Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

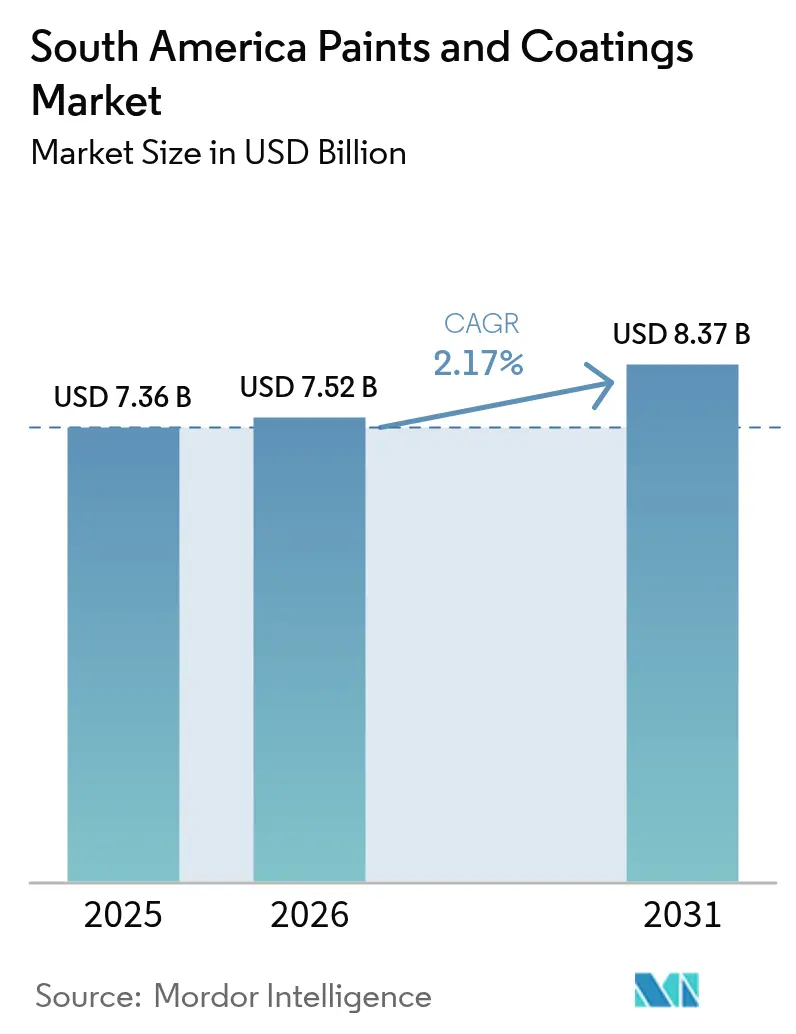

| Base Year Market Size (2025) | USD 7.36 Billion |

| Market Size (2026) | USD 7.52 Billion |

| Market Size (2031) | USD 8.37 Billion |

| Growth Rate (2026 - 2031) | 2.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Paints And Coatings Market Analysis by Mordor Intelligence

The South America Paints and Coatings Market size was valued at USD 7.36 billion in 2025 and estimated to grow from USD 7.52 billion in 2026 to reach USD 8.37 billion by 2031, at a CAGR of 2.17% during the forecast period (2026-2031). Architectural demand, tied to residential and commercial construction, continues to anchor volume; however, the automotive, battery, and cool-roof segments are expanding more rapidly and reshaping supplier priorities. Currency volatility remains the largest short-term risk, as higher import taxes on polymers inflate raw material costs and pressure margins, while stricter Mercosur VOC (Volatile Organic Compound) regulations accelerate the shift toward waterborne and powder technologies. Multinational manufacturers expand their regional footprints through mergers and production upgrades, whereas local players utilize last-mile distribution and custom color services to maintain their share in price-sensitive decorative categories. Against this backdrop, specialty opportunities emerge in lithium-processing plants, reflective roof systems for tropical cities, and digital color-matching services targeting urban DIY (Do-It-Yourself) customers.

Key Report Takeaways

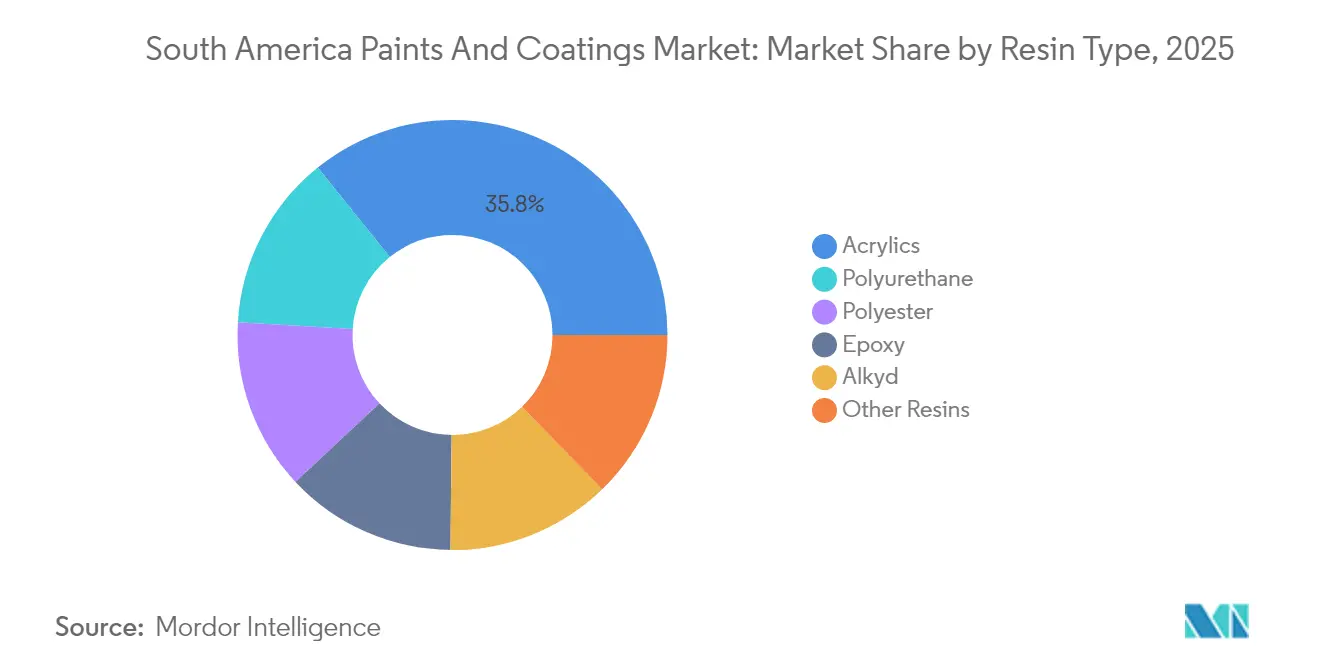

- By resin type, acrylics led with a 35.78% share of the South American paints and coatings market in 2025, while polyurethane resins are forecast to expand at a 5.62% CAGR through 2031.

- By technology, solvent-borne products accounted for 62.10% of the South American paints and coatings market size in 2025; water-borne systems are projected to post the highest CAGR at 5.85% from 2025 to 2031.

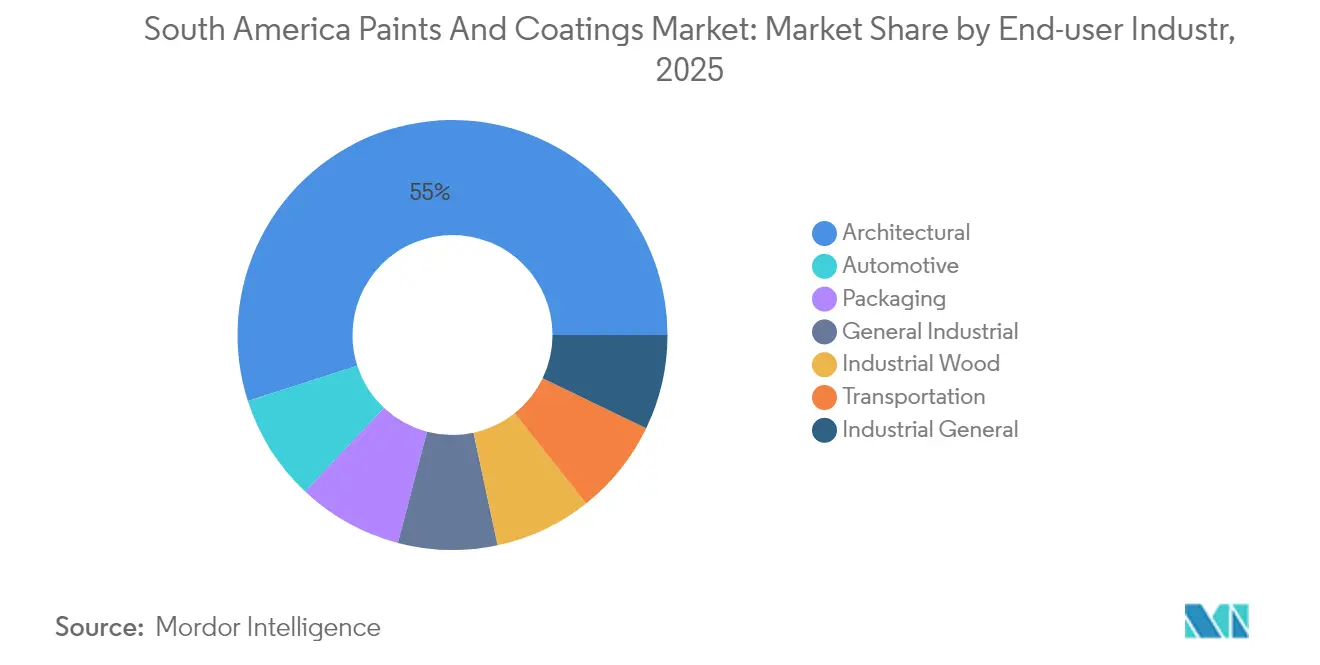

- By end-user industry, architectural applications captured 54.96% of the 2025 revenue, whereas automotive coatings are expected to advance at a 5.78% CAGR through 2031.

- By geography, Brazil held a 47.65% revenue share in 2025, while Colombia is projected to achieve a 5.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of Residential and Commercial Construction Projects | +0.8% | Brazil, Colombia, Chile | Medium term (2-4 years) |

| Recovery of Regional Automotive Production and Exports | +0.6% | Brazil, Argentina, Mexico border regions | Short term (≤ 2 years) |

| Rapid Adoption of Cool-roof Reflective Coatings in Tropical Cities | +0.3% | Brazil, Colombia, Venezuela | Long term (≥ 4 years) |

| Lithium-ion Battery Gigafactory Build-outs Demanding Specialty Coatings | +0.4% | Argentina, Chile lithium triangle | Medium term (2-4 years) |

| Rise of Online DIY Micro-brands for Decorative Paints | +0.2% | Urban centers across South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Residential and Commercial Construction Projects

Elevated housing and infrastructure spending in Colombia and Chile offset Brazil’s early-2025 slowdown and underpin steady architectural volume. Social-housing programs favor low-cost acrylic emulsions, whereas commercial builders increasingly require low-emission, mold-resistant interior finishes that meet green-building criteria. Water-borne acrylic systems share the win because Brazilian life-cycle studies show superior performance in seven of eight environmental metrics compared to solvent-borne coatings[1]Federal University of Santa Catarina, “Life-Cycle Assessment of Water-borne vs. Solvent-borne Paints,” ufsc.br. Government procurements also prioritize bio-based and recycled-content formulas, prompting suppliers to broaden sustainable product lines.

Recovery of Regional Automotive Production and Exports

Brazil produced 2.5 million vehicles in 2024, a 9.7% increase, reviving OEM (Original Equipment Manufacturer) basecoat and refinish consumption. Automakers demand durable, low-VOC finishes that comply with stricter emission rules and withstand tropical climates, spurring investment in water-borne basecoats and high-solid clearcoats. PPG’s Latin America sales climbed 14.1% in 2024, driven largely by automotive OEM and refinish lines. Mexico-border assembly plants that export to North America require coatings certified to US quality standards, widening the addressable market for premium chemistries.

Rapid Adoption of Cool-Roof Reflective Coatings in Tropical Cities

Brazilian field trials confirm that high-reflectance roof coatings sustain energy savings over multiple years, though tropical humidity necessitates periodic maintenance. Utility rebates and municipal heat-island mitigation policies accelerate demand in Rio de Janeiro, Medellín, and Caracas. Suppliers formulate acrylic- and silicone-modified membranes that resist algae, maintain adhesion under high humidity, and endure intense UV (Ultraviolet) exposure. Multinationals adapt global cool-roof platforms to local substrates, while regional brands capture niche demand via cost-effective acrylic elastomers.

Lithium-ion Battery Gigafactory Build-outs Demanding Specialty Coatings

Posco’s USD 800 million lithium-hydroxide plant in Argentina exemplifies chemical-processing facilities that require low-outgassing, solvent-resistant floor and equipment coatings. Argentina’s Mining Secretariat projects that eight lithium exporters will be in operation by 2030, doubling sodium-carbonate demand and broadening the need for chemical-resistant linings. Suppliers winning this segment pair corrosion-control expertise with clean-room compliance, targeting battery and cathode-active-material lines across the lithium triangle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter VOC and Solvent-emission Limits Across Mercosur | -0.40% | Brazil, Argentina, Uruguay, Paraguay | Medium term (2-4 years) |

| Currency Volatility Inflating Imported Raw-material Costs | -0.60% | Argentina, Brazil, Colombia | Short term (≤ 2 years) |

| Shift to Composite Façade Panels Reducing Paint Demand in Premium Offices | -0.30% | Brazil, Chile, Colombia urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter VOC and Solvent-Emission Limits Across Mercosur

Regulators enforce tighter limits on architectural and industrial coatings, mirroring US Rule 1113 benchmarks[2]South Coast Air Quality Management District, “Rule 1113 Architectural Coatings,” aqmd.gov. Larger suppliers leverage global R&D to launch ultra-low-VOC lines, while smaller firms struggle with the costs of reformulation. Compliance spurs demand for water-borne and powder technologies but introduces transitional dual inventories as legacy solvent grades sell through.

Currency Volatility Inflating Imported Raw-Material Costs

Peso and real devaluations lift prices for imported pigments, additives, and resins, compressing margins and delaying projects. PPG Industries, Inc. booked a USD 20 million foreign-exchange loss in Argentina in December 2024, illustrating exposure to sudden shifts. Manufacturers hedge against currency fluctuations and localize sourcing where feasible; however, limited regional petrochemical capacity restricts substitution options for high-performance inputs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylics Dominate, Polyurethane Gains Momentum

Acrylics retained a 35.78% revenue share in 2025, anchoring the South America paints and coatings market through their versatility in water-borne architectural finishes. Polyurethane volumes are climbing at a 5.62% CAGR as lithium battery and automotive customers favor superior chemical and abrasion resistance. Epoxies serve as a protective coating for marine and metal-fabrication assets exposed to corrosive environments, whereas alkyds are being replaced by cost-competitive acrylic emulsions that now meet mid-tier durability needs. Polyester resins support growing powder-coating output for appliances and automotive trim, helping Brazil emerge as one of the fastest-expanding powder pretreatment hubs outside Asia. Specialty silicone and fluoropolymer chemistries fill niches requiring extreme UV or chemical protection on reflective roofs and process equipment.

Market momentum indicates that acrylic-emulsion suppliers are investing in bio-based monomers to differentiate themselves amid tightening VOC rules. Meanwhile, polyurethane formulators add UV-stable aliphatic systems tailored to lithium-hydroxide facilities. Epoxy vendors emphasize rapid-cure novolac blends for minimizing downtime in bulk cargo port maintenance. Thus, resin demand patterns mirror the region’s shifting industrial mix while aligning with environmental policy trajectories.

By Technology: Water-borne Shift Accelerates Regulatory Compliance

Solvent-borne products still accounted for 62.10% of 2025 revenue, yet water-borne technologies are expanding at a 5.85% CAGR, outpacing the overall South American paints and coatings market. Architectural buyers adopt water-borne acrylics that match solvent performance without odor or flammability hazards, and industrial users trial high-solid and self-crosslinking emulsions to reduce energy consumption during the baking process. Powder coatings are gaining traction in appliances and wheels, as their zero-VOC credentials align with corporate sustainability goals. UV-cured finishes remain niche but grow where faster throughput offsets higher equipment costs. Suppliers focus on rheology modifiers and reactive diluents optimized for tropical humidity, ensuring leveling and early rain resistance.

Regulators reinforce the water-borne pivot; Brazilian life-cycle assessments confirmed lower ecotoxicity and carbon intensity for aqueous products. Investment, therefore, concentrates on emulsion-polymer capacity and water-compatible metallic flakes for automotive topcoats. Concurrently, solvent-borne lines remain relevant in the refinish and heavy-duty sectors, where immediate hardness and chemical resistance remain paramount.

By End-User Industry: Automotive Challenges Architectural Dominance

Architectural demand accounted for 54.96% of 2025 sales and underpins volume leadership; however, the automotive segment is expanding at a 5.78% CAGR, driven by Brazil’s vehicle recovery and border-region export assembly. OEMs specify multi-layer water-borne systems that meet global quality and emission benchmarks. Industrial wood coatings are expected to benefit from USD 136 million in plywood and OSB (Oriented Strand Board) capacity additions, which will require UV-curable and waterborne topcoats for furniture exports. General industrial users, ranging from metal furniture to farm machinery, require anti-corrosion primers that are compatible with humid tropical storage conditions. Transportation coatings protect marine hulls and railcars that operate in coastal climates, while packaging lines utilize Bisphenol A (BPA)-free interior lacquers to comply with food-contact regulations. This diverse end-user spread cushions suppliers from cyclical swings in any single sector.

Geography Analysis

Brazil remains the anchor of the South America paints and coatings market, supported by localized resin plants, a 2.5 million-unit vehicle output in 2024, and thousands of branded retail outlets. Yet a high 15% Selic rate raises borrowing costs for developers, tempering architectural momentum. Environmental regulators intensify VOC enforcement, encouraging multinationals to introduce next-generation water-borne lines from global platforms.

Colombia posts the fastest CAGR as public–private partnerships deliver highways and social housing, and as DIY activity rises in expanding urban centers. Local distributors import colorants and additives through Atlantic ports and deliver rapid-mix services to job sites, improving supply responsiveness. Government green-building incentives reward low-emission paints, accelerating the transition to water-borne acrylics.

Argentina’s peso depreciation and inflation strain consumer budgets, but lithium project investments in Salta and Catamarca provinces require chemical-resistant floor and tank linings. Multinationals hedge FX exposure by invoicing in US dollars where permitted and by sourcing solvents from regional petrochemical complexes when available.

Chile’s copper and lithium extraction drives protective-coating needs on pipelines and tank farms in the Atacama Desert. Peru revamps Lima’s metro and port infrastructure, generating architectural and industrial demand despite modest GDP growth. Smaller economies such as Uruguay and Paraguay benefit from cross-border trade and agro-processing facilities that require durable epoxy and polyurethane finishes.

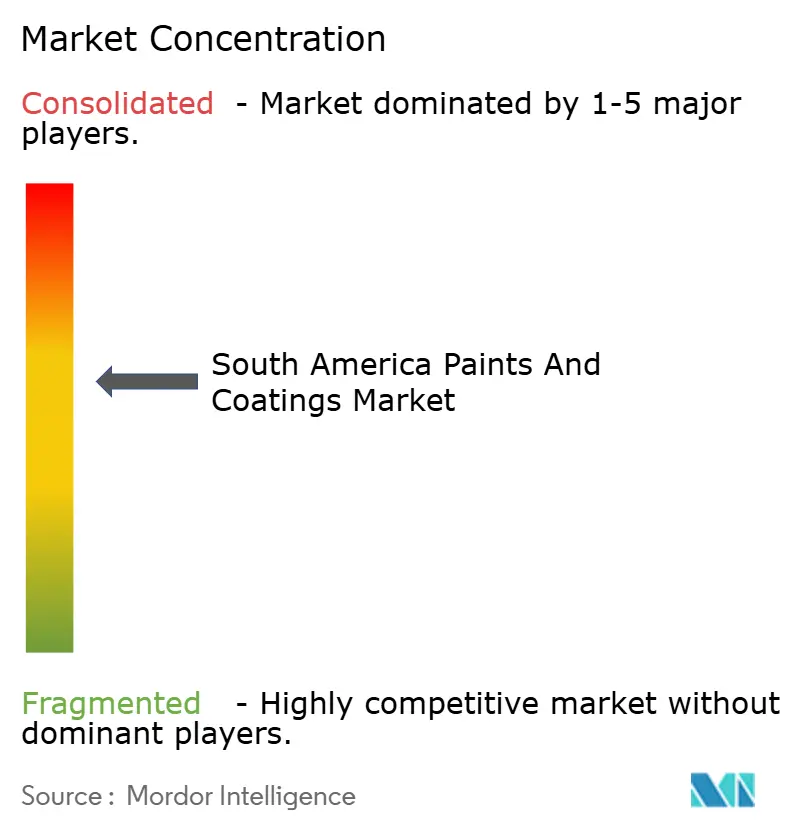

Competitive Landscape

The South America Paints and Coatings market is moderately consolidated. The Sherwin-Williams Company deepened its regional reach by acquiring BASF’s Suvinil decorative brand for USD 1.15 billion, adding a portfolio of color stores and contractor relationships. Strategic moves center on water-borne technology transfers, digital color platforms, and joint manufacturing to offset currency risk. Lubrizol’s USD 20 million acrylic-emulsion expansion bolsters regional binder capacity and underpins local supply of advanced low-VOC products. Suppliers are eyeing emerging niches, such as cool-roof membranes, powder primers for appliance exports, and epoxy novolac systems for lithium brine equipment.

South America Paints And Coatings Industry Leaders

PPG Industries, Inc.

Akzo Nobel N.V.

The Sherwin William Company

BASF

Renner Herrmann SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kölor Paints, the exclusive brand of Homecenter, teamed up with Glasst-Unpaint to launch Kölor-Unpaint in Colombia. This removable paint allows users to effortlessly switch colors and designs, preserving the original surface's integrity and durability.

- February 2025: BASF and The Sherwin-Williams Company signed an agreement on the sale of the Brazilian decorative paints business, which is part of BASF’s Coatings division. The purchase price on a cash and debt-free basis is USD 1.15 billion.

South America Paints And Coatings Market Report Scope

Paints and coatings are thin layers of substance added to a surface to protect, beautify, or improve its usefulness. Paints are usually aqueous solutions, while coatings are often applied using solvent-based systems. In most cases, a brush, scraper, and sprinkler are used to apply them. The major raw materials utilized in producing paints and coatings are resins, pigments, solvents, and other materials.

The market is segmented by resin type, technology, end-user industry, and geography. By resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types (polypropylene, etc.). By technology, the market is segmented into water-borne, solvent-borne, powder, and UV-cured coating. By end-user industry, the market is segmented into architectural, automotive, wood, industrial, and other end-user industries. The report also covers the market size and forecasts for the market in 5 countries across the region.

For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin Type

| Acrylics |

| Epoxy |

| Alkyd |

| Polyester |

| Polyurethane |

| Other Resins (Silicone, Fluoropolymer, etc.) |

By Technology

| Water-borne |

| Solvent-borne |

| Powder |

| UV-cured |

By End-User Industry

| Architectural |

| Automotive |

| Industrial Wood |

| Industrial General |

| General Industrial |

| Transportation |

| Packaging |

By Geography

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Resin Type | Acrylics |

| Epoxy | |

| Alkyd | |

| Polyester | |

| Polyurethane | |

| Other Resins (Silicone, Fluoropolymer, etc.) | |

| By Technology | Water-borne |

| Solvent-borne | |

| Powder | |

| UV-cured | |

| By End-User Industry | Architectural |

| Automotive | |

| Industrial Wood | |

| Industrial General | |

| General Industrial | |

| Transportation | |

| Packaging | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America paints and coatings market in 2026?

The market stands at USD 7.52 billion in 2026 and is projected to reach USD 8.37 billion by 2031.

Which segment is growing fastest within South America paints and coatings?

Automotive coatings exhibit the highest growth, posting a 5.78% CAGR through 2031.

Why are water-borne coatings gaining share in South America?

Stricter Mercosur VOC regulations and proven life-cycle benefits are driving a 5.85% CAGR for water-borne systems.

Which country offers the strongest growth outlook?

Colombia is forecast to grow at a 5.35% CAGR thanks to infrastructure investment and housing programs.

How is consolidation altering competitive dynamics?

Sherwin-Williams’ USD 1.15 billion purchase of BASF’s Suvinil brand and PPG’s organic expansion illustrate a trend toward greater regional scale and technology depth among multinationals.

Page last updated on: