Mexico Oral Anti-Diabetic Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

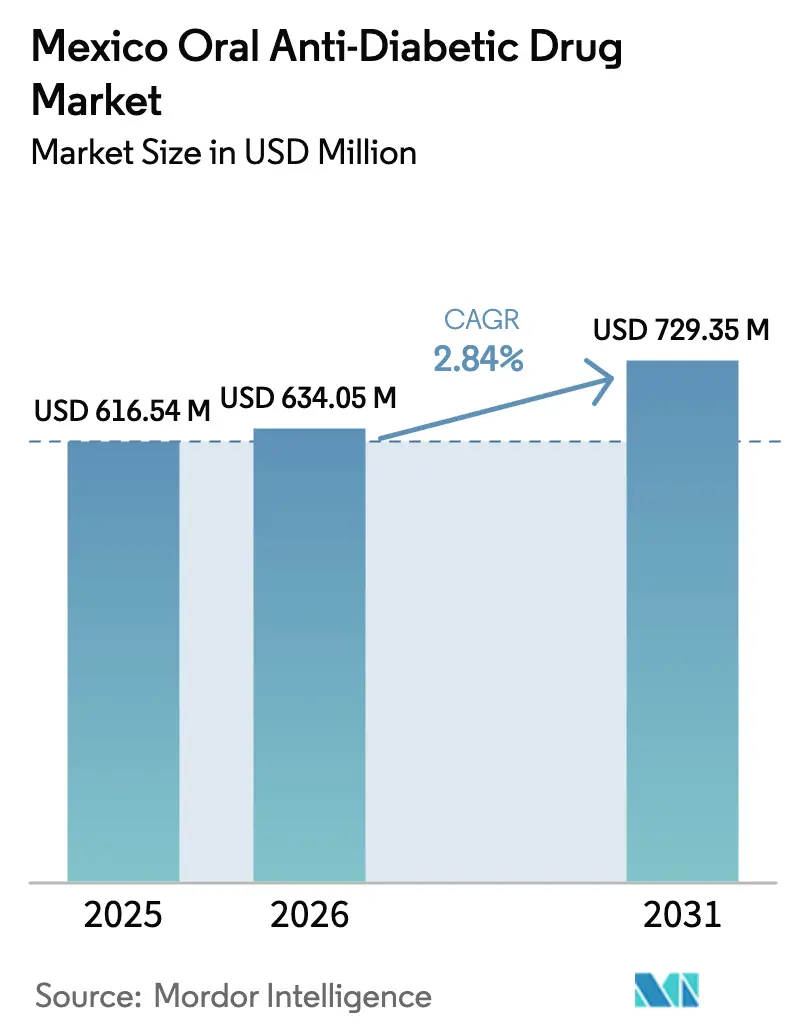

| Base Year Market Size (2025) | USD 616.54 Million |

| Market Size (2026) | USD 634.05 Million |

| Market Size (2031) | USD 729.35 Million |

| Growth Rate (2026 - 2031) | 2.84% CAGR |

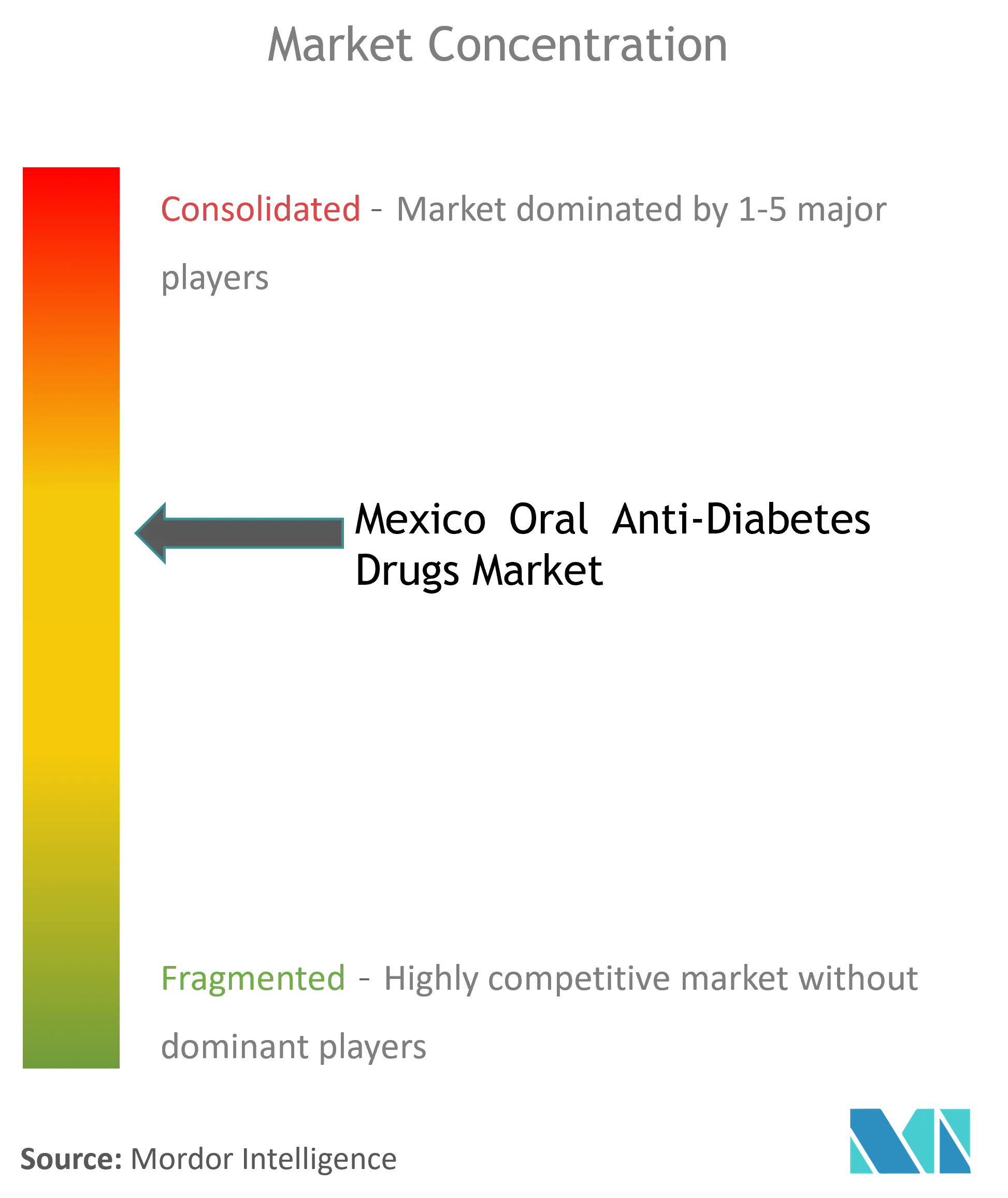

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Oral Anti-Diabetic Drug Market Analysis by Mordor Intelligence

The Mexico oral anti-diabetic drug market size was valued at USD 616.54 million in 2025 and estimated to grow from USD 634.05 million in 2026 to reach USD 729.35 million by 2031, at a CAGR of 2.84% during the forecast period (2026-2031). Demand expands as President Claudia Sheinbaum’s “Pharmacies for Well-being” program begins nationwide free-medicine distribution to low-income households, improving prescription fill rates. Mexico carries the world’s sixth-highest diabetes prevalence and will likely rank seventh by 2030, placing sustained pressure on healthcare budgets. Aging demographics, rising obesity, and rapid urbanization drive consistent uptake of oral therapies, while patent-linkage reforms signed in February 2025 shorten approval queues and attract innovator pipelines. Still, price ceilings on essential medicines, import reliance for active pharmaceutical ingredients (APIs), and the spread of counterfeit products temper revenue growth.

Key Report Takeaways

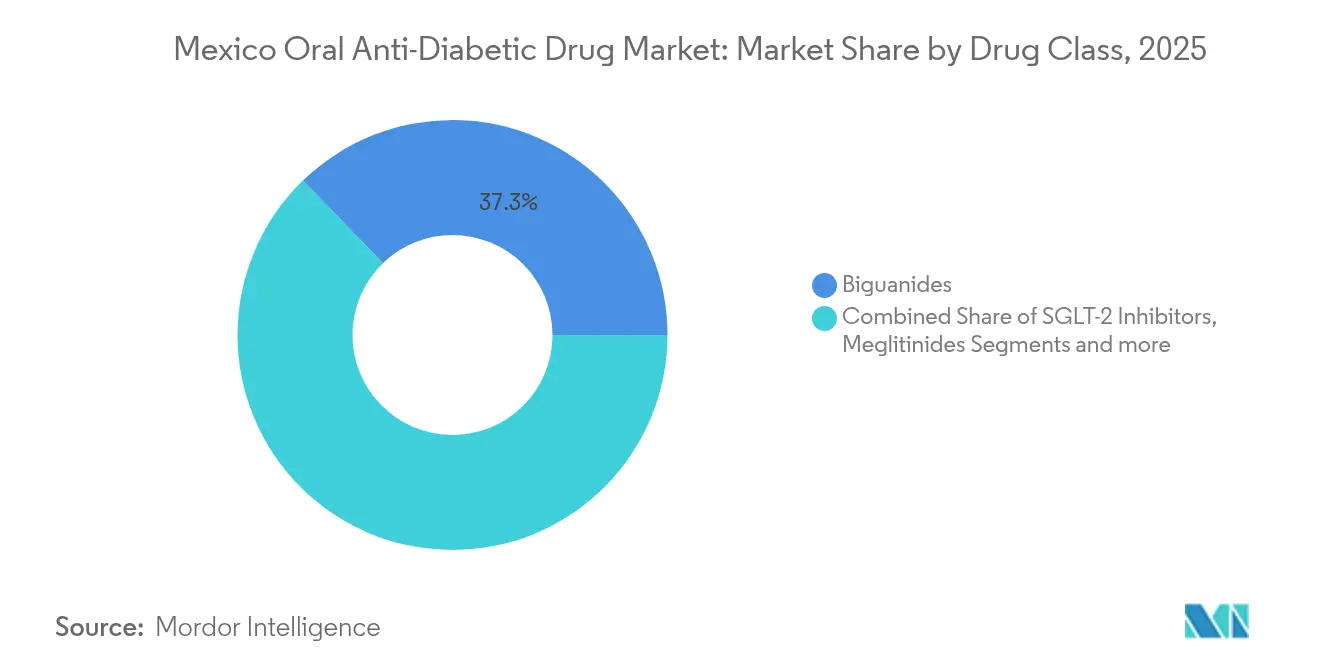

- By drug class, Biguanides led with 37.25% revenue share in 2025; SGLT-2 inhibitors are projected to expand at a 3.38% CAGR through 2031.

- By age group, adults held 67.45% of 2025 demand, while the geriatric cohort is set to rise at a 3.48% CAGR to 2031.

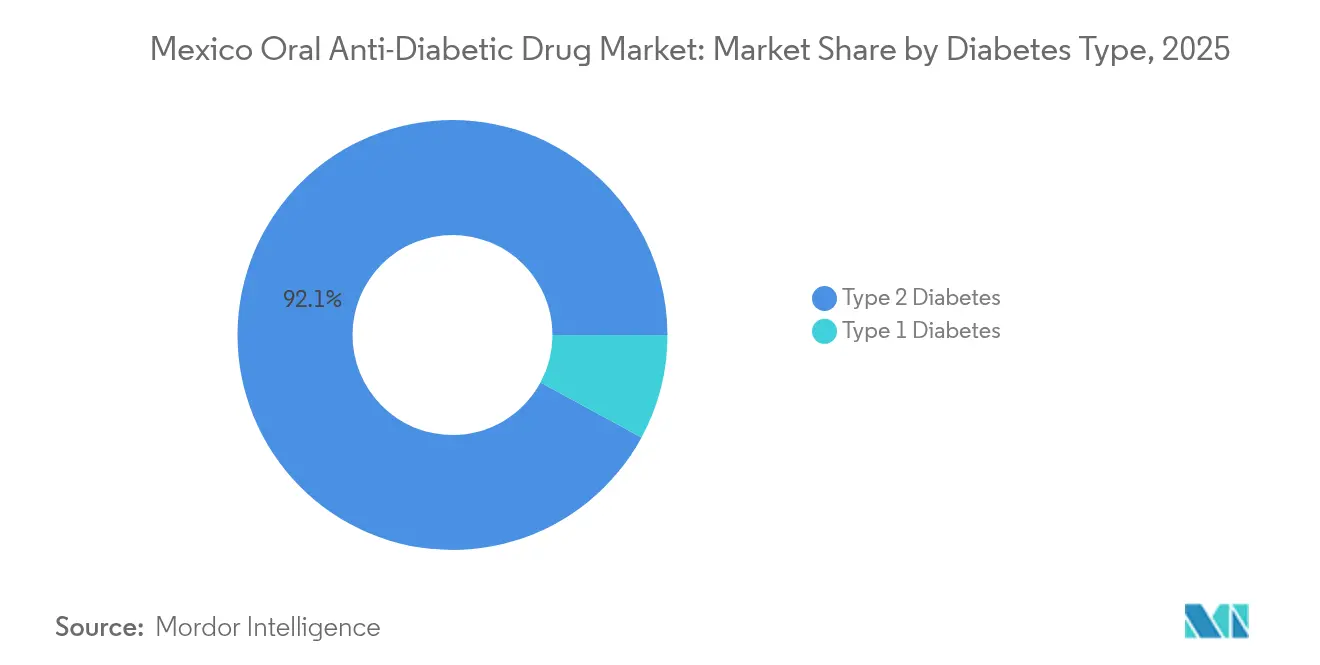

- By diabetes type, Type 2 accounted for 92.10% of the Mexico oral anti-diabetic drug market share in 2025 and maintains a 3.60% CAGR outlook.

- By distribution channel, hospital pharmacies commanded 67.10% of 2025 sales, whereas online pharmacies record the fastest 3.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Figures recorded within Mexico feed into a worldwide estimate while studying the global industry. Mordor Intelligence's oral anti-diabetic drugs market size captures this aggregation.

Mexico Oral Anti-Diabetic Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating prevalence of Type 2 diabetes | +0.8% | National, urban focus | Long term (≥ 4 years) |

| Expansion of Seguro Popular & IMSS reimbursement lists | +0.6% | National, stronger in rural states | Medium term (2-4 years) |

| Faster uptake of SGLT-2 inhibitors post-CVOT evidence | +0.5% | National, early adoption in metro areas | Medium term (2-4 years) |

| Growth of fixed-dose combination pills | +0.4% | National, private-sector preference | Short term (≤ 2 years) |

| Tele-medicine and e-prescription boosting adherence | +0.3% | Urban first, rural roll-out | Short term (≤ 2 years) |

| Fin-tech micro-credit enabling monthly drug purchases | +0.2% | Urban and semi-urban | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Prevalence of Type 2 Diabetes

Mexico’s diabetes epidemic deepens as lifestyle change outpaces public-health intervention. Household survey data show 18% of adults live with diabetes; incidence rises faster in women because of unequal access to preventive care [1]Marina Gonzalez-Samano, "Diabetes, life course and childhood socioeconomic conditions: an empirical assessment for Mexico," BMC Public Health, bmcpublichealth.biomedcentral.com. IMSS now treats more than 3.5 million patients annually, and complication clusters in central states strain resources. Higher mortality in the Yucatán Peninsula illustrates socioeconomic inequities [2]Claudio Alberto Dávila Cervantes, "Mortality from type 2 diabetes mellitus across municipalities in Mexico," Archives of Public Health, archpublichealth.biomedcentral.com. Because oral therapies remain first-line, sustained volume growth in the Mexico oral anti-diabetic drug market is inevitable. Community screening by Project HOPE expands detection among marginalized women.

Expansion of Seguro Popular & IMSS Reimbursement Lists

Bulk procurement covering 4,454 product codes secures 97.6% of essential medicines for 2025-2026, shrinking stock-out risk and lifting adherence. A 130-billion-peso budget extends formulary breadth, primarily benefitting metformin and select SGLT-2 agents in rural clinics. Free-drug distribution lowers out-of-pocket spends, widening the treated pool inside the Mexico oral anti-diabetic drug market.

Faster Uptake of SGLT-2 Inhibitors Post-CVOT Evidence

Meta-analysis confirms 15% cardiovascular mortality reduction and 30% heart-failure hospitalization drop with SGLT-2 therapy. Mexican real-world studies show 19.6% HbA1c control for dapagliflozin alone, rising to 30.3% in combinations. Physicians now initiate SGLT-2 inhibitors earlier, lifting unit demand despite price ceilings [3]Luz Alcantar-Vallin, "SGLT2i treatment during AKI and its association with major adverse kidney events," Frontiers in Pharmacology, frontiersin.org.

Growth of Fixed-Dose Combination Pills

Prescription audits indicate 60.7% of Type 2 patients receive polypharmacy, yet nearly three-quarters lack nutritional assessment. Fixed-dose options such as dapagliflozin-metformin ease pill burden and improve compliance. Xigduo XR retails at MXN 1,212 for 14 tablets and has gained shelf space in leading chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government price ceilings on essential drugs | −0.4% | National, public sector | Long term (≥ 4 years) |

| High out-of-pocket spending in rural states | −0.3% | Rural and marginalized | Medium term (2-4 years) |

| API import dependence causing supply shocks | −0.2% | National, generics | Short term (≤ 2 years) |

| Counterfeit OADs in informal farmacias similares | −0.1% | Border areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Price Ceilings on Essential Drugs

Drug spending absorbs 27.2% of Mexico’s health budget, far above the 16.3% OECD mean. The December 2024 rule permitting imports without local authorization trims costs but may undermine innovation and patent rights. Manufacturers offset margin pressure by prioritizing high-volume products within the Mexico oral anti-diabetic drug market.

High Out-of-Pocket Spending in Rural States

Medication costs reached USD 2.79 billion in 2020, limiting adherence among uninsured rural citizens. Innovative clinics such as Clinicas del Azucar cut yearly expenses to USD 250 and achieve better control, offering scalable relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: SGLT-2 Inhibitors Lead Innovation Wave

In 2025, Biguanides retained 37.25% of the Mexico oral anti-diabetic drug market share through metformin’s entrenched first-line status. Segment expansion remains slow, yet volume durable. Conversely, SGLT-2 inhibitors post the fastest 3.38% CAGR as cardiometabolic evidence drives earlier use. The Mexico oral anti-diabetic drug market size for SGLT-2 inhibitors is projected to climb alongside improved reimbursement and patent-linkage clarity. Secondary classes such as DPP-4 inhibitors and sulfonylureas serve legacy cohorts but face stagnation. Thiazolidinedione use declines amid safety concerns, while alpha-glucosidase inhibitors occupy small post-prandial niches.

Therapeutic dynamics reflect Mexico’s pivot to outcome-based prescribing. Novo Nordisk concluded an oral semaglutide study in 187 Mexican adults during April 2024, bolstering GLP-1 pipeline confidence. Boehringer Ingelheim’s EUR 120 million European capacity build for empagliflozin secures supply for Latin America, reducing shortages.

By Age Group: Geriatric Segment Accelerates Growth

Adults held 67.45% of 2025 volume, yet the geriatric cohort grows quickest at 3.48% CAGR as population aging intensifies. The Mexico oral anti-diabetic drug market size attributed to seniors will therefore widen through 2031. Older Mexicans experience 15.1% prevalence with higher disability rates. Age-specific care models prioritize metformin unless renal contraindications arise. Community gerontology programs cut metabolic-syndrome incidence by 72%, illustrating preventive leverage.

Pediatric Type 2 diabetes climbs from 20.2% to 33% across 2013-2018, underscoring future demand. The PAANDA program reduced HbA1c by 1.8% within six months, hinting at scalable interventions for adolescents.

By Diabetes Type: Type 2 Dominance Drives Market Expansion

Type 2 diabetes shapes 92.10% of the Mexico oral anti-diabetic drug market and preserves a 3.60% growth trajectory. The segment’s vast base originates from lifestyle shifts and obesity affecting 75% of adults. Recent semaglutide 2.4 mg rollout targets BMI ≥30 or ≥27 with comorbidities and should enlarge prescription volume. Type 1 represents a smaller group but demands specialized regimens; median HbA1c of 8.7% signals reasonable control despite limited resources.

Guidelines position metformin as first line for Type 2, with SGLT-2 inhibitors or GLP-1 agents added for cardiovascular risk. Combined, these policies keep the Mexico oral anti-diabetic drug market on a stable, moderate growth path.

By Distribution Channel: Digital Transformation Reshapes Access

Hospital pharmacies accounted for 67.10% of sales in 2025, a reflection of Mexico’s institution-centric care model. Online channels are growing at a 3.63% CAGR as consumers adopt telemedicine and e-prescription tools. The Mexico oral anti-diabetic drug market size sold via online portals is still small but expanding quickly. Major chains list Ozempic at MXN 4,317-5,847 and Rybelsus at MXN 4,251, highlighting retail premium pricing. Counterfeit risk grows along the northern border, where inspections uncovered fentanyl-laced fake diabetes drugs.

Digital health apps such as “Salud Activa” crowdsource lifestyle data and nudge adherence, while Takeda’s innovation hub in Mexico City builds data-governance frameworks to support omnichannel engagement. These trends collectively improve medication continuity across the Mexico oral anti-diabetic drug market.

Geography Analysis

Urban hubs—Mexico City, Guadalajara, Monterrey—anchor advanced diabetes care infrastructure and concentrate specialist clinics. Flagship networks like Clinicas del Azucar deliver HbA1c below 7% in a higher share of patients than public facilities by blending behavioral science with technology. Central Mexico and the Yucatán Peninsula show elevated mortality, tied to marginalization and low educational attainment. IMSS family practice data reveal microvascular complications cluster in industrial belts, while macrovascular events dominate rural landscapes.

Rural states bear the brunt of out-of-pocket spending, curtailing treatment continuity despite national price caps. “Pharmacies for Well-being” deploys free medicines in these areas starting 2025, a policy expected to enlarge the treated cohort inside the Mexico oral anti-diabetic drug market. Border zones attract US medical tourists but also host informal outlets peddling counterfeit pills, prompting WHO alerts.

Pharmaceutical manufacturing sits mainly in Mexico City, Jalisco, and Puebla, with 138 plants serving domestic and export markets. Exports top USD 2.5 billion yet equal only 1.5% of US imports, offering upside for nearshoring once API dependence on China and India declines. Urban prevalence stands at 12.1% versus 8.3% rural, but resource gaps amplify rural mortality. Telehealth expansion and mobile health apps can bridge these divides, pointing to incremental demand pockets within the Mexico oral anti-diabetic drug market.

Mordor Intelligence evaluates the oral anti-diabetic drugs market across all key regional markets, including North America, Europe, and Asia, with deeper country-level insights covering Brazil, France, Vietnam, South Korea, Indonesia, and Philippines.

Competitive Landscape

Global innovators and domestic generics create a moderately consolidated field. Novo Nordisk captures 34% global diabetes value share and 56% of the GLP-1 arena, reinforcing leadership with oral semaglutide research and Mexico launch. Eli Lilly’s USD 3 billion Wisconsin expansion and Boehringer’s European scale-up ensure injectable and oral supply continuity across North America. Generic opportunity intensifies after the FDA cleared Hikma’s liraglutide in December 2024, signaling future erosion in the GLP-1 class.

Strategically, firms pursue vertical integration and digital-health alliances to boost adherence. Takeda’s Mexico digital hub focuses on analytics and omnichannel support, while Clinicas del Azucar collaborates with device makers to integrate continuous glucose monitoring. Patent-linkage agreements between COFEPRIS and the patent office, finalized February 2025, shorten time to market for novel molecules and biosimilars, further energizing the Mexico oral anti-diabetic drug market.

White-space persists in pediatric and geriatric formulations, with Type 2 diabetes prevalence in children rising sharply. Companies exploring chewable metformin or lower-dose fixed combinations can tap underserved niches. Supply-chain resilience remains a differentiator; 2023 FDI inflows of USD 36 billion into Mexican manufacturing signal momentum for nearshoring that could ease the API shortfall and shield margins.

Mexico Oral Anti-Diabetic Drug Industry Leaders

-

Astrazeneca

-

Astellas

-

Eli Lilly

-

Sanofi

-

Johnson and Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Novo Nordisk launched semaglutide 2.4 mg in Mexico for adults with BMI ≥30 or ≥27 with comorbidities, broadening obesity-diabetes crossover therapy. Mexico Business News

- February 2025: Mexico’s patent office and COFEPRIS signed a pact to align patent data with regulatory reviews, aligning with USMCA standards.

- January 2025: Ministry of Health secured 97.6% of essential medicines for 2025-2026, covering 4,454 product codes across 26 institutions. Mexico Business News

Mexico Oral Anti-Diabetic Drug Market Report Scope

Orally administered antihyperglycemic drugs reduce blood glucose levels. Diabetes medications are employed to manage diabetes mellitus by reducing the glucose concentration in the bloodstream. Apart from insulin, the majority of GLP receptor agonists (such as liraglutide, exenatide, and others) and pramlintide are taken orally, earning them the name of oral hypoglycemic agents or oral antihyperglycemic agents. The Mexico Oral Anti-Diabetic Drug Market is segmented into drugs. The report offers the value (in USD) and volume (in Units) for the above segments.

| Biguanides |

| Sulfonylureas |

| Meglitinides |

| Thiazolidinediones |

| Alpha-Glucosidase Inhibitors |

| DPP-4 Inhibitors |

| SGLT-2 Inhibitors |

| Others |

| Adults |

| Pediatric |

| Geriatric |

| Type 1 Diabetes |

| Type 2 Diabetes |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| By Drug Class | Biguanides |

| Sulfonylureas | |

| Meglitinides | |

| Thiazolidinediones | |

| Alpha-Glucosidase Inhibitors | |

| DPP-4 Inhibitors | |

| SGLT-2 Inhibitors | |

| Others | |

| By Age Group | Adults |

| Pediatric | |

| Geriatric | |

| By Diabetes Type | Type 1 Diabetes |

| Type 2 Diabetes | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies | |

| Online Pharmacies |

Key Questions Answered in the Report

What is the current Mexico oral anti-diabetic drug market size?

The market is valued at USD 634.05 million in 2026 and is projected to grow to USD 729.35 million by 2031 at a 2.84% CAGR during the forecast period (2026-2031).

Which therapeutic class is growing fastest in the Mexico oral anti-diabetic drug market?

SGLT-2 inhibitors show the highest growth with a 3.38% CAGR, driven by cardiovascular outcome evidence and wider reimbursement.

How significant is Type 2 diabetes in Mexico compared with Type 1?

Type 2 diabetes holds 92.10% market share, making it the predominant segment, while Type 1 remains a smaller but essential niche.

What channel is expanding most quickly for drug distribution?

Online pharmacies post the fastest 3.63% CAGR as telemedicine and e-prescriptions gain traction nationwide.

How are government policies affecting pricing?

National price ceilings compress margins but improve affordability, while recent procurement reforms secure 97.6% of essential medicines for public institutions.

Are counterfeit diabetes drugs a serious issue?

Yes, WHO and border-control reports identify falsified oral anti-diabetics in informal pharmacies, particularly along tourist corridors, posing safety risks and revenue leakage.

Page last updated on: