Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

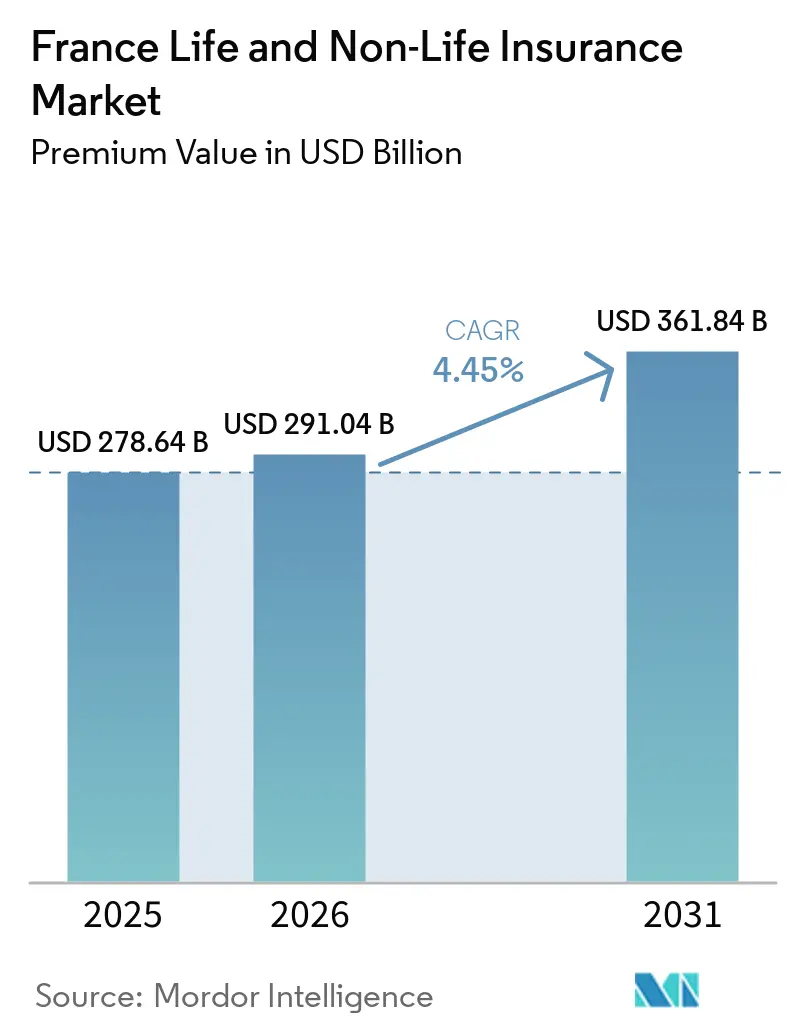

| Base Year Market Size (2025) | USD 278.64 Billion |

| Market Size (2026) | USD 291.04 Billion |

| Market Size (2031) | USD 361.84 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Life and Non-Life Insurance Market Analysis by Mordor Intelligence

The France Life And Non-Life Insurance Market size in terms of premium value is projected to expand from USD 278.64 billion in 2025 and USD 291.04 billion in 2026 to USD 361.84 billion by 2031, registering a CAGR of 4.45% between 2026 to 2031.

Solid household savings habits, expanding mandatory coverage, and sustained bancassurance dominance underpin this growth even as IFRS-17 introduces earnings volatility. Direct-to-consumer digital models are scaling quickly, spurring sharper price competition and compressing acquisition costs. Heightened climate-related claims and persistently low real bond yields are pressuring underwriting discipline, nudging insurers to diversify toward unit-linked products and capital-light fee income. Strategic M&A continues as incumbents seek scale and technology capabilities to defend market share against agile InsurTech entrants[1]Reuters Staff, “AXA to Buy 51% of Italy’s Prima Assicurazioni,” reuters.com .

Key Report Takeaways

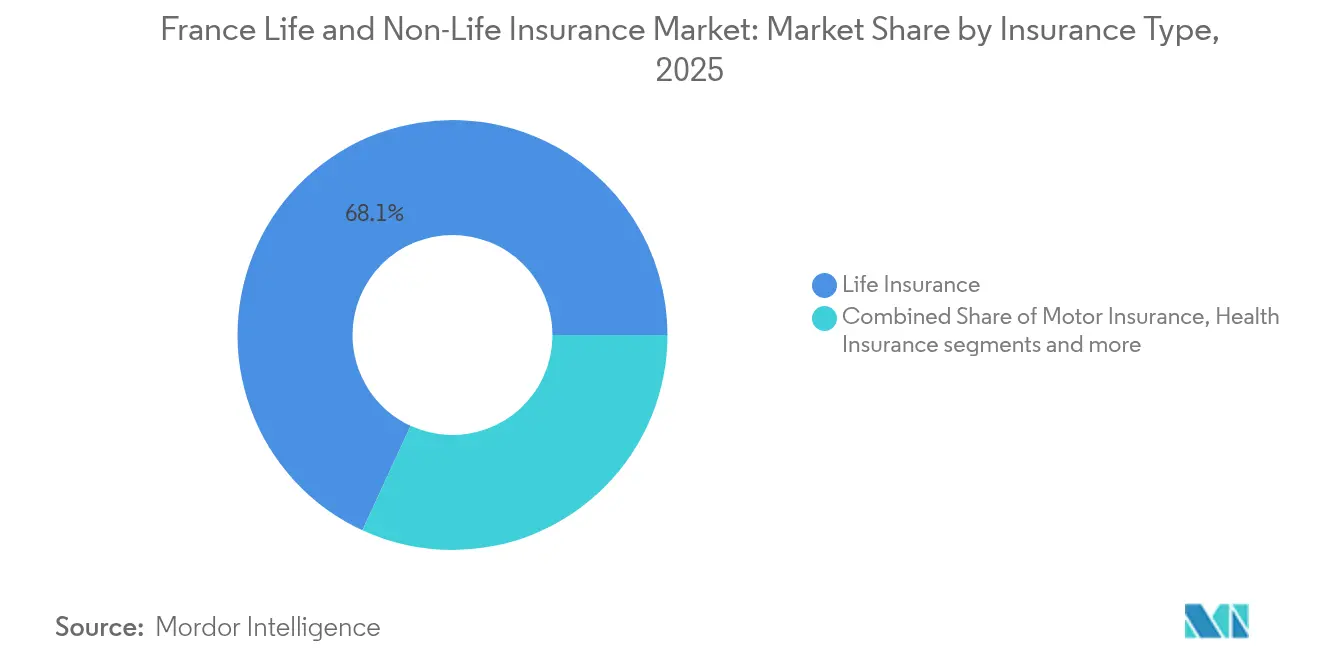

- By insurance type, life accounted for 68.12% of the France life & non-life insurance market share in 2025; non-life is forecast to advance at a 4.53% CAGR through 2031.

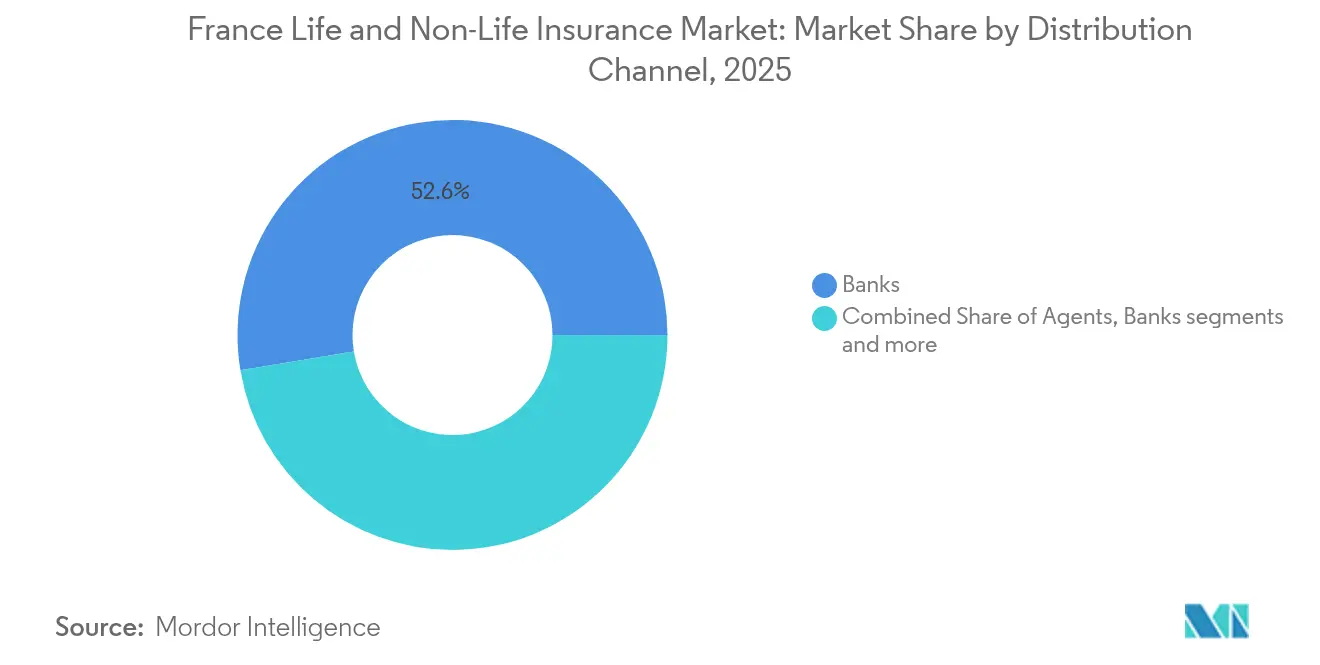

- By distribution channel, banks led with 52.63% revenue share of the France life & non-life insurance market in 2025, direct sales are projected to grow at a 3.45% CAGR to 2031.

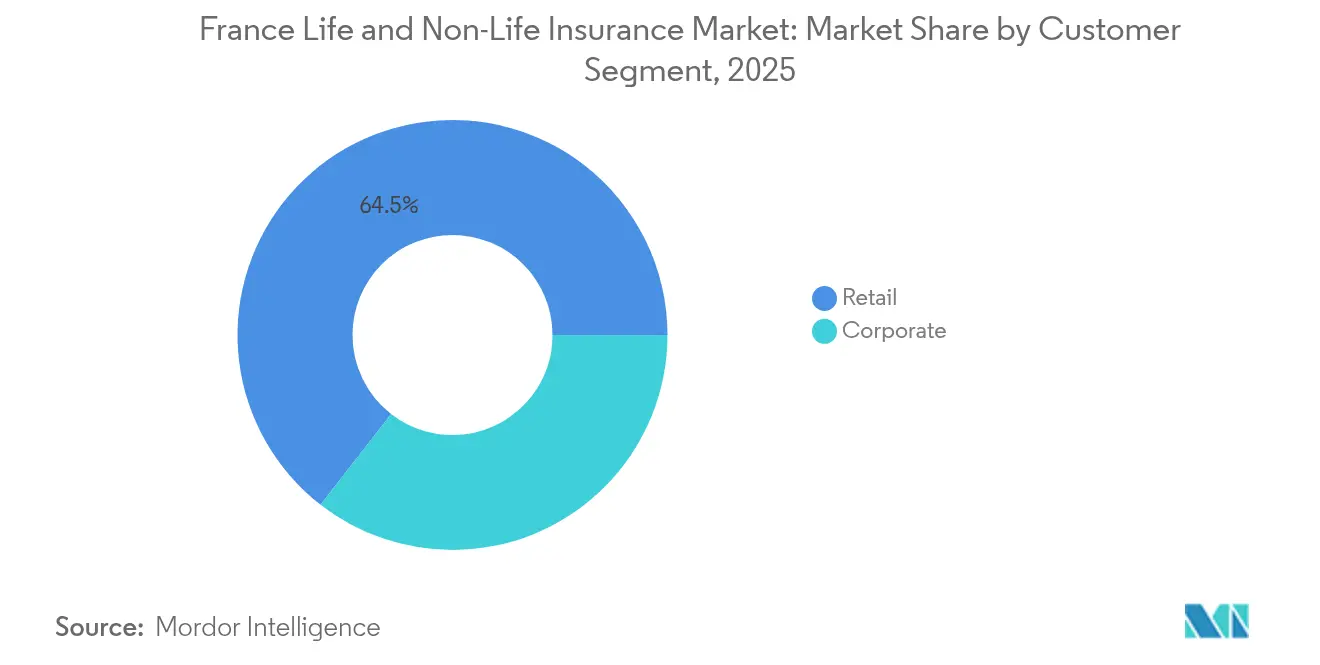

- By customer segment, retail captured 64.48% of the France life & non-life insurance market size in 2025, and corporate lines are expected to expand at a 3.85% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Life and Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising bancassurance dominance | +0.8% | France, with spillover to Belgium, partnerships | Medium term (2-4 years) |

| Shift from euro-funds to unit-linked savings | +0.6% | France's core, limited international exposure | Long term (≥ 4 years) |

| Mandatory motor & health coverage expansion | +0.7% | France national, regional implementation variations | Short term (≤ 2 years) |

| Digital-first insurers & InsurTech partnerships | +0.5% | France's primary European expansion was secondary | Medium term (2-4 years) |

| Emerging pay-per-mile auto propositions | +0.3% | France's urban centers, rural areas lagging | Long term (≥ 4 years) |

| ESG-linked premium incentives | +0.4% | France national, EU regulatory alignment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Bancassurance Dominance

Banks controlled 53.23% of distribution in 2024, leveraging deep customer data, integrated advisory platforms, and ACPR-approved compliance structures. Their embedded position inside everyday banking journeys lowers acquisition costs and extends lifetime value across savings, credit, and protection touchpoints. Crédit Agricole Assurances exemplifies the scale benefits, pairing branch traffic with mobile banking cross-sell to widen household wallet share. Capital efficiency also improves because banks can pool liquidity from deposits and life premiums. Continued consolidation among regional mutual banks points to further entrenchment of the bancassurance model over the medium term.

Shift from Euro-Funds to Unit-Linked Savings

Sub-1% guaranteed rates on traditional euro funds drove savers to unit-linked contracts despite market volatility, helping insurers trim duration mismatches[2]Moody’s Investors Service, “CNP Assurances Credit Opinion, June 2024,” moodys.com. The 2025 Loi Industrie Verte mandates minimum allocations to non-listed green assets, compelling product redesign toward flexible investment sleeves that transfer market risk to policyholders while meeting ESG targets. This migration boosts fee income and lowers capital charges under Solvency II. It also positions insurers as facilitators of national sustainability financing, enhancing their social license to operate.

Mandatory Motor & Health Coverage Expansion

Greater enforcement against uninsured drivers lifted average motor premiums to USD 567.6 (EUR 545) in 2025, a 5% yearly rise amid higher claims inflation[3]LeLynx.fr, “Tarifs Assurance Auto 2025,” lelynx.fr. . Parallel reforms extending employer-paid health benefits to civil servants opened a sizable pool of 65,000 lives recently won by Alan, a digital-first health insurer. These mandates widen the France life & non-life insurance market, yet they heighten competitive intensity as carriers battle on pricing and service to secure newly compulsory risks. Fast product adaptation and efficient claims automation are becoming decisive success factors.

Digital-First Insurers & InsurTech Partnerships

Alan’s USD 520.7 million (EUR 500 million) annualized revenue run-rate in 2024, up 48% year over year, showcases the viability of app-centric, subscription-like insurance propositions. Strategic partnerships such as its distribution pact with Belgium’s Belfius Bank illustrate a hybrid growth model that fuses technology agility with incumbent reach. Incumbents are responding by co-developing APIs, deploying AI for fraud detection, and buying minority stakes in promising startups. This collaborative ecosystem accelerates product cycles, personalizes underwriting, and keeps switching costs low for consumers, fueling overall market expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nat-cat loss inflation & drought risk | -0.9% | France is a national, the Mediterranean regions most exposed | Short term (≤ 2 years) |

| Persistently low real bond yields | -0.6% | France's core, European monetary policy is dependent | Long term (≥ 4 years) |

| IFRS-17 capital volatility on life portfolios | -0.5% | France national, EU regulatory harmonization | Medium term (2-4 years) |

| Rise in uninsured drivers despite enforcement | -0.3% | France's national urban concentration is higher | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Nat-Cat Loss Inflation & Drought Risk

Exceptional floods and prolonged droughts are inflating loss ratios and challenging traditional catastrophe models. Drought-related subsidence events affect wide areas simultaneously, limiting diversification benefits and pushing combined ratios above historical norms. Insurers are rebuilding pricing models with richer climate data sets and advocating for stronger prevention incentives. Government-backed natural disaster compensation schemes temper consumer impact but raise uncertainty over future levy adjustments. The resulting volatility weighs on underwriting appetite for property risks in exposed regions.

IFRS-17 Capital Volatility on Life Portfolios

Transition to IFRS-17 has revalued contract service margins, exposing earnings swings tied to discount rate movements. CNP Assurances disclosed EUR 16.9 billion CSM at end-2023, underscoring the scale of deferred profit recognition. The standard forces granular tracking of cash flows and onerous data governance, elevating operational costs. Management is accelerating the pivot toward capital-lite unit-linked contracts to smooth volatility. While transparency benefits investors, near-term uncertainty may restrain product innovation until systems fully stabilize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Life Dominance Faces Non-Life Acceleration

Life products controlled 68.12% of the France life & non-life insurance market in 2025, underpinned by favorable tax treatment and bancassurance sales. Yet non-life premiums are set to compound at a 4.53% CAGR, narrowing the gap as mandatory motor, health, and property lines outpace traditional savings. Motor remains the largest non-life class; higher accident frequency and component costs drove 5% annual premium growth, contributing a substantial lift to the France life & non-life insurance market size in 2025. Property growth is spurred by climate-linked product redesigns that bundle prevention services with coverage, while professional liability demand rises with expanding knowledge-economy employment.

The Loi Industrie Verte accelerates ESG integration by requiring green asset quotas within life policies, blending protection with investment objectives. This blurring of product boundaries enhances cross-sell between life and non-life portfolios. Insurers adept at modular policy architecture can pivot quickly between guarantee structures, capturing incremental France life & non-life insurance market share as consumer preferences evolve. Conversely, carriers slow to retire costly legacy products risk margin erosion and capital strain under stricter solvency charges.

By Distribution Channel: Banks Lead While Direct Sales Surge

Bancassurance retained 52.63% control of the France life & non-life insurance market in 2025, benefiting from branch networks and embedded digital banking journeys. Direct-to-consumer channels, however, will post the fastest 3.45% CAGR to 2031 as consumers embrace instant policy issuance and price transparency. These trends enlarge the overall France life & non-life insurance market size by drawing younger, tech-savvy segments previously underinsured.

Traditional agents and brokers are repositioning as risk advisors in complex commercial lines, integrating API connectivity for instant quotes. Hybrid models mixing online onboarding with human advisory for high-ticket contracts are gaining traction, allowing carriers to balance cost efficiency and customer intimacy. Successful players orchestrate omnichannel experiences so policyholders can fluidly switch between mobile apps, call centers, and branch visits without data loss.

By Customer Segment: Retail Stability Meets Corporate Dynamism

Retail policyholders produced 64.48% of 2025 premiums, reflecting entrenched life savings habits and mandatory personal lines. Corporate demand is climbing to a 3.85% CAGR as businesses upgrade protection against cyber, environmental, and supply-chain risks. Small and medium enterprises, once deterred by paperwork, are flocking to simplified digital portals that quote and bind cover within minutes, broadening France's life & non-life insurance market reach.

Mutual and cooperative insurers such as MAIF, now serving 4.1 million members with EUR 23 billion in AUM, illustrate the power of community branding coupled with efficient digital engagement. In group health, Alan’s win of a large civil-service tender signals that data-driven health management and user-friendly apps resonate with employers seeking productivity gains. Corporate lines’ trajectory prompts carriers to invest in risk-engineering services and sector-specific underwriting expertise to deepen share of wallet.

Geography Analysis

Metropolitan France comprises the entire France life & non-life insurance market, yet regional contrasts shape distribution choices and risk pricing. Paris, Lyon, and Marseille deliver the bulk of premium volume, supported by higher disposable income, dense bancassurance footprints, and rapid InsurTech adoption. In contrast, rural departments still rely on branch-based consultation, favoring the embedded trust of local savings banks. These patterns influence acquisition strategies, with digital-only insurers allocating marketing budgets toward urban millennials while partnership-oriented carriers fortify regional mutual ties.

Risk exposure also varies geographically. Mediterranean departments face soaring drought-linked subsidence claims, leading to differentiated property premium surcharges. Atlantic coastal zones contend with flood frequency spikes, spurring insurers to deploy satellite imagery and IoT sensors for proactive loss mitigation. Such granular underwriting supports a balanced France life & non-life insurance market size by preserving insurability without blanket rate hikes.

France’s Solvency II alignment and participation in EU passporting agreements foster cross-border competition. AXA’s 51% purchase of Italy’s Prima illustrates outbound expansion enabled by strong domestic solvency ratios and management bandwidth. These outward moves reinforce domestic competency in digital claims handling and modular product design as lessons flow back into home portfolios. Consequently, even purely domestic policyholders indirectly benefit from the innovation imported through multinational activity.

Competitive Landscape

The market exhibits moderate concentration. Incumbents such as AXA, CNP Assurances, and Crédit Agricole Assurances wield bancassurance scale, brand trust, and diversified capital buffers to defend their share. Newer digital challengers like Alan and Luko penetrate specific verticals with low-cost cloud infrastructures and friction-free customer journeys.

Strategic moves center on technology investment, ESG positioning, and inorganic growth. AXA’s acquisition of Prima widens its embedded-insurance capabilities in southern Europe and unlocks telematics data for usage-based motor products. BNP Paribas Cardif is integrating asset-management boutiques to enrich unit-linked offerings, capturing fee income while meeting sustainable-finance disclosure rules. Meanwhile, mutual groups pool IT resources via shared platforms to preserve community roots while achieving scale economies.

Innovation pipelines focus on AI-driven underwriting, parametric climate covers, and health ecosystems that bundle wellness coaching with reimbursement. Collaborative sandboxes run by ACPR accelerate prototype testing under supervisory guidance, enabling both incumbents and startups to launch compliant propositions faster than in neighboring markets. As technology levels the playing field, differentiation increasingly hinges on brand credibility, claims empathy, and the ability to tailor coverage to emerging lifestyles such as shared mobility and remote work.

France Life and Non-Life Insurance Industry Leaders

AXA SA

Crédit Agricole Assurances

CNP Assurances

Groupama

Crédit Mutuel Alliance Fédérale (GACM)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: AXA agreed to acquire a 51% stake in Italy’s Prima, expanding its southern European retail franchise.

- August 2025: AXA reported H1 2025 gross written premiums of EUR 64.3 billion, up 7% from H1 2024, with underlying earnings of EUR 4.5 billion, up 6%.

- March 2025: France Assureurs announced life insurance assets surpassed EUR 2 trillion in January 2025, the highest on record.

- January 2025: Alan disclosed 2024 annualized recurring revenue topping EUR 500 million, while trimming net losses to EUR 54 million.

France Life and Non-Life Insurance Market Report Scope

Life insurance provides a lump sum amount of the sum assured at the time of maturity or in case of the death of the policyholder. Non-life insurance policies offer financial protection to a person for health issues or losses due to damage to an asset. The France life & non-life insurance market is segmented by insurance type (life insurance (individual and group), non-life insurance (motor, home, health, and other non-life insurance)), and by distribution channel (direct, agency, banks, online, and other distribution channels). The report offers market size and forecasts for France life & non-life insurance market in value (USD billion) for all the above segments.

By Insurance Type (Value)

| Life Insurance | |

| Non-Life Insurance | Motor Insurance |

| Health Insurance | |

| Property Insurance | |

| Liability Insurance | |

| Other Insurance |

By Customer Segment (Value)

| Retail |

| Corporate |

By Distribution Channel (Value)

| Brokers |

| Agents |

| Banks |

| Direct Sales |

| Other Channels |

| By Insurance Type (Value) | Life Insurance | |

| Non-Life Insurance | Motor Insurance | |

| Health Insurance | ||

| Property Insurance | ||

| Liability Insurance | ||

| Other Insurance | ||

| By Customer Segment (Value) | Retail | |

| Corporate | ||

| By Distribution Channel (Value) | Brokers | |

| Agents | ||

| Banks | ||

| Direct Sales | ||

| Other Channels | ||

Key Questions Answered in the Report

What is the forecast value of the France life & non-life insurance market in 2031?

The market is expected to reach USD 361.84 billion by 2031, expanding at a 4.45% CAGR.

Which product group is growing fastest inside French non-life insurance?

Motor insurance leads non-life growth, benefiting from stricter enforcement against uninsured vehicles and yearly premium gains of about 5%.

How significant is bancassurance in French insurance distribution?

Banks accounted for 52.63% of 2025 premiums, far ahead of agents, brokers, and direct channels.

Why are unit-linked life policies gaining traction?

Sub-1% guaranteed rates on euro funds and new green-investment quotas are driving savers toward unit-linked contracts that offer higher return potential.

What challenges do insurers face from climate change?

Rising flood and drought claims are inflating loss ratios and forcing recalibration of catastrophe models and property pricing.

How are InsurTech firms influencing the market?

Digital insurers like Alan are winning large group health contracts and posting double-digit revenue growth by offering seamless app-based experiences and partnering with traditional banks.

Page last updated on: