Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

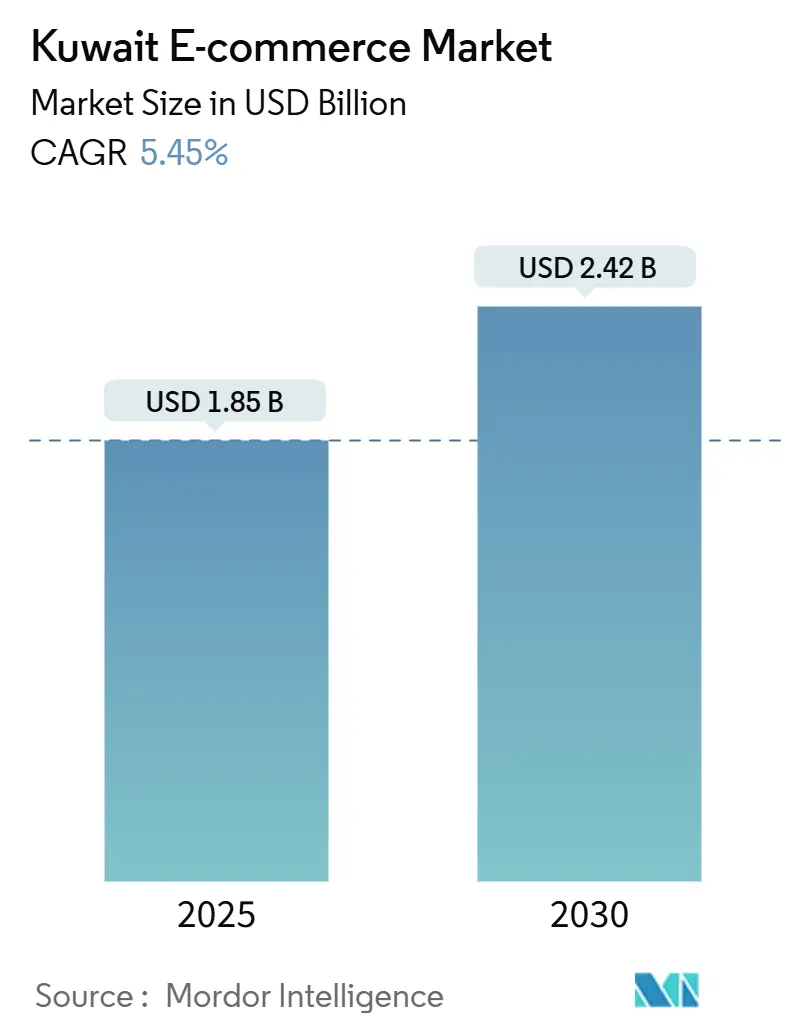

| Market Size (2025) | USD 1.85 Billion |

| Market Size (2030) | USD 2.42 Billion |

| Growth Rate (2025 - 2030) | 5.45% CAGR |

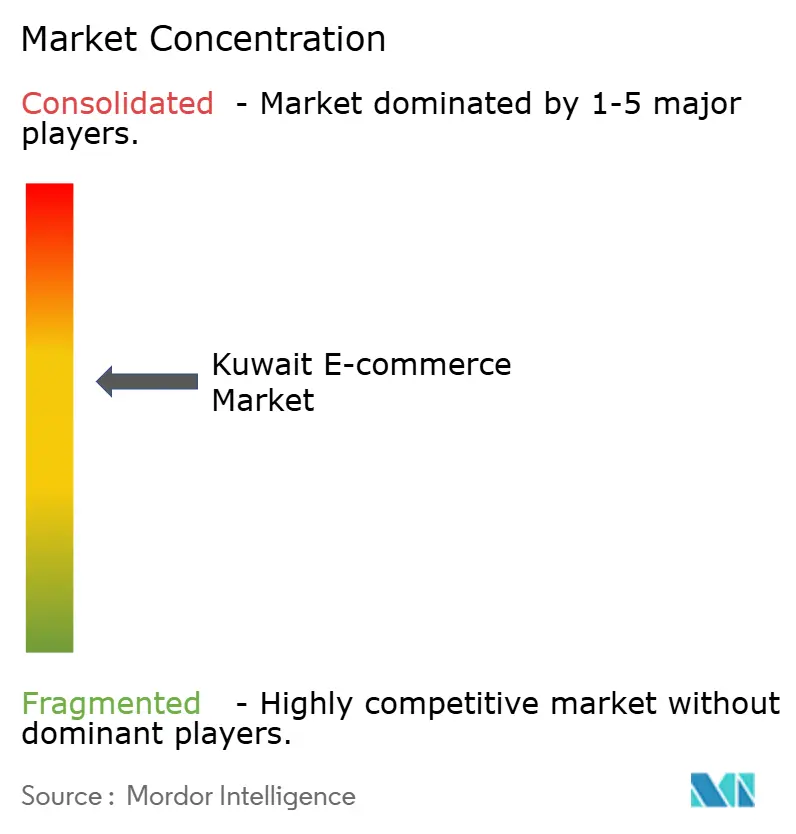

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Kuwait E-commerce Market Analysis by Mordor Intelligence

The Kuwait e-commerce market is valued at USD 1.85 billion in 2025 and is forecast to reach USD 2.42 billion by 2030, translating into a 5.45% CAGR over the period. The steady expansion mirrors the country’s broader digital transformation program, which channels significant public investment into 5G connectivity, cloud capacity, and fintech regulation. Demand is reinforced by 99.7% internet penetration, 158% mobile-subscription density, and Kuwait Pay’s rapid rollout, collectively reducing friction for online shopping and merchant onboarding. The competitive field is becoming more layered as foreign platforms respond to new ownership rules while local players leverage Kuwait Direct Investment Promotion Authority (KDIPA) grants to digitize legacy retail formats. At the product level, consumer electronics still anchor revenue, yet on-demand grocery and prepared-meal fulfillment have gained momentum as dark-store operators race to secure micro-warehousing in Kuwait City’s dense districts. Together, these drivers position the Kuwait e-commerce market as a digitally maturing economy inside the GCC rather than a nascent adopter.

Key Report Takeaways

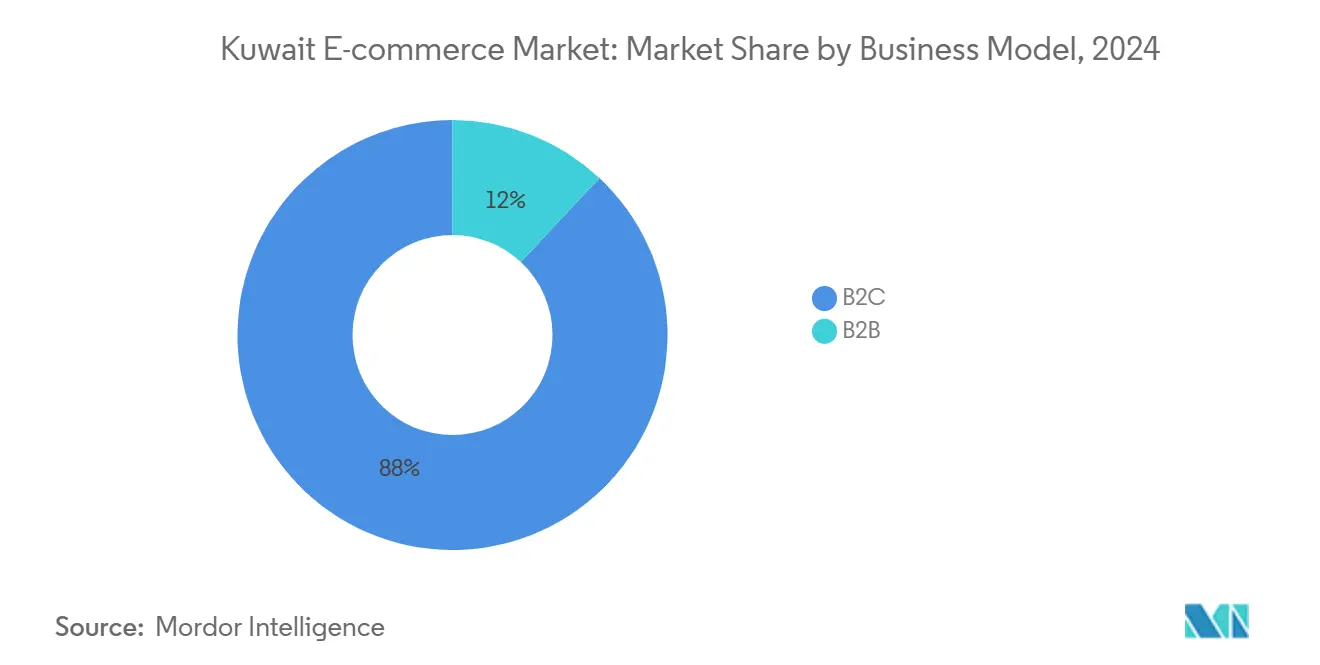

- By business model, the B2C segment held 88.03% of the Kuwait e-commerce market share in 2024, while B2B is projected to compound at 9.12% through 2030.

- By device type, smartphones captured 72.43% revenue share in 2024; other device types are forecast to expand at a 10.35% CAGR to 2030.

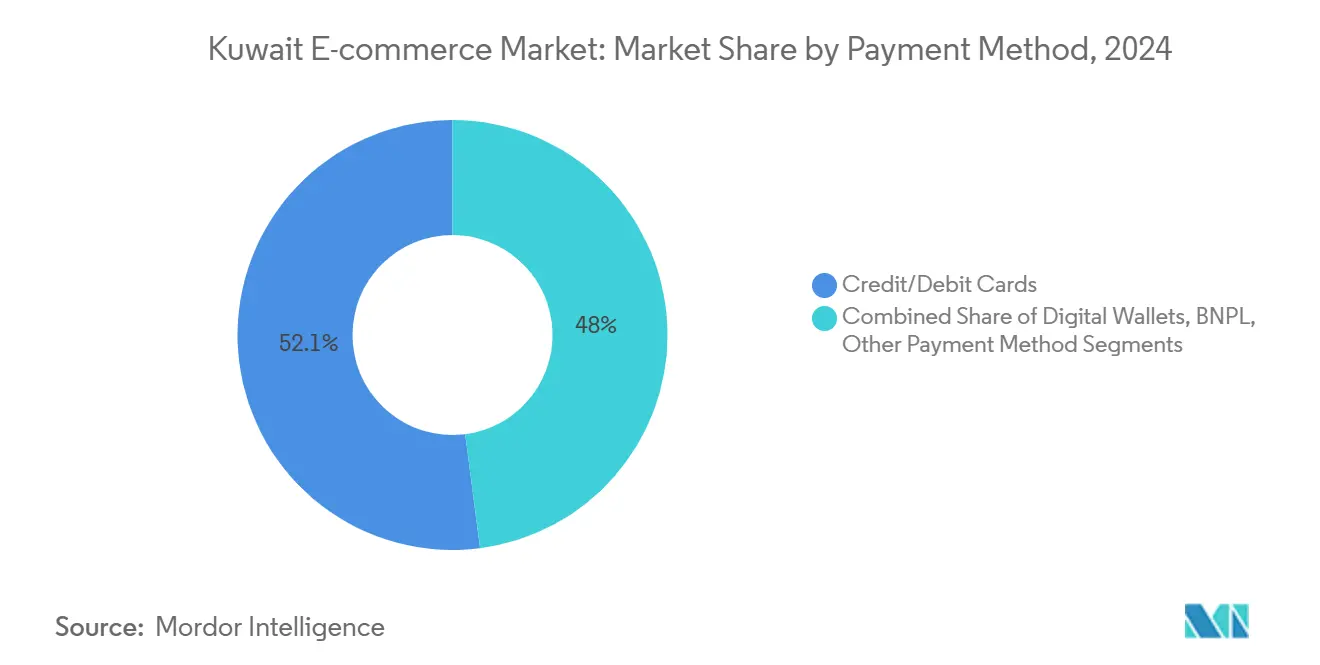

- By payment method, cards accounted for 52.05% of the Kuwait e-commerce market size in 2024, whereas digital wallets register the highest projected CAGR at 11.42% to 2030.

- By B2C product category, consumer electronics commanded 34.06% share of the Kuwait e-commerce market size in 2024, with food & beverages advancing at a 12.21% CAGR through 2030.

Kuwait E-commerce Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Domestic Digital Wallet Adoption Driven by "Kuwait Pay" & Mobile-Banking Reforms | +1.2% | National, with early gains in Kuwait City, Hawalli, Farwaniya | Medium term (2-4 years) |

| Rapid Expansion of On-Demand Quick-Commerce Dark Stores in Kuwait City | +0.8% | Kuwait City metropolitan area, spillover to Ahmadi | Short term (≤ 2 years) |

| Mandate for 2024 Government E-Invoicing Accelerating Merchant On-Boarding | +0.6% | National, concentrated in commercial districts | Short term (≤ 2 years) |

| 5G Roll-Out Enabling Rich-Media Shopping & Live Commerce | +0.9% | National coverage with urban concentration | Medium term (2-4 years) |

| Rising Cross-Border Purchasing Limits after GCC Customs Unification | +0.4% | GCC-wide, with Kuwait as import hub | Long term (≥ 4 years) |

| KDIPA Grants Digitalizing SME Retailers & Expanding Seller Base | +0.3% | National, focused on traditional retail sectors | Long term (≥ 4 years) |

Source: Mordor Intelligence

Surge in Domestic Digital-Wallet Adoption Driven by “Kuwait Pay” & Mobile-Banking Reforms

Digital-wallet penetration is accelerating as regulatory clarity encourages banks and fintech start-ups to launch frictionless payment products. The Central Bank’s 2024 digital-banking law enabled Kuwait Finance House to introduce WAMD instant transfers, embedding biometric authentication that lowers fraud risk and raises consumer confidence.[1]Kuwait Finance House, “KFH Launches WAMD Instant Transfers,” kfh.com Apple Pay and Google Pay achieved nationwide merchant acceptance by early 2024, compressing adoption cycles previously measured in years into quarters.[2]Trade.gov, “Digital Wallet Acceptance in Kuwait,” trade.gov As a result, cash-on-delivery (COD) usage fell to 20% in 2023, releasing working-capital pressure on merchants and feeding incremental gross-merchandise-value growth. Banks benefit from higher fee pools and richer data streams, while merchants gain lower checkout abandonment and stronger loyalty. The spillover effect supports ancillary services such as micro-lending and pay-by-installment models.

Rapid Expansion of On-Demand Quick-Commerce Dark Stores in Kuwait City

Over the last 18 months, operators have opened dozens of hyper-local dark stores within Kuwait City’s dense neighborhoods to meet sub-60-minute delivery expectations. Talabat’s USD 2 billion IPO proceeds fund multi-category fulfillment capacity, pushing the platform’s revenue to USD 2.2 billion in 2023. These facilities incorporate temperature-controlled zones to handle fresh groceries and pharmaceuticals, creating high capital barriers for newcomers. Real-estate clustering near Kuwait City’s commercial arteries minimizes route length but leaves suburban demand under-served, signaling white-space opportunities for regional specialists with cold-chain know-how. Inventory optimization software and predictive analytics tools are now mandatory to curb stockouts and shrinkage.

Mandate for 2024 Government E-Invoicing Accelerating Merchant On-Boarding

The Ministry of Commerce and Industry’s compulsory e-invoice framework nudges unregistered merchants into the formal economy, forcing them to adopt POS terminals and digital payments. Standardized data flow produces clean transaction histories that improve credit-scoring accuracy, enabling banks to extend working-capital lines at lower risk. ERP vendors and systems integrators are capitalizing on demand for compliant plug-ins, while payment processors gain broader acceptance networks. Implementation costs weigh heavier on micro-retailers, raising the likelihood of consolidation or platform partnerships that offer turnkey compliance.

5G Roll-Out Enabling Rich-Media Shopping & Live Commerce

Ninety-seven percent population coverage in 5G lets retailers stream high-resolution product demos, host live auctions, and deploy augmented-reality try-ons without buffering. Platforms investing in immersive interfaces secure higher conversion and reduced returns, especially in categories such as fashion and home décor where tactile inspection matters. The technical leap also supports influencer-led flash sales hosted inside social networks, blending entertainment with commerce. Development costs are significant, but first movers enjoy defensible differentiation as consumers equate superior visual fidelity with trustworthiness.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Last-Mile Costs from Low Address-System Density Outside Urban Centers | -0.7% | Suburban and rural areas outside Kuwait City | Long term (≥ 4 years) |

| Cultural Preference for COD Hinders the Market | -0.5% | National, with higher impact in traditional communities | Medium term (2-4 years) |

| Foreign-Ownership Caps in Select Verticals Limiting Global Seller Participation | -0.3% | National, affecting international platform operations | Long term (≥ 4 years) |

| Scarcity of Automated, Temperature-Controlled Fulfilment Space | -0.4% | Kuwait City and major commercial centers | Medium term (2-4 years) |

Source: Mordor Intelligence

High Last-Mile Costs from Low Address-System Density Outside Urban Centers

In many suburban districts, courier drivers must rely on landmarks or phone directions due to non-standardized addresses, lifting per-parcel cost and extending delivery windows. Shuwaikh Port truck restrictions during peak hours add complexity for inbound freight, delaying inventory restocking.[3]Kuwait Port Authority, “Operational Notice on Shuwaikh Truck Access,” ports.gov.kw International 3PLs such as Kuehne + Nagel have built new hubs in Dubai to serve the wider GCC, yet Kuwaiti last-mile inefficiencies remain unresolved. Absent a unified addressing initiative, e-retailers over-index on Kuwait City volumes, constraining penetration in outlying governorates.

Cultural Preference for COD Hinders the Market

While COD’s share fell from 41% in 2020 to 20% in 2023, older demographics and traditional households still favor cash settlement, requiring dual delivery workflows. Cash handling raises security concerns and inflates vehicle-idle time, pressuring carrier margins. Moreover, COD orders limit data harvest, impairing personalization algorithms that underpin higher average-order values. Over time, digital-ID proliferation and biometric onboarding are expected to erode remaining COD reliance, but the transition remains uneven across segments and geographies.

Segment Analysis

By Business Model: Accelerating B2B Platform Uptake

B2C transactions dominated 88.03% of revenue in 2024, reflecting long-standing consumer enthusiasm for cross-border shopping and branded electronics. However, B2B sales are forecast to grow at 9.12% CAGR, outpacing the broader Kuwait e-commerce market as e-invoicing and KDIPA subsidies reduce integration frictions for SME suppliers. The forthcoming Domestic Minimum Top-Up Tax compels large enterprises to document transaction trails digitally, making electronic procurement portals more attractive. As cross-border logistics become cheaper under the GCC tariff code, Kuwaiti wholesalers are utilizing marketplace rails to reach Saudi and UAE buyers, lowering customer-acquisition cost and widening assortment depth. C2C remains niche because cultural norms favor in-person negotiation and limited third-party trust mechanisms.

A parallel evolution is unfolding in platform monetization. Subscription-based B2B portals are experimenting with embedded trade-finance tools that draw on structured invoice data, offering next-day settlement against a small fee. Such innovations shorten cash cycles for contractors serving Kuwait’s oil and construction sectors and ultimately expand the Kuwait e-commerce market.

By Device Type: Mobile Dominance With Emerging Multi-Screen Commerce

Smartphones maintained 72.43% of purchases in 2024, reflecting Kuwait’s status as a mobile-first society. Nevertheless, the “Other Device Types” segment—smart TVs, voice assistants, kiosks, and wearables—is projected to log a 10.35% CAGR, hinting at multi-modal engagement. Household penetration of smart TVs is rising alongside fiber-to-the-home upgrades, enabling couch-commerce tied to streaming apps. Voice-activated re-ordering via smart speakers resonates with time-pressed households, especially for essentials such as bottled water and pet food. In-store kiosks deployed by consumer-electronics chains now facilitate endless-aisle browsing, converting floor-space into digital showrooms. These developments diversify funnel entry points and raise lifetime value across the Kuwait e-commerce market.

Sellers optimize for both micro-moments on handheld screens and immersive browsing on widescreen TVs, using adaptive design and compressed-checkout APIs. The shift augments customer-acquisition economics by distributing ad spend across previously untapped contexts.

By Payment Method: Wallets Challenge Card Hegemony

Cards represented 52.05% of transaction value in 2024, anchored by KNET’s network, yet digital wallets are on a 11.42% CAGR trajectory, shrinking the share of cards over the forecast horizon. Wallets combine loyalty programs, biometric sign-in, and one-click payout, decreasing cart abandonment by double-digit percentages in pilot studies shared by leading marketplaces. Kuwait Finance House’s facial-recognition login and WAMD instant transfers accelerate settlement speeds beyond traditional interchange rails, spotlighting a roadmap for banks to monetize micro-payments. BNPL usage, though small, is multiplying among 18-34-year-olds, often embedded at the product-detail page. Regulatory guardrails remain nascent, giving early movers a chance to shape consumer expectations and underwriting frameworks. Cryptocurrencies remain peripheral given capital-control vigilance.

Note: Segment shares of all individual segments available upon report purchase

By B2C Product Category: Electronics Sustain Volume While Food Outpaces Growth

Consumer electronics held a 34.06% slice in 2024, benefiting from affluent consumers who refresh smartphones every two to three years. Samsung’s 2024 revenue of KRW 225,082.6 billion (USD 168.4 billion) underscores enduring appetite for flagship devices in GCC markets. Yet margins are tightening as gray-market imports and flash-sale pricing erode average selling price, pushing retailers to diversify into services and extended warranties. Food & beverages are set to register a 12.21% CAGR through 2030, catalyzed by dark-store penetration and temperature-controlled delivery innovations. Quick-commerce players integrate AI demand-forecasting to cut waste, and strategic partnerships with local farms improve freshness perception, bolstering repeat purchase rates.

Fashion’s omnichannel pivot continues, evidenced by H&M’s 30% digital sales ratio. Home-furnishing categories grapple with bulky-item logistics, but 3D-room-planner tools are closing visualization gaps. Media, toys, and DIY supplies benefit from downloadable or subscription formats, smoothing supply-chain constraints and locking in recurring revenue.

Geography Analysis

Kuwait sits at the northern edge of the GCC trade corridor, allowing merchants to leverage customs-union privileges for inventory pooling and export redistribution. The January 2025 Integrated Customs Tariff lifts the number of product codes to 13,400, synchronizing inspection procedures with neighbors and trimming clearance times, thereby enlarging the addressable cross-border segment of the Kuwait e-commerce market. Shuwaikh Port’s 21 berths and 3.2 million m² footprint underpin container throughput, yet restricted truck access during peak hours obliges retailers to rebalance inventory toward off-peak inbound slots and micro-fulfillment nodes.

Domestically, Kuwait City, Hawalli, and Farwaniya absorb the majority of online spending, but rising 5G coverage extends the serviceable area to Ahmadi and Jahra. Rural penetration faces the dual challenge of address ambiguity and lower basket values, tempering last-mile ROI. Nonetheless, biometrics-enabled national-ID rollouts have surpassed 3 million registrations, creating a reliable KYC backbone for fintech onboarding nationwide.

Competitive tension comes from UAE and Saudi Arabia, whose logistics investments dwarf Kuwait’s. UAE’s freight market is projected at USD 27.51 billion by 2029, prompting Kuwaiti policymakers to fast-track bonded-warehouse licenses and digital-free-zone pilots. Meanwhile, Decree No. 114/2024 restricts foreign majority stakes in certain e-commerce operations, nudging multinationals toward joint ventures with local sponsors. The policy aims to retain value onshore, though it raises compliance diligence for new entrants.

Longer term, cross-border purchasing caps are increasing under GCC harmonization, letting Kuwaiti consumers access a more diverse catalogue while smoothing import duties. For merchants, synchronized product codes unlock scale in procurement, reducing landed cost per unit and strengthening Kuwait’s role as a re-export node. Consequently, the Kuwait e-commerce market is set to deepen integration with regional supply chains, yet maintain idiosyncratic regulatory nuances that require bespoke operating models.

Competitive Landscape

The Kuwait e-commerce market displays moderate concentration anchored by half a dozen regional champions. Talabat leverages its mature rider network and payment wallet to extend into pharmacy and pet-care SKUs, pursuing order-frequency uplift per active user. Noon focuses on first-party inventory for electronics and fashion, countering Amazon’s marketplace breadth with private-label price aggression. Ubuy differentiates via cross-border catalog access, importing niche brands under simplified customs clearance.

On the omnichannel front, Carrefour and Lulu integrate click-and-collect services at hypermarkets, exploiting real-estate footprint to reduce last-mile cost and raise basket size. Their loyalty programs feed data into AI assortment planning, aiming for margin recovery. At the technology layer, start-ups such as Tap Payments and One Global underscore the rise of payment-as-a-service, attracting banks that seek wallet white-labeling options.

Regulatory milestones shape rivalry. Mandatory e-invoicing advantages platforms with mature seller dashboards, while the 15% Domestic Minimum Top-Up Tax affects profitability modeling for large multinationals, potentially slowing aggressive discounting campaigns but also lowering predatory pricing risks to domestic players. Biometric authentication investments raise the bar on security, creating switching friction that benefits early adopters.

Strategic moves underscore differentiation. Talabat’s USD 2 billion IPO signals long-term capital availability for horizontal expansion. Amazon’s 2024 introduction of Arabic voice search tailors the UI to local preferences, raising conversion among first-time online shoppers. Noon’s cross-listing of noon Pay as a separate fintech subsidiary diversifies revenue beyond retail, mirroring global platform-play strategies.

Kuwait E-commerce Industry Leaders

-

Apparel Group FZ-LLC – 6thStreet.com

-

Namshi General Trading LLC

-

H&M Hennes and Mauritz AB

-

Ubuy Inc.

-

Noon AD Holdings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: GCC disclosed collective 2023 GDP of USD 2.1 trillion and foreign direct investment of USD 649 billion, strengthening the macro foundation for intra-regional e-commerce.

- January 2025: The GCC Customs Union Authority implemented an integrated tariff system with 13,400 codes.

- January 2025: Kuwait enacted a 15% Domestic Minimum Top-Up Tax on multinationals earning EUR 750 million (USD 816 million) or more.

- November 2024: Kuwait Finance House launched WAMD instant transfers and added facial recognition log-in across its digital suite.

Kuwait E-commerce Market Report Scope

The Kuwait e-commerce market is segmented into B2B E-commerce and B2C E-commerce. By B2C E-commerce, the market studied is further subdivided into beauty and personal care, consumer electronics, fashion and apparel, food and beverage, and furniture and home. The report analyzes the impact of COVID-19 on the studied market.

The study also tracks important market metrics, underlying growth influencers, and significant industry vendors, providing support for Kuwait's market estimates and growth rates throughout the anticipated period. The study assesses COVID-19's overall influence on the market.

| By Business Model | B2C |

| B2B | |

| By Device Type | Smartphone / Mobile |

| Desktop and Laptop | |

| Other Device Types | |

| By Payment Method | Credit / Debit Cards |

| Digital Wallets | |

| BNPL | |

| Other Payment Method | |

| By B2C Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories |

By Business Model

| B2C |

| B2B |

By Device Type

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method

| Credit / Debit Cards |

| Digital Wallets |

| BNPL |

| Other Payment Method |

By B2C Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Kuwait e-commerce market?

The market stands at USD 1.85 billion in 2025 and is forecast to reach USD 2.42 billion by 2030.

Which product category generates the most revenue online in Kuwait?

Consumer electronics leads with 34.06% share, although food & beverages show the fastest growth at 12.21% CAGR.

How fast are digital wallets growing compared with cards?

Digital wallets are projected to expand at 11.42% CAGR between 2025 and 2030, outstripping card growth and steadily compressing card dominance.

What are the main regulatory changes affecting foreign e-commerce players?

Decree No. 114/2024 limits foreign ownership stakes, while the 15% Domestic Minimum Top-Up Tax elevates compliance costs for large multinationals.

Why do last-mile delivery costs remain high outside Kuwait City?

Low address-system density forces carriers to rely on landmark navigation and phone-coordination, increasing travel time and labor overhead.

Will B2B e-commerce overtake B2C in Kuwait?

B2B is growing faster at 9.12% CAGR, yet B2C retains the majority share; convergence depends on how quickly SMEs adopt digital procurement platforms supported by e-invoicing mandates.

Page last updated on: June 30, 2025