Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 76.76 Billion |

| Market Size (2026) | USD 77.85 Billion |

| Market Size (2031) | USD 83.53 Billion |

| Growth Rate (2026 - 2031) | 1.42% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Office Real Estate Market Analysis by Mordor Intelligence

The Japan Office Real Estate Market size was valued at USD 76.76 billion in 2025 and estimated to grow from USD 77.85 billion in 2026 to reach USD 83.53 billion by 2031, at a CAGR of 1.42% during the forecast period (2026-2031). The Bank of Japan lifted its policy rate from negative territory to 0.25% and signaled that the corridor could widen to 1.0% by late-2025, a pivot that improves relative yields for domestic and offshore buyers. Central bank surveys forecast GDP expanding above potential as a modest pickup in global trade combines with a self-reinforcing rise in wages, consumption, and capital spending, particularly in automation and data infrastructure. The IMF’s latest Financial Sector Assessment notes sizeable exposures to equity and bond markets and flags pockets of stretched pricing in select real estate districts, although offices have held up through the pandemic. At the policy level, the administration’s “New Form of Capitalism” blueprint directs incentives toward semiconductors, cloud services, and related supply chains that depend on modern office capacity.

Key Report Takeaways

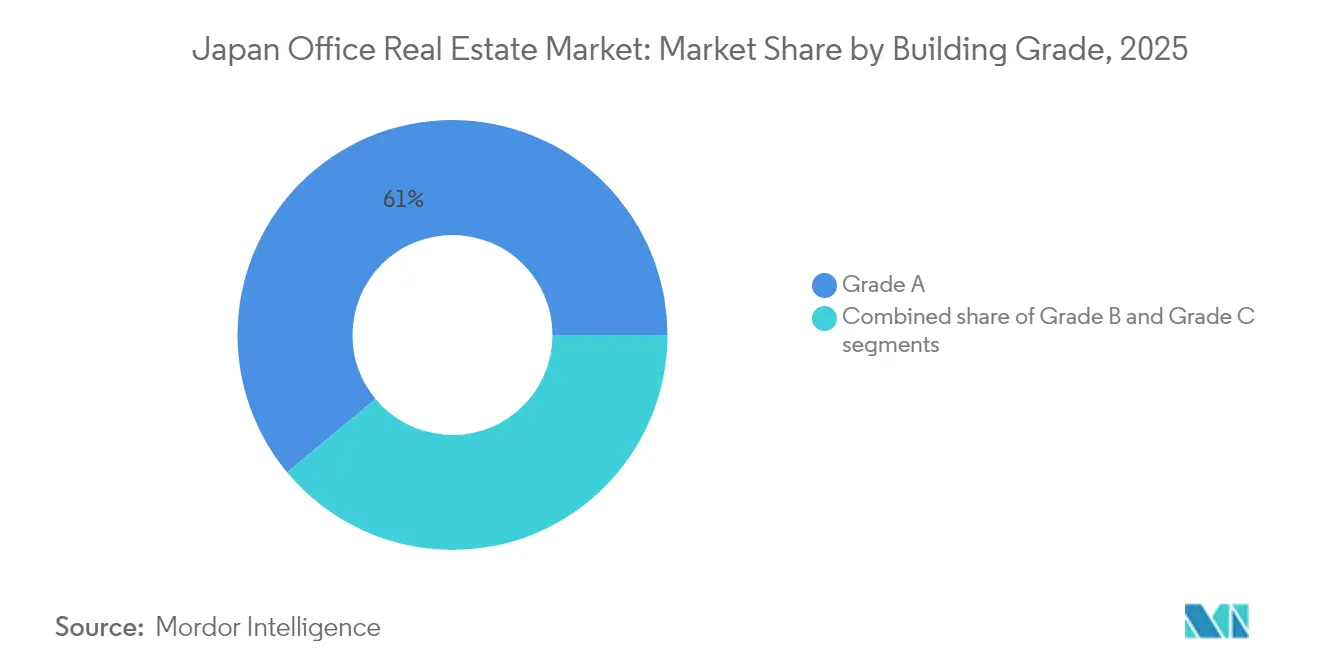

- By building grade, Grade A properties accounted for 61.03% of Japan's office real estate market share in 2025, while this premium cohort is forecast to expand at a 1.58% CAGR through 2031.

- By transaction type, Rental transactions contributed 70.72% to the Japan office real estate market size in 2025; the sales segment is projected to post the fastest growth at a 1.66% CAGR.

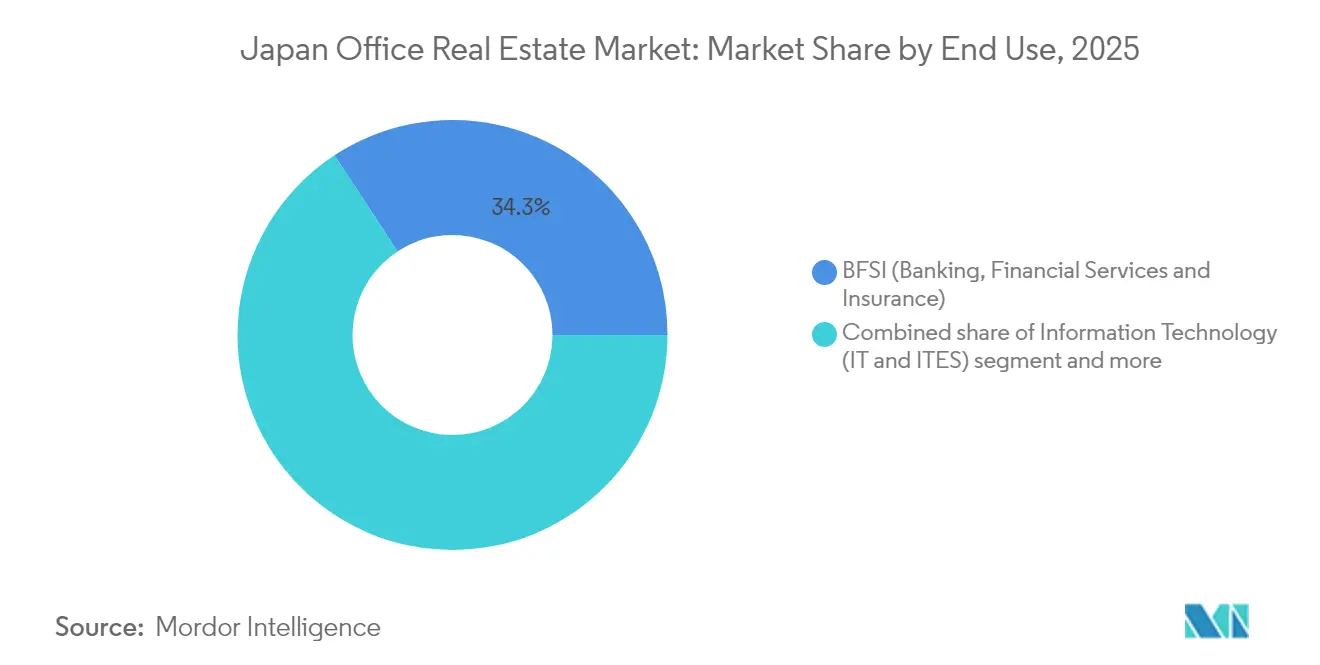

- By end use, the BFSI segment held 34.25% of Japan's office real estate market share in 2025, with Information Technology poised to post the highest growth at a 1.70% CAGR.

- By city, Tokyo captured 57.05% of the Japan office real estate market in 2025, whereas Osaka is expected to register the strongest CAGR at 1.76% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Office Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seismic-resilient & energy-efficient offices | +0.3% | Nationwide; Tokyo, Osaka, Nagoya | Medium term (2-4 years) |

| Government-led urban redevelopment | +0.2% | Tokyo, Osaka; spillover to Nagoya | Long term (≥4 years) |

| Wellness-oriented & tech-integrated space | +0.4% | Tokyo core, spreading to regional cities | Short term (≤2 years) |

| Professional services & IT expansion | +0.3% | Tokyo, Osaka; growing in Nagoya | Medium term (2-4 years) |

| Flexible & co-working network growth | +0.2% | Nationwide; suburban nodes | Short term (≤2 years) |

| Heightened foreign investor interest | +0.1% | Tokyo, Osaka; selective major cities | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Earthquake-Resilient and Energy-Efficient Office Buildings

Tenant and investor priorities in Japan are increasingly shaped by seismic safety and energy performance, elevating the appeal of next-generation office assets. Seismic retrofitting mandates compel owners to upgrade or replace older stock, channeling occupier demand toward recently built projects that already comply with stringent codes. Capital expenditure rises for owners of legacy towers, while developers of new structures gain pricing power through safer, greener designs that align with corporate ESG priorities. The dual necessity of quake resilience and sustainability accelerates tenant migration to Grade A assets, reinforcing the premium commanded by those buildings in the Japan office real estate market. Smart façades, efficient HVAC, and on-site renewables further bolster operating cost advantages that tenants increasingly quantify in lease negotiations. As a result, compliance-driven safety upgrades and ESG imperatives are converging to define the next era of demand in Japan’s office sector.

Government-Led Urban Redevelopment Projects Stimulating New Office Supply

National renewal programs now sit inside a wider digital-society agenda that asks planners to weave data, automation, and low-carbon design into every major district upgrade. Researchers describe Japan’s deregulated “flexible” zoning rules as weak by global standards, yet note that special districts allow planners to adjust height limits and land use to compete for talent and investment. New ministerial guidelines extend the legal service life of timber structures to at least 50 years, a change expected to unlock cheaper finance for low-carbon construction. Advisory panels urge schemes that protect local identity, arguing that copy-paste high-rise blocks erode livability and raise build costs as the population shrinks. Together, these measures keep the redevelopment pipeline active while steering designers toward climate goals and stronger community outcomes.[1]Cabinet Office of Japan, “Basic Policy on Economic and Fiscal Management and Reform 2024,”

Rising Tenant Preference for Wellness-Oriented and Tech-Integrated Office Environments

Health, sustainability, and digital infrastructure have become non-negotiables for tenants seeking to enhance employee experience and retention. More than 60% of occupiers have stabilized attendance policies and now refine space to improve experience and retention. Real-time air-quality monitoring, touchless entry, and sensor-driven climate systems increasingly appear on mandatory requirement lists as firms seek to boost productivity while demonstrating duty of care. Surveys reveal 43% of firms hitting peak utilization above 80%, suggesting that right-sized footprints are feasible when paired with data-led space management. Developers respond by embedding programmable lighting, biophilic terraces, and on-site fitness to secure green certifications such as CASBEE and LEED, which in turn support rental premiums. For the Japan office real estate market, the convergence of wellness and technology is no longer a differentiator but a prerequisite for top-tier assets. This evolution reinforces the premium placed on smart, human-centric environments that align with the future of work.

Growth in Professional Services and IT Sectors Driving Demand

Japan’s push to digitize public and private workflows is lifting office demand from technology vendors, consultants, and allied service firms. Cabinet Office analysis positions artificial intelligence as a broad platform that raises productivity and triggers fresh job creation, requiring large-scale reskilling programs that translate into new tenant requirements for training space. Bank of Japan industry studies confirm that machinery, construction, and other investment-heavy sectors carry an outsized share of GDP momentum, reinforcing the need for central locations that support complex supply chains. Meanwhile, the government’s action plan to double inward foreign direct investment to USD 530 billion by 2030 includes tax and visa reforms aimed at building Asia’s largest start-up hub in Tokyo. Against a backdrop of fourteen straight years of national population decline, Tokyo retains 11.5% of residents and posts the fastest growth rate, concentrating talent and workspace demand in the capital.[2]Bank of Japan, “Japan’s Economy and Monetary Policy,”

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent remote work adoption | -0.2% | Nationwide; strongest in Tokyo CBD | Medium term (2-4 years) |

| Oversupply risk for Grade B/C stock | -0.1% | Secondary areas in Tokyo & Osaka | Short term (≤2 years) |

| High seismic retrofitting costs for aging buildings | -0.2% | Older assets across all major cities | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Persistent Remote Work Adoption Reducing Large Occupier Space Requirements

Flexible work models are driving long-term shifts in occupier strategy, curbing demand for large, traditional office footprints. Hybrid work has matured into a permanent structure, compelling large corporates to trim excess capacity and pursue distributed footprints that blend headquarters, satellite hubs, and on-demand space. Demand decouples from Gross Leasable Area and shifts toward fit-out quality, pushing rental growth into prime towers while sub-prime vacancy swells. Consequently, Grade A landlords remain insulated but lower-tier owners face asset repositioning costs in the Japan office real estate market. Even so, most occupiers retain a central flagship to safeguard culture and client access, tempering the drag on sector-wide absorption. While the flagship office remains relevant, decentralization continues to challenge the scale and utilization patterns of Japan’s office market.

Oversupply Concerns in Tokyo and Osaka Submarkets

Localized development peaks and aging stock are amplifying vacancy risk in key Japanese submarkets. While headline supply is moderating, completion peaks within five Tokyo wards create local pressure, especially for older mid-rise buildings that cannot match new amenity packages. Osaka’s surge in investment masks pockets of softness where secondary corridors host legacy towers ill-suited to current demand. Owners weigh capital-intensive retrofits against potential demolition in a land-scarce environment, and disposal activities by domestic REITs accelerated in 2024 to preempt value erosion. Vacancy risk therefore concentrates in specific blocks rather than the broader Japan office real estate market. Unless legacy assets are repositioned effectively, these pockets of oversupply may continue to weigh on rent growth and capital values.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Building Grade: Premium Assets Drive Market Evolution

Grade A space commanded 61.03% of Japan's office real estate market share in 2025, underlining tenant flight to quality that underpins a projected 1.58% CAGR for this cohort through 2031. Record net absorption of 105,000 tsubo in Tokyo in Q1 2025 validates continued appetite for high-spec, ESG-compliant towers despite subdued macro growth. Rising construction outlays and limited CBD land ensure new deliveries arrive in smaller annual tranches, sustaining pricing power for existing Grade A owners within the Japan office real estate market.

Faced with escalating retrofit obligations, Grade B landlords explore shell-and-core upgrades or conversion to alternative uses when economic. Grade C assets often cannot bridge the cost-value gap, encouraging site aggregation by deep-capital developers who can justify demolition and rebuild. Smart-building systems, carbon-neutral materials, and WELL certification now define the minimum standard for maintaining Class A status. Companies such as Japan Real Estate Investment Corporation have already secured green labels on 76.4% of their office portfolio, capturing rent premiums that ripple through the Japan office real estate market.

By Transaction Type: Rental Dominance Reflects Market Maturity

Rental deals represented 70.72% of the Japan office real estate market size in 2025, confirming that corporates still value balance-sheet flexibility over asset ownership. Lease structures remain multi-year with stepped escalation clauses, offering stable cash flows that underpin REIT dividend strategies. Meanwhile, the smaller sales segment is forecast to deliver a 1.66% CAGR to 2031, buoyed by overseas investors hunting yield and domestic institutions rotating assets.

Listed REITs unloaded USD 5.1 billion of office holdings in 2024, monetizing capital gains for share buybacks that enhance total return metrics. High-profile trades such as overseas sovereign wealth funds capturing Marunouchi trophy assets demonstrate that liquidity persists for prime stock. Consequently, rental stability acts as ballast while transaction velocity allows active players to recycle capital, reinforcing depth in the Japan office real estate market.

By End Use: Technology Sector Emergence Reshapes Demand

The BFSI (Banking, Financial Services, and Insurance) community retained 34.25% of the Japan office real estate market share in 2025 through entrenched headquarters and regulatory needs for secure environments. Yet, Information Technology is set to chart a 1.70% CAGR through 2031 as start-ups scale and global platforms grow, in Japanese engineering hubs. This expansion stimulates demand for modular floorplates and advanced connectivity, making IT a structural driver of the Japan office real estate market.

Professional services maintain a steady roster of requirements while leveraging flexible clauses to manage project cycles. Fintech and proptech cross-pollination blurs sector lines; for instance, Mitsubishi Estate’s flex-office arm saw robust revenue of USD 2.3 billion thanks to enterprise subscriptions. The diversification of occupier mix thus reduces over-reliance on any single industry and broadens resilience across the Japan office real estate market.

Geography Analysis

Tokyo retained 57.05% of its national share in 2025 and sustained six consecutive quarters of rent growth as Grade A vacancy fell to 3.6%. Flagship redevelopments such as Tokyo TORCH refresh the skyline while enhancing multimodal connectivity, reinforcing the capital’s magnetism for multinational headquarters and global investors operating within the Japan office real estate market. Rising construction costs temper speculative supply, which in turn maintains upward rent pressure in core districts. Investor activity, topping USD 34 billion in 2024, further amplifies Tokyo’s liquidity and cements its status as the premier gateway city.

Osaka’s share sits below Tokyo’s, but records as World Expo preparations accelerate infrastructure and place-making projects. Office absorption outpaced new completions in 2024, driving Grade A vacancy down to 2.6% and validating capital inflows from cross-border buyers attracted to comparatively wider yields. The USD 4 billion Umekita scheme will add mixed-use inventory that integrates life-science, hospitality, and workspace, anchoring long-term competitiveness in the Japan office real estate market. Local stakeholders leverage the Expo platform to brand Osaka as a global innovation hub, differentiating it from Tokyo’s corporate pedigree.

Nagoya delivers mid-single-digit rental gains as automotive and aerospace majors lock in footprints near supplier ecosystems. Grade A vacancy fell to 2.3% in Q1 2025, the tightest in four years, reflecting deep-seated industrial demand. Beyond the three megacities, regional centers vary: Fukuoka benefits from IT offshoring; Sapporo leverages tourism; and Sendai undertakes downtown renewal. Government incentives support decentralization, yet demographic headwinds require cities to cultivate niche specializations to sustain office absorption across the Japan office real estate market.

Competitive Landscape

The Japan office real estate market is highly concentrated. Large developers still dominate, yet the central bank’s Financial System Report cautions that elevated pricing in a few districts and rising vacancy in older towers warrant close monitoring. Field studies show that one quarter of central Tokyo’s stock already offers modern amenities and commands rents about 6.5% above market, although vacancy in this cohort inched up by 1.7 points as new deliveries hit the market. Tenant surveys confirm that indoor environmental quality explains half of the variation in user satisfaction, underscoring why owners continue to invest in air, light, and acoustic upgrades. High concentration allows these players to dictate design standards while absorbing compliance costs that deter smaller rivals within the Japan office real estate market.

Strategically, developers favor block redevelopment over single-site builds, allowing integration of office, retail, and hospitality that maximizes land value. Technology adoption—smart air-handling, AI-based energy dashboards, and tenant apps—creates service stickiness, and firms like Mitsubishi Estate dedicate dedicated venture arms to proptech incubation, aligning buildings with digital tenant requirements. REITs add a fluid capital market dimension; for example, record sales of USD 5.1 billion in 2024 freed liquidity for dividend boosts and unit buybacks, intensifying total-return competition.

Foreign finance reshapes bidding dynamics, as North American pension funds and Middle Eastern sovereign vehicles broaden mandate scopes to include Osaka, Nagoya, and even regional cities. Joint ventures give domestic groups access to cheaper capital, while overseas partners leverage local origination acumen. Emerging disruptors, notably flexible-workspace brands, partner with landlords to back-fill partial vacancies and power communal amenity floors, adding diversity to the Japan office real estate market’s competitive tapestry.

Japan Office Real Estate Industry Leaders

Mitsui Fudosan Co., Ltd.

Mitsubishi Estate Co., Ltd.

Sumitomo Realty & Development Co., Ltd.

Tokyu Land Corporation

Nomura Real Estate Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Government published standards that let wooden commercial buildings qualify for 50-year service lives, double the former limit, paving the way for cheaper finance and lower-carbon construction.

- March 2025: Official land-price survey showed the fourth straight annual increase, with Tokyo commercial plots up 8.2% and Osaka up 6.7%

- February 2025: Japanese REITs sold USD 5.1 billion of offices in 2024, a record disposal volume used mainly for share repurchases.

- January 2025: Bank of Japan projected growth above potential and a consumer inflation rate of 2.5-3.0% for FY 2024, citing strong capex tied to digitalization and labor shortages

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study sizes the Japan office real estate market as the aggregate capital value of income-producing office buildings, Grade A, B, and C, located in Tokyo, Osaka, Nagoya, and other prefectural cities, along with business parks and mixed-use projects where office space exceeds sixty percent of gross floor area. We convert all yen-denominated evidence to constant 2024 US dollars before modeling.

Scope exclusion: serviced-apartment floors, stand-alone co-working outlets inside retail malls, and corporate campuses used strictly for owner-occupation are not counted.

Segmentation Overview

- By Building Grade

- Grade A

- Grade B

- Grade C

- By Transaction Type

- Rental

- Sales

- By End Use

- Information Technology (IT & ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Services

- Other Services (Retail, Lifesciences, Energy, Legal)

- By City

- Tokyo

- Osaka

- Nagoya

- Rest of Japan

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed leasing directors at domestic developers, foreign capital allocators active in Tokyo, occupier representatives in IT, BFSI, and professional services, and regional brokers in Osaka and Nagoya. The conversations tested vacancy inflection points, achievable rents, cap-rate expectations, and pipeline schedules, letting us refine yield and absorption assumptions surfaced in secondary research.

Desk Research

We started with land price surveys, building completions, and approved floor-area data issued by the Ministry of Land, Infrastructure, Transport and Tourism, the Statistics Bureau's Annual Report on Housing and Land, and quarterly vacancy series from Miki Shoji and CBRE. Trade associations such as the Association for Real Estate Securitization, public J-REIT filings, and Real Capital Analytics transaction logs supplied pricing benchmarks and deal flow. Our team also checked macro indicators from the Bank of Japan, labor force data, and prefecture GDP to frame demand pools. Premium insights from Dow Jones Factiva and D&B Hoovers helped trace headline corporate moves that shift large blocks of office demand. This list is illustrative; many other public and subscription sources informed the desk work.

Market-Sizing & Forecasting

We apply a top-down stock-and-flow construct, beginning with national office inventory in square meters, pairing it with average achieved prices from recorded transactions to derive annual market value. Results are cross-checked with a selective bottom-up roll-up of landmark asset sales and sampled asking-rent multiplied by occupied-area calculations. Key variables that steer the model include Grade A and B vacancy, net absorption in tsubo, median transaction cap rate, construction cost inflation, and yen-dollar exchange shifts; forecast paths for each were stress-tested through multivariate regression before scenario filters translated them into the 2025-2030 outlook.

Data Validation & Update Cycle

Outputs face a three-layer review: automated variance scans against historic series, peer comparison inside the real-estate analyst pod, and management sign-off. We refresh every twelve months, re-opening the model sooner when seismic policy changes, major portfolio trades, or macro shocks breach preset triggers.

Why Mordor's Japan Office Real Estate Baseline Commands Reliability

Published figures often differ because firms pick unique asset scopes, price bases, and refresh timetables. By anchoring on full building asset value and harmonizing yen data into real US dollars, we provide a consistent yardstick that decision-makers can retrace.

Key gap drivers include: some studies cap their scope at rental revenue, a few exclude Grade C stock or secondary cities, while others inflate totals by folding in owner-occupied premises. Exchange-rate assumptions and one-off bulk-sale adjustments further widen the spread.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 76.76 B (2025) | Mordor Intelligence | - |

| USD 77 B (2024) | Regional Consultancy A | Uses nominal yen, omits currency normalization, limited forecast back-testing |

| USD 21.6 B (2024) | Trade Journal B | Counts rental revenue only, excludes provincial stock and strata-titled floors |

| USD 20.7 B (2024) | Industry Tracker C | Focuses on Class A and B in five central wards, ignores capital transactions below JPY 5 B |

In short, Mordor's disciplined scope selection, transparent variable set, and annual model upkeep yield a balanced baseline that clients and regulators alike can audit and replicate with confidence.

Key Questions Answered in the Report

How big is Japan’s office property sector in 2026?

The Japan office real estate market stands at USD 77.85 billion in 2026 and is forecast to reach USD 83.53 billion by 2031.

Which city leads national office demand today?

Tokyo holds 57.05% of Japan office real estate market share, supported by deep corporate clusters and repeated record inflows of foreign capital.

What segment commands the largest occupier share?

Financial services accounts for 34.25% of occupied space, though Information Technology is the fastest-growing end user with a 1.70% CAGR outlook.

Why are Grade A towers outperforming other buildings?

Stricter seismic codes, ESG targets, and wellness requirements channel occupier demand and investment into new or recently refurbished Grade A assets.

How is hybrid work changing investment strategy?

Corporations reduce total floor area but pay premiums for tech-enabled, flexible layouts, while investors place larger bets on core assets offering resiliency in the Japan office real estate market.

What role does foreign capital play in current pricing?

Overseas investors—lured by stable yields and a comparatively weak yen—drove a 68% YoY jump in Q4 2024 transactions, especially in Tokyo and Osaka.

Page last updated on: