Microphone Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

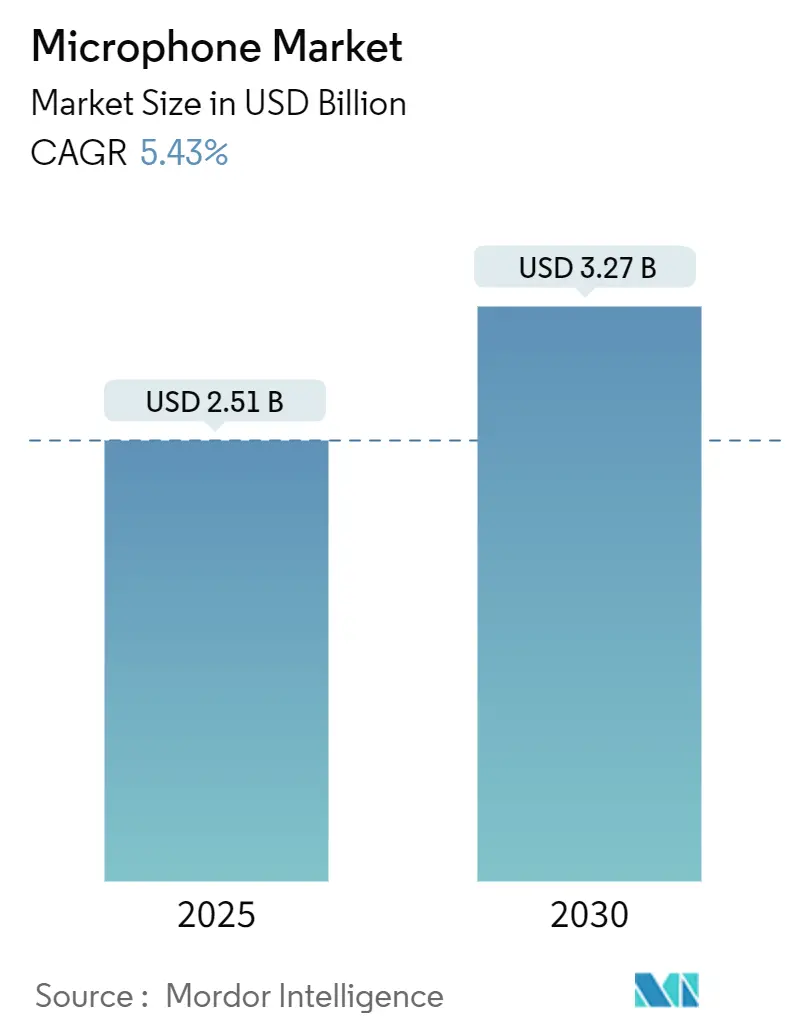

| Market Size (2025) | USD 2.51 Billion |

| Market Size (2030) | USD 3.27 Billion |

| Growth Rate (2025 - 2030) | 5.43% CAGR |

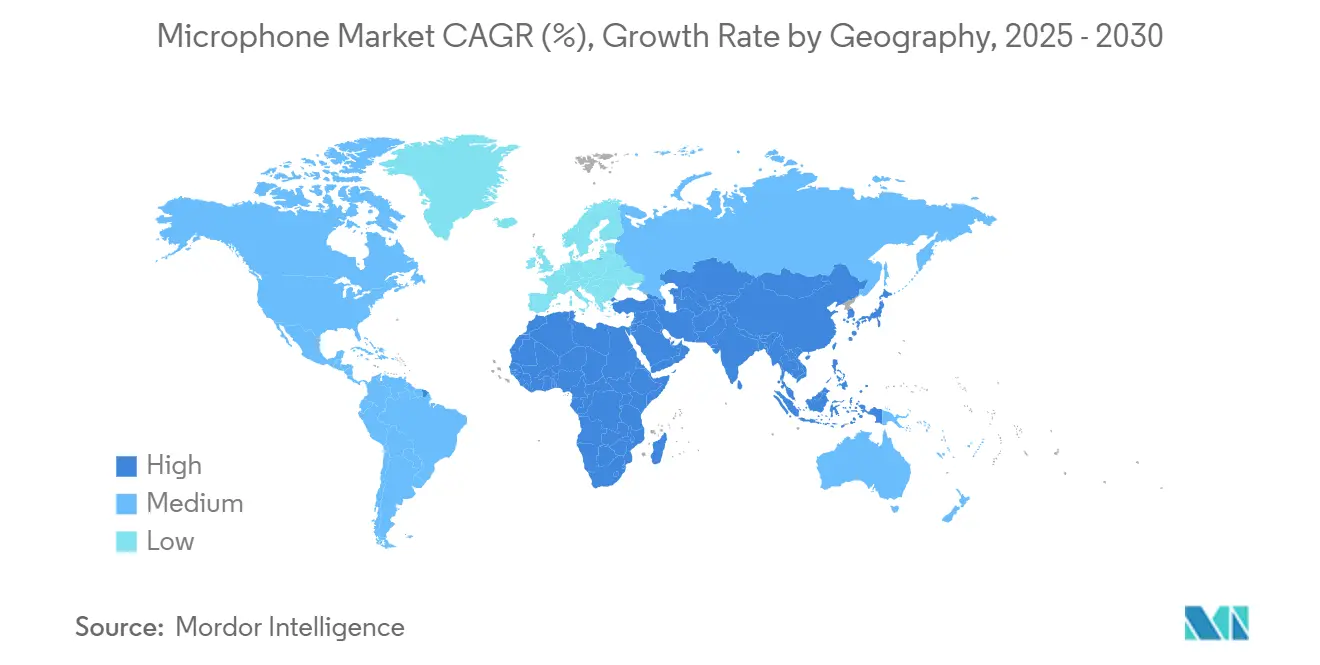

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Microphone Market Analysis by Mordor Intelligence

The global microphone market is revenue-positive in 2025, standing at USD 2.51 billion, and is forecast to advance to USD 3.27 billion by 2030 at a 5.43% CAGR. Growth rests on rising multi-mic deployments in smart devices, the shift to AI-enabled audio processing, and steady downstream demand from electric vehicles, unified-communications suites, and the expanding creator economy. Wireless architectures, beam-forming arrays, and environmental-sensing microphones are emerging as critical design focal points, while supply-chain investments worth USD 3.6 billion in 2024 indicate a sector preparing for sustained capacity expansion. Competitive advantage increasingly hinges on miniaturization, on-edge AI, and power efficiency, with MEMS platforms delivering the size, reliability, and digital-integration benefits required by modern OEMs. Regionally, the microphone market remains strongly anchored in Asia Pacific for manufacturing, but North America leads many innovation curves, especially in enterprise collaboration and content-creation toolkits.

Key Report Takeaways

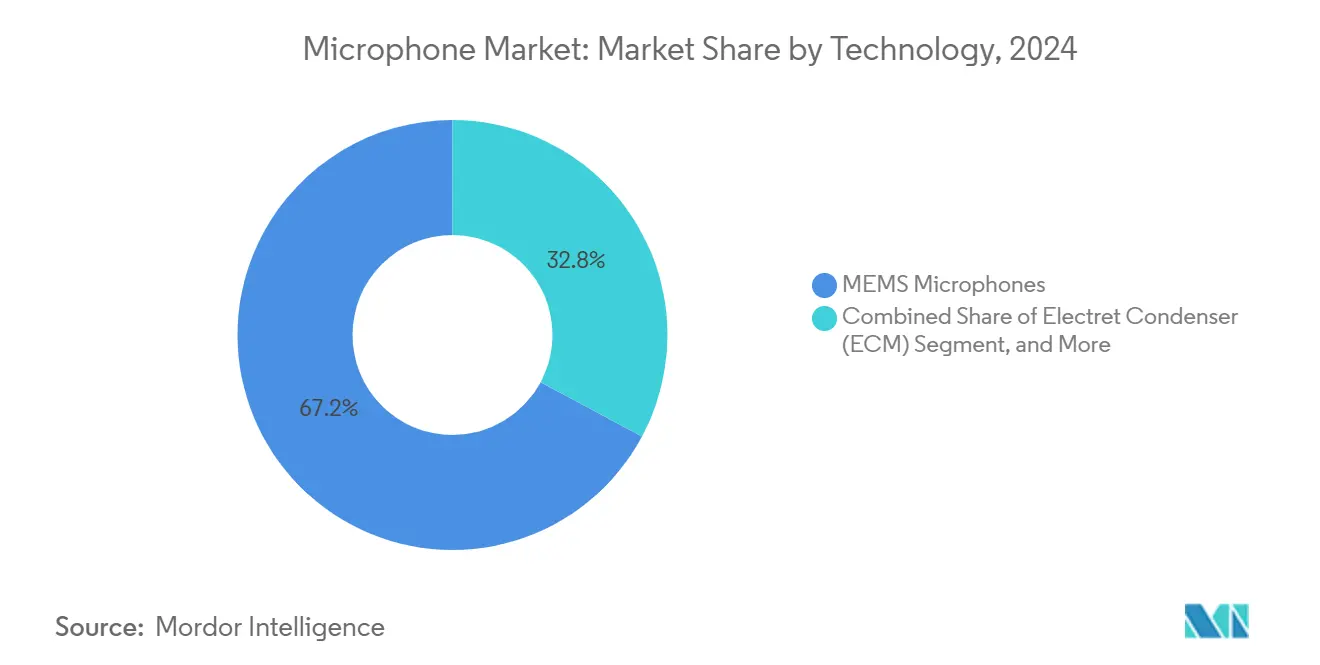

- By technology, MEMS microphones held 66.5% of microphone market share in 2024; digital MEMS is forecast to grow at a 5.6% CAGR through 2030.

- By product type, handheld units led with 35.2% revenue in 2024, while array and beam-forming modules are set to expand at 6.2% CAGR between 2025-2030.

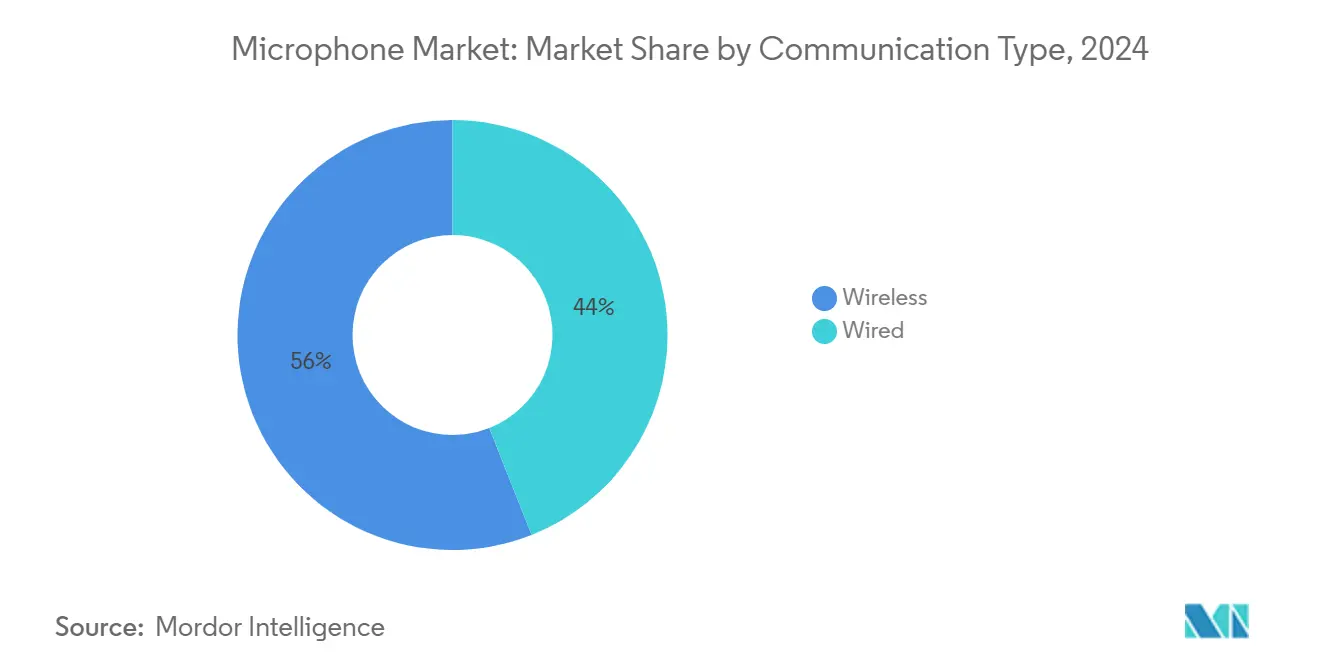

- By communication type, wireless solutions accounted for 56% of the microphone market size in 2024 and should rise at a 7.4% CAGR to 2030.

- By end-user vertical, consumer electronics commanded 42.1% of the microphone market size in 2024; automotive is projected to accelerate at 6.7% CAGR.

- By geography, Asia Pacific captured 38.4% of microphone market share in 2024, and the Middle East & Africa region is expected to post the fastest 8.1% CAGR to 2030.

Global Microphone Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of MEMS microphones in TWS | +1.2% | Asia Pacific, spillover to North America & Europe | Medium term (2-4 years) |

| Automotive OEM shift to in-cabin voice UX | +0.9% | Europe & North America, emerging adoption in China | Long term (≥4 years) |

| AI-enabled beam-forming arrays in enterprise | +0.8% | North America & Europe, growth in developed APAC | Medium term (2-4 years) |

| Content-creator demand for premium mics | +0.7% | North America, expansion to Europe & urban APAC | Short term (≤2 years) |

| Wireless spectrum re-farming mandates | +0.6% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Health-wearable acoustic biosensing | +0.5% | North America & Europe, growth in developed APAC | Long term (≥4 years) |

Source: Mordor Intelligence

Proliferation of MEMS microphones in true-wireless earbuds across Asia

True wireless stereo earbuds now embed two to four low-power MEMS transducers per bud, allowing richer ANC and ambient-sound passthrough. Asian OEMs dominate this design race by pairing wafer-level processing with ultra-compact housings, showcased by Xiaomi Buds 5 Pro and HMD’s Amped Buds, both released in 2025. The resulting volume uplift keeps the microphone market on a steep shipment trajectory and pushes fabs toward 200-mm wafers to rein in cost per unit. Component vendors are responding with neural-noise-cancellation chips drawing less than 150 µA, enabling day-long battery life without acoustic compromise. As regional champions scale, spillover demand for associated testing, packaging, and software services is reinforcing Asia’s primacy in the global supply web.[1]International Monetary Fund, “Transcript of Asia Pacific Department April 2024 Press Briefing,” imf.org

Automotive OEM shift to in-cabin voice UX for EV platforms

Quieter EV cabins allow microphone arrays to capture speech with far higher signal-to-noise ratios than legacy combustion architectures. Solutions such as Kardome Mobility’s 3-D spot-forming software turn a single roof-mounted array into a six-seat pickup grid, while Cerence extends voice control to exterior vehicle functions.[2]Kardome, “Revolutionizing In-Car Voice Interactions,” kardome.comBetween 2025 and 2031, in-car microphone units are expected to rise by over 15% as hands-free mandates and safety features become standard. OEM differentiation is now tied to latency-free natural-language interfaces as much as drivetrain efficiency. Suppliers that combine automotive-grade MEMS, high SPL tolerance, and over-the-air upgradability are securing long-term platform wins with European, North American, and Chinese automakers.

Rapid adoption of AI-enabled beam-forming arrays in enterprise UC equipment

Hybrid work has heightened expectations for boardroom acoustics. Ceiling tiles such as the ClearOne BMA 360 integrate ultra-wideband, frequency-invariant beamforming, while Panasonic’s 64-element array self-calibrates sensitivity to shifting seating layouts.[3][4]ClearOne, “BMA 360 Beamforming Ceiling Tile,” clearone.com Panasonic Connect, “Beamforming Ceiling Microphone Array,” panasonic.comAI-powered direction-of-arrival logic tracks voices and suppresses keystrokes or HVAC rumble, producing studio-grade clarity without complex DSP tuning. North American and European integrators now treat beam-forming as table stakes for new conferencing builds, which is boosting premium ASPs across the microphone market. As open-office concepts return in Asia’s tech hubs, similar demand patterns are emerging in Singapore, Seoul, and Tokyo.

Content-creator economy fueling premium handheld & USB mics

Global creator-platform payouts exceeded USD 38 billion in 2024, stoking appetite for broadcast-quality capture gear. Handheld cardioid models such as the Shure SM7dB or Elgato Wave:3 rank high on streamer wish-lists, while AI-assisted wireless kits like Saramonic Ultra merge low-latency 2.4 GHz transport with onboard voice enhancement. Chinese entrants now ship metal-body USB condensers retailing below USD 90 yet rivaling established brands on frequency response and self-noise. Such price/performance disruption is broadening access and funneling fresh talent into podcasting, e-sports commentary, and social-commerce demos, thereby widening the microphone market’s premium tier.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RF congestion in sub-1 GHz bands | -0.7% | North America & Europe, rising impact in urban APAC | Medium term (2-4 years) |

| Silicon substrate shortages | -0.6% | Global, highest pressure on APAC fabs | Short term (≤2 years) |

| Counterfeit after-market capsules | -0.4% | Asia Pacific, spillover to global markets | Medium term (2-4 years) |

| EU WEEE/RoHS compliance costs | -0.3% | Europe, potential expansion to North America & APAC | Long term (≥4 years) |

Source: Mordor Intelligence

RF congestion & interference risk in sub-1 GHz bands for wireless mics

Shrinking spectrum allotments have forced professional audio crews to squeeze dozens of channels into narrower blocks, elevating dropout risk during live events. The FCC’s green light for very-low-power devices across 6 GHz extends usable airspace but complicates coordination for hospitality venues already juggling Wi-Fi 6E deployments.[5]Federal Communications Commission, “Unlicensed Use of the 6 GHz Band: Third Report and Order,” fcc.govAdvanced filters, frequency-agile PLLs, and machine-learning coexistence schemes are mitigating the pain, yet rental houses still face rising equipment amortization and engineering costs when operating in dense metros.

BOM-cost inflation from silicon substrate shortages

Persistent wafer tightness, especially on 200-mm lines suited to MEMS monolithic processing, has inflated die cost by up to 30% since late-2023. Tier-one microphone vendors have partly offset the spike through long-term foundry contracts and alternate SOI sourcing, but smaller design houses are contending with allocation cuts and delayed tape-outs. The risk of price pass-through threatens to dampen adoption of multi-mic architectures in entry-level devices until capacity expansions in Taiwan, the United States, and Germany come fully online.

Segment Analysis

By Technology: MEMS microphones consolidate leadership through miniaturization insights

MEMS captured 66.5% of microphone market share in 2024 as their wafer-level assemblability slashed per-unit cost and enabled seamless pairing with on-edge DSP cores. This density advantage allows handset and earbud OEMs to embed three to five sensors per product without dimensional trade-offs. In revenue terms, the microphone market size attributed to MEMS platforms is projected to climb from USD 2.51 billion in 2025 to USD 6 billion by 2033. Digital MEMS, now shipping with built-in pulse-density modulation, is expanding at a 5.6% CAGR, buoyed by higher immunity to electromagnetic interference and straightforward routing into SoC audio hubs.

ECM technologies retain niche hold in price-sensitive conference endpoints and certain instrument-pickup roles, leveraging mature supply chains and a warm analog tonality cherished by audio purists. Dynamic capsules dominate high-SPL stage environments given their resilience, while ribbon units persist in boutique studio workflows where natural transient response is essential. Hybridization trends are nevertheless accelerating: OEMs increasingly pair MEMS for ANC feed-forward tasks with larger-diaphragm electrets for full-band capture, ensuring balanced frequency coverage in true-wireless buds and studio headsets.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Handheld designs command revenues as beam-forming arrays scale

Handheld transducers led 2024 unit sales with a 35.2% slice of the microphone market size thanks to broad utility in broadcast, stage, and field-recording scenarios. Weight-reduced alloys and improved shock-mount suspensions have refreshed the form factor without sacrificing ruggedness. Meanwhile, ceiling or bar-format beam-forming arrays are registering the fastest expansion at 6.2% CAGR through 2030; enterprises view them as the acoustic anchor of room-centric UC builds. The Ponte-tech RM702A array, for instance, leverages twin DSP cores to synthesize 360° pickup and AI noise gating, illustrating the trajectory toward integrated smart endpoints.

Head-worn and lavalier options remain staples for live theater and sports commentary, whereas gooseneck microphones preserve relevance at lecterns and conference dais due to directional control. Freestanding USB models ride the creator-economy boom, integrating multi-pattern capsules, hardware-level limiters, and latency-free monitor returns that once required external mixers. This specialization stratifies price tiers and allows vendors to tailor SKUs for discrete workflows, keeping innovation velocity high across the microphone market.

By Communication Type: Wireless connectivity sets the pace for refresh cycles

Wireless solutions owned 56% revenue share in 2024 as performers, educators, and corporate presenters prioritized mobility and uncluttered installations. Feature innovations span 24-bit digital modulation, 6 GHz VLP operation, and AI-driven frequency coordination that scans crowded airwaves in sub-second intervals. The microphone market size for wireless configurations is anticipated to double by 2032, underpinned by demand for hybrid event production and campus-wide audio distribution.

Wired models preserve footholds where absolute reliability and zero-latency performance outweigh cable management issues. Flagship conference systems such as the Yealink 2025 wired portfolio underscore that secure, power-over-Ethernet signal paths still meet stringent enterprise policies. A hybrid procurement strategy is now common: facilities deploy wired arrays for mission-critical rooms and complement them with portable wireless links for adaptable spaces, thereby balancing resilience with flexibility.

Note: Segment shares of all individual segments available upon report purchase

By End-User Vertical: Consumer electronics dominate while automotive surges

Smartphones, hearables, and voice-assisted smart-home hubs consumed 42.1% of microphone market size in 2024. Design evolution toward distributed mic clusters—often five per handset—underpins this dominance and sustains yearly upticks in silicon content per device. Automotive, however, delivers the steepest climb at 6.7% CAGR as EV makers weave ANC, voice assistants, and driver-monitoring features into cabin architectures. Infineon’s automotive-grade XENSIV IM68A130A MEMS sensor, qualified for -40 °C to 105 °C, exemplifies devices tailored for this stringent vertical.

Broadcast and media remain loyal to high dynamic-range transducers; corporate and education channels seek intelligibility improvements that cut virtual-meeting fatigue; and healthcare innovators exploit ultra-low-frequency microphones for biosignal analytics. Industrial players employ acoustic arrays for predictive maintenance, while environmental agencies deploy MEMS-based sound meters, such as Svantek’s SV 973, for continuous urban-noise mapping. Such cross-vertical proliferation keeps the microphone market resilient to single-sector demand swings

Geography Analysis

Asia Pacific led the microphone market in 2024 with a 38.4% revenue share and shipped more than 2.7 billion units from Chinese factories alone. Regional dominance is sustained by vertically integrated handset, notebook, and TWS earbud supply networks, with South Korean and Japanese firms pushing boundaries in wafer-level packaging and low-power DSP co-design. Government incentives for semiconductor fabs in mainland China, Taiwan, and Singapore seek to mitigate global substrate shortages and shore up future capacity.

North America ranks second by sales value, fueled by a large creator community, a mature live-events infrastructure, and early adoption of AI-centric audio solutions. Silicon Valley startups drive edge-AI firmware that elevates beam-forming performance, while established broadcast houses upgrade to 6 GHz-ready wireless systems ahead of major sports events. Regulatory actions by the FCC, including the 2025 extension of unlicensed VLP rights, continue to shape both product-roadmap timing and channel-restock cycles.

The Middle East & Africa cluster, though a smaller baseline, is forecast to expand at an 8.1% CAGR through 2030. Mega-events, film-production hubs in the Gulf, and rising podcast listenership underpin this growth. Sony’s 2025 Alta Mic 1 debut in Abu Dhabi, plus record footfalls at CABSAT and Integrate Middle East, demonstrate how global OEMs are courting regional distributors. Investments in 5G backbones and broadcast satellite uplinks further widen prospective deployment avenues for high-specification microphones.

Competitive Landscape

Market structure is moderately concentrated. Audio stalwarts such as Shure, Sennheiser, and Audio-Technica continue to leverage heritage acoustics know-how, while fab-centric players like Infineon, Knowles, and STMicroelectronics supply the MEMS die underpinning next-generation arrays. Infineon’s 43.5% unit share in MEMS microphones, coupled with deep automotive design wins, underscores the strategic premium on semiconductor IP. Shure’s 2025 launch schedule—including the MoveMic 88+ wireless kit—shows analog legends actively pivoting toward software-defined, mobile-first workflows.

Strategic moves reflect rising vertical integration. Infineon and Knowles co-locate back-end packaging with wafer fabs to secure substrate availability. Sennheiser expanded into corporate UC by embedding its ceiling array platform within Microsoft Teams Rooms certifications. Chinese value-price disruptors, showcased at NAB 2025, challenge incumbents on cost and time-to-market, accelerating product-feature cycles. Across the microphone market, AI firmware, low-power codec partitioning, and platform-agnostic SDKs now weigh as heavily as diaphragm material or mechanical tolerances in vendor selection.

White-space opportunities span acoustic biosensors, environmental noise intelligence, and smart-appliance feedback loops. Early entrants pairing MEMS arrays with on-device neural networks stand to capture patentable differentiation. Simultaneously, compliance with stricter EU eco-design directives is turning recyclability and repairability into competitive talking points—factors likely to impact procurement decisions, especially among publicly funded broadcasters.

Microphone Industry Leaders

-

Georg Neumann GmbH

-

Knowles Corporation

-

Robert Bosch GmbH

-

Omron Corporation

-

Audio-Technica Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sony Middle East and Africa introduced the Alta Mic 1 wireless microphone at an Abu Dhabi launch, reinforcing its commitment to region-specific pro-audio portfolios.

- April 2025: hure unveiled the MV7i smart mic and MoveMic 88+ wireless kit, both aimed at content creators needing portable, broadcast-grade capture.

- March 2025: PIMIC and ZillTek released the Clarity NC100 deep-neural-network ANC chip, drawing only 150 µA and designed for single-microphone wearables.

- February 2025: The FCC opened unlicensed very-low-power device operation across the entire 6 GHz band, altering spectrum-planning strategies for wireless microphone fleets.

Global Microphone Market Report Scope

A microphone is an input device that converts voice or other sound vibrations into an electrical signal and stores the sound in analog or digital form. Microphones are incorporated in almost all laptops, computers, and microphones.

The scope of the study focuses on the market analysis of microphones sold across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The report's scope encompasses market sizing and forecasts for segmentation by type, communication type, end-user vertical, and geography. The study further analyzes the impact of COVID-19 on the ecosystem.

| By Technology | MEMS Microphones | Analog MEMS | ||

| Digital MEMS | ||||

| Electret Condenser (ECM) | ||||

| Dynamic Microphones | ||||

| Ribbon Microphones | ||||

| By Product Type | Handheld | |||

| Head-worn | ||||

| Gooseneck | ||||

| Freestanding/USB | ||||

| Array and Beam-forming Modules | ||||

| By Communication Type | Wired | |||

| Wireless | ||||

| By End-user Vertical | Broadcasting and Media | |||

| Consumer Electronics | Smartphones | |||

| Hearables (TWS and Headphones) | ||||

| Smart Speakers and Home Devices | ||||

| Cameras and Gaming | ||||

| Corporate and Institutional | Enterprise/Conference | |||

| Education | ||||

| Live Performances and Events | ||||

| Automotive | In-vehicle Infotainment | |||

| ADAS and Voice Control | ||||

| Healthcare and Medical Devices | ||||

| Industrial and Environmental | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| South Korea | ||||

| India | ||||

| South East Asia | ||||

| Australia | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Rest of South America | ||||

| Middle East and Africa | Middle East | United Arab Emirates | ||

| Saudi Arabia | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Rest of Africa | ||||

| MEMS Microphones | Analog MEMS |

| Digital MEMS | |

| Electret Condenser (ECM) | |

| Dynamic Microphones | |

| Ribbon Microphones |

| Handheld |

| Head-worn |

| Gooseneck |

| Freestanding/USB |

| Array and Beam-forming Modules |

| Wired |

| Wireless |

| Broadcasting and Media | |

| Consumer Electronics | Smartphones |

| Hearables (TWS and Headphones) | |

| Smart Speakers and Home Devices | |

| Cameras and Gaming | |

| Corporate and Institutional | Enterprise/Conference |

| Education | |

| Live Performances and Events | |

| Automotive | In-vehicle Infotainment |

| ADAS and Voice Control | |

| Healthcare and Medical Devices | |

| Industrial and Environmental |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| South East Asia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the microphone market?

The microphone market size stands at USD 2.51 billion in 2025 and is on track to reach USD 3.27 billion by 2030, reflecting a 5.43% CAGR.

Which technology segment leads the microphone market?

MEMS microphones lead, holding 66.5% of microphone market share in 2024 thanks to their compact form factor and digital-integration benefits.

Why are wireless microphones growing faster than wired models?

Wireless units offer mobility and simpler installations; adoption is supported by advanced digital modulation and new 6 GHz spectrum access, propelling a 7.4% CAGR through 2030.

How are electric vehicles influencing microphone demand?

Lower cabin noise in EVs encourages in-car voice assistants and active-noise-cancelation systems, driving microphone integration at a 6.7% CAGR within the automotive vertical.

What role does AI play in next-generation microphone products?

AI enhances beam-forming, noise suppression, and speaker tracking, making microphones smarter and expanding use cases from conference rooms to health wearables.

Which region shows the fastest growth outlook?

The Middle East & Africa region is projected to expand by 8.1% CAGR to 2030, fueled by telecom investments and burgeoning media-production activity.

Page last updated on: June 20, 2025