MEMS Lidar Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.34 Billion |

| Market Size (2031) | USD 3.66 Billion |

| Growth Rate (2026 - 2031) | 20.04% CAGR |

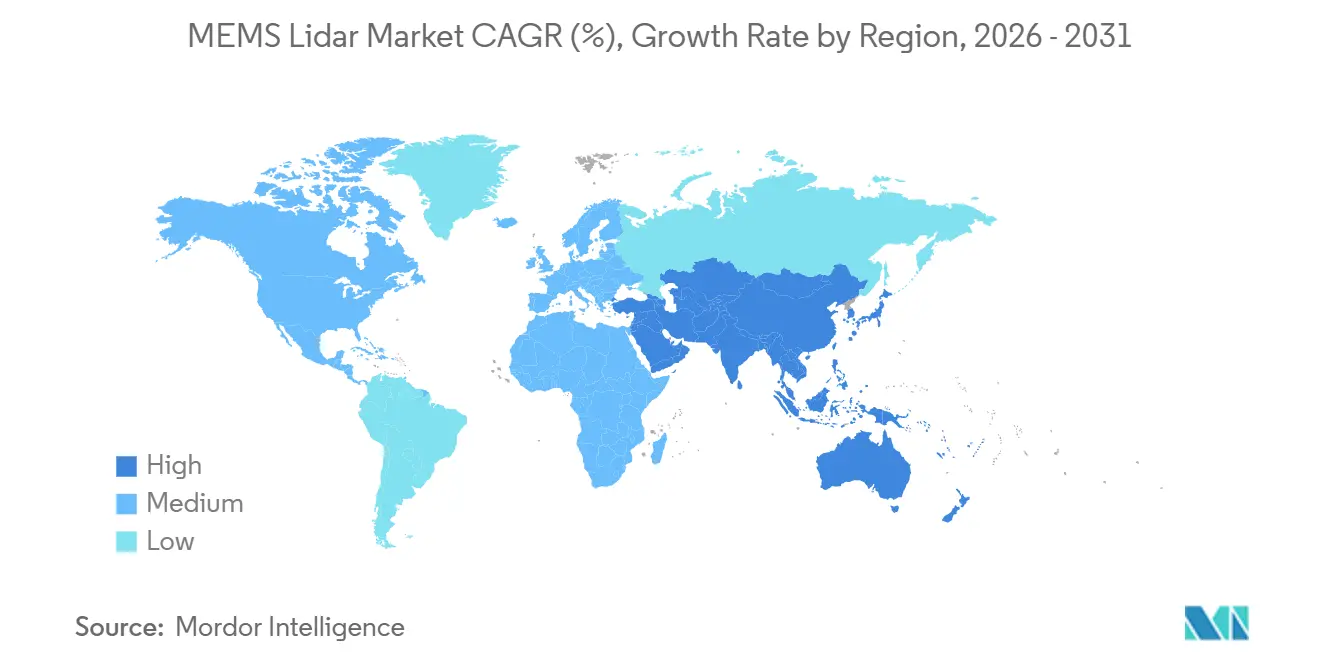

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

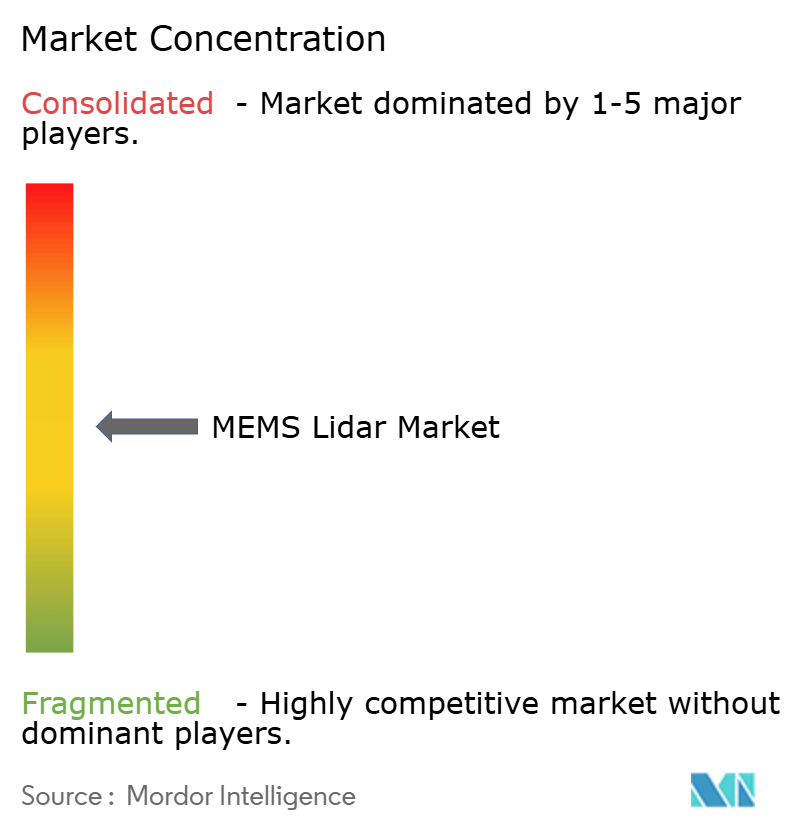

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MEMS Lidar Market Analysis by Mordor Intelligence

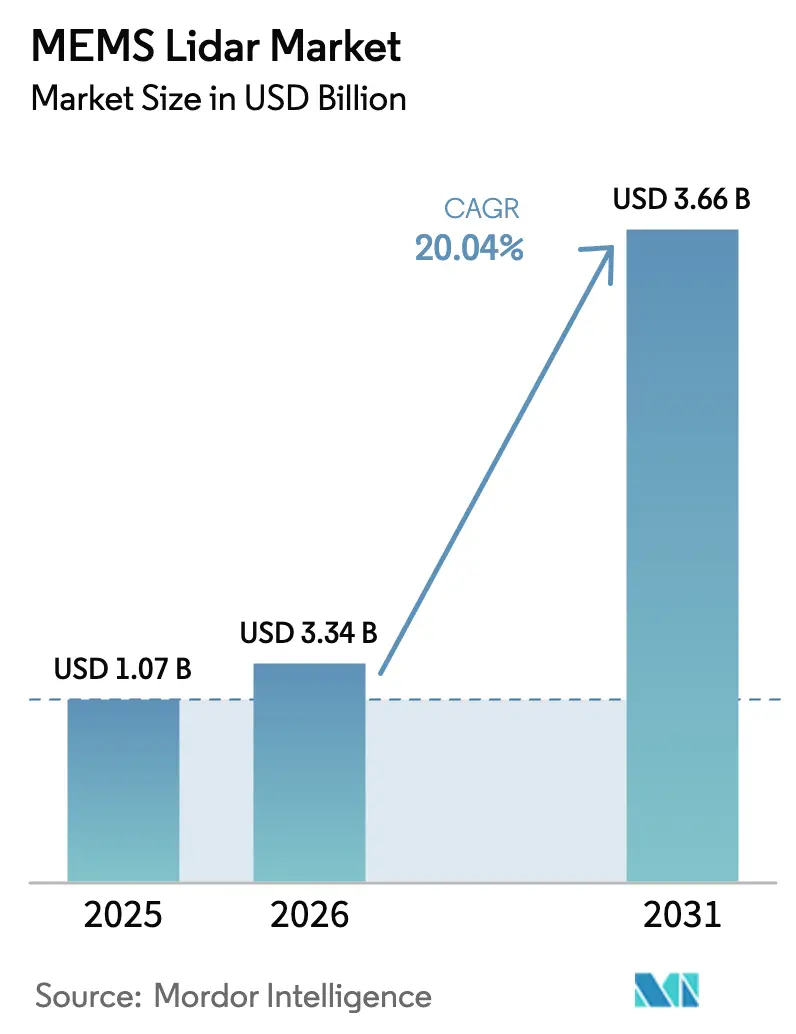

The MEMS Lidar Market size is projected to be USD 1.07 billion in 2025, USD 3.34 billion in 2026, and reach USD 3.66 billion by 2031, growing at a CAGR of 20.04% from 2026 to 2031.

Growing safety mandates in major vehicle markets, wafer-level cost efficiencies, and the shift from mechanical to solid-state architectures are the central forces expanding demand. Automakers are pairing these compact scanners with camera-radar stacks to unlock Level 2+ and Level 3 functions, while warehouse and drone operators are adopting low-weight units that map cluttered spaces at sub-decimeter accuracy. Concurrently, 1550-nanometer designs that operate at eye-safe power levels are gaining traction for long-range perception in poor weather, and semiconductor foundries are dedicating 300-millimeter lines to photonics, compressing bill-of-materials costs and production lead times. Competition remains fragmented as Tier-1 suppliers, fabless start-ups, and vertically integrated Chinese firms race to lock in multiyear design wins, setting the stage for consolidation through 2028.

Key Report Takeaways

- By component, transmitter modules led with 46.01% revenue share in 2025, while receiver modules are forecast to expand at a 21.34% CAGR through 2031.

- By end-user industry, automotive held 31.22% of revenue in 2025, whereas robotics and drones are projected to record the highest growth at 21.89% CAGR to 2031.

- By range, mid-range systems accounted for 41.00% of demand in 2025, and long-range modules are expected to rise at a 21.27% CAGR through 2031.

- By wavelength, 905-nanometer devices captured 55.00% share in 2025, while 1550-nanometer systems are anticipated to accelerate at 21.56% CAGR to 2031.

- By geography, Asia Pacific commanded 41.29% revenue share in 2025, with the North America poised to post the fastest growth at 21.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global MEMS Lidar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Autonomous Vehicles | +4.20% | Global, with concentration in China, United States, Germany | Medium term (2-4 years) |

| Expansion of Advanced Driver Assistance Systems in Mass-Market Models | +3.80% | North America, Europe, Asia Pacific | Short term (≤ 2 years) |

| Cost Reduction Through Semiconductor-Scale MEMS Manufacturing | +3.50% | Asia Pacific core, spillover to North America | Medium term (2-4 years) |

| Regulatory Mandates for Vehicle Safety Sensors | +2.90% | Europe (GSR), North America (FMVSS), China (C-NCAP) | Short term (≤ 2 years) |

| Emergence of MEMS LiDAR-On-Chip for In-Cabin Gesture Control and Driver Monitoring | +1.60% | Global, early adoption in premium segments | Long term (≥ 4 years) |

| Integration of MEMS LiDAR in Smart Infrastructure for Adaptive Traffic Management | +2.10% | Middle East, Asia Pacific smart cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Autonomous Vehicles

Pilot programs in 2025 pivoted from citywide robotaxi demonstrations to freight corridors and shuttle loops, tightening lidar performance targets around deterministic object detection at highway speeds. Chinese OEMs installed sub-USD 500 MEMS units delivering 150-meter range in production cars, while U.S. freight fleets specified frequency-modulated continuous-wave variants exceeding 1,000 meters for long-haul autonomy.[1]Aeva Technologies, “Frequency-Modulated Continuous-Wave Lidar for Daimler Truck,” aeva.com Draft United Nations amendments that allow Level 4 motorway operation by 2028 are expected to codify forward-facing lidar as mandatory, accelerating global design cycles.

Expansion of Advanced Driver Assistance Systems in Mass-Market Models

Five-star safety ratings in Europe now require low-light pedestrian emergency braking, a scenario where camera-radar stacks underperform and lidar closes the perception gap. China’s sub-USD 30 000 sport-utility segment offered lane-change assist and automated parking in 2025 using USD 500 solid-state lidars, cutting the technology’s entry price by 60% in two years. Updated United States proposals for rear-object detection by model year 2029 further widen the addressable vehicle base.[2]U.S. Federal Register, “Proposed Update to FMVSS 127 Rear Visibility,” federalregister.gov

Cost Reduction Through Semiconductor-Scale MEMS Manufacturing

Foundries in Italy and Taiwan qualified eight-inch wafer lines for high-volume beam-steering mirrors in 2025, reducing assembly cost from USD 120 to USD 35 per unit and lifting yield to 82% by automating in-line etch depth control. Allocation of 300-millimeter photonics capacity signals a structural shift that brings lidar supply chains in line with radio-frequency front-end economics.[3]Taiwan Semiconductor Manufacturing Co., “300 mm Integrated Photonics Capacity Allocation,” tsmc.com

Regulatory Mandates for Vehicle Safety Sensors

The European General Safety Regulation that took effect in 2024 obliges new vehicle types to include advanced braking and lane-keeping, pushing OEMs toward lidar to achieve ≥95% detection confidence in complex environments. Germany’s 2025 guidance on redundant perception, China’s C-NCAP bonus points, and smart-road grants in the United States collectively tighten the compliance window, translating policy into near-term purchase orders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Automotive-Grade LiDAR Modules | -2.80% | Global, acute in price-sensitive segments | Short term (≤ 2 years) |

| Performance Degradation in Adverse Weather Conditions | -1.90% | Northern Europe, North America, northern Asia Pacific | Medium term (2-4 years) |

| Yield Variability in Wafer-Level MEMS Mirrors Affecting Scalability | -1.40% | Asia Pacific and Europe manufacturing hubs | Medium term (2-4 years) |

| Limited Supply of Automotive-Qualified InGaAs SPAD Arrays for 1550 nm Systems | -1.20% | Global, supply concentrated in North America and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Automotive-Grade Lidar Modules

Automotive-qualified units remained in the USD 800-USD 1 200 bracket in 2025, triple the cost of imaging radar. Qualification adds roughly USD 180 per unit in non-recurring engineering and a year of extra development, while 28% of hardware cost stems from laser arrays. Chinese vendors lowered prices to USD 450 by relaxing cold-start requirements, yet those modules remain unsuitable for Nordic and Canadian markets that demand -40 °C operation.

Performance Degradation in Adverse Weather Conditions

Mie scattering at optical wavelengths halves 905-nanometer range in moderate rain, forcing sensor-fusion stacks to lean on radar during 15%-25% of yearly driving hours in temperate zones. Although 1550-nanometer devices offer 30% better fog penetration, they depend on costly InGaAs detectors, and global automotive-grade capacity stayed below 0.5 million units in 2025, tempering near-term volume adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Transmitter Modules Anchor Revenue, Receiver Innovation Drives Growth

Transmitter modules accounted for 46.01% of 2025 sales, reflecting long-established VCSEL and edge-emitter supply chains. That leadership will persist as volume ramps in China keep prices below USD 60 per die, protecting margins even as broader hardware deflation unfolds. Receiver innovation, however, is where competitive gaps widen. Single-photon avalanche diode arrays provide a 15-decibel sensitivity lift over legacy avalanche photodiodes, propelling the receiver slice to a forecast 21.34% CAGR that outstrips the overall MEMS lidar market. The shift cuts required laser power, thereby easing eye-safety constraints and lowering thermal budgets, two factors that simplify module packaging.

Signal-processing electronics are collapsing into system-on-chip designs that embed time-to-digital converters alongside neural-network accelerators, squeezing board count and halving power draw. MEMS mirror assemblies, although only 6% of 2025 revenue, dominate engineering attention because sub-micrometer flatness variation can scrap an entire wafer lot. Suppliers are introducing closed-loop actuators that nudge mirror position in real time to offset drift. The others category of optics, heat spreaders, and enclosures is evolving from milled metal to polymer composites with hydrophobic coatings, extending service life in under-body installations and mitigating road-salt corrosion.

By End-User Industry: Automotive Leads, Robotics Accelerates

Automotive retained 31.22% of 2025 value as Chinese new-energy vehicles embedded forward-facing lidar to win C-NCAP points, while European luxury brands assigned lidar to Level 3 flagship sedans. That revenue base guarantees the sector’s primacy through 2031, even though its growth rate will trail faster-moving niches. Robotics and drones, projected at a 21.89% CAGR, are scaling on warehouse automation budgets that need sub-USD 400 scanners capable of millimetre-level mapping within 50 meters. Drone deliveries favour the same weight-optimized modules, stimulating cross-volume synergies.

Industrial automation holds roughly one-fifth of segment dollars, where lidar displaces 2D safety curtains by offering three-dimensional zone monitoring that meets ISO 13849 robot-cell requirements. Smart infrastructure deployments, from traffic signal optimization to tolling, are climbing as municipalities seek passive, privacy-preserving sensing. Cabin-gesture control remains a small yet premium pocket where sub-one-watt modules fetch double the average selling price by eliminating physical buttons.

By Range: Mid-Range Dominates, Long-Range Gains Traction

Mid-range devices between 50 and 150 meters held 41.00% of 2025 demand because they enable pedestrian emergency braking and automated parking without exceeding the camera computation envelope. The MEMS lidar market size for long-range units, however, will expand at 21.27% CAGR as conditional highway automation requires 200-meter envelopes to secure five-second driver handover buffers. Many suppliers are therefore releasing software-defined products that widen pulse width and integration time in highway mode, effectively covering both range classes with a single bill of materials.

Short-range sensors continue to battle ultrasonic and radar incumbents on cost. Their relevance rises in rear-object detection mandates, yet price ceilings below USD 150 restrict lidar penetration. Long-range hardware faces its own trade-offs: widening field of view dilutes point density at distance, so OEMs increasingly deploy a narrow forward lidar for velocity-critical tasks while cameras cover lateral awareness. This architectural shift rebalances cost away from lidar toward on-board compute that fuses sparse but precise distance points with dense imagery.

By Wavelength: 905 nm Dominates, 1550 nm Gains on Safety and Range

The 905-nanometer class commanded 55.00% of 2025 revenue owing to smartphone-driven VCSEL economies that deliver arrays for USD 45-USD 60. However, eye-safety limits cap power output, curbing range under fog and rain. The 1550-nanometer segment, already 28% of sales, is projected to outgrow the overall MEMS lidar market at 21.56% CAGR because it tolerates 40-times higher laser power while meeting Class 1 safety. That performance edge proved decisive in Volvo and Mercedes-Benz contracts, lifting premium lidar average selling prices to USD 1 000 per unit.

Cost hurdles persist as automotive-grade InGaAs detectors carry a three-and-a-half-times premium over silicon. Vendors are therefore co-designing photonic integrated circuits that integrate modulators, splitters, and detectors on common indium phosphide substrates to cut assembly steps. An intermediate 940-nanometer tier has surfaced as a compromise, offering solar-noise rejection superior to 905 nm without InGaAs expense. Dual-wavelength prototypes remain experimental, yet they spotlight the possibility of near-field and far-field fusion inside one housing once laser drivers and optics converge on shared packages.

By Scanning Technology: MEMS Beam Steering Leads, Solid-State Architectures Emerge

MEMS beam-steering platforms represented 52% of 2025 sales because they strike a balance among field of view, resolution, and cost at current scale. Hybrid semi-solid designs, mixing MEMS motion on one axis with fixed diffusers on the other, secured just under one-quarter of revenue by reducing moving parts while holding range constant. Pure solid-state optical phased arrays and flash architectures together comprised close to 18% of value yet logged the fastest engineering investment, buoyed by silicon photonics roadmaps that promise 180-degree fields of view once grating-lobe suppression matures.

Rotary mechanical legacy units declined to 7% share, now limited to surveying and mapping. Digital lidar schemes replace analog avalanche photodiodes with CMOS-based single-photon arrays, unlocking low-voltage operation and seamless integration with edge classifiers. These advances foreshadow a modular era where the same receiver silicon can pair with MEMS, OPA, or flash transmitters, letting OEMs fine-tune field of view and range through firmware rather than hardware swaps.

Geography Analysis

Asia Pacific generated 41.29% of 2025 revenue, a lead cemented by Chinese factories that co-locate MEMS mirror etching, VCSEL packaging, and automotive qualification under one roof, shaving logistics expense by nearly one-fifth. Vertically integrated champions shipped quarter-million units domestically in 2025 and began to court European programs after earning functional-safety certificates. Japan, though smaller in volume, commanded premium pricing through trusted supply relationships with Toyota and Honda, while South Korea launched a USD 450 million subsidy plan to seed domestic MEMS capacity.

North America contributed roughly 28% of sales as Texas and California factories ramped 1550-nanometer production for premium sedans and long-haul trucks. Federal smart-infrastructure grants, worth USD 5 billion through 2026, are also seeding demand for roadside lidar that guides connected vehicles in pilot corridors. Europe followed at about 22%, driven by Germany’s Tier-1 suppliers bundling lidar with complete ADAS stacks, though slower electric-vehicle uptake constrained unit volumes versus China.

The Middle East is forecast to log a 21.96% CAGR to 2031 on the back of Saudi Arabia’s NEOM and the United Arab Emirates’ autonomous mobility targets. These projects buy durable, infrastructure-mounted sensors with decade-long lifetimes, tolerating higher unit prices and bolstering supplier margins. Africa and South America together stayed below 5% of 2025 revenue, focused on mining and agriculture robotics where lidar’s 3D mapping benefits outweigh high upfront cost.

Competitive Landscape

The MEMS lidar market remains moderately fragmented; the five largest players held a combined 34% revenue share in 2025. Chinese leaders leveraged subsidy-backed vertical integration to undercut Western pricing by up to 40%, yet global OEMs still spread risk across multiple suppliers to hedge functional-safety and geopolitical exposure. Premium-segment specialist Luminar secured large European contracts for its 1550-nanometer architecture, but scaling costs kept its operating margin negative in 2025.

Established Tier-1s, notably Valeo and Continental, embed lidar within broader sensor suites, trading sensor-level profit for platform stickiness. This approach favours joint ventures with semiconductor giants to co-develop wafers on 300-millimeter lines, targeting bill-of-materials below USD 200 by 2028. Patent activity has shifted from mechanical design toward control algorithms and photonic integration, indicating an impending pivot where firmware and beamforming software differentiate offerings more than hardware alone.

Emerging challengers are experimenting with frequency-modulated continuous-wave and fully digital receivers that measure velocity and range simultaneously, a feature trucking fleets prize for high-speed merges. Acquisition activity quickened in late 2025 as lidar pure-plays sought Tier-1 distribution channels, and Tier-1s bought intellectual property to secure future design wins. These moves foreshadow a consolidation wave that could lift the combined share of the top five suppliers above 50% by decade-end if integration hurdles are cleared.

MEMS Lidar Industry Leaders

Preciseley Microtechnology Corporation

RoboSense Technology Co., Ltd

JENOPTIK AG

Microvision, Inc.

Fraunhofer IPMS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Hesai Technology closed a CNY 2.8 billion (USD 385 million) Series E round led by CATL and Xiaomi to triple eight-inch MEMS wafer capacity by Q4 2027.

- December 2025: Luminar doubled its Iris purchase commitment with Mercedes-Benz to 300 000 units for 2026-2028 flagship models.

- November 2025: Valeo and STMicroelectronics formed a joint venture to deliver a 300-millimeter monolithic MEMS lidar wafer targeting sub-USD 200 bill-of-materials.

- October 2025: RoboSense obtained ISO 26262 ASIL-B certification for its M-series lidar, unlocking eligibility for European programs.

Global MEMS Lidar Market Report Scope

MEMS LiDAR represents a quasi-mechanical variant of LiDAR technology, wherein the laser source remains stationary. Instead, the system employs MEMS mirrors manipulated to direct and modulate the laser beam while the rest of the apparatus remains fixed.

The study tracks the revenue accrued through the sale of MEMS Lidar by various players in the global market. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The MEMS lidar market is segmented by component (transmitter module, receiver module), by end-user vertical (automotive, industrial, others), and by geography (North America, Europe, Asia Pacific, and rest of the world). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Transmitter Module |

| Receiver Module |

| Signal-Processing Electronics |

| MEMS Scanning Unit |

| Others By Component |

| Automotive |

| Industrial Automation |

| Robotics and Drones |

| Smart Infrastructure |

| Others End-User Industry |

| Short Range (Less than equal to 50 m) |

| Mid-Range (50-150 m) |

| Long Range (More than equal to 150 m) |

| 905 nm Class |

| 940 nm VCSEL Class |

| 1550 nm Class |

| Multi-Spectral / Others |

| MEMS Beam Steering |

| Hybrid Semi-Solid |

| Pure Solid-State (OPA / Flash) |

| Mechanical Rotary Legacy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Transmitter Module | |

| Receiver Module | ||

| Signal-Processing Electronics | ||

| MEMS Scanning Unit | ||

| Others By Component | ||

| By End-User Industry | Automotive | |

| Industrial Automation | ||

| Robotics and Drones | ||

| Smart Infrastructure | ||

| Others End-User Industry | ||

| By Range | Short Range (Less than equal to 50 m) | |

| Mid-Range (50-150 m) | ||

| Long Range (More than equal to 150 m) | ||

| By Wavelength | 905 nm Class | |

| 940 nm VCSEL Class | ||

| 1550 nm Class | ||

| Multi-Spectral / Others | ||

| By Scanning Technology | MEMS Beam Steering | |

| Hybrid Semi-Solid | ||

| Pure Solid-State (OPA / Flash) | ||

| Mechanical Rotary Legacy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the MEMS lidar market in 2026 and what growth rate is expected through 2031?

The market reached USD 1.34 billion in 2026 and is projected to climb to USD 3.34 billion by 2031, reflecting a 20.04% CAGR.

Which component segment commands the highest share?

Transmitter modules led with 46.01% of 2025 revenue, driven by mature VCSEL and edge-emitter production lines.

What segment will grow fastest by end-user?

Robotics and drones are forecast to expand at a 21.89% CAGR to 2031 as warehouses and aerial delivery fleets scale adoption.

Which wavelength is gaining momentum and why?

1550-nanometer systems are growing at 21.56% CAGR because eye-safety rules allow higher laser power, extending range in poor weather.

Which region will post the strongest growth?

North America is expected to post the strongest growth through 2031, supported by expanding premium-vehicle and smart-infrastructure deployments.

What is the main cost barrier to wider adoption?

Automotive-grade modules still cost USD 800-USD 1 200 due to laser arrays, MEMS assemblies, and stringent qualification tests, limiting mass-market penetration.

Page last updated on: