Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

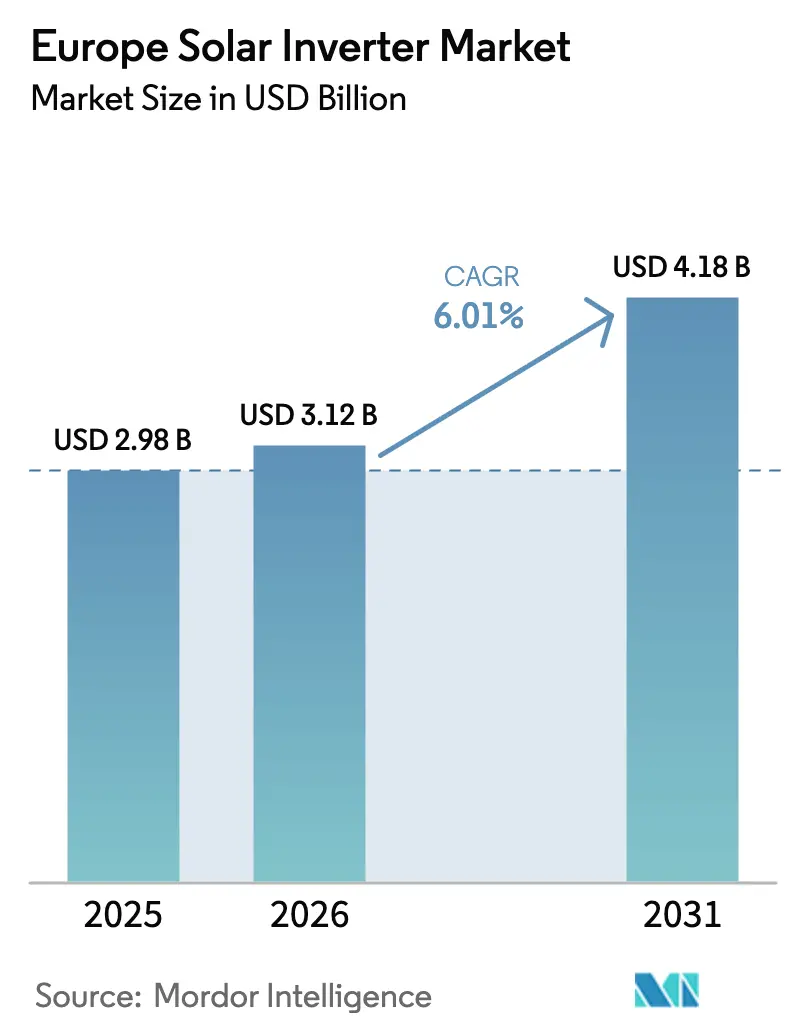

| Base Year Market Size (2025) | USD 2.98 Billion |

| Market Size (2026) | USD 3.12 Billion |

| Market Size (2031) | USD 4.18 Billion |

| Growth Rate (2026 - 2031) | 6.01% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Solar Inverter Market Analysis by Mordor Intelligence

The Europe Solar Inverter Market size is expected to increase from USD 2.98 billion in 2025 to USD 3.12 billion in 2026 and reach USD 4.18 billion by 2031, growing at a CAGR of 6.01% over 2026-2031.

The surge reflects accelerated photovoltaic build-out under REPowerEU, the continued rooftop boom fed by high retail electricity prices, and a regulatory pivot toward grid-forming functionality that is reshaping product design and supplier strategies. Central inverters retained dominance because of Spain’s and Portugal’s utility-scale pipelines, while microinverters gained momentum in shade-prone northern roofs. Semiconductor supply constraints moderated price erosion but did not derail demand, as suppliers re-tooled firmware to comply with ENTSO-E’s 2026 grid-forming mandates. Competitive intensity stayed moderate; the top five firms captured roughly 55-60% revenue, leaving space for cost-driven Chinese challengers and software-oriented niche specialists.

Key Report Takeaways

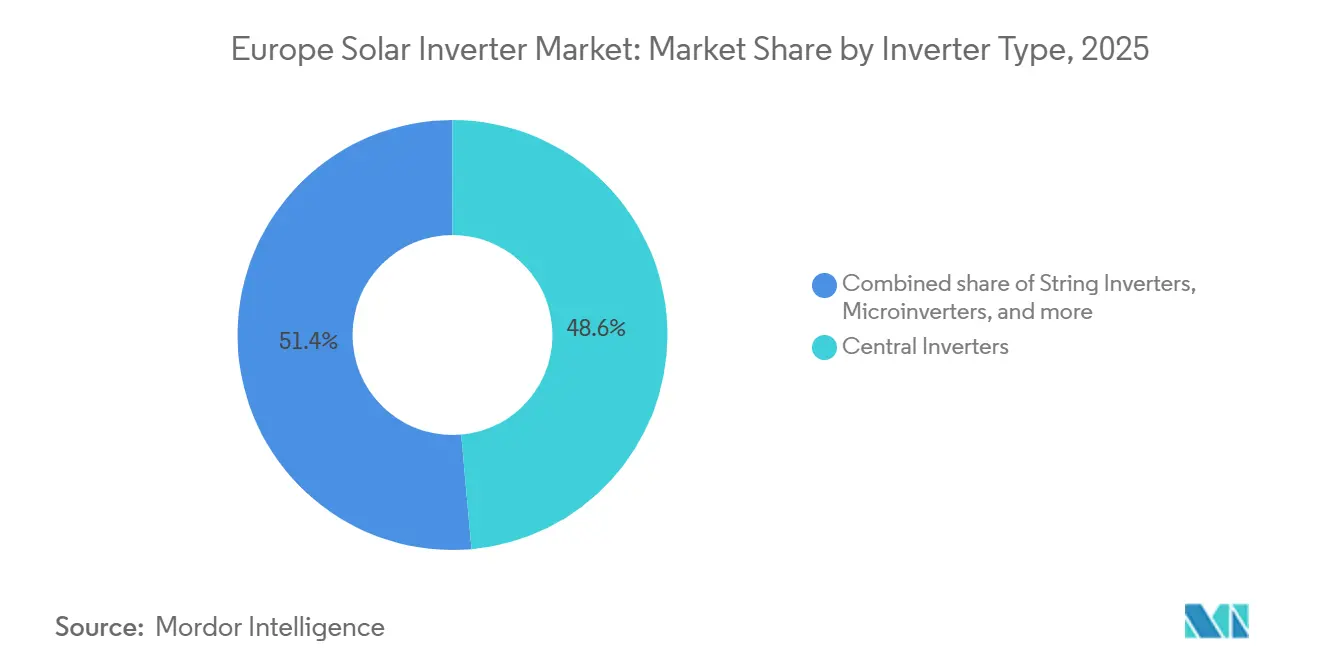

- By inverter type, central inverters led with 48.6% revenue share in 2025; microinverters are projected to expand at a 7.3% CAGR through 2031.

- By phase, three-phase products accounted for 73.4% of demand in 2025; single-phase units will rise at a 6.4% CAGR, mirroring the rooftop surge.

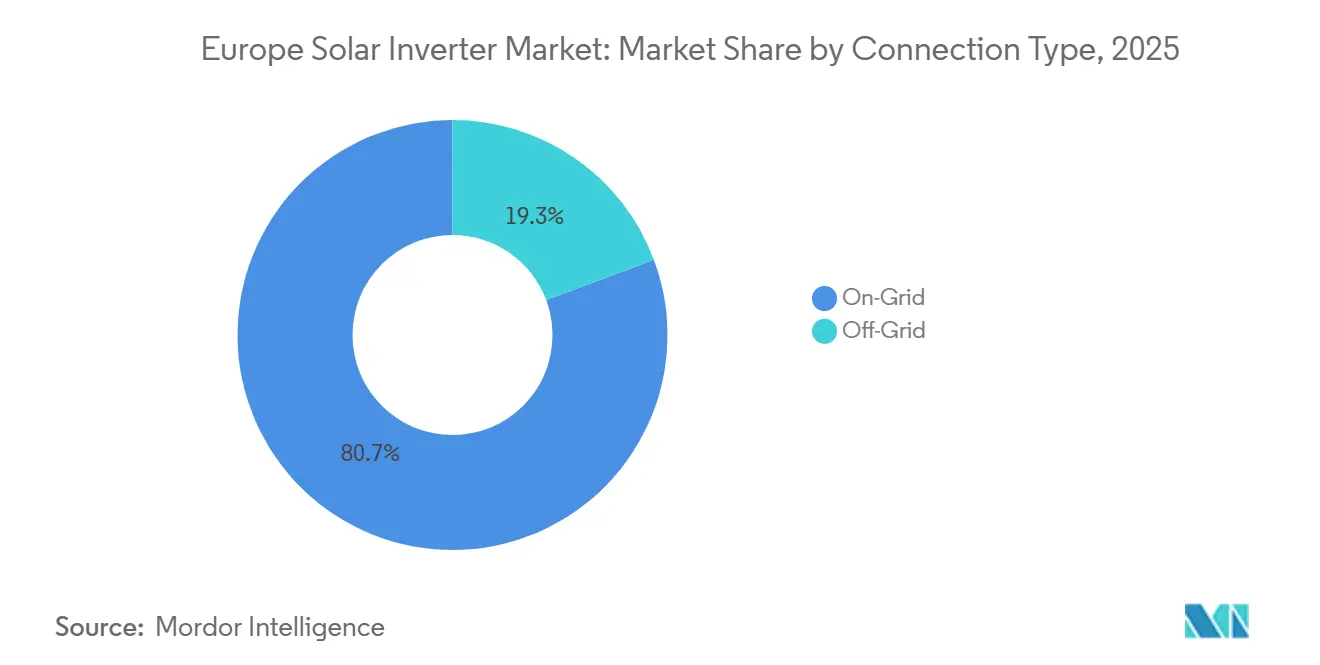

- By connection type, on-grid designs held 80.7% share in 2025, whereas off-grid inverters are forecast to climb at a 7.7% CAGR as islanded microgrids gain traction.

- By application, utility-scale systems commanded 59.1% of the European solar inverters market share in 2025, while residential installations are expected to grow at a 6.8% CAGR during the forecast period.

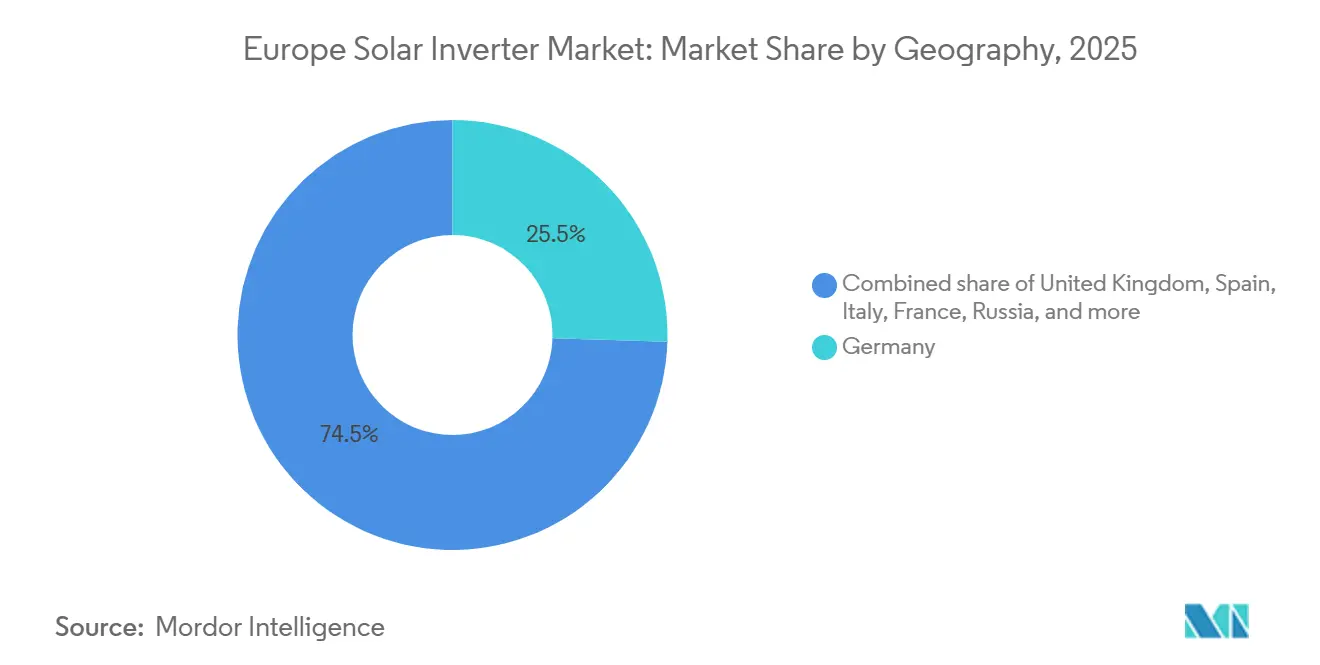

- By geography, Germany captured 25.5% revenue in 2025; Italy is poised for the fastest 11.1% CAGR thanks to streamlined permitting and record 2024 additions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Solar Inverter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Fit-for-55 & REPowerEU deployment targets | 1.80% | EU-wide, led by Germany, Spain, Italy, France | Medium term (2-4 years) |

| Rooftop self-consumption boom amid high retail electricity prices | 1.50% | Germany, Netherlands, Belgium, Denmark | Short term (≤ 2 years) |

| Declining $/W of string & hybrid inverters | 1.20% | Southern and Eastern Europe | Medium term (2-4 years) |

| Utility-scale PPA pipeline acceleration across Spain, Portugal & Greece | 1.00% | Iberian Peninsula, Greece | Medium term (2-4 years) |

| Mandatory grid-forming “smart inverter” codes (NC RfG 2026 update) | 0.60% | Germany, Netherlands, France, Italy | Long term (≥ 4 years) |

| IPCEI-backed reshoring of European inverter manufacturing | 0.40% | Germany, France, Italy, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Fit-for-55 & REPowerEU Deployment Targets

Binding 42.5% renewable-energy legislation and the EU Solar Strategy lift average annual installations to 60-70 GW, more than double the 2019-2023 pace.[1]European Commission, “Solar Energy,” energy.ec.europa.eu Faster rooftop approvals under Council Regulation 2022/2577 compressed permitting to three months, steering demand toward string and microinverters. Germany added 14.6 GW and Italy 5.3 GW in 2024, underscoring early policy traction.[2]Clean Energy Wire, “Germany's Energy Consumption and Power Mix in Charts,” cleanenergywire.org The Iberian pipeline illustrates geographic concentration where high irradiance and PPAs intersect. Collectively, these factors underpin the 6.01% CAGR projected for the European solar inverters market.

Rooftop Self-Consumption Boom Amid High Retail Electricity Prices

EU household tariffs averaged EUR 0.28 per kWh in 2025, about 40% above pre-2021 levels, sustaining sub-7-year payback for solar-plus-storage.[3]Eurostat, “Electricity Price Statistics,” ec.europa.eu Germany’s EUR 0.32 per kWh retail price drove a rooftop wave that relied on hybrid inverters capable of battery arbitrage. The Netherlands accelerated battery adoption by phasing out net metering in 2025.[4]Dutch Government, “Solar Energy Policy and Net Metering,” government.nl Microinverters benefited from shade mitigation in dense urban roofs, while software features such as dynamic tariff response became key differentiators. The residential up-trend explains why the European solar inverters market is tilting toward premium, software-rich products.

Declining $/W of String & Hybrid Inverters

Average selling prices for 10-50 kW string units fell from USD 0.12 to USD 0.10 per watt between 2023 and 2025 as Chinese scale-up improved silicon-carbide yields. Hybrid models saw even steeper drops, narrowing the cost gap versus basic string devices and lifting attach rates for residential batteries. Price erosion expanded access in Southern and Eastern Europe, where project IRRs are tight. Western incumbents countered margin pressure by emphasizing grid services and long warranties. Notably, grid-forming variants still carry an 8-12% premium, reflecting higher-rated power electronics.

Utility-Scale PPA Pipeline Acceleration Across Spain, Portugal & Greece

Spain’s 62 GW pipeline and Portugal’s successive auctions create a deep order book through 2031. Central inverters benefit from low balance-of-system cost at scale, yet developers increasingly specify 100-250 kW string units to optimize bifacial tracker arrays. Greece’s National Energy and Climate Plan lifts solar ambition to 7.7 GW by 2030. PPA structures with partial merchant exposure reward advanced inverter controls that enhance capture rates, favoring suppliers with proven ancillary-service firmware. The European solar inverters market, therefore, rewards both low-cost central architectures and premium string solutions that unlock grid-service revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor supply bottlenecks for IGBTs & SiC MOSFETs | -0.9% | EU-wide, with acute effects in Germany, France, Italy (high-volume markets) | Short term (≤ 2 years) |

| Grid-connection delays & curtailment risks in DE/NL/IT | -0.7% | Germany, Netherlands, Italy (high-penetration grids) | Medium term (2-4 years) |

| Cyber-security scrutiny on imported inverters (ENISA guidelines) | -0.4% | EU-wide, particularly affecting non-EU manufacturers and importers | Medium term (2-4 years) |

| Sunset of net-metering incentives in key markets | -0.5% | Netherlands, Belgium, Austria, with potential spillover to Denmark and Sweden | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply Bottlenecks for IGBTs & SiC MOSFETs

Lead times for 1200 V SiC devices averaged 26-32 weeks in 2025, double pre-pandemic norms, as electric-vehicle demand competed for wafers. SMA reported shipment delays totalling 1.5 GW in its 2024 filings. Substituting lower-spec IGBTs reduces efficiency and raises thermal losses, squeezing project margins. New fabs from Infineon and Wolfspeed will ease scarcity after 2027, but short-term friction persists, trimming expected growth in the European solar inverters market.

Grid-Connection Delays & Curtailment Risks in DE/NL/IT

Germany’s connection queue exceeded 40 GW in 2025, with average waits of 18-24 months, while curtailment hit 8.2 TWh in 2024. Similar bottlenecks plague the Netherlands and Italy, where transmission upgrades lag generation growth. A 10% curtailment rate can shave 150 basis points off project IRR, discouraging near-term procurement. Developers respond by co-locating batteries, which favors hybrid inverters, yet connection uncertainty tempers the overall European solar inverters market expansion in congested regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Inverter Type: Central Dominance Meets Microinverter Momentum

Central units controlled 48.6% of 2025 revenue, riding Spain’s and Portugal’s utility pipelines where single 1-5 MW blocks minimize balance-of-system expense. String designs, at roughly 35% share, gained in commercial rooftops and terrain-complex solar fields that need finer MPPT granularity. Hybrid variants lifted their slice amid rising prosumer storage demand. Microinverters held just under 10% but will outpace all others at a 7.3% CAGR through 2031 as rooftops in Germany and the Netherlands favor module-level optimization.

Regulation magnifies differentiation. Grid-forming mandates above 1 MW threaten legacy central designs that lack virtual-synchronous capability, steering developers toward compliant string products or next-generation central architectures. Microinverters remain exempt due to small unit size, yet benefit from heightened safety codes that require rapid shutdown and arc-fault detection. Consequently, the European solar inverters market rewards suppliers able to juggle cost-competitive central units and premium micro or hybrid lines with advanced firmware.

By Phase: Three-Phase Supremacy with Single-Phase Upswing

Three-phase equipment represented 73.4% of revenue in 2025, omnipresent in C&I rooftops and utility arrays where balanced load flow is mandatory. Modular 20-100 kW three-phase strings allow factories to scale generation without oversizing. Single-phase devices, linked to systems below 10 kW, are set for a 6.4% CAGR in line with residential growth. Italy’s 5.3 GW 2024 rooftop tally underlines single-phase momentum.

Compliance drives product roadmaps: national codes such as VDE-AR-N 4105 require firmware updates that smaller suppliers sometimes lag. Hybrid single-phase inverters with battery ports and blackout protection strengthen supplier lock-in at the household level, adding stickiness to the European solar inverters market.

By Connection Type: On-Grid Core, Off-Grid Niche Widens

On-grid products covered 80.7% of 2025 sales, reflecting mature European grids and export-oriented PPA models. Yet off-grid solutions will rise at a 7.7% CAGR through 2031, catalyzed by island communities in Italy and Greece replacing diesel generation. Victron and SMA lead with inverter-chargers that handle load surges and generator sync.

Hybrid units blur boundaries, enabling on-grid households to island during outages and to maximize self-use when net metering fades. The distinction between on- and off-grid therefore softens, but both modes expand overall demand within the European solar inverters market size forecasts.

By Application: Utility-Scale Leads, Residential Races Ahead

Utility-scale systems held 59.1% of 2025 demand, supported by Iberian PPAs and Greece’s tender schedule. These plants favor high-capacity three-phase blocks for their lower LCOE. Residential demand, however, is set to expand at a 6.8% CAGR as retail tariffs stay high and permitting accelerates under Council Regulation 2022/2577. Single-phase hybrid inverters dominate this segment, boosting attach rates for batteries and EV chargers.

Commercial and industrial rooftops, roughly 25-30% share, grow more slowly because lower business tariffs stretch payback periods. Yet demand-charge management and ESG targets keep this slice relevant, especially where dynamic tariffs reward peak shaving. Overall, application mix shifts gradually but meaningfully, keeping the European solar inverters market diversified across value pools.

Geography Analysis

Germany retained a 25.5% share in 2025 on the back of 14.6 GW additions and cumulative 95 GW installed, yet faces 40 GW in connection queues and rising curtailment. Stringent VDE codes and cybersecurity scrutiny favor domestic champions with deep engineering support. Italy is forecast to post an 11.1% CAGR, the fastest across the bloc, helped by Decreto Semplificazioni’s six-month permitting cap and a 3.5 GW FER-X auction in 2024. Rooftop, agrivoltaic, and hybrid projects diversify demand beyond utility-scale plants, tilting purchasing toward flexible string and hybrid designs.

Spain and Portugal together accounted for about 18-20% in 2025, propelled by a 62 GW Spanish pipeline and Portugal’s successive auctions. High-irradiance sites coupled with merchant-heavy PPAs keep cost discipline front and center, opening doors for value-priced Chinese central inverters. France, the UK, and the Netherlands made up 15-17%; France’s PPE aims for 40 GW by 2028, the UK targets 50 GW by 2030, while the Dutch net-metering sunset accelerated battery-ready sales. Scandinavia and Eastern Europe combined supplied the remaining share, ripe for suppliers able to tailor products to cold climates and nascent codes. Overall geographic fragmentation mandates localized go-to-market strategies across the European solar inverters market.

Competitive Landscape

The top five suppliers, SMA Solar, Huawei, Sungrow, SolarEdge, and FIMER, controlled about 55-60% in 2025, reflecting moderate concentration. SMA kept leadership through grid-forming central units and strong O&M services. Huawei and Sungrow climbed on aggressive pricing, in-house device manufacture, and AI-enabled monitoring platforms. SolarEdge dominated rooftops via DC-optimized architectures, although its 2024 restructuring hinted at margin strain. FIMER re-entered contention after its 2025 recapitalization.

Vertical integration and software differentiation surfaced as key strategies. Huawei and Sungrow invested in SiC fabs to secure chips, while SMA and Fronius bought software firms to add tariff optimization and EV-charging orchestration. Off-grid niches saw Victron and Schneider Electric winning telco towers and island microgrids due to inverter-charger expertise.

Emergent disruptors include Enphase, whose IQ8 microinverter gained IEC 62109 certification for grid-forming operation, and GoodWe, which opened a Rotterdam service hub to cut warranty lead times. The market thus bifurcates into a low-cost tier and a premium grid-services tier, a split likely to widen as ENTSO-E codes tighten. The European solar inverters market, therefore, rewards continual firmware evolution and local service depth just as much as hardware cost.

Europe Solar Inverter Industry Leaders

FIMER SpA

SMA Solar Technology AG

Huawei Technologies

Sungrow Power Supply

SolarEdge Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Schneider Electric bought 25% of Energy Team to augment its EcoStruxure platform with dynamic tariff response.

- November 2025: ENTSO-E issued Phase II grid-forming guidelines, binding for projects above 1 MW from 2026.

- May 2025: Huawei rolled out FusionSolar 5.0 with AI yield forecasting for Spain, Italy, and Germany.

- January 2025: McLaren Applied and Greybull Capital completed the acquisition of FIMER, injecting EUR 50 million to restart Italian production.

Europe Solar Inverter Market Report Scope

A solar PV inverter is a power inverter that converts electricity in direct current (DC) output from a photovoltaic (PV) solar panel into alternating current (AC) at utility frequency. This can be fed into use for commercial electrical grids or used by a local off-grid electrical network, such as micro-grids or nano-grids. The inverter system is critical for the balance of system components in a photovoltaic system, allowing the use of ordinary AC-powered equipment. Solar power inverters have special functions adapted for use with photovoltaic arrays, including maximum power point tracking and anti-islanding protection.

The European solar inverters market is segmented by inverter type, phase, connection type, application, and geography. By inverter type, the market is segmented into central inverters, string inverters, and micro-inverters. By phase, the market is segmented into single-phase and three-phase. By connection type, the market is divided into on-grid and off-grid. By application, the market is segmented into residential, commercial and industrial, and utility-scale. The report also covers the market size and forecasts for the European solar inverter market across major countries in the region. The report offers the market size in value terms in USD for all the abovementioned segments.

By Inverter Type

| Central Inverters |

| String Inverters |

| Microinverters |

| Hybrid/Battery-Ready Inverters |

By Phase

| Single-Phase |

| Three-Phase |

By Connection Type

| On-Grid |

| Off-Grid |

By Application

| Residential |

| Commercial and Industrial |

| Utility-Scale |

Geography

| Germany |

| United Kingdom |

| Spain |

| Italy |

| France |

| NORDIC Countries |

| Netherlands |

| Russia |

| Rest of Europe |

| By Inverter Type | Central Inverters |

| String Inverters | |

| Microinverters | |

| Hybrid/Battery-Ready Inverters | |

| By Phase | Single-Phase |

| Three-Phase | |

| By Connection Type | On-Grid |

| Off-Grid | |

| By Application | Residential |

| Commercial and Industrial | |

| Utility-Scale | |

| Geography | Germany |

| United Kingdom | |

| Spain | |

| Italy | |

| France | |

| NORDIC Countries | |

| Netherlands | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the Europe solar inverters market be by 2031?

The market is projected to reach USD 4.18 billion by 2031 on a 6.01% CAGR.

Which inverter type is growing fastest across Europe?

Microinverters are expected to rise at a 7.3% CAGR through 2031, led by rooftop installations in high-price electricity markets.

Why are grid-forming capabilities becoming mandatory?

ENTSO-E's 2026 code update requires large projects to supply synthetic inertia and voltage support to stabilize frequency as fossil generators retire.

Which country offers the highest growth potential to 2031?

Italy shows the fastest outlook, with an 11.1% CAGR driven by streamlined permitting and aggressive FER-X auctions.

How are semiconductor shortages influencing inverter prices?

Limited IGBT and SiC MOSFET supply lengthens lead times and sustains an 8-12% cost premium for grid-forming models, partly offsetting broader price declines.

What role do hybrid inverters play in residential adoption?

Hybrid units enable battery integration and self-consumption during net-metering phase-outs, making them the default choice in Germany and the Netherlands.

Page last updated on: