Micro Combined Heat And Power (CHP) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

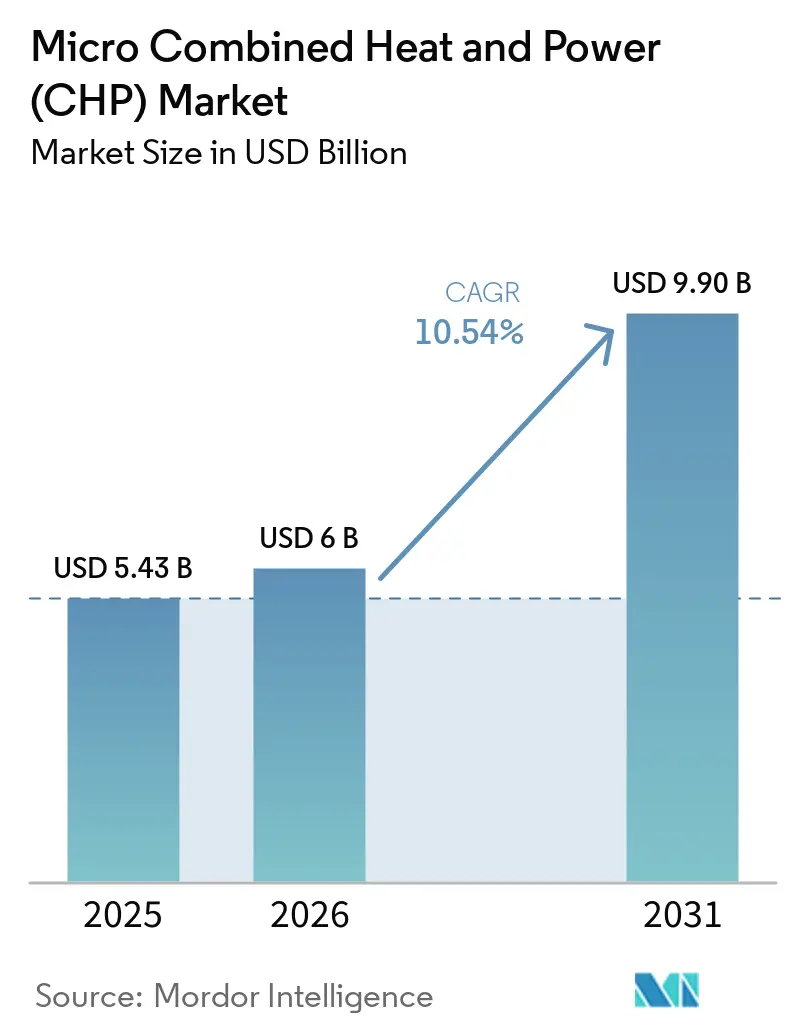

| Market Size (2026) | USD 6 Billion |

| Market Size (2031) | USD 9.90 Billion |

| Growth Rate (2026 - 2031) | 10.54% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Micro Combined Heat And Power (CHP) Market Analysis by Mordor Intelligence

The Micro Combined Heat And Power Market size is projected to expand from USD 5.43 billion in 2025 and USD 6 billion in 2026 to USD 9.90 billion by 2031, registering a CAGR of 10.54% between 2026 and 2031. The micro combined heat and power market is moving into a broader distributed-energy role because building decarbonization rules now reward high-efficiency cogeneration rather than simple boiler replacement. The micro combined heat and power market is also benefiting from energy-security planning that accelerated after the Russia-Ukraine conflict, as building owners and commercial users place greater value on on-site generation and thermal resilience. High-efficiency CHP systems can recover waste heat that conventional generation discards, and the EU has now tied future eligibility more tightly to stricter efficiency thresholds and to cleaner fuel pathways over time.[1]European Commission, “Commission Recommendation (EU) 2024/2395 on Setting Out Guidelines for the Interpretation of Article 29 of Directive (EU) 2023/1791 as Regards the Assessment of Comprehensive Assessment for Efficient Heating and Cooling,” Official Journal of the European Union, eur-lex.europa.eu Japan has shown that long-running subsidy support can compress system costs materially, with ENE-FARM residential SOFC pricing falling from JPY 8 million, USD 77,000, per unit in 2009 to JPY 1.0-1.2 million, USD 8,000-9,700, by 2025. The micro combined heat and power market still faces subsidy distortions, installer bottlenecks, and strong competition from electrified heating, yet vendors with hydrogen-ready products, remote monitoring, and proprietary service networks are better placed to capture recurring value over the equipment life cycle.

Key Report Takeaways

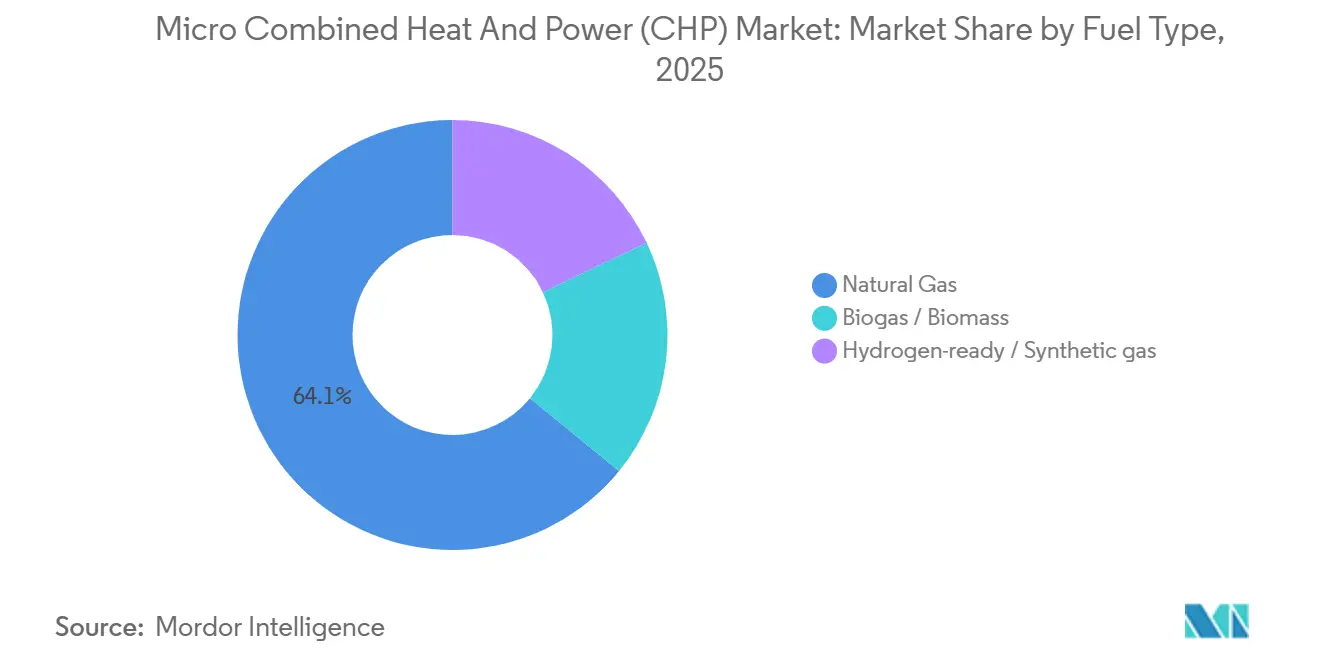

- By fuel type, natural gas held 64.1% of the micro combined heat and power market share in 2025, while hydrogen-ready and synthetic-gas platforms are projected to expand at a 15.3% CAGR through 2031.

- By prime-mover technology, internal-combustion engines accounted for 40.7% share of the micro combined heat and power market size in 2025, while fuel-cell systems are advancing at a 13.2% CAGR through 2031.

- By capacity class, the 5-20 kWe band captured 35.3% share of the micro combined heat and power market size in 2025 and is also forecast to grow at the fastest 11.3% CAGR through 2031.

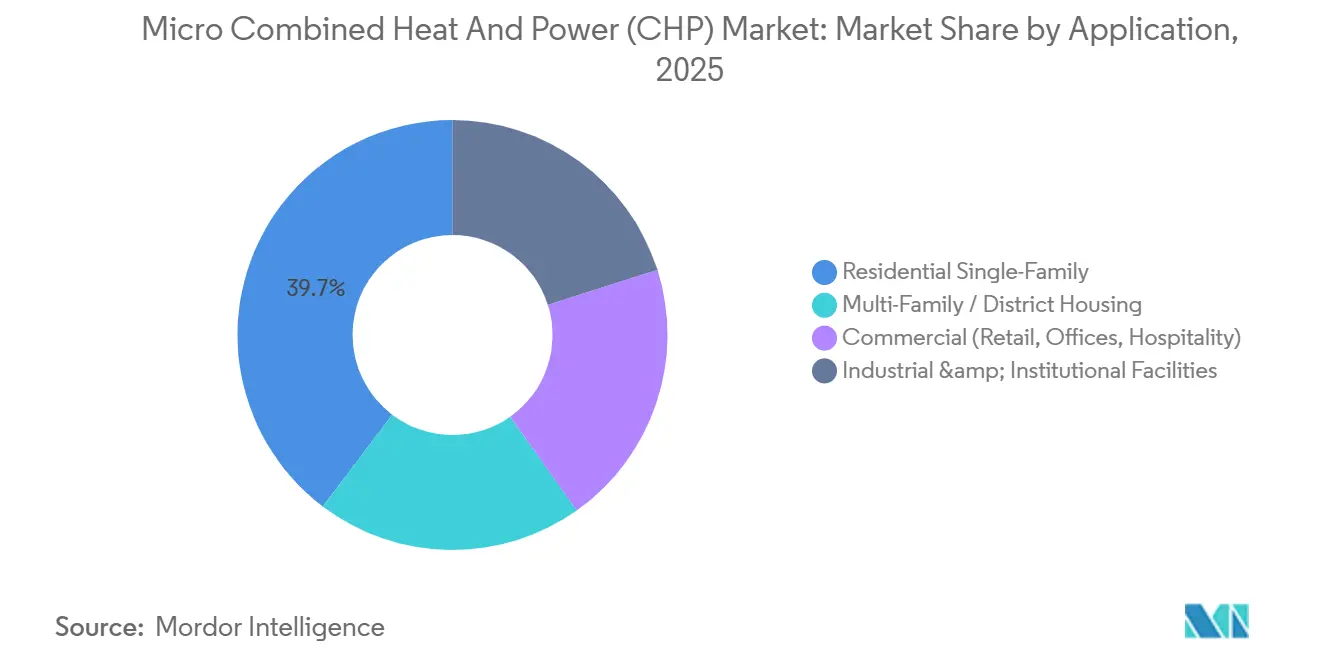

- By application, residential single-family premises led with 39.7% revenue share in 2025, while multi-family and district-housing installations are projected to expand at a 12.1% CAGR through 2031.

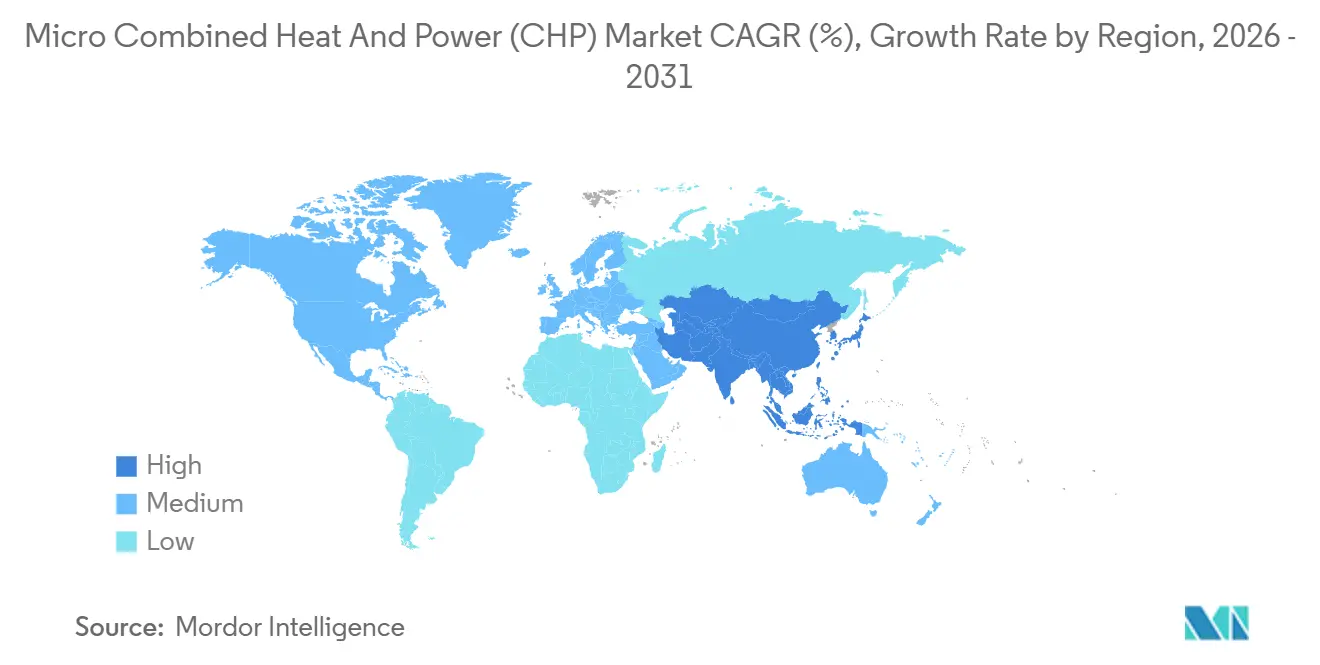

- By geography, Asia-Pacific led with 49.2% revenue share in 2025 and is projected to expand at a 10.8 % CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Micro Combined Heat And Power (CHP) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Residential Fuel-Cell Micro-CHP Roll-Outs In Japan And EU | +2.5% | Japan, Germany, UK, Netherlands, Rest of EU | Short term (≤ 2 years) |

| Energy-Security Push For On-Site Generation Post Russia-Ukraine | +1.8% | Europe, spillover to Global | Short term (≤ 2 years) |

| Emissions Rules Rewarding High-Efficiency Cogeneration | +1.5% | EU, UK, Japan, early adoption in North America | Medium term (2-4 years) |

| Hydrogen-Ready Platforms Unlocking Fuel Flexibility | +2.0% | Germany, Japan, UK, Netherlands | Medium term (2-4 years) |

| Hybrid Micro-CHP Plus Heat-Pump Solutions In Cold-Climate Buildings | +1.2% | Northern Europe, Canada, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Residential Fuel-Cell Micro-CHP Roll-outs in Japan and EU

The micro combined heat and power market is gaining support from Japan’s long-running ENE-FARM framework, which continues to shape residential fuel-cell procurement at scale. METI’s 2025 Kyutou Shoene subsidies provide JPY 160,000, USD 1,050, per base unit and JPY 40,000, USD 260, for network-connected models, and that structure clearly favors units that can participate in grid-interactive operation rather than act only as stand-alone generators. The micro combined heat and power market benefits from that design because each subsidized installation also strengthens a future virtual power plant base in the residential sector. Germany is following a similar path through revised fuel-cell heating support, with the KfW 433 framework updated in January 2024 to provide 30-70% funding coverage for fuel-cell appliances. AISIN’s March 2026 launch of the solar-priority ENE-FARM type S, with 55% lower-heating-value electrical efficiency and integrated PV-priority dispatch, shows how the micro combined heat and power market is moving beyond heat recovery and into household energy-management hardware.[2]AISIN Corporation, “AISIN Launches Solar-Priority ENE-FARM Type S,” AISIN, aisin.com

Energy-Security Push for On-site Generation Post-Russia-Ukraine

The micro combined heat and power market has been strengthened by the shift in European energy policy after the Russia-Ukraine conflict, which pushed energy security into the center of investment decisions. In this market, on-site generation is no longer viewed only as a carbon-saving option, because many buyers now value it as a resilience asset that protects heat and power continuity during grid or fuel disruptions. Hospitals, hotels, data centers, and other facilities with continuous energy loads are increasingly willing to accept a higher system cost when that cost reduces operational risk. Capstone Green Energy’s October 2025 MOU with Microgrids 4 AI shows that the micro combined heat and power market is now also reaching AI-linked data-center redundancy use cases that sit well beyond traditional residential heating demand. This broader buyer mix reduces reliance on any single subsidy program and gives the micro combined heat and power market a more resilient demand base across commercial, institutional, and specialty power applications.

Emissions Regulations Rewarding High-Efficiency Cogeneration

The micro combined heat and power market is being pulled forward by emissions rules that now reward high-efficiency cogeneration more clearly than in earlier policy cycles. The EU’s revised Energy Efficiency Directive introduces stricter primary-energy thresholds from January 2028, removes qualification for fossil-only systems from 2035, and limits future eligibility from 2050 to renewable-fed or waste-heat-fed cogeneration systems. That compliance path gives manufacturers a much clearer product roadmap, because current design choices now need to support cleaner fuel blends and higher efficiency performance over a longer period. Ireland’s Commission for Regulation of Utilities updated its high-efficiency CHP certification process in November 2025 and introduced digital submission pathways that became effective in January 2026. The micro combined heat and power market benefits when certification and grid-connection procedures become simpler, because shorter administrative timelines improve project bankability for both vendors and building owners.

Hydrogen-Ready Micro-CHP Platforms Unlock Future Fuel Flexibility

The micro combined heat and power market is also being reshaped by hydrogen-ready product design, which gives buyers a clearer path to fuel switching without replacing the full system. MWM released its 25H2-Kit in April 2025, enabling up to 25 volume-% hydrogen admixture in existing gas-engine CHP units and delivering an 8% greenhouse-gas reduction without full equipment replacement. The EU-funded SO-FREE project then unveiled a 5 kWe SOFC platform in February 2026 that can operate across the 0-100% hydrogen range while reaching 90-94% total efficiency. AISIN’s December 2025 Kyoto demonstration tested a 10 kW-class SOFC on pure hydrogen at above 60% electrical efficiency, which shows that this shift is moving beyond laboratory work and into applied product validation. The micro combined heat and power market gains a long-term advantage from this flexibility because buyers can protect assets purchased today against future gas-grid hydrogen blending and tighter emissions standards.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Against Boilers And Heat Pumps | -1.8% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) |

| Rapid Cost Declines In Electric Heat Pumps And Storage | -1.5% | Western Europe, North America | Medium term (2-4 years) |

| Installer Skill Gap For Fuel-Cell Maintenance | -0.8% | Global, most acute in EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost vs Condensing Boilers and Heat Pumps

The micro combined heat and power market still faces a clear cost barrier in residential applications because many systems remain far more expensive to install than condensing boilers and many standard heating alternatives. This price gap is especially difficult in single-family homes, where payback depends on high utilization, supportive export tariffs, and strong subsidy coverage. The micro combined heat and power market also carries additional installation complexity in fuel-cell systems, and that raises project costs where trained technicians are scarce. Buyers often compare headline installed price rather than full life-cycle value, which weakens the sales case for systems that deliver savings over a much longer operating period. Until production volumes rise enough to deliver broader manufacturing scale, upfront cost will remain a meaningful brake on the micro combined heat and power market in price-sensitive regions.

Rapid Cost Declines of Electric Heat Pumps and Storage

The micro combined heat and power market is under pressure from electric heating and storage technologies that continue to improve in cost and policy support, even after a weaker sales year in Western Europe. The UK Government projected a 33% reduction in low-temperature heat-pump capital expenditure between 2021 and 2035, which signals a strong medium-term cost path for competing systems. BDR Thermea reported that Western European heat-pump sales fell by 350,000 units in 2024, yet the company still emphasized product strategies that combine heat pumps with other technologies rather than retreat from the category. The micro combined heat and power market faces a tougher competitive setting when battery prices fall at the same time, because storage can partially replicate dispatch flexibility in high-electricity-price environments. Vendors that position hybrid solutions with micro-CHP, heat pumps, and battery storage are better placed than those that sell the micro combined heat and power market only as a stand-alone replacement for boilers or grid electricity.

Segment Analysis

By Fuel Type: Hydrogen-Blend Readiness Reshaping Natural Gas Dominance

Natural gas commanded 64.1% of the micro combined heat and power market in 2025, reflecting the reach of existing gas-grid infrastructure in Europe, North America, and East Asia and the large installed base of units already optimized around gas use. In the micro combined heat and power market, that installed base still matters because service know-how, fuel availability, and buyer familiarity all favor established gas-based systems over newer options. Tokyo Gas has already initiated a 20% hydrogen-blend pilot for ENE-FARM units, which shows that the gas segment is not fixed and is starting to absorb cleaner fuel content over time. Biogas and biomass remain smaller in volume, yet they hold strategic value in Northern and Central Europe where agricultural residues and localized fuel supply can support distributed generation. The µBIO CHP project, completed in March 2026, demonstrated a 2.5 kWe SOFC combined with a 15 kW wood-pellet gasifier and achieved above 90% total efficiency, which supports the case for biomass-fed systems in off-grid or rural use cases.

Hydrogen-ready and synthetic-gas platforms are the fastest-growing fuel segment in the micro combined heat and power market, with a projected 15.3% CAGR through 2031. That growth reflects a purchasing mindset focused on future compliance, because buyers want systems that can continue operating as hydrogen blending expands and emissions rules tighten. MWM’s 25H2 retrofit path gives existing gas-engine owners a practical route into blended-fuel operation without replacing complete systems, which is important for cost-sensitive commercial assets. The SO-FREE project and AISIN’s pure-hydrogen SOFC demonstration show that the micro combined heat and power industry is also advancing toward systems that can move from partial blends to full hydrogen operation over time. Commercial and institutional buyers are adopting this segment faster than households because longer asset lives make stranded-asset risk more material in non-residential procurement.

By Prime-Mover Technology: Fuel Cells Accelerating as ICE Defends the Base

Internal-combustion engines held 40.7% of the micro combined heat and power market in 2025, and they remain important because service networks are mature, replacement parts are easy to source, and installed costs are lower than for fuel-cell systems. This installed base gives ICE vendors a durable position in the micro combined heat and power market, especially in commercial sites where maintenance familiarity matters more than maximum electrical efficiency. A 2024 Nature Communications study reported an opposed-piston engine with 35.2% AC electrical efficiency and above 93% total CHP efficiency, which shows that engine innovation is still moving forward rather than stopping at legacy performance levels. Stirling engines continue to serve quieter residential settings, while micro-turbines appeal to commercial users that want multi-fuel flexibility and remote monitoring through structured service contracts. That means the technology mix remains broad even as attention shifts toward higher-efficiency electrochemical systems.

Fuel-cell systems are the fastest-growing prime-mover category in the micro combined heat and power market, with forecast growth of 13.2% through 2031. The SO-FREE platform reached 90-94% total efficiency across a 0-100% hydrogen range, which gives fuel cells a clear advantage in efficiency-led product positioning. Elcogen added another step in May 2026 by launching the elcoStack E3000 G2 and scaling stack manufacturing capacity to 360 MW at Tallinn, with a claimed 75% electrical efficiency for the platform. In the micro combined heat and power market, these gains matter because better electrical output improves on-site economics and can strengthen the case for grid-connected operation and export revenue. As supply scales further, competitive differentiation is likely to move away from stack production alone and more toward controls, integration, digital service, and field reliability.

By Capacity Class: The 5–20 kWe Band Straddles Residential and Commercial Demand

The 5-20 kWe band held 35.3% of the micro combined heat and power market in 2025 and is also the fastest-growing capacity class, with an 11.3% CAGR through 2031. This part of the micro combined heat and power market works well because it fits multi-family residential blocks, small offices, and community buildings that have steadier thermal and electrical demand than detached homes. Those customer groups usually run higher annual load factors, so the economics improve when compared with smaller residential-only systems. The same band also matches the needs of buyers who want to add grid services, building-level optimization, and remote management without moving into a much larger industrial system class. Its dual position across residential and small commercial use explains why it leads on both current share and forecast growth.

The lower end of the micro combined heat and power market still serves premium single-family applications, and that space remains important in Japan where compact fuel-cell systems fit dense urban housing and can be paired with rooftop solar and battery storage. AISIN’s FY2026 multi-unit housing demonstration reflects this direction, because it combines sub-1 kWe SOFC units with battery and PV integration to improve building-level energy control. The 20-50 kWe and 50-100 kWe ranges support light industrial, institutional, and resilient commercial applications, including hospitals, schools, and data-oriented facilities where downtime carries a higher cost. The Fit4Micro project, scheduled to complete in September 2026, is testing hybrid micro-turbine CHP configurations for multi-family buildings and adds support for mid-range systems that balance fuel flexibility with strong thermal output. That leaves the 5-20 kWe segment in a strong middle position between compact residential formats and larger institutional units.

By Application: Multi-Family and District Housing Outpacing the Residential Base

Residential single-family premises accounted for 39.7% of the micro combined heat and power market in 2025, and this base remains strongest in Japan and Germany where owner-occupier economics are supported by long-running incentives and strong awareness of household energy costs. In the micro combined heat and power market, leading OEMs are now trying to raise lifetime revenue from this base through remote monitoring and service subscriptions rather than relying only on one-time equipment sales. That shift matters because residential unit volumes can be large, but recurring service revenue offers a steadier margin profile than hardware alone. The segment therefore stays important not only for installed share, but also for aftermarket monetization and brand lock-in over the system life cycle.

Multi-family and district-housing applications are forecast to grow at 12.1% in the micro combined heat and power market through 2031, which is the strongest application-level rate in the report. Building managers in this segment can aggregate loads, access utility tariffs more efficiently, and justify virtual power plant participation in a way that is harder for individual homeowners to achieve. Panasonic’s December 2024 Cardiff installation, with 21 hydrogen fuel-cell units, 372 kW of PV, and a 1 MWh battery, provides a visible reference for hybrid energy systems that combine generation, storage, and on-site management in a single location. Commercial premises remain a mid-tier opportunity where steady heat loads support co-generation economics, while institutional and industrial users at the higher end of the micro combined heat and power industry continue to validate advanced configurations such as PV-SOFC integration with major carbon reductions. The application mix is therefore shifting from dispersed single-home use toward professionally managed buildings that can extract more value from flexibility, service, and energy trading.

Geography Analysis

Asia-Pacific represented 49.2% of the micro combined heat and power market size in 2025, and the region is projected to grow at a 10.8% CAGR through 2031. Japan remains the anchor of the regional micro combined heat and power market because ENE-FARM support continues to channel demand toward residential fuel cells and grid-connected installations. METI’s 2025 subsidy design gives additional support to network-connected models, which helps build a broader installed base for coordinated distributed energy services. Japan’s 7th Basic Energy Plan reaffirmed hydrogen as a next-generation energy carrier, and Tokyo Gas’s 20% hydrogen-blend pilot for ENE-FARM units shows how policy ambition is being matched by practical network testing. China adds scale through distributed-energy policy support, while South Korea and Australia contribute demand through resilience-focused energy strategies tied to broader decarbonization goals.

Europe is the second-largest regional block in the micro combined heat and power market share structure, and it is also the most regulation-intensive. Germany anchors regional demand in both residential and commercial use, while the United Kingdom remains part of the European demand base for smaller commercial and residential systems. The EU’s compliance timeline, with stricter high-efficiency thresholds from 2028 and fossil-only exclusion from 2035, is pushing vendors in the micro combined heat and power market to design current systems for cleaner future fuels rather than near-term gas use alone. France, Italy, Spain, and the Netherlands form the next group of European markets, and Ireland’s digital HE CHP certification process from January 2026 supports a steadier project pipeline by lowering administrative friction.

North America remains underused in the micro combined heat and power market despite strong building stock and relevant thermal demand. The United States still concentrates deployment in light industrial and commercial settings because lower gas prices, uneven net-metering rules, and the absence of a Japan-style residential fuel-cell subsidy limit household penetration. Canada is beginning to test stronger multi-family use cases in colder provinces, while Mexico offers an emerging opening for micro-turbine and ICE systems where power-cost management is becoming more strategic. South America remains centered on Brazil’s biogas-linked CHP potential and Argentina’s resilience needs, while the Middle East and Africa stay early-stage markets led by industrial diversification in Saudi Arabia and the UAE and by grid-reliability concerns in South Africa.

Competitive Landscape

The micro combined heat and power market is moderately fragmented. European OEMs such as Vaillant Group, Viessmann Group, BDR Thermea, and 2G Energy remain strong in residential and small commercial installations because they combine established service reach with experience in subsidy-linked sales channels. Japanese manufacturers, especially AISIN and Yanmar, hold an important position in the high-efficiency SOFC tier and continue to define product direction in compact residential systems. Mid-tier ICE-based vendors still compete effectively in the micro combined heat and power market by emphasizing lower installed cost, serviceability, and proven field performance for commercial buyers. BDR Thermea’s 2024 acquisition of minority stakes in 6 Italian and Spanish heating service companies shows how leading firms are investing in service infrastructure to address installer scarcity and build recurring maintenance revenue.

The competitive frontier in the micro combined heat and power market is shifting toward hydrogen integration and toward new power-resilience use cases outside the traditional home-heating base. Honda entered this space in 2026 with a hydrogen fuel-cell CHP demonstration program in Offenbach, Germany, bringing automotive fuel-cell engineering into a field long led by specialist energy companies. Capstone Green Energy’s October 2025 MOU with Microgrids 4 AI shows how micro-turbine vendors are positioning for AI data-center redundancy rather than relying only on conventional CHP demand. Elcogen’s May 2026 stack launch and 360 MW capacity expansion suggest that upstream scaling could lower component costs and move more competitive value toward system integration, software control, and field service.

The micro combined heat and power market is also likely to see competitive change if standardized interfaces reduce component lock-in across the fuel-cell value chain. SO-FREE’s proposal for IEC standardization of SOFC stack interfaces points in that direction and could make it easier for new entrants to assemble systems around more modular upstream supply. Even so, leadership in the micro combined heat and power market will still depend on field execution because service coverage, installer training, and control software remain difficult to copy quickly. The strongest white space remains in multi-family portfolio energy-management software, hydrogen-blend retrofit kits for existing assets, and biogas-linked systems for agri-industrial clusters where waste streams and grid weakness can support local generation economics.

Micro Combined Heat And Power (CHP) Industry Leaders

Vaillant Group

Viessmann Group

Yanmar Holdings

BDR Thermea (Remeha)

AISIN Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Elcogen launched the elcoStack E3000 G2, a mass-manufacturable SOFC stack platform delivering 75% electrical efficiency and 90% total efficiency with heat recovery, with production capacity scaled to 360 MW at its Tallinn facility. The launch positions Elcogen as a high-volume upstream stack supplier capable of supporting broader European micro-CHP scale-up at reduced stack cost

- May 2026: Honda announced development of a hydrogen fuel-cell CHP system for commercial and residential buildings, establishing a demonstration laboratory in Offenbach, Germany, scheduled for summer 2026 operation. Honda's entry introduces automotive fuel-cell engineering depth and global supply-chain scale to a market previously dominated by specialist CHP OEMs

- December 2025: Kiturami Boiler has enhanced its efforts in the North American market by exporting a 200 kW-class micro combined heat and power (CHP) system to the United States.

- November 2025: 2G Energy has formed a strategic partnership with Kiturami, a leading South Korean manufacturer of boilers and cooling systems. This collaboration seeks to combine 2G’s efficient CHP systems with Kiturami’s advanced thermal and cooling technologies to provide integrated energy solutions tailored to the South Korean market. Kiturami’s active involvement in South Korea’s district heating and local heating sectors further strengthens the partnership’s potential to address the country’s increasing demand for efficient and sustainable energy infrastructure.

Global Micro Combined Heat And Power (CHP) Market Report Scope

Micro combined heat and power (micro-CHP) is an energy system designed to generate electricity and usable heat simultaneously from a single fuel source, catering to individual homes or small buildings. By capturing waste heat from power generation, it provides space and water heating, achieving an overall energy efficiency of up to 80%.

The Micro Combined Heat and Power Market is segmented into fuel type, prime-mover technology, capacity class, application, and geography. By fuel type, the market is segmented into natural gas, biogas/biomass, and hydrogen-ready/synthetic gas systems. By prime-mover technology, the market is segmented into internal-combustion engine (ICE), Stirling engine, micro-turbine, and fuel cell technologies, including PEM and SOFC. By capacity class, the market is segmented into less than 5 kWe, 5–20 kWe, 20–50 kWe, and 50–100 kWe. By application, the market is segmented into residential single-family, multi-family/district housing, commercial establishments including retail, offices, and hospitality, and industrial and institutional facilities. The report also covers the market size and forecasts for the micro combined heat and power market in 21 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Natural Gas |

| Biogas / Biomass |

| Hydrogen-ready / Synthetic gas |

| Internal-Combustion Engine (ICE) |

| Stirling Engine |

| Micro-Turbine |

| Fuel Cell (PEM, SOFC) |

| Less than 5 kWe |

| 5 - 20 kWe |

| 20 - 50 kWe |

| 50 - 100 kWe |

| Residential Single-Family |

| Multi-Family / District Housing |

| Commercial (Retail, Offices, Hospitality) |

| Industrial & Institutional Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Fuel Type | Natural Gas | |

| Biogas / Biomass | ||

| Hydrogen-ready / Synthetic gas | ||

| By Prime-Mover Technology | Internal-Combustion Engine (ICE) | |

| Stirling Engine | ||

| Micro-Turbine | ||

| Fuel Cell (PEM, SOFC) | ||

| By Capacity Class | Less than 5 kWe | |

| 5 - 20 kWe | ||

| 20 - 50 kWe | ||

| 50 - 100 kWe | ||

| By Application | Residential Single-Family | |

| Multi-Family / District Housing | ||

| Commercial (Retail, Offices, Hospitality) | ||

| Industrial & Institutional Facilities | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for global micro combined heat and power?

The global micro combined heat and power market stands at USD 6.00 billion in 2026 and is projected to reach USD 9.90 billion by 2031, growing at a 10.54% CAGR over 2026-2031.

Which fuel type leads adoption today?

Natural gas remains the largest fuel segment with 64.1% share in 2025 because existing gas infrastructure still gives it the strongest installed-base advantage.

Which technology is growing fastest in micro-CHP systems?

Fuel-cell systems are the fastest-growing prime-mover category, with forecast growth of 13.2% through 2031, supported by higher efficiency and hydrogen-ready development.

Why is Asia-Pacific the leading regional hub?

Asia-Pacific held 49.2% of 2025 revenue and is also projected to grow at 10.8% CAGR through 2031, with Japans ENE-FARM support and broader regional distributed-energy policy driving demand.

What application is expanding the fastest?

Multi-family and district housing is the fastest-growing application at 12.1% CAGR through 2031 because building operators can aggregate loads, improve economics, and access grid-interactive value streams.

What is the biggest risk to wider deployment?

High upfront system cost remains the main barrier, and the pressure is increasing as heat pumps and storage continue to improve in cost, support policy, and buyer familiarity.

Page last updated on: