Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

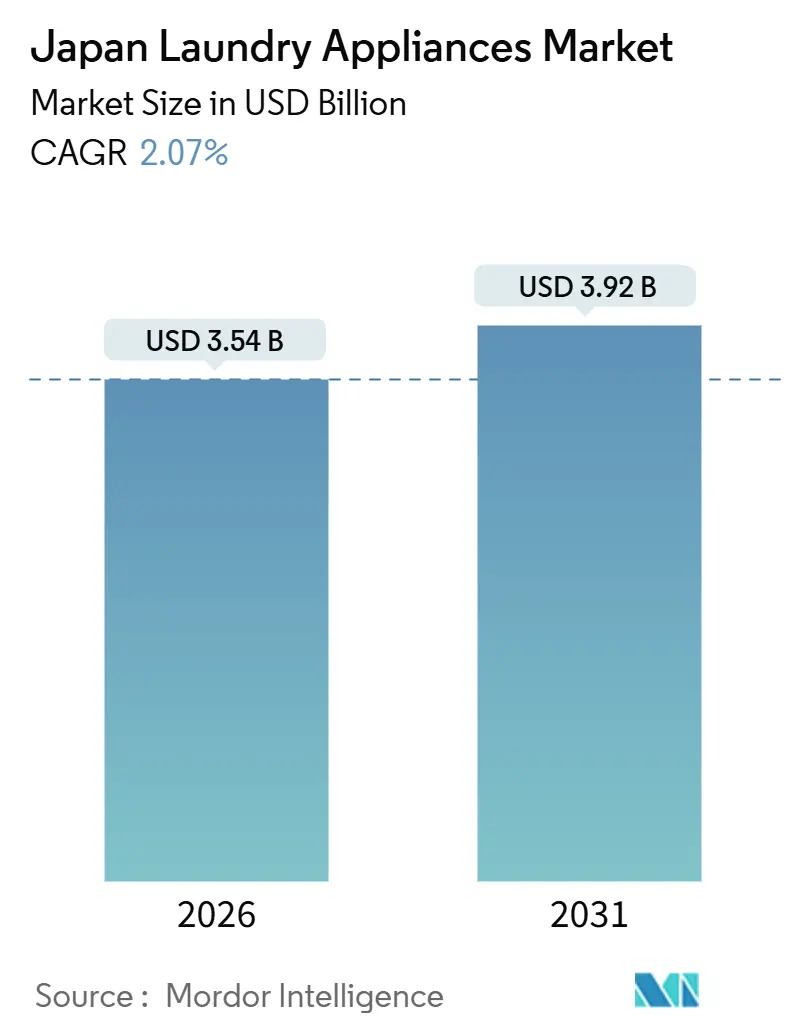

| Market Size (2026) | USD 3.54 Billion |

| Market Size (2031) | USD 3.92 Billion |

| Growth Rate (2026 - 2031) | 2.07% CAGR |

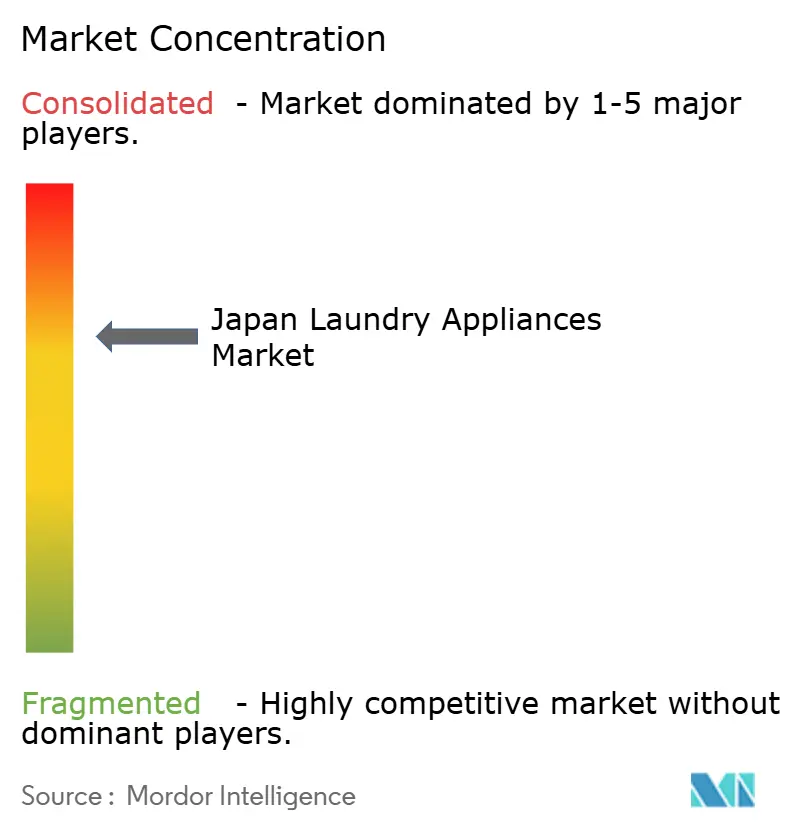

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Laundry Appliances Market Analysis by Mordor Intelligence

The Japan laundry appliances market size reached USD 3.54 billion in 2026 and is forecast to reach USD 3.92 billion by 2031, reflecting a CAGR of 2.07%. The Japan laundry appliances market is growing mainly due to consistent replacement demand in a highly saturated market. Nearly all households already own appliances, so consumers upgrade to newer models rather than adding units. Strict energy-efficiency regulations push manufacturers to innovate and encourage households to purchase more efficient appliances. Government incentive programs for eco-friendly models further stimulate purchases, particularly in dense urban areas. The increase in single-person households drives demand for compact, versatile machines that save space and fit smaller living environments. An aging population creates interest in user-friendly features such as voice control, automated alerts, and ergonomic designs. Technological innovations, including heat-pump dryers and smart diagnostics, enhance performance and appeal to consumers. Multi-brand retail stores and expanding online channels make it easier for buyers to access new products and compare features. Competitive pressure encourages brands to continually refresh product lines, adding more options and advanced functionalities.

Key Report Takeaways

- By product type, washing machines led with 70.83% of the Japan laundry appliances market share in 2025, while clothes dryers are the fastest-growing category with a projected 2.91% CAGR through 2031.

- By technology, fully automatic models accounted for 81.93% of the Japan laundry appliances market share in 2025 and hold the highest growth outlook at a 2.13% CAGR.

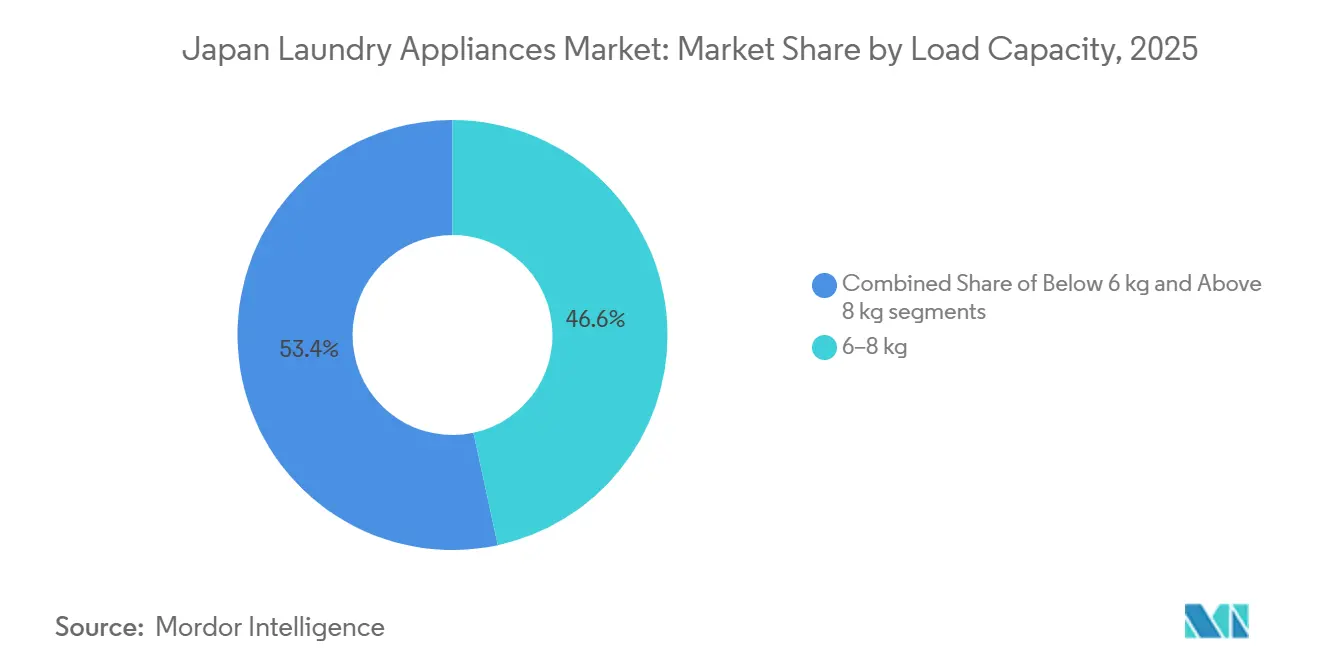

- By load capacity, the 6–8 kg segment represented 46.63% of the Japan laundry appliances market share in 2025, while the above-8-kg tier is the fastest-growing at a 2.84% CAGR.

- By distribution channel, multi-brand stores captured 58.12% of the Japan laundry appliances market share in 2025, whereas online retail is the fastest-growing route at a 3.12% CAGR.

- By geography, Kanto held 35.71% of the Japan laundry appliances market share in 2025, and Kansai is the fastest-growing region with a 2.43% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Laundry Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of energy-efficient appliances under Top Runner standards | +0.6% | Global, with early gains in Kanto, Kansai, and Chubu | Medium term (2–4 years) |

| Growing single-person households are driving compact washer-dryer demand | +0.5% | National, concentrated in Tokyo, Osaka, and Yokohama urban cores | Long term (≥ 4 years) |

| Government eco-point subsidies are accelerating replacement sales | +0.4% | National, early implementation in Tokyo, Mie, Fukui, Toyama | Short term (≤ 2 years) |

| Subscription-based appliance rentals are increasing replacement cycles | +0.3% | Kanto, Kansai urban areas, spillover to Chubu | Medium term (2–4 years) |

| Antimicrobial drum coatings appealing to hygiene-conscious consumers | +0.2% | National, higher penetration in aging-population prefectures | Medium term (2–4 years) |

| Rising demand for smart, IoT-connected washers with predictive maintenance | +0.2% | Kanto core, spreading to Kansai, Chubu metropolitan regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Energy-Efficient Appliances Under Top Runner Standards

The Top Runner Program sets performance benchmarks that manufacturers must reach within defined timelines, which results in continuous redesign of motors, heat exchangers, and control systems to stay compliant. In 2024, METI refined energy-efficiency targets for washing machines and dryers, reinforcing an upgrade cycle that favors newer, more power-thrifty models. Heat-pump-based configurations, as seen in Hitachi’s 2024 front-load portfolio, reduce electricity consumption by significant double-digit percentages compared with older heater-based units and eliminate water use during the drying phase[1]Hitachi, “Smart Life & Ecofriendly Systems,” Hitachi Review, hitachihyoron.com. Retail programs and in-store merchandising actively highlight compliant models, which influences shopper choices within multi-brand showrooms where side-by-side comparisons are common. Local rebate schemes such as Tokyo’s Zero Emission Point have added momentum by lowering out-of-pocket costs for households replacing pre-Top Runner era units, which brings forward planned purchases in dense urban clusters.

Growing Single-Person Households Driving Compact Washer-Dryer Demand

Single-person households now account for a large share of Japan’s households, representing about one-third of all households and making them the largest household type in the country. This demographic shift reflects broader trends, including fewer families with children and a continuing decline in average household size, which supports demand for compact footprints, integrated drying, and feature sets tuned to small loads[2]Nippon.com, One in Three Japanese Households Consists of Just One Person, nippon.com. Design preferences concentrate around narrow-width machines that fit standard apartment alcoves, with capacity and cycle options aligned to fewer garments and quick turnarounds after work or school. Product roadmaps from leading brands have focused on slimmer enclosures and intelligent wash-dry programs that shorten cycle times without sacrificing care for delicates. New models in 2025 and 2026 embed connected controls and tailored presets that match the daily routines of solo residents, strengthening the appeal of compact washer-dryer combos in metropolitan housing. The growing prevalence of individuals living alone, particularly in Tokyo and Osaka cores, increases demand for appliances that maximize space efficiency and convenience.

Government Eco-Point Subsidies Accelerating Replacement Sales

Local eco-point programs have broadened the pool of buyers eligible for rebates when scrapping older appliances and purchasing units that exceed efficiency thresholds. The Tokyo Metropolitan Government has expanded its “Tokyo Zero Emission Points” program to accelerate the replacement of old home appliances with high-efficiency models. The initiative offers points redeemable as direct discounts at purchase for products such as air conditioners, refrigerators, water heaters, and laundry machines, with higher support provided for older appliances. Subsidies can reach up to Yen 80,000 (USD 508), encouraging households to replace long-used units with energy-efficient ones. Tokyo’s program processed tens of thousands of applications within its first two quarters, and prefectural programs have followed, translating into immediate unit uplift in participating municipalities[3]Tokyo Metropolitan Government, Tokyo Zero Emission Points Program, Press Release, Mar 28, 2024. These incentives lower payback periods when households consider energy savings over several years, which increases conversion to premium efficiency tiers in showrooms. Retailers have embedded eligibility checks into their sales processes so that buyers can confirm benefits before installation bookings, making decisions more straightforward.

Rising Demand for Smart, IoT-Connected Washers with Predictive Maintenance

Connected platforms now underpin brand ecosystems that extend from onboarding and remote monitoring to predictive maintenance and auto-scheduling of service work. Panasonic’s AI roadmap centers on hardware-software integration that enables voice-guided troubleshooting and dynamic course selection, which aligns with user expectations formed by smart-home devices. Hitachi’s connected app consolidates cycle monitoring and maintenance alerts across its product lines, which reduces friction during daily use. Sharp’s generative-AI service personalizes course recommendations and downloads programs over Wi-Fi, which accelerates digital adoption in laundry routines[4]Sharp Corporation, “FY2024 Financial Summary and Medium-term Plan,” Sharp Corporation, finance-frontend-pc-dist.west.edge.storage-yahoo.jp. These features resonate with aging households that prioritize fewer surprises and easy-to-understand prompts, supporting higher attachment rates for connected units in large metro regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturated household penetration limits unit growth | -0.4% | National, particularly rural Tohoku, Hokkaido, and Shikoku | Long term (≥ 4 years) |

| Price sensitivity amid stagnant real wages | -0.3% | National, acute in non-metropolitan prefectures | Medium term (2–4 years) |

| Aging condominium plumbing limits large-capacity installations | -0.2% | Metropolitan cores, legacy housing stock from the 1970s–1990s | Long term (≥ 4 years) |

| Limited consumer awareness of energy-efficient upgrades | -0.2% | National, especially in smaller cities and rural areas | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Saturated Household Penetration Limits Unit Growth

Ownership levels across income brackets leave little room for incremental unit additions, which emphasizes replacement timing and feature-led upgrades. Replacement intervals lengthen when consumers focus on durability and serviceability, which moderates annual unit volumes even during promotional periods. Rural areas with older populations extend usage further, which softens the regional contribution to national growth. Manufacturers adapt by improving energy performance and connectivity while keeping form factors familiar, which encourages upgrades without forcing changes to installation footprints. The Japan laundry appliances market, therefore, grows through specification improvements and targeted promotions rather than large swings in installed base.

Aging Condominium Plumbing Limits Large-Capacity Installations

Legacy plumbing and drainage in condominiums built several decades ago limit the ability to install large and heavy units without targeted retrofits. Older water lines, smaller drains, and limited floor reinforcement can deter buyers from stepping up to jumbo capacities even when family needs change. Municipal code updates for new buildings improve compatibility with washer-dryer combos, but these do not address the existing housing stock. Some buyers in older buildings continue to prefer machines that match standard alcove dimensions, which narrows feasible capacity choices. Building code updates in Tokyo since 2024 support forward compatibility in new developments, which creates a gradual, long-horizon path to easing this constraint in the Japan laundry appliances market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fleets and Hygiene Propel Washer Tiers

Washing machines accounted for 70.83% of revenue in 2025, which reflects the depth of the installed base and recurring replacement behavior in the Japan laundry appliances market. Clothes dryers hold a smaller base but show the fastest growth at a 2.91% CAGR as heat-pump technology cuts electricity consumption and as drying becomes a priority in humid months. The washing machine category continues to add capacity options and cleaning features that improve fabric care while reducing water use. Heat-pump dryers increasingly appeal to households that need gentle cycles at lower temperatures, which helps maintain textile quality. Taken together, these shifts reinforce a transition toward integrated combos and more efficient standalone formats across households in dense urban regions.

Feature differentiation continues to focus on hygiene, energy performance, and usability that fits small spaces common in metro apartments. Brands are investing in antimicrobial cycles, auto-clean routines, and drum designs that reduce residue, which appeals to households with infants or elderly members. Vendor roadmaps show continued improvements in cleaning algorithms, fabric sensors, and convenience functions that reduce maintenance. As model updates roll out, certified efficiency remains prominent in retailer displays and online descriptions. These product-level changes sustain incremental pricing power at the premium end while meeting the everyday needs of the Japan laundry appliances market.

By Technology: Automation Gains but Manual Segments Persist in Rural Zones

Fully automatic machines held 81.93% of sales in 2025 and are projected to expand at a 2.13% CAGR through 2031, making this the largest and fastest-growing technology tier in the Japan laundry appliances market. Growth in this segment is driven by convenience features, load sensing, and connected apps that simplify daily routines. Newer ranges add predictive maintenance alerts and guided troubleshooting, which reduce unexpected service calls. Rural segments continue to purchase simpler machines where electrical capacity or ease of repair remains a deciding factor. The technology mix, therefore, reflects both high-tech adoption in metros and enduring preference for straightforward controls in select rural prefectures.

Semi-automatic and manual formats remain in use where households value mechanical simplicity and budget pricing, which helps maintain a modest share for these models. Manufacturers sustain limited portfolios that target this need while prioritizing R&D around fully automatic ranges. Efficiency rules under the Top Runner guide motor choices and energy performance in new models, which pushes inverter designs into mainstream lines. Voice support and smart-home integration are rising in metropolitan sales, where buyers value remote control and monitoring in multi-device ecosystems. Over time, automation and connectivity anchor the premium and mid-tier, while basic functionality continues to serve select regional niches in the Japan laundry appliances industry.

By Load Capacity: Mid-Tier Dominates but Jumbo Washers Gain Among Aging, DINKS Segments

The 6–8 kg capacity tier represented 46.63% of sales in 2025, aligning with common household sizes and the available space in many urban apartments. This mid-tier balances energy use, drum volume, and ease of loading, which explains its broad appeal across life stages. Brands emphasize refined wash programs and sensors that optimize cycles without user input. The Japan laundry appliances market continues to standardize around this capacity band as a practical default for two-to-three-person households. Within this bracket, models with intelligent dosing and cycle optimization maintain strong sell-through, where showroom staff can demonstrate benefits.

Above-8-kg machines are the fastest risers with a 2.84% CAGR, which reflects time-saving batch habits among dual-income couples and multi-generational families. New-home building standards adopted since 2024 in large metros improve drainage and support for heavier units, which eases some historical constraints on jumbo installations. Vendors market jumbo drums with messaging around weekly loads, bedding, and sportswear, which aligns with busy schedules. At the same time, compact combos continue to serve small apartments that favor space savings over maximum capacity. This spectrum of choices supports a wide range of use cases in the Japan laundry appliances market.

By Distribution Channel: Multi-Brand Showrooms Hold Ground as E-Commerce Surges

Multi-brand stores held 58.12% of sales in 2025, which shows the continued weight of consultative showrooms and installation support. Sales associates guide shoppers through side-by-side comparisons and coordinate delivery and take-back, which reduces friction for replacements. Retailers integrate eligibility checks for local rebates into the purchase process, which increases confidence at checkout. In parallel, online channels are the fastest-growing route with a projected 3.12% CAGR as shoppers blend research and purchase across web and store. The result is a stable core of in-person sales with rising digital volumes for the Japan laundry appliances market.

Omnichannel behaviors include browsing online, inspecting units in-store, and opting for store pickup for convenience and quick installation. Government analysis shows Japanese shoppers engage heavily with retailer-mediated online-to-offline flows, which keeps showrooms central to big-ticket appliance purchases. The Home Appliance Recycling Law defines take-back obligations and fees for disposal, which retailers handle during delivery. This logistics backbone supports both showroom and e-commerce growth and underpins high satisfaction scores for organized installation. These operating norms reinforce trust and repeat purchase patterns in the Japan laundry appliances market.

Geography Analysis

Kanto led with 35.71% of revenue in 2025, supported by dense housing starts, premium product mixes, and strong adoption of connected features. Local incentives, such as Tokyo’s Zero Emission Point, amplified energy-efficient upgrades and pulled forward replacement cycles. Kansai is the fastest-growing region at a 2.43% CAGR as manufacturing clusters, tourism-related housing conversions, and brand loyalty to domestic names sustain demand. These dynamics combine to anchor a large share of the Japan laundry appliances market in the country’s two largest metropolitan corridors. Brands allocate product launches and marketing budgets accordingly to match the scale and pace of demand in these regions.

Chubu provides a stable contribution built on industrial employment and steady household formation that supports recurring replacements. Product mixes skew toward mid-tier specifications with a focus on efficiency and durability for day-to-day use. Local R&D and production capabilities among leading manufacturers strengthen responsiveness to climate and housing conditions in the region. This includes dryer variants tuned for humid summers and operational reliability for small-space laundry areas. The combination of manufacturing ecosystem depth and pragmatic consumer preferences supports consistent, mid-cycle upgrades in the Japan laundry appliances market.

The rest of Japan aggregates diverse conditions that range from cold-climate adaptations in Hokkaido to solar-enabled households in parts of Kyushu and Okinawa. Kyushu and Okinawa post the fastest sub-regional growth trajectory at a 4.31% CAGR as infrastructure upgrades and new residential installations favor efficient appliances. Cold prefectures maintain steady demand for machines with enhanced freeze protection and temperature control in unheated laundry spaces. Aging populations in several regions prioritize simple controls, clear displays, and audible prompts that assist daily use. These varied demands encourage localized assortments and regional product configurations across the Japan laundry appliances market.

Regulatory Landscape

Japan laundry appliances are regulated primarily under METI oversight through the Act on the Rational Use of Energy (Top Runner Program), the Electrical Appliances and Materials Safety Act (PSE Law), and the Act on Recycling of Specified Kinds of Home Appliances (Home Appliance Recycling Law). In 2024, METI refined energy-efficiency targets for washing machines and dryers under the Top Runner framework, which reinforced redesign cycles around motors, controls, and drying systems to meet the updated benchmarks.

For safety and end-of-life compliance, the PSE Law requires conformance to technical standards and prescribed conformity processes for electrical appliances, with safety expectations supported by standards such as JIS C 9335-2-7 for washing machines. The Home Appliance Recycling Law sets take-back and recycling responsibilities across consumers, retailers, and manufacturers, shaping reverse-logistics planning and retail installation workflows alongside disposal fee collection at replacement time. Consumer-safety oversight is also supported by the Consumer Affairs Agency (CFA), including child-safety considerations for drum-type designs.

Value Chain Analysis

The Japan laundry appliances value chain starts with component inputs (motors, control boards, sensors, drums, pumps, and, for dryers, heat-exchanger and heat-pump related sub-systems), followed by assembly by OEMs and brand owners that incorporate localized engineering for Japanese housing constraints and energy rules. Compliance steps under the Electrical Appliances and Materials Safety Act (PSE Law), including required procedures for manufacturers and importers, sit between production and commercialization, adding testing and documentation into the go-to-market path.

Distribution relies on multi-brand appliance retailers, brand stores, and fast-growing online channels, with delivery, installation, and haul-away services serving as the key last-mile nodes for replacements. After-sales service and maintenance are supported by manufacturer networks and specialist ecosystems (including technician training bodies such as the Japan Washer Repair Association). End-of-life collection and processing are institutionalized through the Home Appliance Recycling Law, creating a closed-loop channel that feeds recovered materials back into industry supply chains, while trade bodies such as AEHA and JEMA help coordinate industry practices across home appliance manufacturers and related stakeholders.

Competitive Landscape

The competitive landscape of the Japan laundry appliances market is highly consolidated, with a few major brands capturing most of the revenue. Leading manufacturers benefit from structural advantages created by energy-efficiency regulations and recycling requirements, which favor companies with proprietary motor designs, heat-pump expertise, and nationwide service networks. Vendors are increasingly integrating hardware with software and cloud-based services to manage registrations, diagnostics, and maintenance. These capabilities strengthen partnerships with multi-brand retailers and support premium positioning for connected, high-efficiency models. As a result, incumbents maintain strong control over core residential sales while shaping the expectations for product depth and service integration.

Opportunities for growth exist in emerging formats and alternative access models, including subscription-based services and compact commercial units located near transit hubs. Appliance rental programs have grown in popularity, rotating inventory more frequently and feeding refurbished units into secondary channels. Micro-laundromats in major cities cater to commuters and single-person households, offering quick-turn services that complement residential demand. Certain brands lead in commercial coin-operated units by combining localized R&D with tailored product offerings for business operators. These niche segments provide avenues for innovation even as mainstream residential sales remain dominated by established brands.

Manufacturers are also focusing on software and AI strategies to add value beyond the physical appliance. Some companies are integrating AI to offer predictive maintenance, voice-guided troubleshooting, and service-driven revenue opportunities. Others are refining unified apps that provide analytics, cycle recommendations, and maintenance support across connected appliances. Newer entrants experiment with camera-assisted and AI-driven cycle selection to simplify fabric care for cost-conscious consumers. This diversity of product and service strategies highlights the variety of competitive approaches shaping the Japan laundry appliances market.

Japan Laundry Appliances Industry Leaders

Panasonic Corporation

Hitachi Global Life Solutions

Toshiba Lifestyle Products & Services

Sharp Corporation

Haier Japan (AQUA)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product and service differentiation is creating premiumization opportunities around usability, compactness, and connected support in a replacement-led market. In April 2026, Toshiba Lifestyle launched new washing machines that emphasize a low and wide inlet design to improve loading and unloading, aligning product design with aging households and smaller laundry spaces. At the same time, compact drum-type washer-dryer launches (for example, Haier Japan Sales introducing DeLAITO series models in January 2026) indicate active competition around space-saving formats and higher-value drying features.

A second opportunity area is tighter integration between retail touchpoints, service operations, and product development, where feedback loops can translate into faster model refreshes and better-fit features for Japanese living conditions. In April 2026, Hitachi and Nojima announced plans to establish a new company to strengthen Hitachi-branded home appliance operations, which points to a channel-and-service driven approach that can support faster iteration on energy-efficient, smart, and compact laundry platforms while improving customer experience in installation and maintenance workflows.

Recent Industry Developments

- April 2026: Hitachi and Nojima announced plans to establish a new company to strengthen the Hitachi-branded home appliance business and connect retail and service frontlines more tightly with manufacturing capabilities. The plan is intended to support faster product improvement cycles by capturing customer feedback at point of sale and during after-sales support, while reinforcing competitiveness in a replacement-led market.

- May 2025: Haier Japan Sales announced a strategic partnership with a major retailer to expand the DeLAITO line across Japan and broaden after-sales service coverage. The arrangement expands channel access and speeds service responsiveness in urban and suburban markets, reinforcing Haier's position in compact but high-efficiency laundry formats.

- August 2024: Panasonic launched seven drum-type washer-dryer models in Japan, including the NA-LX129DL, featuring a stain removal course developed with Kao Corporation for accumulated sebum stains. Collaboration-led wash programs and fabric-care positioning support premium differentiation beyond basic capacity and energy performance.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Japan laundry appliances market is defined as the value of household and light commercial appliances used to wash, dry, and finish laundry, sold through offline and online channels within Japan.

Scope exclusions: We exclude cleaning chemicals and services, spare parts sold separately, and repair or installation-only revenues.

Segmentation Overview

- By Product Type

- Washing Machines

- Clothes Dryers

- Others(Garment Steamers, Electric Irons, Laundry Dehumidifiers)

- By Technology

- Fully Automatic

- Semi-Automatic /Manual

- By Load Capacity

- Below 6 kg

- 6-8 kg

- Above 8 kg

- By Distribution Channel

- Multi-brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Region

- Kanto

- Kansai

- Chubu

- Rest of Japan

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the outer boundaries for demand and pricing in Japan before we built the model. We relied on public statistics and rulebooks that help explain appliance ownership, housing constraints, and energy-efficiency requirements, since these factors shape replacement cycles and product mix.

Illustrative sources included government and official datasets such as Japan household spending and CPI series, energy-efficiency standards and labeling guidance, customs trade statistics for appliances and components, and broader manufacturing and retail indicators. We also reviewed company annual reports, investor decks, product catalogs, and reputable press coverage for product launches and channel shifts. In addition, we used select paid subscriptions for company financials and structured news, plus an import-export shipment-level dataset and patent databases to validate timing of technology adoption. The sources listed here are not exhaustive, and we consulted additional public and paid references for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions and fill gaps around average selling prices, product mix, and channel margins. We spoke with industry participants including manufacturers, distributors, retailers, aftersales stakeholders, and category specialists across Japan, so the assumptions could be checked from more than one angle.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | |

| Mid tier: 45% | Functional/Unit leaders: 41% | |

| Smaller Players: 21% | Managers: 47% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where the demand pool is reconstructed from appliance ownership and replacement behavior, then translated into yearly unit demand and value. For Japan laundry appliances, inputs such as household counts, urban housing constraints that affect adoption of dryers and compact units, replacement cycles for washers, and efficiency-driven upgrades were used to shape volumes.

Those totals were then corroborated with selective bottom-up checks, including sampled price points by product class, channel mix shifts between specialty stores and online, and supplier and retailer feedback on mix changes (for example, automatic versus semi-automatic, and the share of combo or related finishing devices). Where direct visibility was limited, gaps were handled through conservative interpolation based on adjacent years and category-level indicators, and then adjusted only when interview feedback supported the shift.

For forecasting, scenario analysis was applied around a central case, since demand is mostly replacement-led and sensitive to a few practical drivers. The final outlook was guided by expected shifts in energy-efficiency rules, consumer purchasing power, product premiumization, and the pace of online channel expansion, which were reviewed again with primary respondents to confirm direction and timing.

Data Validation & Update Cycle

Model outputs were checked against independent signals such as import trends, retail pricing movement, and observed product-mix changes, and any large jumps were investigated before sign-off. We also ran variance checks across segments so that no single assumption, such as a sudden ASP increase, could inflate the total without support.

Before finalization, a second analyst review was completed, and follow-up calls were triggered when primary feedback conflicted with desk signals or when a key input moved outside expected ranges. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is performed so clients receive the most current view.

Mordor Intelligence's Japan Laundry Appliances Market Market Size Compared With Other Published Estimates

Different published market sizes for Japan laundry appliances often look inconsistent because each publisher sets its own product boundary, value chain coverage, and timing of the base year. Even when the same words are used in a title, what gets counted as a laundry appliance, and whether the value is at retail or closer to manufacturer revenue, can change the final number.

The gap usually comes from three practical choices, scope and where revenue is captured, how prices are averaged across product types, and how recent updates are applied. Some estimates lean on a narrower set of products or assume a different mix of premium models, while others apply currency timing or inflation handling differently, which can move the USD total even if unit demand is similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.54 B (2026) | |

| Industry Publisher A | USD 2.20 B (2025) | Uses an earlier base year and typically reflects a smaller counted value pool, with a different treatment of product mix and pricing levels across washers, dryers, and finishing devices. |

| Market Analytics Group B | USD 2.16 B (2024) | Anchored to an older demand point and can understate the market if price progression and the shift toward automatic and higher-spec models are not updated in step with recent retail and channel changes. |

The table shows a wide spread mainly because of timing and what is counted inside the market boundary, and in Mordor Intelligence's model the value includes the full set of laundry appliances listed on the report page (including electric smoothing irons and other related devices) within Japan for the stated base year. With the scope and assumptions written into the model, decision-makers can trace the total back to clear demand drivers and repeatable steps, then adjust scenarios if their commercial view differs.

Key Questions Answered in the Report

What is the current size and growth outlook for the Japan laundry appliances market?

The Japan laundry appliances market size is USD 3.54 billion in 2026 and is projected to reach USD 3.92 billion by 2031 at a 2.07% CAGR.

Which product categories are leading and growing fastest in Japan?

Washing machines led with 70.83% of revenue in 2025, while clothes dryers show the fastest growth at a 2.91% CAGR on heat-pump adoption and combo formats.

How do regulations influence purchasing in the Japan laundry appliances market?

METI’s Top Runner standards and Tokyo’s Zero Emission Point rebates push upgrades to efficient models, which shortens replacement cycles in urban regions.

Which technology segment holds the largest share?

Fully automatic machines dominated with 81.93% in 2025 and also carry the highest growth outlook due to convenience, sensors, and connected features.

Which regions contribute most to sales?

Kanto held 35.71% in 2025, and Kansai is the fastest-growing at a 2.43% CAGR, reflecting dense populations and strong adoption of connected and efficient models.

Page last updated on: