Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

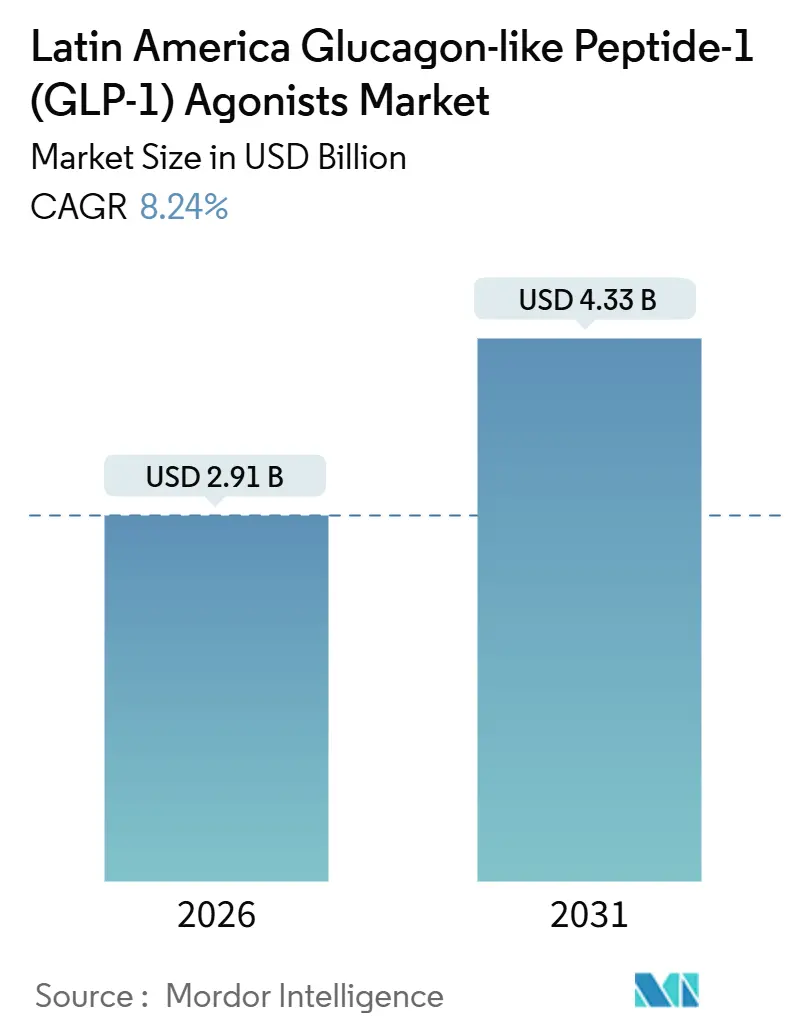

| Market Size (2026) | USD 2.91 Billion |

| Market Size (2031) | USD 4.33 Billion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America Glucagon-like Peptide-1 (GLP-1) Agonists Market Analysis by Mordor Intelligence

The Latin America Glucagon-like Peptide-1 Agonists Market size is estimated at USD 2.91 billion in 2026, and is expected to reach USD 4.33 billion by 2031, at a CAGR of 8.24% during the forecast period (2026-2031).

Surging diabetes and obesity prevalence, a looming patent cliff for semaglutide, and escalating local-manufacturing plans are reshaping competitive dynamics across Brazil, Mexico, Argentina, and secondary markets. Early biosimilar pipelines now coincide with once-weekly and dual-incretin innovations, encouraging payers to re-examine cost-effectiveness thresholds and to broaden indication coverage beyond glycemic control. At the same time, e-commerce channels, telemedicine-led prescribing, and retailer omnichannel models shorten patient pathways, tilting volume toward self-administration. Manufacturers are therefore embedding fill-finish capacity inside Brazil and exploring Mexican licensing deals to hedge supply-chain risk and comply with “Buy National” mandates. Together, these trends create a pivotal moment for the Latin America GLP-1 agonists market as budget holders juggle clinical value, affordability, and local-content requirements.

Key Report Takeaways

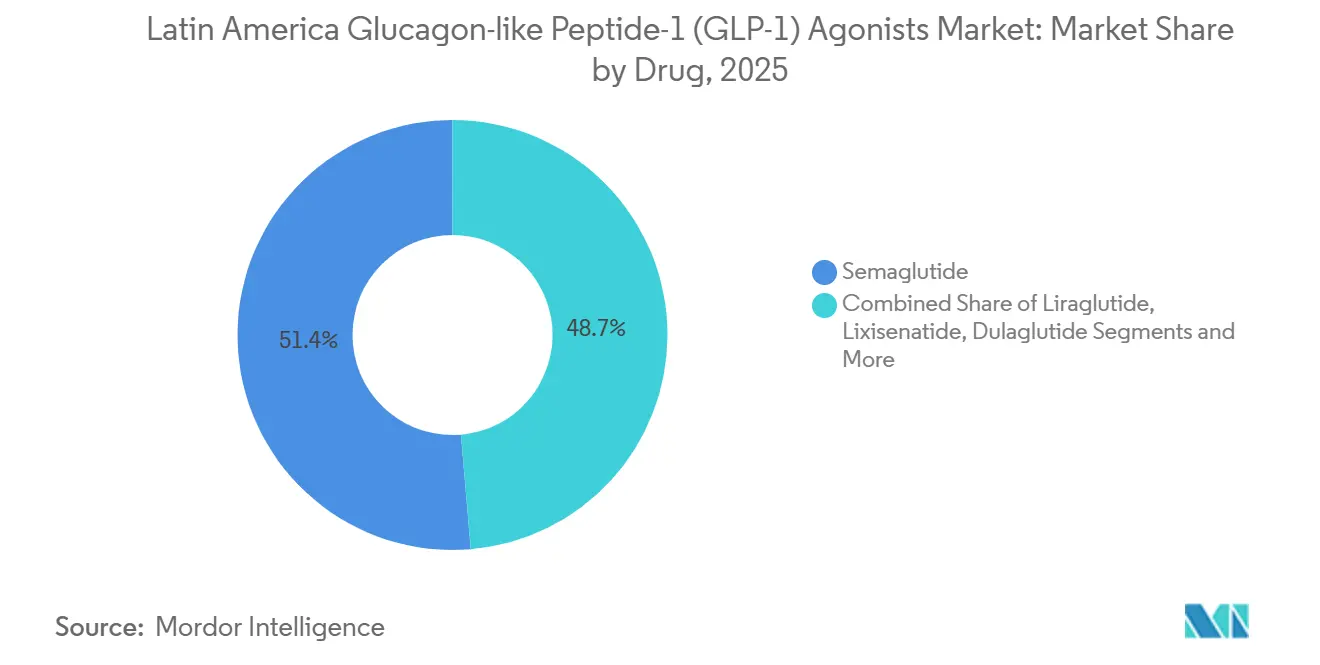

By drug, semaglutide led with 51.35% of the Latin America GLP-1 agonists market share in 2025, while tirzepatide is projected to record the fastest 12.12% CAGR through 2031.

By route of administration, injectable pens held 91.68% revenue in 2025, whereas oral tablets are expected to post a 10.35% CAGR over 2026-2031.

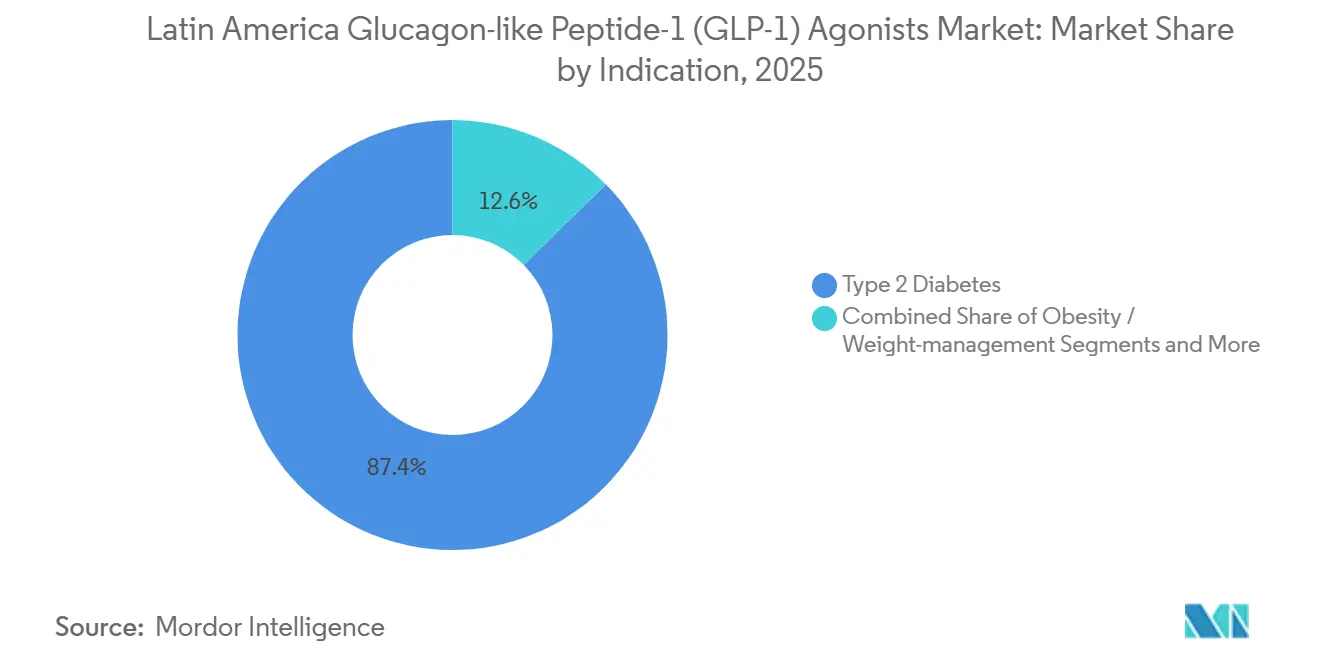

By indication, type 2 diabetes accounted for 87.36% revenue in 2025, but obesity and weight-management prescriptions are forecast to grow at 11.57% CAGR to 2031.

By distribution channel, retail chain pharmacies captured 61.24% revenue in 2025, while e-commerce and tele-pharmacy platforms are poised for a 12.79% CAGR through 2031.

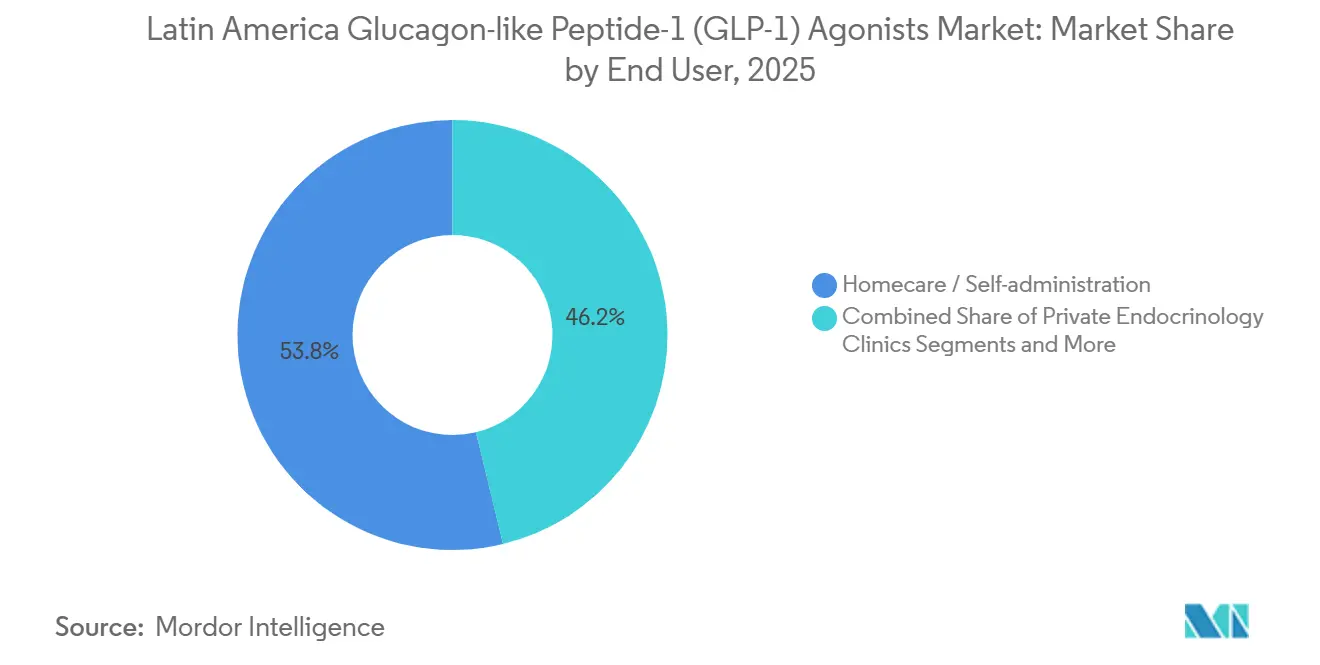

By end user, homecare and self-administration represented 53.78% revenue in 2025, yet private endocrinology clinics are slated to expand at an 11.24% CAGR to 2031.

By geography, Brazil commanded 59.82% revenue in 2025, whereas Mexico is forecast to achieve a 10.57% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Latin America Glucagon-like Peptide-1 (GLP-1) Agonists Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising T2D & obesity prevalence fuels baseline demand | +1.8% | Brazil, Mexico, Argentina, Colombia | Long term (≥ 4 years) |

| Physician shift toward once-weekly / dual-incretin therapies | +1.5% | Brazil, Mexico, urban centers in Argentina | Medium term (2-4 years) |

| Gradual reimbursement expansion in Brazil, Colombia et al. | +1.2% | Brazil SUS, Colombia PBS, Mexico IMSS pilot zones | Medium term (2-4 years) |

| Local manufacturing & fill-finish investments lower supply risk | +1.0% | Brazil (Montes Claros, Hortolândia), Mexico border zones | Long term (≥ 4 years) |

| CV- & renal-outcome evidence opens multi-budget wallets | +1.4% | Brazil private plans, Mexico ISSSTE, Argentina PAMI | Medium term (2-4 years) |

| Expansion of tele-medicine & e-pharmacy channels widens GLP-1 reach | +0.9% | Brazil metropolitan areas, Mexico City, Buenos Aires | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising T2D And Obesity Prevalence Fuels Baseline Demand

Adult diabetes cases in South and Central America climbed from 32 million in 2021 to 35.4 million in 2024 and are projected to reach 51.5 million by 2050, creating a vast patient pool for the Latin America GLP-1 agonists market.[1]International Diabetes Federation, “IDF Diabetes Atlas 2024,” International Diabetes Federation, diabetesatlas.org Mexico's 2023 documented 38.9 percent of obesity prevalence among adults, while 37.3 percent of the population is classified as overweight or obese, creating a high patient pool of individuals.[2]World Obesity Federation Data Team, “Mexico Obesity Prevalence Dataset,” World Obesity Federation, data.worldobesity.org In Brazil, 16.6 million residents carry a diabetes diagnosis, yet fewer than 40% achieve HbA1c targets under public care models. Better adherence profiles for once-weekly GLP-1 agents therefore present a clinical upgrade over older sulfonylureas. Regional cardiovascular-mortality data further underline the urgency of therapies that simultaneously address glycemia, weight, and cardiometabolic risk.

Physician Shift Toward Once-Weekly And Dual-Incretin Therapies

Brazilian and Mexican endocrinologists report 30%-40% higher 12-month persistence for once-weekly semaglutide or dulaglutide compared with daily liraglutide. Tirzepatide’s 2.0%-2.5% mean HbA1c reduction in SURPASS studies outperformed semaglutide by roughly 0.5 percentage points, prompting Mexico’s regulator to authorize the drug for obesity in 2024. Survey data from Brazil showed 62% of specialists preferring weekly regimens for patients with prior adherence issues. Private insurers in São Paulo and Rio logged a 45% annual jump in once-weekly GLP-1 scripts in 2025, showing that convenience translates to volume gains once costs moderate.

Gradual Reimbursement Expansion In Brazil, Colombia, And Beyond

Although Brazil’s health-technology body CONITEC deferred full semaglutide incorporation in 2024, the 2025 federal budget increased diabetes-drug funding by 15%, hinting at future tender capacity.[3]News Article, “Brazil’s Conitec Rejects GLP-1 Slimming Drugs for Inclusion in SUS,” Navlin Daily, navlindaily.com Colombia’s benefit plan already covers liraglutide for high-BMI patients, while Mexico’s IMSS logged a 1.8% HbA1c drop and 8 kg weight loss in its 2024 pilot that combined semaglutide with remote monitoring. Argentina’s PAMI allows dulaglutide for retirees with cardiovascular history, setting precedent for indication-based access even amid fiscal pressure.

Local Manufacturing And Fill-Finish Investments Lower Supply Risk

Novo Nordisk’s USD 1.09 billion upgrade to its Montes Claros complex, announced in April 2025, will begin producing GLP-1 pens domestically in late 2026, shielding the Latin America GLP-1 agonists market from future import bottlenecks. EMS’s R$ 60 million Hortolândia plant opened in August 2024, and its tech-transfer pact with Fiocruz aims to supply 2 million biosimilar pens per year by 2028. Mexican authorities are evaluating similar pacts with Liomont and Probiomed. Local capacity not only cuts logistics risk but satisfies procurement clauses that favor national content in public tenders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost and patchy public coverage | -1.6% | Brazil SUS, Mexico IMSS, Argentina public system | Long term (≥ 4 years) |

| Global supply shortages and allocation caps | -0.9% | Brazil, Mexico, Argentina | Short term (≤ 2 years) |

| Tightened anti-obesity prescription rules | -0.7% | Brazil, spill-over to Colombia | Medium term (2-4 years) |

| Data-coding gaps that slow health-technology assessments | -0.5% | Brazil CONITEC, Colombia IETS, Mexico CENETEC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost And Patchy Public Coverage

Monthly branded semaglutide costs reach BRL 1,200 (USD 240) in Brazil—about 80% of the minimum wage—placing it out of reach for many SUS beneficiaries. Mexico’s IMSS serves less than 5,000 GLP-1 patients annually via exception pathways, despite more than 12 million diabetics. Argentina and Colombia apply strict prior-authorization hurdles that lengthen initiation and depress uptake, effectively confining large segments of the Latin America GLP-1 agonists market to private payers.

Global Supply Shortages And Allocation Caps

2023-2024 shortages saw Latin American shipments cut by roughly 25% as U.S. and European demand soared. Brazil’s regulator logged 487 shortage complaints in the first half of 2024, and Mexico instituted parallel-import fast tracks to offset caps. Persisting physician caution on supply reliability dampens new starts even in 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug: Semaglutide Dominance Faces Dual-Agonist Disruption

Semaglutide captured 51.35% of the Latin America GLP-1 agonists market in 2025 thanks to once-weekly convenience and robust SUSTAIN and STEP data. Tirzepatide’s 12.12% forecast CAGR reflects its dual receptor mechanism and superior weight-loss performance, with COFEPRIS granting an obesity label in 2024. Dulaglutide maintains a steady user base among Brazilian private insurers who favor its auto-injector design, while liraglutide’s daily-injection regimen is losing ground to longer-acting rivals. Biosimilar pipelines will accelerate after semaglutide’s Brazilian patent expiry in March 2026, as Fiocruz-EMS aims for 2 million annual pens by 2028. Oral semaglutide remains a niche alternative for needle-averse patients, though fasting-administration requirements curtail adherence.

In value terms, tirzepatide could command 30% of the drug class by 2031 if HTA bottlenecks clear and price parity tightens. Exenatide and lixisenatide remain relegated to cost-sensitive tender lots, preserving minimal but steady volume. The Latin America GLP-1 agonists market size for pipeline and biosimilar entrants is projected to grow quickly once public sectors secure 30%-40% list-price discounts.

By Route Of Administration: Injectable Pens Anchor Market

Injectable pens controlled 91.68% revenue in 2025 thanks to pre-filled accuracy, once-weekly scheduling, and audible dose cues that benefit low-vision patients. Brazil’s telemedicine rule accelerates pen adoption because video-based injection training is easily delivered. However, oral tablets are projected to post a 10.35% CAGR as private plans expand Rybelsus coverage and as potential biosimilar competition narrows cost gaps. If oral semaglutide prices fall below USD 150 per month once local licensees enter, tablets could reach a 15% share by 2031.

Pen innovation continues: Novo Nordisk’s FlexTouch and Eli Lilly’s KwikPen incorporate tactile feedback that reduces dosing errors. Mexico’s labeling rules mandate Spanish instructions and tactile dose indicators, raising costs yet boosting patient safety. The Latin America GLP-1 agonists market size for pens still dwarfs tablets, but oral formats will increasingly attract first-line therapy seekers who dislike injections.

By Indication: Obesity Applications Gain Momentum

Type 2 diabetes generated 87.36% of 2025 revenue, but obesity-related demand is forecast to expand at 11.57% CAGR. Regulatory nods for Wegovy in Mexico and Brazil widen eligibility to millions of high-BMI adults, while cardiovascular-outcome data support use in secondary prevention. WHO’s 2025 guideline underpins broader payer consideration, increasing the Latin America GLP-1 agonists market size for cardio-renal indications by an estimated 25%. Yet cash-pay barriers keep real-world penetration below 200,000 patients so far, implying enormous headroom once biosimilar pricing compresses.

Obesity prescriptions may outgrow diabetes scripts after 2028 if public payers embrace cost-offset logic tied to reduced heart-failure hospitalizations and dialysis rates. Cardiovascular-risk coverage under private plans in São Paulo already rose in 2025, and Mexico’s ISSSTE is examining similar add-on benefits for 2027.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Retail chains accounted for 61.24% of 2025 sales, but e-commerce and tele-pharmacy are set for a 12.79% CAGR through 2031. Brazil’s Resolution 2314 green-lights online prescribing, while Drogasil’s 24-hour cold-chain delivery addresses pen-temperature constraints. E-pharmacy share already hits 8% in São Paulo and Rio, and Farmacias Guadalajara is piloting similar last-mile services. Hospital pharmacies stay stable, dispensing mainly to inpatients or clinic-based diabetes programs. Long-form prescription retention rules introduced in 2025 favor well-capitalized platforms with enterprise IT, skewing volume toward dominant e-pharmacy brands.

By End User: Homecare Leads, Private Clinics Accelerate

Homecare and self-administration captured 53.78% revenue in 2025, as once-weekly auto-injectors minimize clinic visits. Specialist-led private clinics should grow at 11.24% CAGR as payers see value in dose-optimization protocols that reduce ER admissions for hypoglycemia or GI events. Hybrid consultation models—initial in-clinic titration followed by telehealth—shrink overhead and appeal to cost-conscious insurers. Hospitals maintain a role in complex cases and pre-bariatric protocols, but their share is capped by outpatient-dispensing rules. The Latin America GLP-1 agonists market continues to tilt toward patient-managed care pathways.

Geography Analysis

Brazil generated 59.82% of 2025 revenue, buoyed by a 16.6 million diabetes population and 50 million private-insured lives. Novo Nordisk’s USD 1.09 billion Montes Claros expansion plants defensive roots against biosimilar pressure and embeds local content for SUS tenders. Fiocruz-EMS aims to deliver 2 million biosimilar pens annually by 2028, which could trim prices 30%-40% and enlarge public access. Patent expiry in March 2026 invites further generics, potentially accelerating volume but pressuring branded margins within the Latin America GLP-1 agonists market.

Mexico is forecast for a 10.57% CAGR, propelled by IMSS pilots pairing semaglutide with tele-monitoring and by a regulator that green-lit tirzepatide for obesity in 2024. ISSSTE added dulaglutide for albuminuric patients in 2025, illustrating payer willingness to bankroll therapies with proven renal outcomes. Parallel-import fast tracks eased but did not fully resolve supply gaps, and broader IMSS formulary inclusion remains the swing factor for future growth.

Argentina, Colombia, Chile, and Peru contribute smaller but steady increments. Argentina’s ANMAT approval of tirzepatide has yet to convert into volume because reimbursement remains restricted to retirees with cardiovascular events. Colombia covers liraglutide for high-BMI cases but imposes multi-step prior authorization. Chile’s public system still omits GLP-1 agents, limiting uptake to private insurers. Currency volatility and lower health-care spend slow penetration, yet IDF’s prevalence forecast suggests eventual policy shifts once biosimilar prices sink.

Competitive Landscape

Novo Nordisk and Eli Lilly jointly command a major share of the Latin America GLP-1 agonists market through semaglutide, dulaglutide, and tirzepatide portfolios. Novo Nordisk’s manufacturing bet in Brazil protects share under domestic-content rules and mitigates exchange-rate shock. Eli Lilly leverages tirzepatide’s dual-incretin superiority to justify premium pricing inside private plans. Boehringer Ingelheim maintains niche loyalty for dulaglutide via its auto-injector design, though share erosion is visible. Sanofi’s lixisenatide remains tender-favored when acquisition cost outweighs dosing convenience.

Local challengers—Biomm, Eurofarma, Hypera—are preparing biosimilar liraglutide and generic exenatide lines timed to patent roll-offs. Fiocruz-EMS’s tech transfer stands as the first large-scale domestic biosimilar effort, aiming to undercut branded prices by up to 40%. White-space opportunities extend to oral formulations and multi-indication positioning for cardio-renal protection. Digital-health disruptors such as Conexa Saúde and Dr. Consulta already command close to 8% of retail value in Brazil by bundling virtual consults, drug delivery, and remote monitoring.

Latin America Glucagon-like Peptide-1 (GLP-1) Agonists Industry Leaders

AstraZeneca

Novo Nordisk A/S

Eli Lilly and Company

Sanofi

Hypera S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: WHO recommended GLP-1 receptor agonists as part of comprehensive adult-obesity care, citing cardio-metabolic benefits.

- August 2025: Fiocruz and EMS formalized a tech-transfer deal to manufacture biosimilar liraglutide and semaglutide for SUS tenders, targeting 2 million pens annually by 2028.

- April 2025: Novo Nordisk committed USD 1.09 billion to expand Montes Claros fill-finish capacity, with operations slated for late 2026.

- February 2025: Novo Nordisk announced that semaglutide 2.4 mg would be available in Mexican pharmacies by April 2025, with an average 17.5% weight loss observed in pivotal trials.

Latin America Glucagon-like Peptide-1 (GLP-1) Agonists Market Report Scope

GLP-1 receptor agonists mimic the hormone Glucagon-Like Peptide-1 (GLP-1) to manage type 2 diabetes and obesity by stimulating insulin release, slowing digestion, and reducing appetite. They lower blood sugar, aid weight loss, and benefit cardiovascular and kidney health.

Drugs, route of administration, indication, distribution channel, end-user, and geography segment the Latin America glucagon-like peptide-1 (GLP-1) agonists market. By Drug, market is segmented by Exenatide, Liraglutide, Lixisenatide, Dulaglutide, Semaglutide, Tirzepatide, Pipeline & Biosimilar/Generic GLP-1. By Route of Administration, market is segmented by Injectable Pens, Oral Tablets. By Indication, market is segmented by Type 2 Diabetes, Obesity / Weight-management, Cardiovascular & Renal Risk Reduction. By Distribution Channel, the market is segmented by Hospital Pharmacies, Retail Chain Pharmacies, and E-Commerce / Tele-pharmacy. By End User, market is segmented by Hospitals & Specialty Diabetes Centers, Private Endocrinology Clinics, Homecare / Self-administration. By Geography, market is segmented by Brazil, Mexico, Argentina, Rest of Latin America. The report offers the value (in USD) for the above segments.

By Drug

| Exenatide |

| Liraglutide |

| Lixisenatide |

| Dulaglutide |

| Semaglutide |

| Tirzepatide (dual GIP/GLP-1) |

| Pipeline & Biosimilar/Generic GLP-1s |

By Route of Administration

| Injectable Pens |

| Oral Tablets |

By Indication

| Type 2 Diabetes |

| Obesity / Weight-management |

| Cardiovascular & Renal Risk Reduction |

By Distribution Channel

| Hospital Pharmacies |

| Retail Chain Pharmacies |

| E-Commerce / Tele-pharmacy |

By End User

| Hospitals & Specialty Diabetes Centers |

| Private Endocrinology Clinics |

| Homecare / Self-administration |

By Geography

| Brazil |

| Mexico |

| Argentina |

| Rest of Latin America |

| By Drug | Exenatide |

| Liraglutide | |

| Lixisenatide | |

| Dulaglutide | |

| Semaglutide | |

| Tirzepatide (dual GIP/GLP-1) | |

| Pipeline & Biosimilar/Generic GLP-1s | |

| By Route of Administration | Injectable Pens |

| Oral Tablets | |

| By Indication | Type 2 Diabetes |

| Obesity / Weight-management | |

| Cardiovascular & Renal Risk Reduction | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Chain Pharmacies | |

| E-Commerce / Tele-pharmacy | |

| By End User | Hospitals & Specialty Diabetes Centers |

| Private Endocrinology Clinics | |

| Homecare / Self-administration | |

| By Geography | Brazil |

| Mexico | |

| Argentina | |

| Rest of Latin America |

Key Questions Answered in the Report

How large is the Latin America GLP-1 agonists market today?

The Latin America GLP-1 agonists market size is USD 2.91 billion in 2026 and is projected to climb to USD 4.33 billion by 2031.

What CAGR is expected for GLP-1 sales in Latin America through 2031?

Revenue is forecast to grow at an 8.24% CAGR over the 2026-2031 period.

Which drug currently leads prescriptions in the region?

Semaglutide held 51.35% of prescriptions in 2025, making it the dominant agent.

Which country contributes the most revenue?

Brazil generated 59.82% of 2025 revenue thanks to large tender volumes and private-insurance uptake.

What is driving faster growth in Mexico?

IMSS tele-monitoring pilots, obesity-label approvals for tirzepatide, and ISSSTE renal-protection coverage are together pushing a 10.57% forecast CAGR.

When will biosimilar competition meaningfully impact pricing?

Semaglutide’s patent expires in Brazil in March 2026; Fiocruz-EMS aims to supply biosimilars by 2028, which could lower public acquisition prices by up to 40%.

Page last updated on: