Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

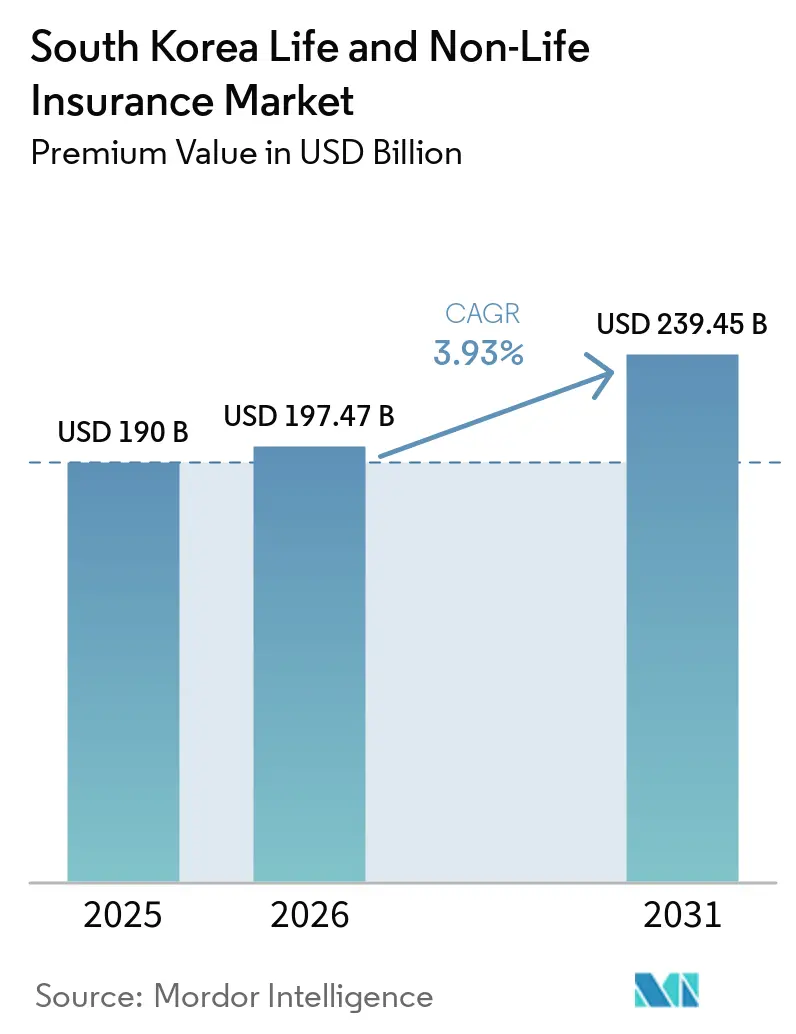

| Base Year Market Size (2025) | USD 190 Billion |

| Market Size (2026) | USD 197.47 Billion |

| Market Size (2031) | USD 239.45 Billion |

| Growth Rate (2026 - 2031) | 3.93% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Life and Non-Life Insurance Market Analysis by Mordor Intelligence

The South Korea Life And Non-Life Insurance Market size in terms of premium value is expected to increase from USD 190 billion in 2025 to USD 197.47 billion in 2026 and reach USD 239.45 billion by 2031, growing at a CAGR of 3.93% over 2026-2031.

Steady growth reflects the market’s response to an aging population, the 2024 shift to K-ICS capital standards, and IFRS-17’s real-time profit recognition, which together force insurers to prioritize protection-type products while managing stricter solvency rules. Health non-life insurance leads to short-term expansion as the state looks to private carriers to narrow National Health Insurance Service (NHIS) deficits. At the same time, digital distribution accelerates through embedded channels on e-commerce, fintech, and mobility platforms, reshaping customer acquisition costs. Overseas expansion gains urgency: Korean insurers earned USD 159.1 million combined profit abroad in 2024 after 2023 losses[1]Asia Insurance Review, “Korean Insurers Swing to Overseas Profit in 2024,” asiainsurancereview.com, highlighting saturation at home. Regulatory support for higher-yield, unit-linked products further diversifies revenue streams, though low interest rates still pressure investment income.

Key Report Takeaways

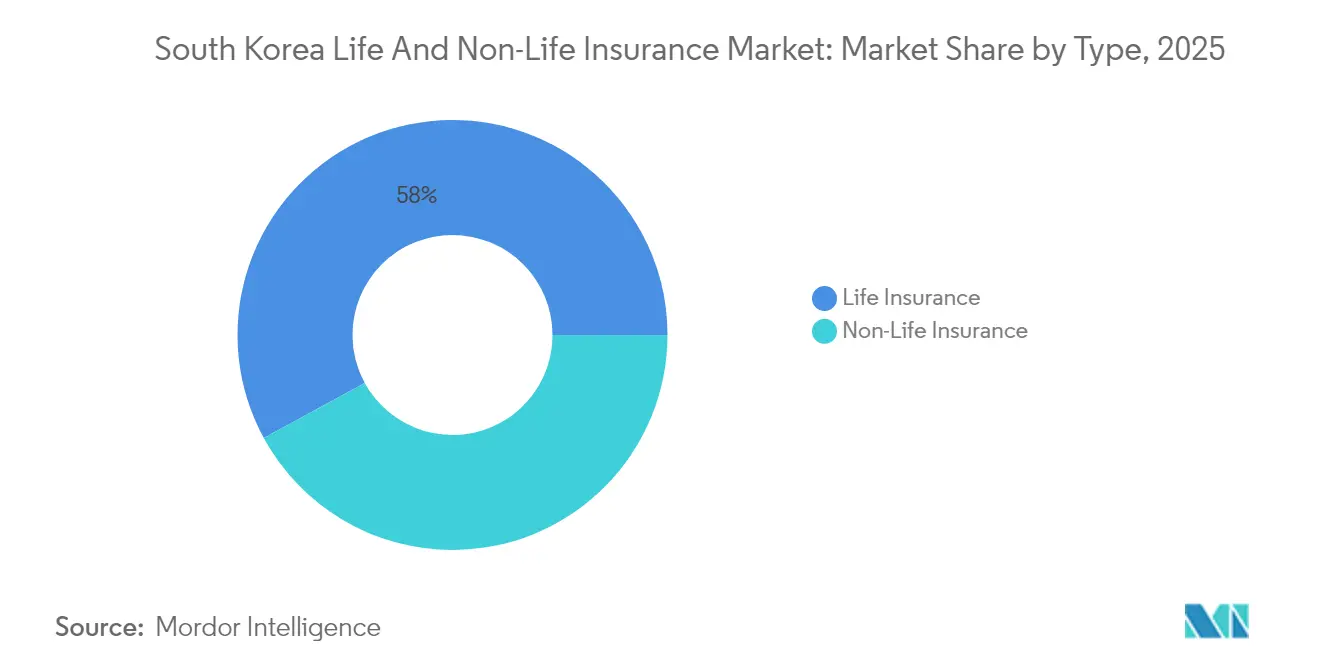

- By product type, life insurance held a 57.95% share of the South Korea life and non-life insurance market in 2025, while health non-life insurance is advancing at a 6.43% CAGR to 2031.

- By distribution channel, the agency force controlled 48.25% of the South Korea life and non-life insurance market share in 2025; online/direct sales are growing at a 12.05% CAGR through 2031.

- By end user, individual customers accounted for 85.05% of the South Korea life and non-life insurance market size in 2025; the corporate segment is set to expand at a 7.10% CAGR by 2031.

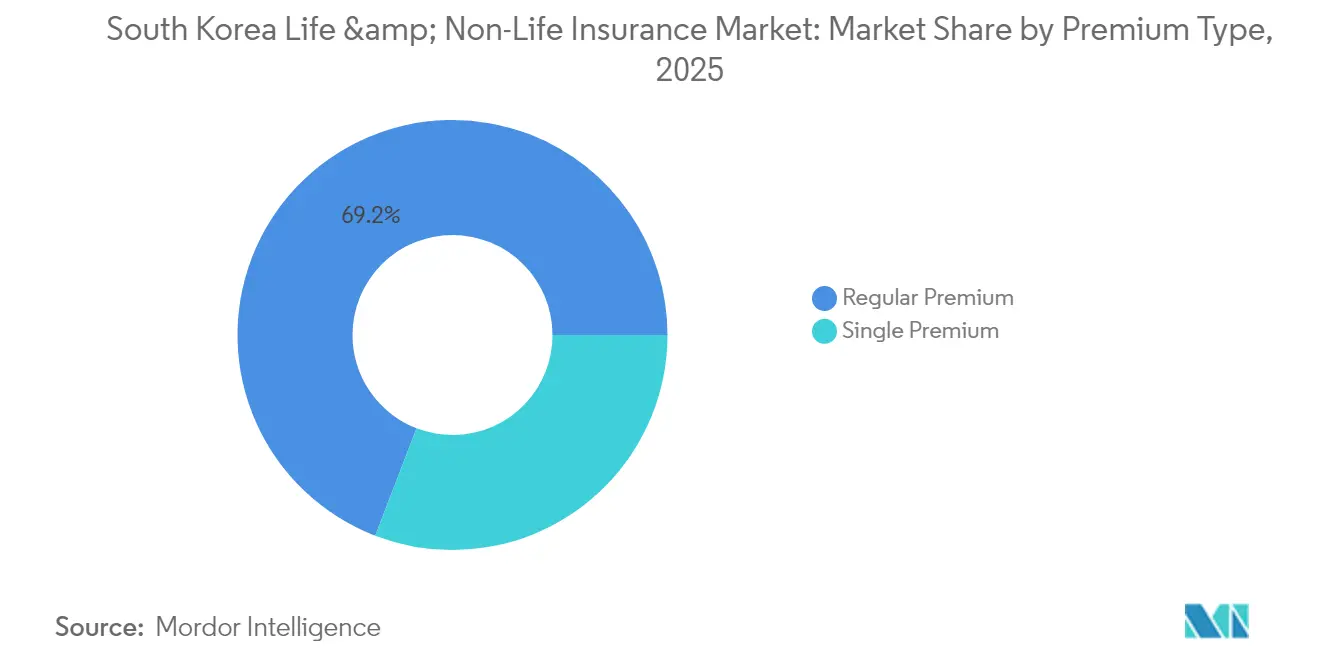

- By premium type, regular premiums represented 69.15% of the South Korea life and non-life insurance market size in 2025, while single premiums are growing by 5.17% annually to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Life and Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid aging population raises annuity demand | +1.2% | National, Seoul area | Long term (≥ 4 years) |

| Government push for private health insurance | +0.8% | National, urban | Medium term (2-4 years) |

| Digital-savvy consumers lift embedded and online sales | +0.6% | National, Seoul area | Short term (≤ 2 years) |

| Mandatory motor liability & EV uptake | +0.5% | National, metro EV hubs | Medium term (2-4 years) |

| Cyber & liability demand under stricter PIPA | +0.4% | Seoul, Chungcheong | Short term (≤ 2 years) |

| Capital-market liberalization elevates unit-linked appeal | +0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapidly Aging Population Fueling Demand for Retirement Annuities and Whole Life Products

Long-term demographic change will double the senior population by 2050, prompting a pivot toward longevity-focused annuities even as whole-life policy sales fell 45% between 2020-2024. Financial authorities now allow policyholders to convert death benefits into monthly income; 339,000 policies worth USD 9.1 billion qualify, signaling regulatory support for flexible payout structures. Yet longevity risk squeezes capital under K-ICS, challenging insurers to fine-tune asset-liability management in a low-rate backdrop. National Pension System dropout rates among low-income seniors amplify private annuity uptake, widening the South Korea life and non-life insurance market. Carriers that master capital-efficient longevity products stand to capture an outsized share in the South Korea life and non-life insurance market.

Government Push for Private Health Insurance Amid Rising NHIS Funding Gap

Annual healthcare spending reached USD 92 billion after rising 52.9% from 2010-2019, overwhelming NHIS finances. The 2025 FSC work plan prioritizes senior-friendly coverage, encouraging insurers to plug public-sector gaps with long-term care and specialized treatment policies[2]Financial Services Commission, “2025 Work Plan for the Insurance Sector,” FSC, fsc.go.kr. Product design must avoid adverse selection while staying affordable to middle-income households, positioning health non-life as the fastest-growing slice of the South Korea life and non-life insurance market. Balancing commercial gain with universal-coverage ethics defines strategic success in the South Korea life and non-life insurance market.

Digital-Savvy Population Accelerating Embedded & Online Policy Purchases

Pacific Life Re and Kakao Pay Insurance have teamed up to launch app-exclusive insurance covers, capitalizing on South Korea's impressive 94% smartphone penetration. In a notable industry shift, Samsung Fire & Marine has exited the bancassurance sector after a 21-year stint. This move is particularly telling, given the revenue implications and the penalties imposed by IFRS-17 regulations on bank-distributed savings-linked products.

Relaxed investment rules permit overseas assets and alternatives, boosting unit-linked appeal and fee income. However, market-value accounting under K-ICS exposes volatility directly to solvency metrics, requiring superior risk controls. Firms that balance yield and capital efficiency can grow their share in the South Korea life and non-life insurance market.

Mandatory Motor Liability and Growing EV Fleet Boosting Motor Premium

Relaxed investment rules permit overseas assets and alternatives, boosting unit-linked appeal and fee income. However, market-value accounting under K-ICS exposes volatility directly to solvency metrics, requiring superior risk controls. Firms that balance yield and capital efficiency can grow their share in the South Korea life and non-life insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-low interest rates crimp investment income | -0.9% | National | Long term (≥ 4 years) |

| Tighter K-ICS & IFRS-17 raise capital strain | -0.7% | National, smaller insurers | Medium term (2-4 years) |

| High distribution costs in agency model | -0.5% | Rural, suburban | Medium term (2-4 years) |

| Urban saturation slows savings-policy growth | -0.4% | Seoul metro | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ultra-Low Interest-Rate Environment Compressing Investment Income

In 2024, the net income for the sector reached USD 10.32 billion. This uptick was primarily driven by investment gains, which counterbalanced underwhelming performance in motor underwriting. However, it's worth stating that the margins on guaranteed products are diminishing. As the challenge of reinvestment risk looms, stemming from long liabilities being matched with low-yield assets. There is a noticeable strategic shift towards pure protection covers in both the life and non-life insurance markets of South Korea. The South Korean insurance market is also witnessing increased competition, with insurers focusing on innovative product offerings and digital transformation to enhance customer experience and operational efficiency. Additionally, regulatory changes are influencing market dynamics, compelling insurers to adapt their strategies to remain compliant while ensuring profitability.

Tightened K-ICS & IFRS-17 Rules Creating Capital Strain

In 2023, K-ICS was launched, prompting nineteen carriers to seek relief. To alleviate systemic stress, the FSC subsequently adjusted the recommended solvency ratio, setting it between 130% and 140%[3]Fitch Ratings, “K-ICS Adjustment Eases Capital Pressure on Korean Insurers,” Fitch Ratings, fitchratings.com. The introduction of IFRS-17, with its emphasis on fair-value liabilities, has made earnings more susceptible to market fluctuations. This shift has prevented aggressive expansion while promoting consolidation within the industry. In the South Korea life and non-life insurance market, smaller firms grapple with disproportionately high-cost burdens, which include compliance expenses, technology upgrades, and operational inefficiencies. These challenges further widen the gap between smaller and larger players, intensifying competition and driving market consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Life Insurance Dominance Faces Health Disruption

Life insurance captured 57.95% of the South Korea life and non-life insurance market in 2025, whereas health non-life is growing fastest at 6.43% CAGR toward 2031. Pension-linked contracts retain significant weight, but whole-life demand waned as longevity risk prompted a pivot to term covers. Non-life segments also gain from natural disaster awareness and compulsory motor lines. The South Korea life and non-life insurance market size for health products is expanding as NHIS funding gaps widen.

IFRS-17 favors protection income and shifting sales mixes. Government incentives for long-term care and specialized treatment drive penetration beyond savings-centric plans. Motor transformation around EVs forces underwriters to adopt new risk models. Insurers that re-price guarantees and focus on health capture incremental revenue in the South Korea life and non-life insurance market.

By Distribution Channel: Agency Resilience Amid Digital Acceleration

Agency force retained a 48.25% share in 2025, underscoring trust in personal advice. At the same time, embedded and online channels posted a 12.05% CAGR, reflecting a digital pivot accelerated by pandemic behavior shifts. Direct sites cut acquisition costs and speed onboarding, which is critical under capital constraints from K-ICS. The South Korea life and non-life insurance market size attached to digital channels is projected to double by 2031.

Samsung Fire & Marine’s bancassurance exit spotlights savings-product headwinds. Affinity ties such as fintech-aligned micro-policies flourish. Yet, strict disclosure rules keep human intermediaries relevant for complex products. Insurers are calibrating hybrid models to reach both urban digital adopters and rural agency loyalists inside the South Korea life and non-life insurance market.

By Premium Type: Regular Premium Stability Supports Single Premium Growth

Regular payments held a 69.15% share in 2025, offering a predictable cash flow crucial for K-ICS asset-liability matching. Single premiums are climbing 5.17% yearly, drawing lump-sum investors near retirement seeking immediate cover or tax breaks. The South Korea life and non-life insurance market size for single-premium products benefits from capital-market liberalization, which widens investment choices in unit-linked wrappers.

IFRS-17 earnings patterns favor steady recognition, keeping insurers invested in regular contributions. Automated digital debits simplify collection and improve persistency, aligning with embedded sales models. However, richer older cohorts still prefer one-off payments for simplicity, ensuring mixed growth across premium types in the South Korea life and non-life insurance market.

By End User: Individual Dominance with Corporate Acceleration

Individuals provided 85.05% of premium income in 2025, but corporate lines are rising 7.1% annually through 2031 on the back of PIPA-driven liability mandates. SMEs now pool demand for cyber, cargo, and credit products, widening commercial risk portfolios. The South Korea life and non-life insurance market share attached to corporate policies will, therefore, expand, though not yet rival individual totals.

Data-privacy fines and mandatory EV-charger cover fuel growth in specialty commercial lines. International operations of Korean conglomerates also require coordinated global programs, prompting insurers to scale regional footprints. This interplay of domestic regulation and outbound expansion underscores the strategic relevance of the corporate segment in the South Korea life and non-life insurance market.

Geography Analysis

Seoul Capital Area remains the premium heartland with the highest penetration, but saturation compresses margins as rival carriers undercut pricing. Dense fintech ecosystems spur online policy uptake, letting innovative players expand their share across the South Korean life and non-life insurance market.

Chungcheong and Gyeongsang provinces show rising industrial activity that drives commercial insurance gains, particularly in property and cargo. Lower household penetration offers a runway for personal covers, aided by regional development incentives. The South Korea life and non-life insurance market size in these regions is forecast to outpace the national average CAGR through 2031.

Jeolla, Gangwon, and Jeju rely on agriculture and tourism, creating needs for seasonal business, travel, and catastrophe covers. Aging and depopulation in rural pockets compel eldercare and micro-insurance solutions delivered through hybrid agency-digital models. Regional EV adoption spreads outward from metro hubs, diversifying motor risk pools and distribution footprints across the South Korea life and non-life insurance market.

Competitive Landscape

In South Korea's insurance landscape, the top five life insurers and non-life players command over half of the written premiums, indicating a moderate concentration in both sectors. Samsung Life, Kyobo Life, and Hanwha Life lead the life insurance domain, while Samsung Fire & Marine, Meritz Fire & Marine, and DB Insurance dominate non-life. Notably, Meritz has surpassed DB in profitability thanks to its emphasis on long-term policies.

Insurers are pivoting towards digital transformation and global outreach. A partnership with AWS equips Kyobo Life with scalable analytics, and Hanwha Life's acquisition of a U.S. brokerage enhances its global distribution network. In a notable turnaround, insurers collectively reaped USD 159.1 million from Vietnam and Indonesia in 2024, marking a rebound from previous overseas losses and hinting at new growth avenues.

With capital pressures from K-ICS, M&A activities are on the rise. The five leading non-life carriers even cooperated to support MG Non-Life Insurance, showcasing a dual focus on managing systemic risks and a keen interest in consolidation. Currently, competitive advantages are increasingly derived from AI-driven underwriting, expansive embedded channels, and agile product designs that resonate with IFRS-17 economics, all of which are redefining the dynamics in South Korea's insurance market.

South Korea Life and Non-Life Insurance Industry Leaders

Samsung Life Insurance Co., Ltd.

Kyobo Life Insurance Co., Ltd.

Hanwha Life Insurance Co., Ltd.

Samsung Fire & Marine Insurance Co., Ltd.

DB Insurance Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Korea’s five largest non-life insurers created a council to acquire MG Non-Life Insurance assets, with KDIC support to shore up the firm’s 4.1% solvency ratio.

- April 2025: The FSC reduced the K-ICS solvency target to 130-140% and introduced a core-capital ratio, easing compliance costs.

- January 2025: Shinhan Bank Vietnam partnered with Petrolimex Insurance to distribute non-life products in Vietnam.

- November 2024: Pacific Life Re and Kakao Pay Insurance signed an MoU for app-exclusive health covers.

- June 2024: Korea Trade Insurance Corp. agreed to provide up to USD 1 billion in financing for Korean firms in Vietnamese gas projects.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Korean life and non-life insurance market as the gross written premiums generated in the country by licensed insurers across life protection, savings, annuity, and all property and casualty lines, including motor, health, liability, marine, aviation, agriculture, travel, and accident, sold through agency, bancassurance, broker, direct, and digital channels.

Scope Exclusions: Reinsurance transactions, inward foreign placements, third-party administrator revenue, and micro-policies below KRW 15,000 a year are excluded so the focus stays on the core primary insurance pool.

Segmentation Overview

- By Type

- Life Insurance

- Term Life

- Whole Life

- Endowment

- Annuities / Pension

- Unit-Linked / Variable

- Non-Life Insurance Product

- Motor

- Health

- Property

- Liability

- Marine & Aviation

- Crop & Agriculture

- Travel

- Accident & Supplemental

- Life Insurance

- By Distribution Channel

- Agency Force

- Bancassurance

- Brokers

- Direct / Offline

- Digital / Online Direct

- Affinity & Embedded Partnerships

- By Premium Type

- Regular Premium

- Single Premium

- By End User

- Individuals

- Corporates

- SME & Affinity Groups

- By Region

- Seoul Capital Area

- Chungcheong Region

- Jeolla Region

- Gyeongsang Region

- Gangwon Province

- Jeju Province

Detailed Research Methodology and Data Validation

Primary Research

We interviewed underwriting managers, distribution heads, actuaries, and regulators across Seoul, Busan, and Jeju. Their insights clarified channel penetration, product mix shifts after IFRS-17 and K-ICS, and average premium moves that desk research alone could not quantify.

Desk Research

Mordor analysts mapped premium flows using publicly available data from the Financial Supervisory Service statistics portal, Korea Insurance Research Institute outlooks, Bank of Korea macro tables, National Health Insurance Service claims files, and yearbooks issued by the General Insurance Association of Korea. Company filings, investor decks, press coverage captured via Dow Jones Factiva, and issuer snapshots from D&B Hoovers rounded out carrier-level intelligence. The sources named are illustrative; numerous additional open documents underpinned data checks and trend confirmation.

Market-Sizing and Forecasting

The model starts with a top-down reconstruction of direct written premiums reported by regulators, which are then split by product, channel, and region using shares validated during interviews. Selective bottom-up tests, carrier roll-ups, sampled average premium multiplied by in-force policies, and channel checks temper outliers. Key variables such as GDP growth, old-age dependency ratio, registered vehicle parc, medical CPI, and digital sales penetration feed a blended multivariate regression and ARIMA forecast to 2030. When product-level gaps appear, aligned growth deltas from comparable carriers are applied after expert review.

Data Validation and Update Cycle

Outputs pass three rounds of anomaly screening, peer review, and director sign-off. We rerun variance scans against fresh FSS releases, macro revisions, and material events; full refreshes occur annually, while mid-cycle updates trigger whenever inputs move beyond preset thresholds.

Why Our South Korea Life and Non-Life Insurance Baseline Stands Firm

Published estimates often differ because providers apply varied premium definitions, channel coverage, and refresh cadences.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 190 B (2025) | Mordor Intelligence | |

| USD 161 B (2024) | Global Consultancy A | Counts only direct life and motor lines, omits long-term accident and embedded digital covers |

| USD 148 B (2024) | Industry Association B | Uses 2021 FX rate and excludes IFRS-17 reclassification impacts |

| USD 196 B (2024) | Research Publisher C | Combines primary and reinsurance premiums and applies a uniform 4.7 percent growth assumption |

Once scope, currency practice, and capital standard adjustments are aligned, figures converge near our estimate. This is where Mordor Intelligence gives decision-makers a balanced, transparent baseline rooted in clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the South Korea life and non-life insurance market?

The market stands at USD 197.47 billion in 2026 and is forecast to reach USD 239.45 billion by 2031.

Which segment is growing fastest within the market?

Health non-life insurance is projected to expand at a 6.43% CAGR through 2031 as the government relies more on private carriers to supplement NHIS coverage gaps.

How are new capital rules influencing insurers?

K-ICS and IFRS-17 heighten capital strain, pushing firms to favor protection-type products, improve risk management, and explore overseas growth.

Why are online and embedded channels important?

Digital distribution is growing at 12.05% CAGR due to lower acquisition costs and consumer preference for app-based insurance, reshaping competitive dynamics.

What drives the rise in cyber liability insurance?

Stricter enforcement of the Personal Information Protection Act mandates liability coverage, boosting corporate demand for cyber and data-breach policies.

How are low interest rates affecting insurers’ profitability?

Ultra-low yields compress investment income, forcing insurers to lean more on underwriting profit and diversify toward higher-yield, unit-linked products.

Page last updated on: