Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.19 Billion |

| Market Size (2026) | USD 2.24 Billion |

| Market Size (2031) | USD 2.52 Billion |

| Growth Rate (2026 - 2031) | 2.35% CAGR |

| Market Concentration | Medium |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Kenya Flexible Packaging Market Analysis by Mordor Intelligence

Kenya flexible packaging market size in 2026 is estimated at USD 2.24 billion, growing from 2025 value of USD 2.19 billion with 2031 projections showing USD 2.52 billion, growing at 2.35% CAGR over 2026-2031. Steady expansion is anchored in Kenya’s role as East Africa’s manufacturing base, public-sector incentives under Vision 2030, and resilient consumer demand in food, personal care, and pharmaceutical segments. Government-backed County Aggregation and Industrial Parks streamline crop aggregation and post-harvest processing, sustaining order volumes even as infrastructure gaps and foreign-exchange swings temper topline growth. Regulatory tightening under the 2024 Extended Producer Responsibility (EPR) rules pushes brand owners toward recyclable or compostable films, accelerating product development in bioplastics. Meanwhile, quick-commerce adoption in Nairobi and Mombasa heightens demand for portion-controlled pouches and sachets that withstand multiple handling points without compromising appearance. Access to geothermal power at the Olkaria Green Energy Park supports cost optimization for energy-intensive extrusion and printing, partially offsetting exchange-rate-driven resin price spikes.

Key Report Takeaways

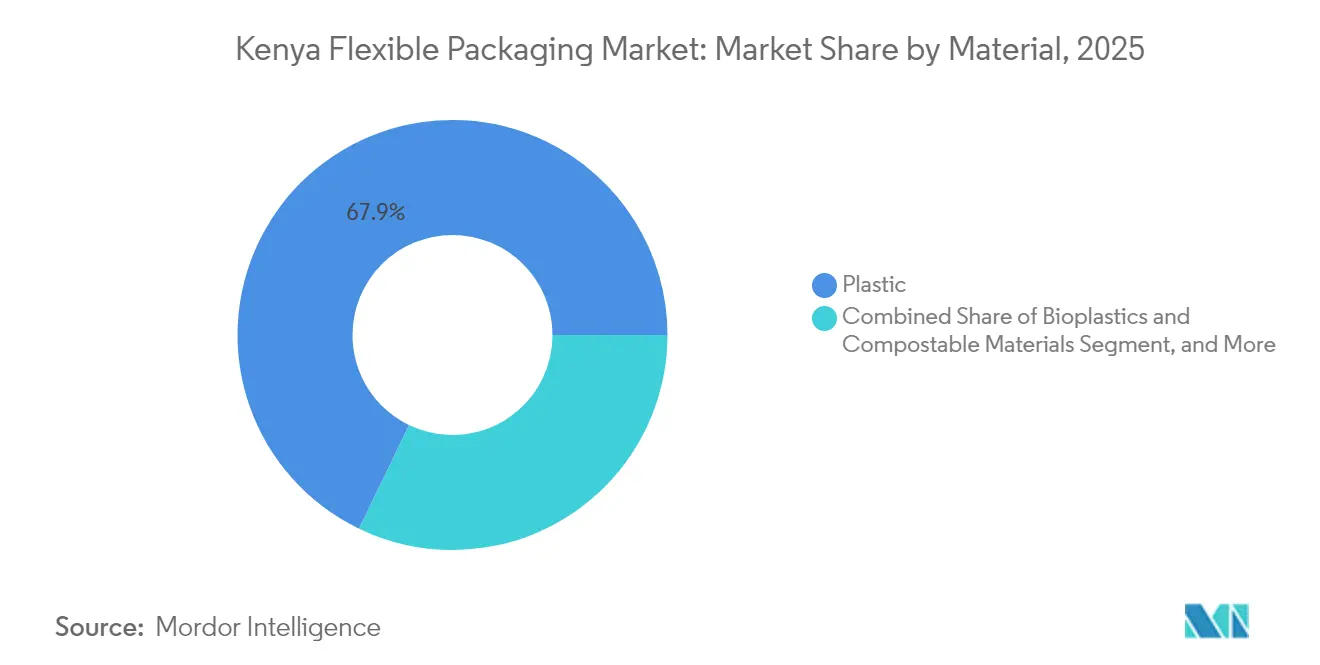

- By material, plastic maintained a 67.85% share of the Kenya flexible packaging market in 2025, whereas bioplastics and compostables are poised for a 4.95% CAGR through 2031.

- By product type, bags and pouches led with 46.92% of the Kenya flexible packaging market share in 2025, while sachets and stick packs are projected to grow at a 4.44% CAGR to 2031.

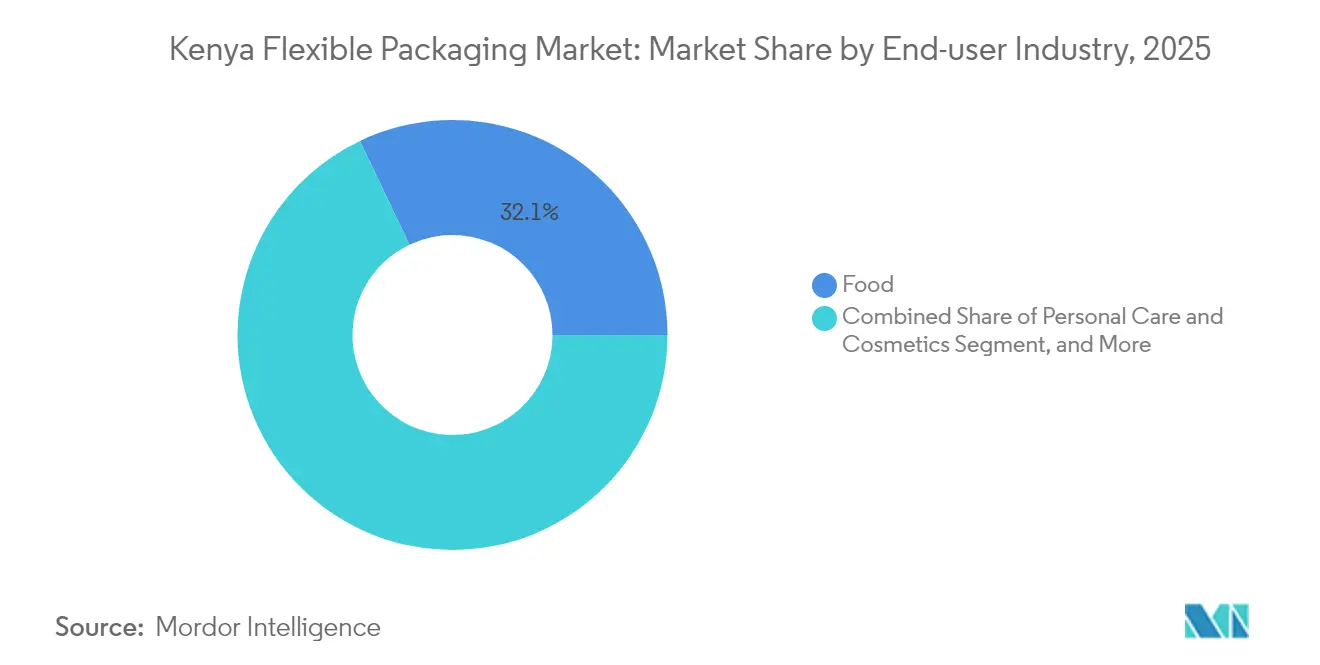

- By end-user industry, food applications represented 32.08% of the Kenya flexible packaging market size in 2025, and personal care and cosmetics is forecast to expand at a 4.71% CAGR through 2031.

- By printing technology, flexography accounted for 45.05% of the Kenya flexible packaging market share in 2025; digital printing is expected to register a 4.89% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kenya Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin |

|---|---|---|---|

| Rise of branded FMCG and modern retail penetration | +0.8% | National, concentrated in Nairobi, Mombasa, Kisumu | Medium term (2-4 years) |

| Explosive growth of quick-commerce and dark-store models | +0.4% | Urban centers, Nairobi metropolitan area | Short term (≤ 2 years) |

| Agricultural-export upgrade to value-added consumer packs | +0.6% | National, strongest in horticultural zones | Long term (≥ 4 years) |

| Mandatory EPR and recyclability targets | +0.3% | National implementation via NEMA | Medium term (2-4 years) |

| Surge in off-grid solar-powered cold-chain nodes up-country | +0.2% | Rural and semi-urban areas | Long term (≥ 4 years) |

| Corporate carbon-footprint pledges driving light-weighting | +0.3% | Global brands operating in Kenya | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise of Branded FMCG and Modern Retail Penetration

Modern supermarkets and convenience chains are expanding beyond Nairobi into secondary towns, compelling consumer-goods producers to adopt high-barrier laminates that preserve freshness, support brand visibility, and meet shelf-readiness standards. [1]Propak East Africa, “Packaging,” propakeastafrica.com Local processors investing under Vision 2030’s manufacturing pillar need tamper-evident seals, resealable zippers, and on-pack labelling that comply with Kenya Bureau of Standards food-safety rules. Flexible films enable SKU proliferation for new flavors and pack sizes without large mold investments, a critical advantage in promotional-driven retail environments. Branded packs also reduce the grey-market diversion that erodes margins in traditional trade channels. As more retailers demand traceability, converters offering variable-data printing gain priority status in supplier rosters.

Explosive Growth of Quick-Commerce and Dark-Store Models

Same-hour delivery platforms require packaging that survives multiple touchpoints from automated picking through motorbike transport to the consumer’s doorstep. Dimensional efficiency becomes vital for basket-optimization algorithms, pushing converters to engineer thinner, stronger multi-layer pouches. Urban consumers increasingly reject over-packaging, so lightweight mono-material films compatible with soft-plastic take-back schemes are in demand. Dark stores favor easy-tear features for rapid order assembly, which in turn drives adoption of laser-scored sachets. Brands leverage digitally printed limited-edition graphics to differentiate in app-based storefronts where thumbnail images influence conversion rates. The intersection of speed, protection, and sustainability positions flexible packaging as the preferred format for Kenya’s quick-commerce boom.

Agricultural-Export Upgrade to Value-Added Consumer Packs

Horticultural exports topped 580,648 t in the first 10 months of 2023, and government programs now subsidize pack-houses that add consumer-ready presentation for European supermarkets. Lightweight liners such as Cargolite cartons reduce airfreight costs and carbon footprint while maintaining structural integrity for cut flowers. AI-enabled cold-chain monitoring from the Kenya Agriculture and Livestock Research Organization informs film-selection decisions to control respiration rates and ethylene migration. Exporters increasingly demand modified-atmosphere pouches for ready-to-eat fresh produce, spurring localized production of barrier films once imported from South Africa. The upshift to retail-ready packs boosts converter margins because technical specs and certification requirements limit low-end competition.

Mandatory EPR and Recyclability Targets

The 2024 Sustainable Waste Management Regulations require every package placed on the market to be reported, and fees are assessed per kilogram through Producer Responsibility Organizations such as KEPRO. Converters must generate lifecycle data and submit design-for-recycling evidence, which raises compliance costs yet positions early movers as preferred suppliers to multinational FMCG firms bound by global circular-economy pledges. Demand is rising for mono-polyolefin laminates that meet polyethylene recycling streams and for compostable films certified to EN 13432. EPR fees also accelerate light-weighting because lower material use translates directly into lower levy payments. The rules shift competitive advantage toward firms with in-house lab testing, chain-of-custody documentation, and accredited recycling partners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FX-driven resin cost volatility | -0.5% | National, affecting all importers | Short term (≤ 2 years) |

| Chronic electricity supply gaps outside Nairobi industrial parks | -0.3% | Rural and secondary urban manufacturing zones | Medium term (2-4 years) |

| Informal micro-packers diluting quality and price discipline | -0.4% | National, concentrated in peri-urban areas | Medium term (2-4 years) |

| Talent scarcity for high-speed printing and lamination lines | -0.2% | National, acute in specialized manufacturing zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FX-Driven Resin Cost Volatility

Polyethylene and polypropylene are imported in U.S. dollars, so shilling depreciation quickly inflates raw-material bills that constitute 60-70% of converter costs. [2]Central Bank of Kenya, “Monthly Exchange Rate (Period Average),” centralbank.go.ke While large players hedge through forward contracts, smaller firms struggle to finance letters of credit, forcing them to accept spot prices and eroding margins. Frequent price revisions alienate price-sensitive agricultural clients who negotiate annual contracts pegged in local currency. High import bills also raise working-capital requirements, limiting funds for equipment upgrades. Although a managed float offers some stability, global crude-based resin price swings add an extra layer of unpredictability that acts as a brake on capital-spending plans.

Chronic Electricity Supply Gaps Outside Nairobi Industrial Parks

Extrusion and lamination lines suffer costly downtime when power dips, causing waste and off-spec runs that must be scrapped. Utilities report over 14 interruptions a month in industrial zones beyond Athi River, compelling converters to invest in diesel gensets that raise energy costs to 28 US cts/kWh versus the grid’s 15 US cts/kWh. [3]The Standard Opinion Desk, “Why Kenya's manufacturing future hubs on clean energy,” standardmedia.co.ke Thermal-shock damage to motors accelerates maintenance cycles and shortens equipment life. Even when grid power is available, voltage variability affects color consistency in flexo printing. The forthcoming Olkaria Green Energy Park offers geothermal electricity at 7 US cts/kWh, but uptake is limited by distance from customer clusters in Nairobi. Until distribution upgrades materialize, power reliability will remain a growth bottleneck.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Sustainability Moves the Center of Gravity

Plastic captured 67.85% of the Kenya flexible packaging market in 2025 thanks to its cost-effectiveness, seal integrity, and adaptability across verticals. However, EPR levies and brand-owner carbon pledges channel R&D budgets toward starch-based and polylactic-acid films that degrade under industrial compost conditions. Bioplastics are projected to grow at a 4.95% CAGR to 2031, outpacing overall market growth and narrowing the price gap with conventional polymers through duty waivers on imported feedstocks. Paper/foil laminates retain niche appeal in premium biscuits and confectionery, while aluminum foil continues as the barrier of choice in high-value pharmaceuticals that require <0.1 cc/m²/day oxygen transmission.

Kenyan converters upscale by integrating additive masterbatches like Vitapak’s VP Bioadd, which enables oxo-biodegradation per ASTM D5511 without compromising optical clarity. Investments in tandem extrusion lines support the production of mono-material PE-PE structures compatible with Nairobi’s soft-plastic take-back scheme. Still, plastics will remain the economic backbone of the Kenya flexible packaging market through 2030 because rigid packaging substitutes cannot meet the lightweight ratios demanded by food processors. Long-term shifts will hinge on steady resin supply at predictable prices and on the scalability of local composting infrastructure.

By Product Type: Portion Control Shapes Demand Curves

Bags and pouches contributed 46.92% to the Kenya flexible packaging market size in 2025 due to broad usage across grains, fertilizers, and detergents. The format benefits from manufacturing economies of scale, easy palletization, and established filling machinery in local factories. Films and wraps persist in bulk agriculture, but their share is edging lower as brands migrate to pre-formed stand-up pouches that provide billboard-like shelf impact. Sachets and stick packs are forecast to lead growth at a 4.44% CAGR thanks to urban consumers preferring single-use packs aligned with daily wage cycles.

Digital presses such as Canon’s V1350 reduce minimum order quantities, encouraging hyper-segmented flavors and promotional artwork without holding costly inventories. Automated multi-lane form-fill-seal equipment widens the cost advantage of stick packs in instant beverage powders and condiments. However, sachet litter remains a public concern, so brand owners test water-soluble films and rigid-paper micro-canisters. Continued innovation is likely to tilt the product mix toward reclosable small packs that balance convenience with lower material-to-product ratios.

By End-User Industry: Food Security at Center Stage

The food sector commanded 32.08% of the Kenya flexible packaging market in 2025 because processors rely on oxygen- and moisture-barrier laminates to cope with a 90 km average farm-to-market distance. Government subsidies for post-harvest cold-chain link solar-powered coolers to multi-layer films that slow respiration in fresh-produce packs. Demand for ready-to-eat cereals and frozen snacks is expanding among the middle class, driving the adoption of microwaveable pouches with susceptor layers. Beverage companies increase orders for retortable spouted pouches that reduce transportation costs by 35% versus glass.

Personal care and cosmetics will post the fastest gains at a 4.71% CAGR through 2031 as rising disposable income boosts consumption of hair-care sachets and moisturizers. Flexible tubes with high-definition flexo printing position local brands alongside international imports on pharmacy shelves. Pharma demand leans on aluminum-foil laminates for moisture-sensitive antibiotics, while agrochemical users shift to co-extruded fitments that prevent spillage. Each vertical’s trajectory underscores how the Kenya flexible packaging market rewards converters capable of customizing barrier, dispensing, and decoration features.

By Printing Technology: Hybrids Bridge Volume and Agility

Flexography held 45.05% of the Kenya flexible packaging market share in 2025, owing to dependable line speeds and declining plate costs. New CI flexo presses with automatic register control cut makeready waste, making the process viable for runs as low as 1,500 m². Rotogravure still owns premium confectionery wrappers where high-density metallic inks drive shelf appeal, but cylinder costs deter short campaigns. Digital printing’s projected 4.89% CAGR stems from e-commerce brands launching micro-series SKUs; their break-even point favors inkjet at fewer than 10,000 impressions.

Converters respond with hybrid workflows, laminating digitally printed top webs to flexo-printed bottom webs, combining agility with cost efficiency. Platinum Packaging’s twin Bobst Master M6 lines integrate inline inspection to maintain ±50 micron register tolerance even at 400 m/min, and an HMI interface reduces changeover to 6 minutes. Meanwhile, desktop digital varnish units add tactile finishes on demand, supporting premiumization in cosmetics. Print-technology convergence will accelerate as brand owners impose shorter lead times and request serialized QR codes for traceability.

Geography Analysis

Nairobi’s Industrial Area and Athi River corridor host more than 60% of Kenya flexible packaging market output, leveraging proximity to FMCG headquarters, port logistics, and skilled technicians. Rental prices in Athi River rose 6.7% in 2024, prompting manufacturers to scout satellite hubs such as Juja and Ruiru, where land costs remain 30% lower, yet road links connect efficiently to the Northern Bypass. County governments co-fund CAIPs that bundle access roads, wastewater plants, and customs one-stop shops, enabling startups to cut commissioning time by six months. For resin-intensive operations, Naivasha’s Olkaria Green Energy Park offers geothermal power priced at USD 0.07 per kWh, slashing electricity bills by half compared with grid averages.

Mombasa Industrial Park serves coastal agro-exporters needing proximity to the port, but chronic congestion on the Mombasa-Nairobi highway drives some converters inland. In western Kenya, Mumias Agri-Processing Zone targets cane-based bioplastics, signaling regional diversification from the Nairobi core. Cross-border trade under the East African Community’s common external tariff allows Kenyan converters to ship duty-free to Uganda, Tanzania, and Rwanda. In 2023, plastic hose exports hit USD 688,840, with Rwanda accounting for USD 166,200, underscoring the Kenya flexible packaging market’s regional reach.

Logistics-intensive sectors favor Nairobi for inbound airfreight of high-spec barrier films and outbound charter flights of horticultural produce. However, companies relying on bulky inputs such as kraft paper locate near Mombasa to save on inland container costs. Supply-chain fluidity influences site selection as operators weigh energy premiums, land price trajectories, and customer clustering against customs efficiencies. Geographic fragmentation will rise as green industrial parks proliferate, yet Nairobi will retain primacy due to its dense ecosystem of ink suppliers, pre-press studios, and maintenance contractors.

Competitive Landscape

The Kenya flexible packaging market hosts a blend of legacy family-owned converters and global entrants, creating a moderate concentration. General Printers Limited leverages four decades of local sourcing relationships to secure volumes in staple food liners, while Platinum Packaging differentiates through solvent-free lamination and food-grade cleanroom certification. Newcomer Nexgen Packaging assembled a green-certified Nairobi plant in April 2024 to supply care labels and heat-transfer films, bringing enterprise resource planning integration that speeds artwork approvals.

Technology investments define competitive edge. Skanem Interlabels added an automated Bobst Master M5 line with turret rewinding and driven chill drums to double output in health-and-beauty labels. Locally, Sky Labels expanded into a 4,000 m² factory, indicating confidence in sustained demand for pressure-sensitive formats. Foreign players like Mondi influence market dynamics indirectly by licensing paper-based barrier solutions that local converters adopt under partnership deals. Meanwhile, informal micro-packers remain active but gradually lose share as supermarkets enforce traceability documentation and as EPR levies penalize non-compliant packaging.

Strategic alliances with raw-material suppliers have become vital to mitigate resin volatility. Larger Kenyan converters negotiate quarterly indexed pricing with Middle-East polymer producers, shielding themselves from spot-market shocks. Some players explore vertical integration into film extrusion to secure supply and capture margin. Intellectual-property barriers remain low, so customer service, on-time delivery, and regulatory advisory support define supplier stickiness. Sustainable-material processing capacity will be the next battleground as multinational brands move toward regional recycled-content mandates.

Kenya Flexible Packaging Industry Leaders

-

Ramco Plexus Ltd.

-

Flexipac Limited

-

Polyflex Industries Limited

-

Silafrica Plastics & Packaging International Ltd

-

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sky Labels prepared to move into an enlarged Nairobi facility, boosting label capacity.

- April 2025: Mondi launched its 2024 Integrated and Sustainable Development reporting suite, outlining new renewable-packaging platforms.

- February 2025: Mondi expanded production of EcoWicketBags to meet rising demand in home and personal-care segments.

- February 2025: Skanem Interlabels Nairobi installed a Bobst Master M5 press to automate label production.

Kenya Flexible Packaging Market Report Scope

The report tracks the consumption value of flexible packaging products in Kenya. The study defines the revenue generated from the sales of packaging products such as bags and pouches, as well as films and wraps. The analysis is based on the market insights captured through secondary research and primaries. The study also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The flexible packaging market in Kenya is segmented by material (paper, plastic, and metal), product type (bags and pouches, films and wraps, and other product types), and end-user industry (food, beverage, healthcare and pharmaceutical, retail, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Material

| Paper |

| Plastic |

| Metal Foil |

| Bioplastics and Compostable Materials |

By Product Type

| Bags and Pouches |

| Films and Wraps |

| Sachets and Stick Packs |

| Labels and Sleeves |

By End-user Industry

| Food | Baked Goods |

| Snacks | |

| Meat, Poultry and Seafood | |

| Confectionery | |

| Pet Food | |

| Other Food Products | |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Agriculture and Horticulture | |

| Other End-User Industries |

By Printing Technology

| Flexography |

| Rotogravure |

| Digital Printing |

| Other Printing Technologies |

| By Material | Paper | |

| Plastic | ||

| Metal Foil | ||

| Bioplastics and Compostable Materials | ||

| By Product Type | Bags and Pouches | |

| Films and Wraps | ||

| Sachets and Stick Packs | ||

| Labels and Sleeves | ||

| By End-user Industry | Food | Baked Goods |

| Snacks | ||

| Meat, Poultry and Seafood | ||

| Confectionery | ||

| Pet Food | ||

| Other Food Products | ||

| Beverage | ||

| Healthcare and Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Agriculture and Horticulture | ||

| Other End-User Industries | ||

| By Printing Technology | Flexography | |

| Rotogravure | ||

| Digital Printing | ||

| Other Printing Technologies | ||

Key Questions Answered in the Report

What is the current value of the Kenya flexible packaging market?

The Kenya flexible packaging market size reached USD 2.24 billion in 2026 and is projected to grow to USD 2.52 billion by 2031.

Which material dominates flexible packaging in Kenya?

Conventional plastics hold a 67.85% market share, although bioplastics are the fastest-growing option.

Which product type is expanding the fastest in Kenya?

Sachets and stick packs are forecast to advance at a 4.44% CAGR as urban shoppers embrace portion-controlled formats.

How are EPR rules affecting Kenyan converters?

EPR regulations impose reporting and end-of-life fees, pushing converters toward mono-material, recyclable, and compostable films.

Where are new flexible-packaging factories locating in Kenya?

Besides Nairobi, investors favor Athi River, Naivasha’s Olkaria Green Energy Park, and emerging County Aggregation and Industrial Parks for energy and land-cost advantages.

What printing technology is gaining share?

Digital printing is growing at a 4.89% CAGR due to demand for short runs, personalization, and rapid turnaround.

Page last updated on: