Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

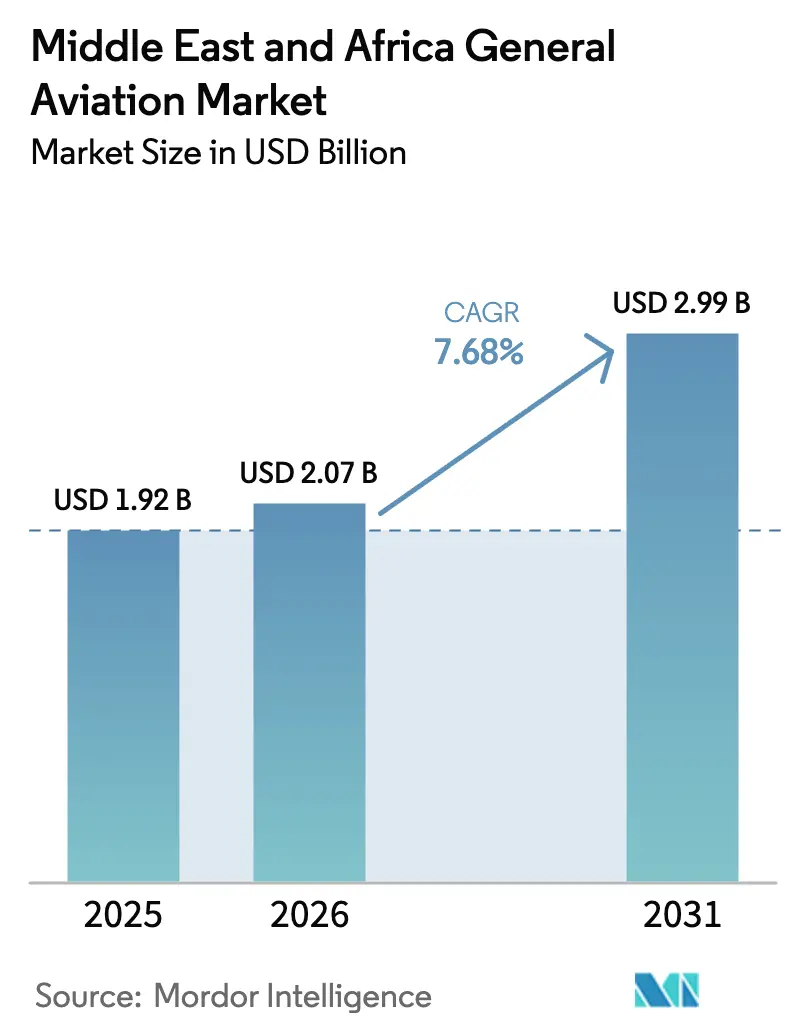

| Base Year Market Size (2025) | USD 1.92 Billion |

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 2.99 Billion |

| Growth Rate (2026 - 2031) | 7.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa General Aviation Market Analysis by Mordor Intelligence

The Middle East and Africa general aviation market size was valued at USD 1.92 billion in 2025 and estimated to grow from USD 2.07 billion in 2026 to reach USD 2.99 billion by 2031, at a CAGR of 7.68% during the forecast period (2026-2031). The expansion of the Middle East and Africa general aviation market reflects capital inflows from sovereign wealth funds, accelerated corporate diversification, and a continuing uptick in ultra-high-net-worth individual (UHNWI) populations across the Gulf. Airport upgrades in Dubai, Abu Dhabi, and Riyadh shorten turnaround times, while harmonized permitting frameworks cut paperwork and facilitate cross-border operations. The rising demand for emergency medical flights, combined with early-stage urban air mobility pilots, presents new growth opportunities. Electrification roadmaps, advanced air mobility (AAM) prototypes, and sustainable aviation fuel (SAF) mandates further underpin the long-term outlook of the Middle East and Africa general aviation market.

Key Report Takeaways

- By aircraft type, business jets led with a 39.02% revenue share in 2025; eVTOL and advanced air mobility vehicles are forecasted to expand at a 6.74% CAGR through 2031.

- By propulsion type, conventional piston and turbine systems held 80.55% of the Middle East and Africa general aviation market share in 2025, while all-electric platforms were projected to register the highest CAGR at 7.11% through 2031.

- By ownership model, full private ownership accounted for 44.67% of the Middle East and Africa general aviation market size in 2025; charter and air-taxi operators are expected to record the fastest CAGR at 6.05% through 2031.

- By end-user application, business and corporate transport accounted for 43.88% of the Middle East and Africa general aviation market size in 2025, whereas emergency medical and air-ambulance services are projected to advance at a 8.97% CAGR through 2031.

- By geography, the United Arab Emirates held 44.72% revenue share in 2025; Saudi Arabia is poised for the highest growth with a 9.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa General Aviation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in UHNWIs and corporate wealth creation | +3.8% | Gulf states core, spillover to Egypt and South Africa | Medium term (2-4 years) |

| Gulf infrastructure spending (airports, FBOs) | +2.8% | UAE, Saudi Arabia, Qatar primary focus | Long term (≥ 4 years) |

| Regulatory easing (e.g., Saudi annual permits) | +1.6% | Saudi Arabia national, regional influence across GCC | Short term (≤ 2 years) |

| Electrification roadmaps and eVTOL pilots | +2.9% | UAE and Saudi Arabia leading, gradual MEA expansion | Long term (≥ 4 years) |

| Fractional ownership platforms scaling | +0.9% | Regional across major MEA cities | Medium term (2-4 years) |

| Carbon-cost arbitrage via green-fuel hubs | +0.6% | UAE and Saudi Arabia hub development | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in UHNWIs and Corporate Wealth Creation

Gulf UHNWIs rose 18% in 2024, adding 599 individuals in the UAE and Saudi Arabia combined, which directly supported new aircraft acquisitions and higher charter utilization.[1]Public Investment Fund, “Annual Review 2024,” pif.gov.sa Rising technology, renewable energy, and financial services earnings amplify private aviation budgets, with sovereign wealth funds channeling USD 15.2 billion into aviation projects in 2024. Each incremental UHNWI contributed roughly 0.3 additional business-jet flight hours, thereby sustaining demand for large-cabin aircraft capable of flying nonstop from the Gulf to Europe or Asia. Family offices are increasingly viewing aircraft as core infrastructure, thereby bolstering the Middle East and Africa general aviation market. Persistent wealth formation underpins long-cycle fleet planning and secures residual values for pre-owned jets.

Gulf Infrastructure Spending (Airports, FBOs)

The UAE committed USD 8.7 billion to aviation facilities in 2024, while Saudi Arabia earmarked USD 12.3 billion for airport modernization.[2]Dubai Airports, “Annual Report 2024,” dubaiairports.ae Dedicated general-aviation terminals in Dubai now handle 60% more movements, and new FBO capacity in Abu Dhabi accommodates 45 simultaneous business jets. Jetex launched four additional regional bases, enhancing ground handling quality and reducing the average turnaround by 23 minutes. Such upgrades strengthen the hub status of Dubai and Abu Dhabi, capturing transit flights and positioning the Middle East and Africa general aviation market for sustained network growth. Improved infrastructure also supports maintenance reliability, elevating safety and service benchmarks.

Regulatory Easing for Private Operators

Saudi reforms reduced permit approval from 45 days to 12 days and introduced annual blanket authorizations, resulting in a 35% reduction in administrative costs.[3]General Authority of Civil Aviation Saudi Arabia, “Statistics 2024,” gaca.gov.sa Private aircraft movements in Saudi Arabia increased by 47% in 2024, with parallel digital portals in the UAE facilitating same-day approvals. Harmonized GCC rules reduce compliance duplication, lowering entry barriers for fractional ownership and charter firms. Simplified procedures expand route flexibility, fostering broader regional connectivity that underpins the general aviation market in the Middle East and Africa. Shorter lead times also support time-sensitive missions such as air ambulance flights.

Electrification Roadmaps and eVTOL Pilots

The UAE enacted the world’s first city-pair eVTOL framework in 2024, authorizing commercial routes between Dubai and Abu Dhabi, while Saudi Arabia piloted autonomous flights during the Hajj.[4]UAE General Civil Aviation Authority, “Digital Reforms 2024,” gcaa.gov.ae Joby Aviation and Archer Aviation secured conditional permits, and 12 vertiports worth USD 340 million received approval across the Emirates. Government research grants and NEOM’s USD 1.2 billion mobility fund spur R&D for electric air vehicles, fueling the AAM ecosystem. Certification pathways aligned to EASA standards give manufacturers confidence to invest, pushing the Middle East and Africa general aviation market toward next-generation propulsion. Early adoption cements the region as a live testbed for global eVTOL rollouts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geopolitical flashpoints and airspace closures | -1.7% | Regional across Middle East, limited Africa impact | Short term (≤ 2 years) |

| Pilot and MRO skill shortages | -1.3% | Global across MEA region | Medium term (2-4 years) |

| AvGas supply-chain fragility | -0.8% | Africa primary impact, Gulf states secondary | Medium term (2-4 years) |

| Vertiport capital intensity for AAM | -0.6% | UAE and Saudi Arabia concentrated | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Geopolitical Flashpoints and Airspace Closures

Red Sea tensions led to 23% of regional business-aviation routes adopting detours, which added 2.3 flight hours per sector in 2024. Intermittent Iran-Israel restrictions disrupted 15 key corridors, resulting in USD 47 million in increased operator fuel bills. Sudan’s conflict removed a critical refueling waypoint, adding 12% to the cost of Gulf-to-South Africa missions. Insurance premiums increased by 35% in designated high-risk zones, prompting some charter firms to suspend their services entirely. Such volatility erodes schedule reliability, compresses margins, and dampens near-term growth for the Middle East and Africa general aviation market.

Pilot and MRO Skill Shortages

Regional operators lacked 2,847 qualified pilots in 2024, with demand projected to exceed 4,200 by 2030. Training schools graduate only 1,200 pilots annually, while 67% of maintenance facilities operate at or below capacity due to technician shortages. Emirates Flight Training Academy expanded its seats by 40% and Saudi entities invested USD 280 million in new centers; yet, a multi-year lag persists before graduates reach line readiness. Salary inflation of 15% per annum raises operating costs, and business-jet operators offer 25% premiums over airlines to secure crews. Persistent shortages temper fleet utilization and moderate growth outlooks in the Middle East and Africa general aviation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Business Jets Dominate While eVTOL Emerges

Business jets controlled 39.02% of the Middle East and Africa general aviation market in 2025 after Gulfstream delivered 47 and Bombardier 31 large-cabin units during the year. Volume gains stem from wealth management, corporate diversification, and family office travel patterns linking the Gulf with Europe, Asia, and Africa. Large-cabin jets capture the lion’s share owing to nonstop range and cabin comfort, while mid-size platforms draw demand from emerging corporates. Light jets thrive in charter and fractional schemes, benefiting from lower capital outlays and high dispatch rates. Turboprop fixed-wing aircraft retain relevance for sub-regional hops and African runways where pavement strength is limited. eVTOL craft, although nascent, registers a 6.74% CAGR, propelled by supportive regulations and city-pair pilot programs. Their capacity to bypass congested surface links positions them as an urban-connectivity solution that widens the addressable customer base for the Middle East and Africa general aviation market.

The second-tier rotorcraft segment enjoys robust demand for medical evacuation and offshore energy services. The Helicopter Company has grown its fleet by in market share 35% and now supports both emergency response and corporate shuttle missions. Piston fixed-wing models continue to serve flight-training schools and leisure flyers, even as elevated AvGas prices hold growth in check. EASA certification harmonization, coupled with improved supply-chain visibility, sustains aftermarket parts availability and keeps older piston platforms serviceable. Over the forecast period, eVTOL adoption is expected to accelerate once vertiport networks mature, leading to a gradual shift here toward electric platforms in the Middle East and Africa general aviation market.

By Propulsion Type: Conventional Dominance with Electric Transition

Conventional piston and turbine engines accounted for 80.55% of the Middle East and Africa general aviation market share in 2025, leveraging decades of reliability and robust support ecosystems. Turbines power the business-jet fleet, supplying the range, climb rates, and cabin pressurization required for intercontinental usage. Piston engines underpin entry-level trainers and recreational aircraft, where operating cost sensitivity dictates purchasing decisions. Existing MRO capacity, spare parts pipelines, and technician expertise reinforce the incumbency of conventional power plants. However, parts scarcity in select African nations pushes operators to stock inventories or ferry aircraft to Gulf centers.

All-electric programs are experiencing the fastest growth at a 7.11% CAGR, buoyed by eVTOL prototypes and sustainability mandates, such as the UAE’s 5% SAF blend requirement by 2026. Hybrid-electric concepts aim to bridge range limitations, offering step-wise reductions in fuel consumption without the certification hurdles associated with pure-battery designs. NEOM’s USD 1.2 billion fund catalyzes R&D in high-density batteries and lightweight materials. As vertiport grids emerge, electric propulsion will transition from demonstration flights to scheduled operations, chipping away at conventional engine dominance within the Middle East and Africa general aviation market.

By Ownership Model: Private Ownership Leads Charter Growth

Full private ownership commanded a 44.67% revenue share in 2025, mirroring the concentrated wealth profiles and privacy needs of Gulf UHNWIs. Ownership assures schedule control, confidentiality, and asset appreciation within balanced-portfolio strategies. Corporate entities deploy aircraft to synchronize far-flung projects, noting 23% productivity gains over commercial itineraries. Nonetheless, high capital costs spur emerging affluent travelers toward charter and air-taxi solutions, now the fastest-growing category, with a 6.05% CAGR. Operators expand fleets and digital booking tools that democratize access while sidestepping depreciation risks.

Fractional ownership scales rapidly, with NetJets adding 23 jets to its Middle East block-time program, signaling broader acceptance of shared-title models. Training academies raised fleet counts by 28% in response to pilot shortages, playing a dual role as capacity builders and aircraft buyers. Governments maintain fleets for border patrol, survey, and humanitarian roles, contributing to stable demand across light utility aircraft. The diversification of ownership models enlarges customer pools and stabilizes revenue cycles for the Middle East and Africa general aviation market.

By End-User Application: Corporate Transport Anchors Emergency Medical Growth

Business and corporate transport applications accounted for 43.88% of the Middle East and Africa general aviation market in 2025, serving as the logistical backbone of cross-border commerce and investment flows. Firms spanning energy, finance, and technology rely on private aircraft to bridge distance, citing 23% productivity gains relative to scheduled airlines. Luxury tourism and second-home ownership also fuel personal and leisure flying, particularly on high-density routes such as Dubai-Maldives and Riyadh-Mykonos.

Emergency medical and air-ambulance operations post the highest growth at 8.97% CAGR, underscored by The Helicopter Company’s 3,500 lifesaving missions and 94% critical-case survival rate in 2024. Gulf governments allocate significant resources to healthcare spending on airborne trauma care and organ transport capabilities. Special-mission segments, such as intelligence and border surveillance, expanded by 31%, spurred by heightened security requirements in North and Central Africa. Flight-training applications benefit from record student enrolments, mitigating pilot shortages and adding a steady revenue layer to the Middle East and Africa general aviation market.

Geography Analysis

The United Arab Emirates retained a 44.72% leadership position in 2025, thanks to integrated airport ecosystems, permissive regulations, and business-friendly tax regimes. Dubai’s Al Maktoum International now handles 180 business-jet movements daily after Phase 2 expansion, while Abu Dhabi’s Zayed International offers luxury service lounges run by Jetex and ExecuJet. Same-day permit processing and streamlined customs flow help operators minimize ground time, reinforcing the UAE’s gateway status for the Middle East and Africa general aviation market.

Saudi Arabia, forecast to grow at a 9.02% CAGR, is accelerating fleet ex, expansionpansion to 847 business jets by 2024 under its USD 64 billion Vision 2030 aviation plan. The kingdom’s blanket-permit regime and digitized clearance cut administrative overhead and encouraged foreign registrants to base aircraft locally. NEOM’s AAM sandboxes entice tech investors and create pilot corridors for electric airframes, positioning Saudi Arabia as a future innovation nucleus within the Middle East and Africa general aviation market.

Secondary growth pockets arise in Qatar, Egypt, Algeria, and South Africa. Qatar experiences event-driven traffic surges, with a 67% spike during major sports tournaments. Egypt’s geographic junction supports transit flights between three continents, though secondary-city airports require modernization. South Africa leverages mature MRO and pilot-training ecosystems yet faces currency and economic headwinds. Algeria channels hydrocarbon revenues into executive transport while revising aviation codes to attract overseas operators. Collectively, these markets broaden the opportunity canvas for stakeholders in the Middle East and Africa general aviation market.

Competitive Landscape

Market concentration is moderate, led by Gulfstream, Bombardier, and Dassault, each boasting strong product-support hubs in Dubai and Riyadh. Gulfstream's deliveries to its regional customers in 2024 underscore sustained appetite for large-cabin jets, while Bombardier's new service center in Riyadh reduces maintenance ferry costs. Competitive edges revolve around dispatch reliability, cabin technology, and assurances of resale value, rather than headline price cuts, aligning with the quality-focused ethos of the Middle East and Africa general aviation market.

Disruptors such as Joby Aviation and Archer Aviation ride the eVTOL wave, winning early certification clearances that sidestep traditional airframe incumbents. Their partnerships with GCC regulators fast-track flight-test envelopes and enhance investor confidence. Maintenance providers like Jetex and ExecuJet expand their footprints to capture the aftermarket, investing in predictive analytics platforms that reduce unscheduled downtime by 18%. African white-space regions, where runway conditions and MRO support lag, offer entry points for OEMs and service firms willing to co-invest in infrastructure, further diversifying the Middle East and Africa's general aviation market ecosystem.

Over the next half-decade, it is expected that tension will intensify within service networks, training academies, and leasing companies as they seek to bundle aircraft, pilots, and maintenance into one-stop solutions. Technology deployments, ranging from satellite communications-enabled flight planning to AI-based health-monitoring systems, will serve as key differentiators. Firms able to orchestrate end-to-end value chains stand to increase their wallet share and consolidate their presence across the Middle East and Africa general aviation market.

Middle East And Africa General Aviation Industry Leaders

General Dynamics Corporation (Gulfstream)

Bombardier Inc.

Textron Inc.

Dassault Aviation

Embraer S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: EHang Holdings Limited has achieved a significant milestone in Africa by successfully completing the continent's first-ever pilotless human-carrying flight with its EH216-S. This accomplishment establishes EHang as the pioneer of pilotless electric vertical take-off and landing (eVTOL) aircraft operations in Africa.

- September 2025: Malta-based VistaJet is set to become the first foreign private jet operator authorized to operate domestic routes in Saudi Arabia. This development follows the lifting of cabotage restrictions by regulators, marking a step toward the liberalization of the Kingdom's airspace.

- October 2023: Textron Aviation announced that it has entered into a purchase agreement with Fly Alliance for up to 20 Cessna Citation business jets, along with options for four firms to purchase 16 additional aircraft.

Middle East And Africa General Aviation Market Report Scope

Business Jets, Piston Fixed-Wing Aircraft, Others are covered as segments by Sub Aircraft Type. Algeria, Egypt, Qatar, Saudi Arabia, South Africa, United Arab Emirates are covered as segments by Country.By Aircraft Type

| Business Jets | Large Jet |

| Mid-Size Jet | |

| Light/Very-Light Jet | |

| Turboprop Fixed-Wing | |

| Piston Fixed-Wing | |

| Rotorcraft | |

| eVTOL/Advanced Air Mobility Vehicle |

By Propulsion Type

| Conventional Piston/Turbine |

| Hybrid-Electric |

| All-Electric |

By Ownership Model

| Full Private Ownership |

| Fractional Ownership |

| Charter/Air-Taxi Operators |

| Training and Academic Institutions |

| Government and Special-Mission Operators |

By End-User Application

| Business/Corporate Transport |

| Personal and Leisure Flying |

| Special Mission (ISR, Surveillance, Law-Enforcement) |

| Emergency Medical/Air-Ambulance |

| Pilot Training |

By Geography

| Algeria |

| Egypt |

| Qatar |

| Saudi Arabia |

| South Africa |

| United Arab Emirates |

| Rest of Middle East and Africa |

| By Aircraft Type | Business Jets | Large Jet |

| Mid-Size Jet | ||

| Light/Very-Light Jet | ||

| Turboprop Fixed-Wing | ||

| Piston Fixed-Wing | ||

| Rotorcraft | ||

| eVTOL/Advanced Air Mobility Vehicle | ||

| By Propulsion Type | Conventional Piston/Turbine | |

| Hybrid-Electric | ||

| All-Electric | ||

| By Ownership Model | Full Private Ownership | |

| Fractional Ownership | ||

| Charter/Air-Taxi Operators | ||

| Training and Academic Institutions | ||

| Government and Special-Mission Operators | ||

| By End-User Application | Business/Corporate Transport | |

| Personal and Leisure Flying | ||

| Special Mission (ISR, Surveillance, Law-Enforcement) | ||

| Emergency Medical/Air-Ambulance | ||

| Pilot Training | ||

| By Geography | Algeria | |

| Egypt | ||

| Qatar | ||

| Saudi Arabia | ||

| South Africa | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa |

Market Definition

- Aircraft Type - General Aviation includes aircraft used for corporate aviation, business aviation and other aerial works.

- Sub-Aircraft Type - Business Jets, Piston Fixed-Wing Aircraft, and helicopters and turboprop aircraft are taken into consideration.

- Body Type - Light Jets, Mid-Size Jets, and Large Jets according to their ability to carry passengers and flying distance ranges have been included under this study.

| Keyword | Definition |

|---|---|

| IATA | IATA stands for the International Air Transport Association, a trade organization composed of airlines around the world that has an influence over the commercial aspects of flight. |

| ICAO | ICAO stands for International Civil Aviation Organization, a specialized agency of the United Nations that supports aviation and navigation around the globe. |

| Air Operator Certificate (AOC) | A certificate granted by a National Aviation Authority permitting the conduct of commercial flying activities. |

| Certificate Of Airworthiness (CoA) | A Certificate Of Airworthiness (CoA) is issued for an aircraft by the civil aviation authority in the state in which the aircraft is registered. |

| Gross Domestic Product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| RPK (Revenue Passenger Kilometres) | The RPK of an airline is the sum of the products obtained by multiplying the number of revenue passengers carried on each flight stage by the stage distance - it is the total number of kilometers traveled by all revenue passengers. |

| Load Factor | The load factor is a metric used in the airline industry that measures the percentage of available seating capacity that has been filled with passengers. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| International Transportation Safety Association (ITSA) | International Transportation Safety Association (ITSA) is an international network of heads of independent safety investigation authorities (SIA). |

| Available Seats Kilometre (ASK) | This metric is calculated by multiplying Available Seats (AS) in one flight, defined above, multiplied by the distance flown. |

| Gross Weight | The fully-loaded weight of an aircraft, also known as “takeoff weight,” which includes the combined weight of passengers, cargo, and fuel. |

| Airworthiness | The ability of an aircraft, or other airborne equipment or system, to operate in flight and on the ground without significant hazard to aircrew, ground crew, passengers or to other third parties. |

| Airworthiness Standards | Detailed and comprehensive design and safety criteria applicable to the category of aeronautical product (aircraft, engine or propeller). |

| Fixed Base Operator (FBO) | A business or organization that operates at an airport. An FBO provides aircraft operating services like maintenance, fueling, flight training, charter services, hangaring, and parking. |

| High Net worth Individuals (HNWIs) | High Net worth Individuals (HNWIs) are individuals with over USD 1 million in liquid financial assets. |

| Ultra High Net worth Individuals (UHNWIs) | Ultra High Net worth Individuals (UHNWIs) are individuals with over USD 30 million in liquid financial assets. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| EASA (European Aviation Safety Agency) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| Airborne Warning and Control System (AW&C) aircraft | Airborne Warning and Control System (AEW&C) aircraft is equipped with a powerful radar and on-board command and control center to direct the armed forces. |

| The North Atlantic Treaty Organization (NATO) | The North Atlantic Treaty Organization (NATO), also called the North Atlantic Alliance, is an intergovernmental military alliance between 30 member states – 28 European and two North American. |

| Joint Strike Fighter (JSF) | Joint Strike Fighter (JSF) is a development and acquisition program intended to replace a wide range of existing fighter, strike, and ground attack aircraft for the United States, the United Kingdom, Italy, Canada, Australia, the Netherlands, Denmark, Norway, and formerly Turkey. |

| Light Combat Aircraft (LCA) | A light combat aircraft (LCA) is a light, multirole jet/turboprop military aircraft, commonly derived from advanced trainer designs, designed for engaging in light combat. |

| Stockholm International Peace Research Institute (SIPRI) | Stockholm International Peace Research Institute (SIPRI) is an international institute that provides data, analysis, and recommendations for armed conflict, military expenditure, and arms trade as well as disarmament and arms control. |

| Maritime Patrol Aircraft (MPA) | A maritime patrol aircraft (MPA), also known as maritime reconnaissance aircraft is a fixed-wing aircraft designed to operate for long durations over water in maritime patrol roles, in particular, anti-submarine warfare (ASW), anti-ship warfare (AShW), and search and rescue (SAR). |

| Mach Number | The Mach number is defined as the ratio of true airspeed to the speed of sound at the altitude of a given aircraft. |

| Stealth Aircraft | Stealth is a Common term applied to low observable (LO) technology and doctrine, that makes an aircraft near invisible to radar, infrared or visual detection. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms