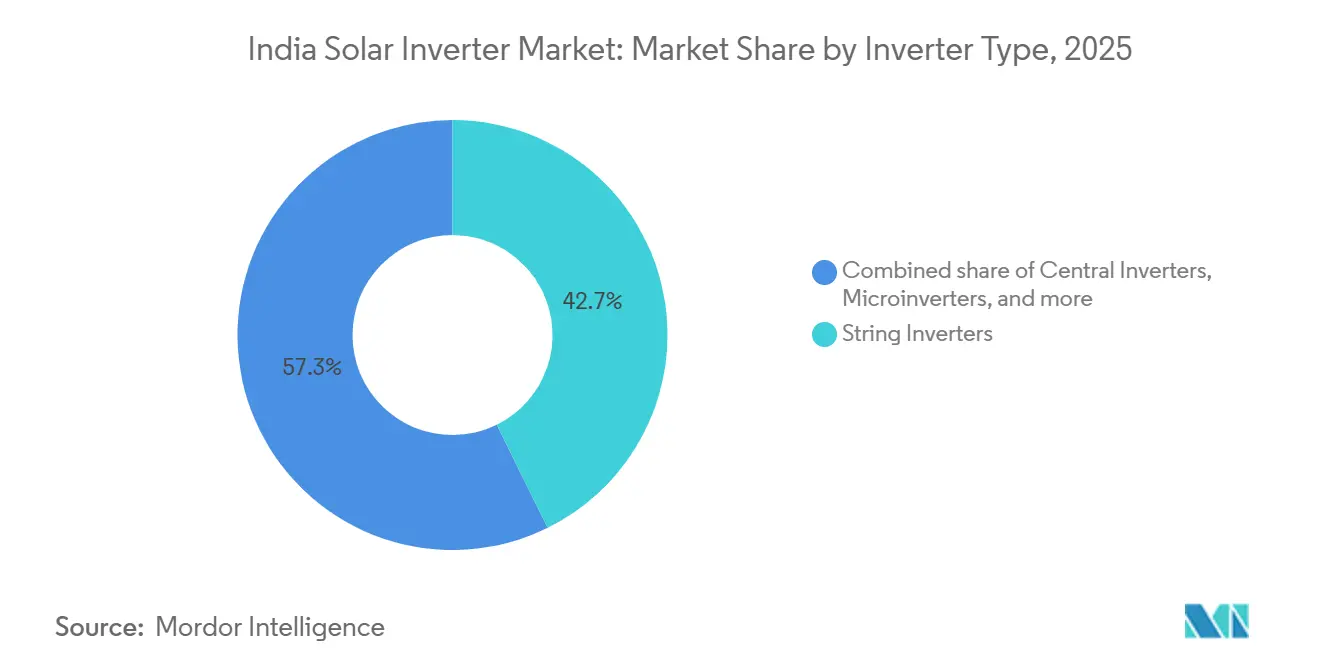

- By inverter type, string inverters led with 42.7% of the India solar inverter market share in 2025, while central units are projected to rise at a 17.3% CAGR through 2031 as multi-gigawatt solar parks standardize on high-capacity blocks.

- By phase, three-phase designs accounted for 67.4% of the India solar inverter market size in 2025, and the same category is forecast to advance at a 14.9% CAGR to 2031 on the back of commercial and utility deployment.

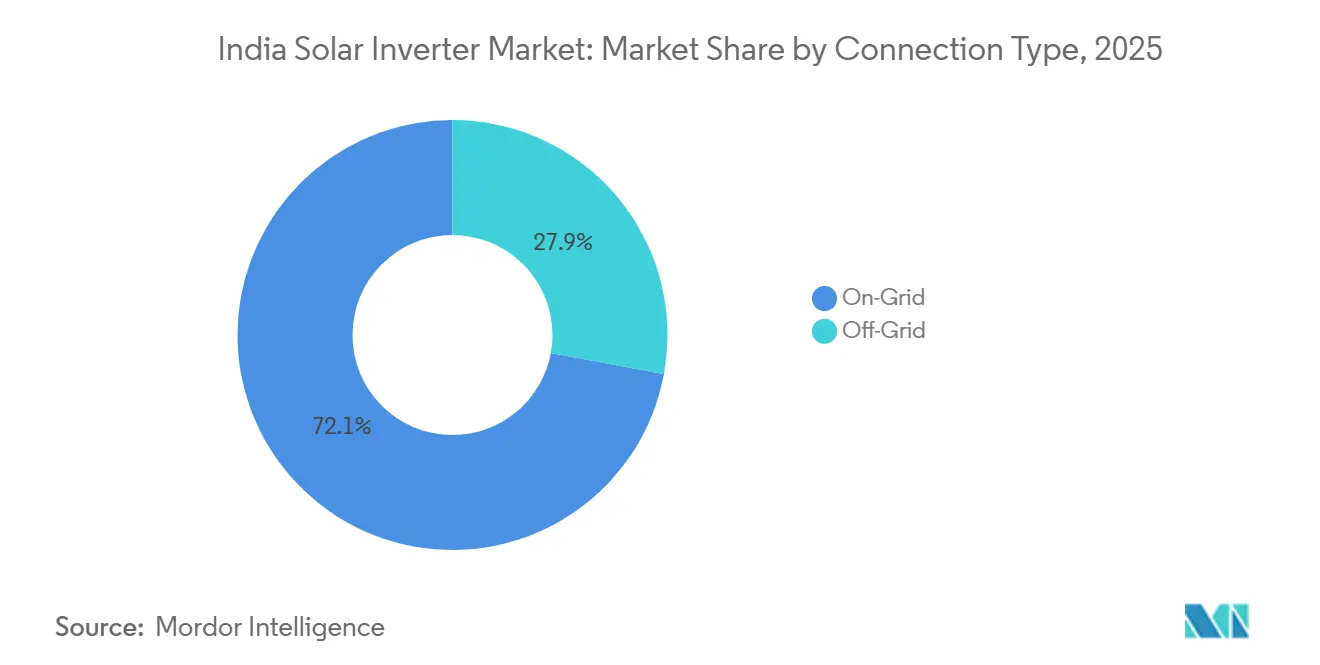

- By connection, on-grid installations held 72.1% of demand in 2025; off-grid systems are the fastest growing, expanding at a 16.5% CAGR as feeder solarization scales under PM-KUSUM.

- By application, utility-scale projects claimed 61.4% of revenue in 2025, whereas residential arrays are expected to register the highest growth at 17.1% CAGR over 2026-2031, supported by the PM Surya Ghar Muft Bijli Yojana.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Solar Inverter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid decline in PV module prices | +3.8% | Gujarat, Rajasthan, Tamil Nadu, national spill-over | Medium term (2-4 years) |

| Favorable net-metering regulations | +2.9% | Delhi, Andhra Pradesh, Kerala, Telangana, national adoption | Short term (≤ 2 years) |

| Rising rooftop adoption among SMEs | +4.2% | Maharashtra, Karnataka, Tamil Nadu, national spread | Medium term (2-4 years) |

| Accelerated green-hydrogen linked solar bids | +3.6% | Gujarat, Rajasthan, emerging hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in PV Module Prices Reshapes Cost Economics

PV module prices dropped to USD 0.11 per watt in early 2025, down from USD 0.15 per watt the previous year, cutting utility-scale solar levelized costs below INR 2.00 per kilowatt-hour in high-irradiance states.[1]National Renewable Energy Laboratory, “Photovoltaic System Pricing Trends Q1 2025,” nrel.gov Cheaper modules raise the relative share of inverters in total system budgets from 6% to 9%, motivating developers to select models with weighted efficiencies above 98.5% to protect project returns. The resulting preference for 1,500 V central platforms in projects greater than 100 MW is clear in Rajasthan’s latest tender awards, where single-station blocks replaced distributed strings to reduce cabling and trenching costs. Equipment vendors are therefore redesigning power blocks with silicon-carbide devices that minimize thermal losses in ambient temperatures above 45 °C, typical of western India. In turn, the supply chain is shifting toward domestic assembly lines that can deliver megawatt-scale units in under eight weeks, a logistics-based differentiator in a market racing to commission capacity before fiscal-year tariff deadlines.

Favorable Net-Metering Regulations Unlock Distributed Generation

Twenty-eight Indian states and union territories now offer net-metering, and several, including Delhi and Telangana, permit virtual crediting across multiple premises, a crucial incentive for chains and housing societies.[2]Andhra Pradesh Electricity Regulatory Commission, “Net Metering Regulations 2024,” aperc.gov.in Telangana raised its per-consumer cap from 1 MW to 10 MW in 2024, opening rooftop opportunities for large factories that require three-phase inverters with voltage-ride-through features.[3]Telangana State Renewable Energy Development Corporation, “Net Metering Guidelines 2024,” tsredco.telangana.gov.in Payback periods for commercial systems have fallen below five years, driving procurement of smart inverters compliant with IEEE 1547-2018 and capable of reactive-power export to stabilize feeders. States such as Kerala also exempt rooftop exports from wheeling charges when generation is consumed within municipal limits, further shortening the break-even horizon for small enterprises. Vendors now bundle remote monitoring platforms and firmware upgrades because installers cite digital diagnostics as a deciding parameter for tender awards.

Rising Rooftop Adoption Among SMEs Drives Segment Diversification

Small and medium enterprises installed 2.8 GW of rooftop solar in 2024 as tariffs for commercial users crossed INR 9.00 per kilowatt-hour in Maharashtra and Karnataka. Capital subsidies of 20% for sub-10 kW systems under PM Surya Ghar reduce cash outlay and encourage SMEs to swap diesel gensets for solar-battery hybrids. String inverters dominate because their modularity lets firms expand capacity in 10 kW steps that mirror incremental load growth. Nevertheless, hybrid designs with integrated battery interfaces are gaining share because enterprises want to shave evening demand charges by discharging stored power during tariff peaks. Vendors that pre-certify to Bureau of Indian Standards (BIS) protocols and offer five-year onsite warranties are winning orders as finance providers insist on proven reliability before approving loans.

Accelerated Green-Hydrogen Linked Solar Tenders Create New Demand Vectors

Solar Energy Corporation of India floated 3.5 GW of bundled solar-electrolyzer tenders during 2024-2025, compelling developers to co-locate PV with hydrogen production that fluctuates rapidly with grid commands. These projects need inverters that can tolerate 130% overload for short bursts and ramp output in milliseconds to match electrolyzer load swings. Gujarat and Rajasthan have already approved 500 MW hubs, spurring demand for bidirectional inverter-controller packages able to manage battery buffers and prevent DC bus oscillations.[4]Ministry of New and Renewable Energy, “National Green Hydrogen Mission,” mnre.gov.in The Central Electricity Authority (CEA) treats these hybrid complexes as grid-support assets, so compliance with new ancillary-services codes is mandatory for financing. Suppliers that embed real-time droop control and grid-forming firmware within power stages are now shortlisted ahead of conventional units during bid evaluations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BIS certification bottle-necks for imports | –2.1% | Nationwide, heavy in states relying on imported hardware | Short term (≤ 2 years) |

| Land-acquisition delays for large parks | –1.8% | Rajasthan, Karnataka, Madhya Pradesh, Uttar Pradesh | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

BIS Certification Bottlenecks for Imports

The 2024 Quality Control Order demands that every grid-connected inverter above 10 kW carry a BIS mark, yet only 12 domestic labs are accredited to run the required IS 61683 and IS 62116 tests. Foreign manufacturers face 3- to 6-month queues, tying up working capital and delaying shipments for projects in Andhra Pradesh and Tamil Nadu. Smaller importers struggle the most because they lack buffer inventory and cannot negotiate priority slots, causing risk-averse developers to switch to locally assembled models that already hold certifications. The Ministry of Commerce has signaled mutual recognition agreements with ISO/IEC 17025-accredited overseas labs, but full implementation is unlikely before late 2026.[5]Directorate General of Foreign Trade, “Quality Control Orders for Solar Inverters 2024,” dgft.gov.in Until then, procurement schedules will remain tight, and developers are factoring certification lead times into bid margins.

Land-Acquisition Delays for Large Solar Parks

Farmers have challenged compensation rates and environmental clearances in Rajasthan’s Bhadla Phase IV and Karnataka’s Pavagada extensions, freezing over 5 GW of planned capacity. Protracted negotiations slow mobilization and defer inverter procurement because EPC contractors cannot confirm delivery windows without land possession. Central inverter suppliers, which need six-month lead times for custom containerized stations, are being asked to hold quotes for longer than usual, inflating hedging costs. Fragmented land ownership in Uttar Pradesh and Madhya Pradesh compounds the problem, with dozens of smallholders holding veto power over contiguous parcels needed for 100 MW-plus arrays. State utilities are experimenting with land pools and single-window clearances, but analysts expect large-park completion schedules to slip into the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Inverter Type: Central Units Capture Utility Momentum

Central inverters are projected to grow at a 17.3% CAGR between 2026 and 2031, the fastest within the India solar inverter market, as developers increasingly prefer single-station blocks for projects above 100 MW. This preference lifts the India solar inverter market size associated with central platforms, especially in Rajasthan’s and Gujarat’s multi-gigawatt parks, where economies of scale matter. Central units rated 1 MW-5 MW cut balance-of-system costs by trimming DC cabling and trench lengths. Vendors are integrating silicon-carbide switches and liquid cooling to surpass the Bureau of Energy Efficiency’s 97.5% weighted-efficiency mandate effective 2026.

String inverters still held 42.7% of the India solar inverter market share in 2025, dominating rooftops and mid-size industrial arrays thanks to modular scalability and simple maintenance regimes. Microinverters, with less than 5% penetration, appeal to shaded residential roofs where module-level mismatch erodes energy yields, though higher unit costs limit uptake. Hybrid and battery-ready products are rising fast because the CEA targets 336 GWh of storage by 2029-30, pushing developers toward bidirectional electronics that can tap ancillary-service revenue streams.

By Phase: Three-Phase Dominance Matches Grid Topology

Three-phase products secured 67.4% of shipments in 2025 and will expand at a 14.9% CAGR through 2031 as most commercial and utility installations tie into 11 kV or 33 kV feeders that demand balanced loads. In turn, the India solar inverter market size for three-phase units increases with each net-metering expansion that elevates rooftop caps for factories. Revised grid codes require reactive-power support within a 0.9 leading-lagging band for arrays above 100 kW, an easy requirement for three-phase blocks but difficult for single-phase alternatives.

Single-phase systems remain vital for homes installing 1 kW-5 kW arrays under the PM Surya Ghar scheme. Price competition is intense because Chinese imports start below INR 5,000 per unit, but domestic assemblers retain share by bundling five-year service warranties and BIS-approved safety features. As time-of-day tariffs widen, hybrid single-phase designs with embedded battery ports should defend margins by enabling peak-shaving for households.

By Connection Type: Off-Grid Gains from Agricultural Push

On-grid equipment retained 72.1% of demand in 2025, yet off-grid and hybrid variants are advancing at a 16.5% CAGR due to PM-KUSUM feeder solarization that targets 2 million standalone pumps. The India solar inverter market size attached to rural feeders is therefore rising faster than the national average. Off-grid units must tolerate heat, dust, and voltage swings while delivering constant torque to irrigation pumps, which steers buyers toward IP65-rated enclosures and wide-input devices.

Rural microgrids that combine solar, storage, and occasional diesel also demand inverters with black-start capability, adding price premiums but ensuring autonomous restarts after outages. International brands such as Victron and Schneider compete here by offering modular inverter-charger stacks scalable from 5 kW upward.

By Application: Residential Surge Reshapes Demand Mix

Utility-scale projects captured 61.4% of orders in 2025 on the back of 18.5 GW of capacity additions that mostly used central inverters. However, residential systems are forecast to grow at a 17.1% CAGR through 2031, the quickest segment of the India solar inverter market, because PM Surya Ghar subsidies cut the post-incentive cost of a 3 kW rooftop array below INR 40,000. Residential buyers now choose single-phase or microinverter models that support battery add-ons to dodge evening peak tariffs topping INR 8.00 per kilowatt-hour.

Commercial and industrial rooftops keep expanding as electricity prices for factories outstrip residential tariffs and as revised net-metering rules let businesses offset up to 90% of consumption in states such as Delhi and Kerala. Developers of utility-scale parks are pivoting toward solar-plus-storage bids that require bidirectional inverters capable of 2-4 hour discharge windows set by SECI tenders.

Geography Analysis

Rajasthan, Gujarat, and Tamil Nadu together hosted 48% of national solar capacity by December 2025, and thus form the epicenter of the India solar inverter market. Rajasthan led with 24.5 GW, mostly utility-scale, demanding central inverters rated for 1,500 V DC strings and AC outputs matched to 33 kV substations. Gujarat followed at 17.8 GW, split evenly between parks and rooftops that benefit from a 20 MW virtual net-metering cap. Tamil Nadu’s 16.2 GW includes 4.5 GW of rooftop installations in textile and automotive clusters, reinforcing demand for three-phase string models.

Karnataka and Maharashtra are emerging growth poles, adding more than 6 GW combined in 2024, helped by state subsidies for commercial rooftops and innovative floating-solar pilots that seek corrosion-resistant inverter housings. Andhra Pradesh and Telangana focus on agricultural feeder solarization, installing hybrid units able to island during evening feeder shut-downs. Northern states such as Uttar Pradesh lag because of land and grid constraints, yet both are tendering parks that will require central stations with ride-through capabilities defined by new CEA codes.

Over the forecast horizon, western and southern zones remain the largest buyers thanks to superior irradiation and proactive policies, though eastern and north-eastern states show pockets of off-grid demand where poor grid penetration drives microgrid deployments.

Competitive Landscape

Market concentration is moderate: the top five brands supplied roughly three-quarters of utility-scale shipments in 2024, but residential and commercial rooftops remain fragmented with more than 30 active labels. Chinese vendors such as Sungrow and Huawei win large-park orders by leveraging vertically integrated supply chains and concessional export credit to keep prices low. European specialists SMA and Fronius protect premium niches through 10-year warranties and grid-support firmware that helps developers secure insurance discounts.

Domestic assembly is accelerating. Sungrow commissioned a 20 GW Bengaluru plant in January 2026, slashing delivery windows to under three weeks and embedding BIS test bays onsite. Delta Electronics expanded its Hosur line by 5 GW in 2025, integrating silicon-carbide devices that raise conversion efficiency above 98.5%. Technology is a key differentiator: vendors shipping grid-forming microinverters or hybrid controllers that combine battery management and advanced islanding protection capture higher margins despite intense price competition.

Entry barriers are climbing. BIS marks are compulsory, the Bureau of Energy Efficiency enforces a 97.5% weighted-efficiency floor from January 2026, and the CEA ties ancillary-service eligibility to demonstrated droop control and black-start functionality. Suppliers without accredited labs or field data to prove compliance are losing share as lenders refuse to finance projects that carry certification risk.

India Solar Inverter Industry Leaders

Sungrow Power Supply Co., Ltd.

Huawei Technologies Co., Ltd.

SMA Solar Technology AG

FIMER S.p.A.

Delta Electronics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Juniper Green Energy has inked an 835 MW inverter supply deal with Sungrow for its solar initiatives in India. Under this pact, Sungrow will supply inverters for Juniper's solar ventures located in Maharashtra and Rajasthan.

- April 2025: POM Systems & Services, based in Bengaluru, has unveiled its new POM hybrid inverters, available in power ratings of 3 kW, 5 kW, and 10 kW. These innovative inverters merge the capabilities of both traditional solar inverters and battery inverters into one unit.

- April 2025: Kosol Energie, in collaboration with GoodWe, a global frontrunner in solar inverters, has successfully commissioned a 10 MW solar project in Kutch, Gujarat. The project, undertaken for the Gujarat State Electricity Corporation Limited (GSECL), prominently featured GoodWe's 350 kW UT string inverters.

- July 2024: Hero Future Energies has awarded Sungrow an 850 MW contract to provide inverters for various renewable energy initiatives across India. Sungrow's cutting-edge 1500V inverter solutions, crafted at their Bengaluru facility, are tailored for demanding environments.

India Solar Inverter Market Report Scope

The Scope of the India Solar Inverter Market includes:-

By Inverter Type

| Central Inverters |

| String Inverters |

| Microinverters |

| Hybrid/Battery-Ready Inverters |

By Phase

| Single-phase |

| Three-phase |

By Connection Type

| On-Grid |

| Off-Grid |

By Application

| Residential |

| Commercial and Industrial |

| Utility-Scale |

| By Inverter Type | Central Inverters |

| String Inverters | |

| Microinverters | |

| Hybrid/Battery-Ready Inverters | |

| By Phase | Single-phase |

| Three-phase | |

| By Connection Type | On-Grid |

| Off-Grid | |

| By Application | Residential |

| Commercial and Industrial | |

| Utility-Scale |

Key Questions Answered in the Report

What is the forecast value of the India solar inverter market by 2031?

The market is projected to reach USD 1.83 billion by 2031.

How fast is the residential segment growing?

Residential installations are forecast to expand at a 17.1% CAGR between 2026 and 2031, the fastest among all applications.

Which inverter type is expected to lead future growth?

Central inverters are poised for the highest growth at 17.3% CAGR as developers build multi-gigawatt solar parks.

Why are three-phase inverters dominant in India?

They suit medium-voltage feeders, meet new reactive-power mandates, and therefore secured 67.4% share in 2025.

How do new BIS rules affect foreign suppliers?

Mandatory domestic testing can delay imports by up to six months, encouraging developers to favor locally certified models.

What role does PM-KUSUM play in off-grid demand?

The scheme subsidizes 2 million standalone solar pumps, driving a 16.5% CAGR in off-grid inverter sales.

Page last updated on: